Setting up bank information in QuickBooks is a crucial step for efficiently managing your business finances. It allows you to connect your bank accounts, credit cards, and other financial institutions directly to QuickBooks, enabling automatic transaction downloads, seamless reconciliation, and real-time financial tracking. To begin, navigate to the Banking menu in QuickBooks, select Banking or Transactions, and choose the option to Connect Account. You’ll then be prompted to enter your bank’s login credentials to securely link your account. Once connected, QuickBooks will download recent transactions, which you can categorize and match to existing records. Ensure your chart of accounts is properly set up to streamline this process. Regularly reviewing and reconciling these transactions ensures accuracy and helps maintain a clear financial overview. Proper setup not only saves time but also provides valuable insights into your cash flow and financial health.

Explore related products

What You'll Learn

- Add Bank Account Details: Input account number, routing number, and bank name accurately in QuickBooks settings

- Connect Bank Feeds: Link bank accounts to QuickBooks for automatic transaction downloads and reconciliation

- Verify Bank Connection: Ensure secure connection by confirming login credentials and enabling two-factor authentication if required

- Set Up Rules: Create rules to categorize transactions automatically for efficient bookkeeping and reporting

- Reconcile Accounts: Match QuickBooks records with bank statements monthly to ensure accuracy and resolve discrepancies

![]()

Add Bank Account Details: Input account number, routing number, and bank name accurately in QuickBooks settings

Accurate bank account details are the backbone of seamless financial management in QuickBooks. A single misplaced digit in your account number or routing number can lead to failed transactions, delayed payments, or even funds being deposited into the wrong account. This not only disrupts your cash flow but can also damage relationships with vendors and employees.

To avoid these pitfalls, QuickBooks requires three critical pieces of information: your account number, routing number, and bank name. The account number uniquely identifies your specific account within the bank, while the routing number directs transactions to the correct financial institution. The bank name acts as a final verification layer, ensuring everything aligns.

Inputting these details correctly is straightforward but demands attention to detail. Locate your account number and routing number on a check—they’re typically found at the bottom. The account number is usually longer (10–12 digits) and appears second, while the routing number (9 digits) is first. If you’re using a bank statement, these numbers are often listed near the top. Double-check each digit against your source material to avoid transposition errors.

