Starting a mobile banking business requires a strategic approach that combines technological innovation, regulatory compliance, and a deep understanding of customer needs. Aspiring entrepreneurs must first conduct thorough market research to identify gaps in existing financial services and define their target audience. Securing the necessary licenses and partnerships with established banks or financial institutions is crucial to ensure legitimacy and trust. Investing in robust, secure, and user-friendly technology platforms is essential, as mobile banking relies heavily on seamless digital experiences. Additionally, developing a clear business model, focusing on revenue streams such as transaction fees or subscription services, and implementing strong cybersecurity measures to protect user data are vital steps. Finally, effective marketing strategies and customer education initiatives will help build awareness and adoption, positioning the mobile banking business for long-term success in a competitive financial landscape.

Explore related products

What You'll Learn

- Market Research: Identify target demographics, competitors, and regulatory requirements for mobile banking services

- Technology Stack: Choose secure, scalable platforms and integrate payment gateways for seamless transactions

- Regulatory Compliance: Obtain necessary licenses, adhere to financial laws, and ensure data protection standards

- Partnerships: Collaborate with banks, telecoms, and fintech firms to enhance service offerings and reach

- Marketing Strategy: Develop user-friendly apps, launch campaigns, and offer incentives to attract customers

![]()

Market Research: Identify target demographics, competitors, and regulatory requirements for mobile banking services

Understanding your target audience is the cornerstone of any successful mobile banking venture. Demographic research reveals that millennials and Gen Z, aged 18–40, are the primary adopters of digital banking, valuing convenience, speed, and accessibility. However, don’t overlook older generations; a 2022 study showed that 40% of individuals over 55 now use mobile banking, driven by user-friendly interfaces and security features. Tailor your services to these groups by offering intuitive apps, educational resources, and multilingual support to bridge the digital divide.

Competitive analysis is your next critical step. Identify direct competitors like Chime, Revolut, and traditional banks with robust mobile platforms. Analyze their fee structures, feature sets, and customer reviews to uncover gaps in the market. For instance, while many apps offer budgeting tools, fewer provide personalized financial coaching or micro-investment options. Position your service as a solution to unmet needs, such as catering to freelancers with irregular income or students seeking credit-building tools.

Regulatory compliance is non-negotiable in the financial sector. Research local and international laws governing mobile banking, such as GDPR for data protection in Europe or the Electronic Fund Transfer Act in the U.S. Partner with legal experts to ensure compliance with anti-money laundering (AML) regulations and obtain necessary licenses, such as a banking charter or e-money institution authorization. Failure to meet these requirements can result in hefty fines or business shutdowns, so treat this step as an investment, not an expense.

A practical tip for integrating these findings: create user personas based on your demographic research, then map competitor features against these personas to identify opportunities. For example, a persona of a 28-year-old freelancer might prioritize fee-free international transfers and tax-tracking tools—features rarely bundled together. Use regulatory insights to build trust by prominently displaying compliance certifications on your platform and marketing materials. This three-pronged approach ensures your mobile banking service is not only viable but also uniquely positioned to thrive.

Does Synchrony Bank Offer Two-Factor Authentication for Enhanced Security?

You may want to see also

Explore related products

![]()

Technology Stack: Choose secure, scalable platforms and integrate payment gateways for seamless transactions

Selecting the right technology stack is the backbone of any mobile banking business, determining not only its security but also its ability to scale and deliver a seamless user experience. Start by prioritizing platforms that comply with financial industry standards such as PCI DSS (Payment Card Industry Data Security Standard) and GDPR (General Data Protection Regulation). These frameworks ensure that sensitive customer data is protected against breaches and unauthorized access. For instance, leveraging cloud-based solutions like AWS or Google Cloud can provide robust security features, including encryption, firewalls, and intrusion detection systems, while offering the flexibility to scale as your user base grows.

Next, focus on integrating payment gateways that support multiple transaction types, currencies, and payment methods. Popular options like Stripe, PayPal, or Braintree offer APIs that seamlessly integrate with mobile applications, enabling features like instant transfers, recurring payments, and fraud detection. When evaluating gateways, consider their transaction fees, processing speed, and compatibility with your target market’s preferred payment methods. For example, if your business targets users in Southeast Asia, ensure compatibility with local e-wallets like GrabPay or GoPay.

Scalability should be a non-negotiable criterion when choosing your technology stack. Mobile banking platforms must handle sudden spikes in user activity without compromising performance. Microservices architecture, where the application is broken into smaller, independent services, allows for easier maintenance and scaling of specific functionalities as needed. Kubernetes, an open-source container orchestration system, can automate the deployment, scaling, and management of these services, ensuring your platform remains responsive even during peak usage times.

Finally, prioritize user experience by ensuring that your technology stack supports real-time transaction processing and minimal downtime. Implement monitoring tools like Prometheus or New Relic to track system performance and identify bottlenecks before they impact users. Additionally, adopt a DevOps culture to streamline collaboration between development and operations teams, enabling faster updates and issue resolution. By combining secure, scalable platforms with well-integrated payment gateways, you can build a mobile banking solution that not only meets regulatory requirements but also exceeds customer expectations.