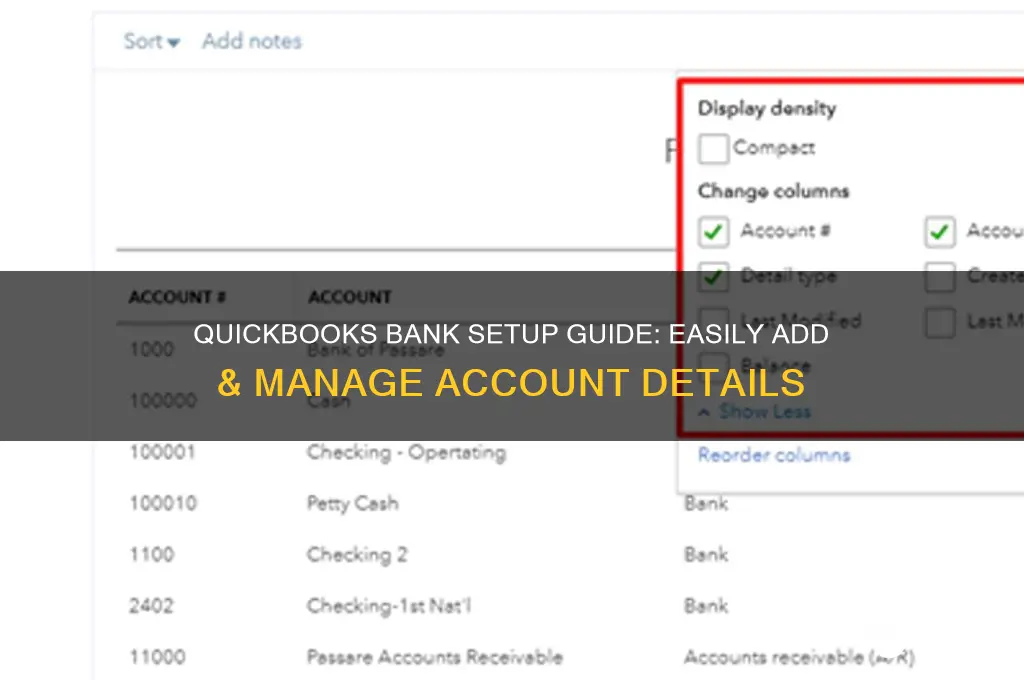

QuickBooks’ interface simplifies this process. Navigate to the "Chart of Accounts" or "Banking" tab, select "Add Account," and choose the appropriate account type (checking, savings, etc.). Enter the details in the designated fields, ensuring the bank name matches exactly as it appears on your statement. QuickBooks often auto-suggests the bank name as you type, reducing the risk of typos.

Pro tip: After inputting the details, QuickBooks may prompt you to connect your account for automatic transaction downloads. This step is optional but highly recommended for real-time financial tracking. If you encounter issues, verify the details with your bank directly—sometimes, special account types (like business accounts) have unique formatting requirements.

By meticulously entering your account number, routing number, and bank name, you lay the foundation for efficient financial management in QuickBooks. This small but crucial step ensures transactions flow smoothly, reports remain accurate, and your business operates without unnecessary financial hiccups.

How to Negotiate Better Interest Rates with Your Bank

You may want to see also

Explore related products

![]()

Connect Bank Feeds: Link bank accounts to QuickBooks for automatic transaction downloads and reconciliation

Linking your bank accounts to QuickBooks through bank feeds revolutionizes how you manage finances by automating transaction downloads and reconciliation. This integration eliminates manual data entry, reduces errors, and ensures your books are always up-to-date. QuickBooks supports over 19,000 financial institutions, making it likely your bank is compatible. Once connected, transactions flow directly into QuickBooks, categorized based on your rules, and flagged for review if needed. This process saves hours each month, allowing you to focus on strategic tasks rather than administrative chores.

To set up bank feeds, start by navigating to the "Banking" menu in QuickBooks and selecting "Bank Feeds." Choose "Set Up Bank Feed" and search for your financial institution. You’ll need your bank login credentials to securely connect the account. QuickBooks uses encryption to protect your data, ensuring a safe transfer of information. After connecting, select the QuickBooks account you want to link to your bank account—ensuring they match (e.g., checking to checking). Once confirmed, QuickBooks begins downloading transactions, typically within 24–48 hours for the initial setup.

While bank feeds streamline reconciliation, they’re not foolproof. Transactions may download with incomplete or incorrect details, requiring manual adjustments. For instance, a vendor name might appear as a generic description like "STORE PURCHASE." To address this, create rules in QuickBooks to automatically categorize recurring transactions. For example, set all transactions from "Amazon" to the "Office Supplies" expense account. Additionally, review downloaded transactions daily or weekly to catch discrepancies early and maintain accuracy.

A common pitfall is neglecting to deactivate old bank feeds when switching accounts or closing them. Inactive accounts with active feeds can clutter your dashboard and lead to confusion. To avoid this, go to the "Chart of Accounts," select the inactive account, and choose "Edit Account." Under the "Bank Feed Settings" tab, click "Disconnect this account." This ensures only active accounts are monitored, keeping your workflow clean and efficient.

In conclusion, connecting bank feeds in QuickBooks is a game-changer for financial management, but it requires proactive oversight. By automating transaction downloads and leveraging categorization rules, you can maintain accurate, real-time records with minimal effort. Regularly review and refine your setup to maximize efficiency and avoid common pitfalls. With this tool, you’ll transform bookkeeping from a tedious task into a seamless part of your business operations.

Calculating Net Sales for Banks: A Comprehensive Step-by-Step Guide

You may want to see also

Explore related products

![]()

Verify Bank Connection: Ensure secure connection by confirming login credentials and enabling two-factor authentication if required

Establishing a secure bank connection in QuickBooks is a critical step that safeguards your financial data. One of the first measures to ensure this security is verifying your bank connection by confirming your login credentials. This process acts as the initial gatekeeper, ensuring that only authorized users can access sensitive banking information. QuickBooks typically prompts you to enter your bank’s username and password during setup. Double-check these details for accuracy, as even a minor typo can disrupt the connection. If your bank uses multi-factor authentication (MFA), QuickBooks will guide you through additional verification steps, such as entering a one-time code sent to your phone or email.

Enabling two-factor authentication (2FA) adds an extra layer of protection to your bank connection. While not all banks require it, enabling 2FA in QuickBooks is a proactive step to prevent unauthorized access. To set this up, navigate to the bank account settings in QuickBooks and look for the security options. If your bank supports 2FA, QuickBooks will prompt you to link your account to a mobile device or email. Once enabled, you’ll receive a unique code each time you attempt to connect, ensuring that even if someone obtains your login credentials, they cannot access your account without the second factor.

A common pitfall during this process is overlooking the importance of keeping login credentials updated. Banks often require periodic password changes or may update their security protocols, which can disrupt your QuickBooks connection. To avoid this, regularly review your bank’s security policies and update your credentials in QuickBooks as needed. Additionally, if you use a password manager, ensure it syncs with QuickBooks to maintain seamless access. Ignoring these updates can lead to connection errors or temporary lockouts, delaying your financial management tasks.

For businesses handling multiple bank accounts, verifying each connection individually is essential. QuickBooks allows you to manage several accounts under one dashboard, but each requires separate verification. Create a checklist to track which accounts have been verified and which need 2FA setup. This organized approach minimizes the risk of overlooking an account and ensures uniform security across all financial data. If you encounter issues during verification, QuickBooks provides troubleshooting guides or customer support to resolve common errors, such as incorrect login details or unsupported bank security features.

Finally, treat the verification process as an ongoing responsibility rather than a one-time task. Regularly monitor your bank connections in QuickBooks to ensure they remain secure and active. Set calendar reminders to review your login credentials and 2FA settings every three to six months. By staying proactive, you not only protect your financial data but also maintain uninterrupted access to critical banking features in QuickBooks. This diligence is particularly vital for businesses, where a compromised bank connection can lead to significant operational and financial disruptions.

Does Nestle Own Banks? Exploring Corporate Financial Ties and Investments

You may want to see also

Explore related products

![QuickBooks Online for Beginners Bible Edition [2 Books in 1]: The Ultimate Fast Learning Guide for QBO, filled with Step-by-Step Illustrated Explanations, Practical Examples and Common Problem Solving](https://m.media-amazon.com/images/I/61WWhskpzAL._AC_UL320_.jpg)

![]()

Set Up Rules: Create rules to categorize transactions automatically for efficient bookkeeping and reporting

Automating transaction categorization in QuickBooks is a game-changer for businesses aiming to streamline their financial processes. By setting up rules, you can ensure that every transaction is accurately classified, reducing manual effort and minimizing errors. This feature is particularly beneficial for businesses with high transaction volumes, where manual categorization can be time-consuming and prone to mistakes. QuickBooks allows you to create custom rules based on criteria such as payee names, transaction descriptions, or amounts, ensuring that each entry is automatically assigned to the correct account or category.

To begin, navigate to the "Banking" menu in QuickBooks and select "Banking Rules." Here, you can create a new rule by specifying the conditions that trigger it. For instance, if you frequently receive payments from a specific client, you can set up a rule that automatically categorizes transactions from that client under "Accounts Receivable." Similarly, recurring expenses like utility bills can be directed to the appropriate expense account. QuickBooks provides a user-friendly interface where you can define these conditions using keywords, amounts, or even specific transaction types, making the process intuitive and efficient.

One of the most powerful aspects of QuickBooks rules is their ability to adapt to your business’s unique needs. For example, you can create rules that handle split transactions, where a single entry is divided between multiple categories. This is particularly useful for transactions like office supply purchases that may include both taxable and non-taxable items. By setting up a rule that recognizes such transactions and splits them accordingly, you can maintain accurate records without manual intervention. Additionally, QuickBooks allows you to prioritize rules, ensuring that the most specific conditions are applied first, preventing conflicts and ensuring precision.