How Often Does Mint Sync with Your Bank: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Regulatory Compliance: Obtain necessary licenses, adhere to financial laws, and ensure data protection standards

Navigating the regulatory landscape is the bedrock of launching a mobile banking business. Before writing a single line of code or designing a user interface, you must secure the necessary licenses. These vary by jurisdiction but typically include a banking license, money transmitter license, or e-money institution authorization. For instance, in the U.S., you’ll need approval from the Office of the Comptroller of the Currency (OCC) or state regulators, while in the EU, compliance with the Payment Services Directive 2 (PSD2) is mandatory. Research local requirements meticulously, as failure to obtain the correct licenses can result in hefty fines or business shutdowns.

Adhering to financial laws is not just a legal obligation—it’s a trust-building measure. Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations are non-negotiable. Implement robust identity verification processes, such as biometric authentication or document scanning, to ensure compliance. For example, using AI-powered tools can streamline KYC checks while reducing errors. Additionally, monitor transactions for suspicious activity and report them to relevant authorities. Ignoring these laws can lead to reputational damage and legal consequences, undermining your business before it even takes off.

Data protection is the linchpin of customer trust in mobile banking. With sensitive financial information at stake, compliance with standards like GDPR in Europe or the California Consumer Privacy Act (CCPA) in the U.S. is critical. Encrypt data both in transit and at rest, and conduct regular security audits to identify vulnerabilities. A practical tip: adopt a zero-trust architecture, where access is granted on a need-to-know basis, minimizing the risk of breaches. Remember, a single data leak can erode years of brand-building efforts.

Balancing innovation with compliance requires a proactive approach. Stay updated on evolving regulations by subscribing to financial regulatory newsletters or hiring a compliance officer. Engage with industry associations to understand best practices and emerging trends. For instance, as central bank digital currencies (CBDCs) gain traction, ensure your platform is adaptable to new regulatory frameworks. Finally, document every compliance step—audits and regulators will scrutinize your processes, and thorough records can be your strongest defense.

How Long Does Plaid Bank Verification Take? A Quick Guide

You may want to see also

Explore related products

![]()

Partnerships: Collaborate with banks, telecoms, and fintech firms to enhance service offerings and reach

Partnerships are the backbone of a successful mobile banking business, transforming isolated services into a robust, interconnected ecosystem. By collaborating with banks, telecoms, and fintech firms, you can amplify your service offerings, expand your customer reach, and create a seamless user experience. Banks bring regulatory compliance and financial infrastructure, telecoms provide network access and customer bases, while fintech firms offer innovative technologies and agile solutions. Together, these partnerships form a trifecta that can propel your mobile banking venture into a competitive market.

Consider the strategic steps involved in forging these alliances. Begin by identifying potential partners whose strengths complement your weaknesses. For instance, if your fintech startup lacks a banking license, partnering with a traditional bank can provide the necessary regulatory framework. Conversely, banks can leverage fintech partnerships to modernize their services without hefty investments in R&D. Telecoms, with their vast subscriber networks, can act as distribution channels, enabling you to reach underserved or unbanked populations. Negotiate win-win agreements that align incentives, such as revenue-sharing models or joint marketing campaigns, to ensure long-term collaboration.

A cautionary note: partnerships require careful management to avoid conflicts and misalignments. Clearly define roles, responsibilities, and expectations from the outset. Establish governance structures, such as joint steering committees, to resolve disputes and monitor progress. Additionally, safeguard your intellectual property and customer data through robust legal agreements. A poorly managed partnership can dilute your brand, compromise service quality, or even lead to regulatory penalties. Diligence in due diligence and ongoing communication are non-negotiable.

To illustrate, examine the success of M-Pesa, a mobile money service that revolutionized banking in Kenya. By partnering with Safaricom (a telecom) and local banks, M-Pesa created a network that allowed users to send, receive, and store money via mobile phones. This collaboration not only expanded financial inclusion but also generated significant revenue for all parties involved. The key takeaway? Partnerships are not just about scaling; they’re about creating value for customers and stakeholders alike.

In conclusion, partnerships are not optional—they are essential for launching and scaling a mobile banking business. By strategically aligning with banks, telecoms, and fintech firms, you can overcome resource constraints, navigate regulatory hurdles, and tap into new markets. Approach these collaborations with clarity, caution, and a focus on shared value. Done right, partnerships can turn your mobile banking venture into a powerhouse of innovation and accessibility.

GST on Bank Fees: What You Need to Know

You may want to see also

Explore related products

![]()

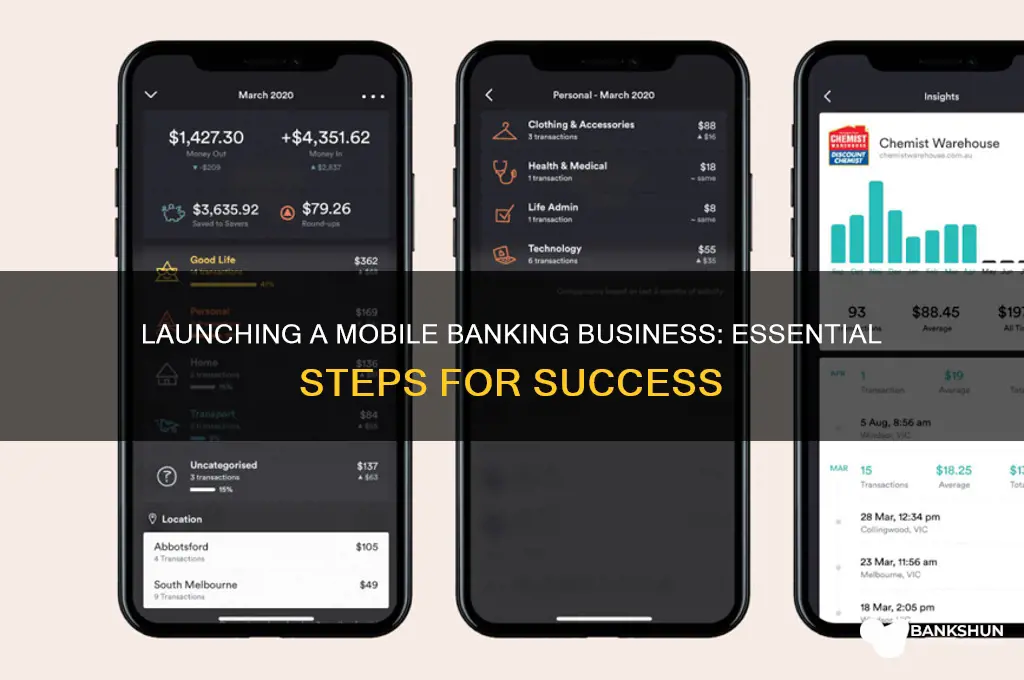

Marketing Strategy: Develop user-friendly apps, launch campaigns, and offer incentives to attract customers

A seamless user experience is the cornerstone of any successful mobile banking app. Customers demand intuitive interfaces, fast loading times, and robust security features. To achieve this, prioritize a clean, minimalist design with clear navigation and easily accessible core functions like balance checks, transfers, and bill payments. Incorporate biometric authentication (fingerprint, facial recognition) and two-factor authentication for added security. Regularly gather user feedback through in-app surveys and analytics to identify pain points and iterate on the design. Remember, a frustrated user is a lost customer.

A well-executed marketing campaign can generate buzz and drive downloads. Leverage social media platforms like Instagram and TikTok to showcase your app's features through engaging videos and influencer partnerships. Targeted ads on Google and Facebook can reach specific demographics, highlighting unique selling points like low fees or high-interest savings accounts. Don't underestimate the power of referral programs – incentivize existing users to invite friends with bonuses or cashback rewards.

Incentives are a powerful tool to attract new users and encourage engagement. Offer sign-up bonuses, such as a cash reward or waived fees for the first month. Implement a loyalty program that rewards users for frequent transactions or maintaining a minimum balance. Consider partnering with local businesses to offer exclusive discounts or cashback when using your app for purchases. However, ensure your incentives are sustainable and aligned with your long-term business goals. Avoid short-term gimmicks that may attract the wrong audience or lead to financial strain.

The key to a successful marketing strategy lies in understanding your target audience. Are you targeting tech-savvy millennials, financially conservative seniors, or underbanked populations? Tailor your app design, campaign messaging, and incentive structures to resonate with their specific needs and preferences. Conduct thorough market research, analyze competitor offerings, and continuously monitor user behavior to refine your approach. By combining a user-centric app, strategic campaigns, and targeted incentives, you can effectively attract and retain customers in the competitive mobile banking landscape.

Mastering Checkbook Balancing: Strategies to Avoid Costly Bank Fees

You may want to see also

Frequently asked questions

Regulatory requirements vary by country but typically include obtaining a banking license, complying with anti-money laundering (AML) and know-your-customer (KYC) regulations, and adhering to data protection laws like GDPR. Partnering with legal experts to navigate local financial regulations is essential.

The initial capital requirement depends on factors like technology development, licensing fees, and operational costs. Estimates range from $500,000 to several million dollars. Securing funding through investors, loans, or partnerships is often necessary.

Core requirements include a secure, scalable mobile app, robust backend systems for transaction processing, encryption for data security, and integration with payment gateways and banking networks. Cloud-based solutions are often preferred for flexibility and cost-efficiency.

Implement multi-factor authentication, end-to-end encryption, and regular security audits. Educate customers on safe banking practices and provide transparent privacy policies. Building a strong reputation through reliable services and responsive customer support is also critical.