While setting up rules, it’s crucial to test and refine them to ensure they work as intended. QuickBooks provides a "Test Rule" feature that allows you to apply a rule to existing transactions to see how it performs. This step is essential for catching any oversights or errors before the rule is applied to new transactions. Regularly reviewing and updating your rules is also important, especially as your business evolves and new types of transactions emerge. By staying proactive, you can maintain a robust system that keeps your books accurate and up-to-date.

In conclusion, creating rules in QuickBooks to automate transaction categorization is a strategic move toward efficient bookkeeping and reporting. It not only saves time but also enhances the accuracy of your financial records, providing a clearer picture of your business’s financial health. By leveraging this feature, you can focus on strategic decision-making rather than getting bogged down by repetitive data entry tasks. Whether you’re a small business owner or part of a larger organization, mastering this functionality in QuickBooks can significantly improve your financial management processes.

Step-by-Step Guide to Activating IndusInd Net Banking Easily

You may want to see also

Explore related products

![]()

Reconcile Accounts: Match QuickBooks records with bank statements monthly to ensure accuracy and resolve discrepancies

Monthly reconciliation is the linchpin of accurate financial reporting in QuickBooks. It’s not just a best practice—it’s a necessity. By systematically comparing your QuickBooks records to your bank statements, you catch errors, identify fraudulent activity, and ensure every transaction is accounted for. Think of it as a financial health check-up, one that prevents small discrepancies from snowballing into major headaches. Without this step, your books may reflect a rosier (or bleaker) picture than reality, leading to misguided decisions.

To reconcile effectively, start by setting aside dedicated time each month—ideally within a week of receiving your bank statement. In QuickBooks, navigate to the *Banking* menu and select *Reconcile*. Enter the ending balance and date from your statement, then meticulously compare each transaction. QuickBooks will flag unmatched entries, prompting you to investigate. Common culprits include uncleared checks, bank fees, or data entry errors. For instance, a $500 deposit recorded as $50 in QuickBooks can throw off your entire balance. Use the *Find Discrepancies* tool to locate and correct such mistakes.

A critical yet often overlooked aspect is handling uncleared transactions. If a check hasn’t cleared or a deposit hasn’t posted, mark it as *Cleared* only when it appears on your statement. This ensures your QuickBooks balance mirrors your actual bank balance. Additionally, leverage QuickBooks’ *Reconciliation Discrepancy Report* to track unresolved issues. For example, if a $200 expense is missing, cross-reference receipts or invoices to locate the oversight. Over time, this process sharpens your attention to detail and reduces recurring errors.

While QuickBooks simplifies reconciliation, human error remains a wildcard. Double-check entries, especially those involving decimals or large sums. For businesses with multiple accounts, create a reconciliation checklist to ensure consistency. For instance, a small business owner might reconcile their operating account, payroll account, and credit card account in sequence, using a spreadsheet to log progress. This structured approach minimizes oversight and saves time.

Finally, treat reconciliation as an opportunity to refine your financial processes. If discrepancies persist—say, recurring bank fees or frequent data entry errors—dig deeper. Are employees misclassifying expenses? Is your bank charging unnecessary fees? Addressing root causes not only ensures accuracy but also optimizes your financial operations. Remember, reconciliation isn’t just about matching numbers—it’s about maintaining the integrity of your financial data. Done consistently, it transforms QuickBooks from a record-keeping tool into a powerful ally for informed decision-making.

Master Hang Seng e-Banking: A Step-by-Step Application Guide

You may want to see also

Frequently asked questions

To add a bank account in QuickBooks, go to the Chart of Accounts, click New, select Bank as the account type, enter the account details (name, description, and balance), and save. Alternatively, use the Banking menu, select Add Account, and follow the prompts to connect your bank or manually enter details.

Go to the Banking menu, select Add Account, and search for your bank. Log in with your bank credentials to securely connect. QuickBooks will automatically download transactions, which you can review, categorize, and add to your records.

If your bank isn’t listed, you can manually enter transactions. Go to the Banking menu, select Add Account, choose Manual Account Setup, and enter your bank details. Then, upload statements or manually record transactions as needed.

![Quicken Classic Deluxe for New Subscribers| 1 Year [PC/Mac Online Code]](https://m.media-amazon.com/images/I/61ypcFpjCuL._AC_UL320_.jpg)