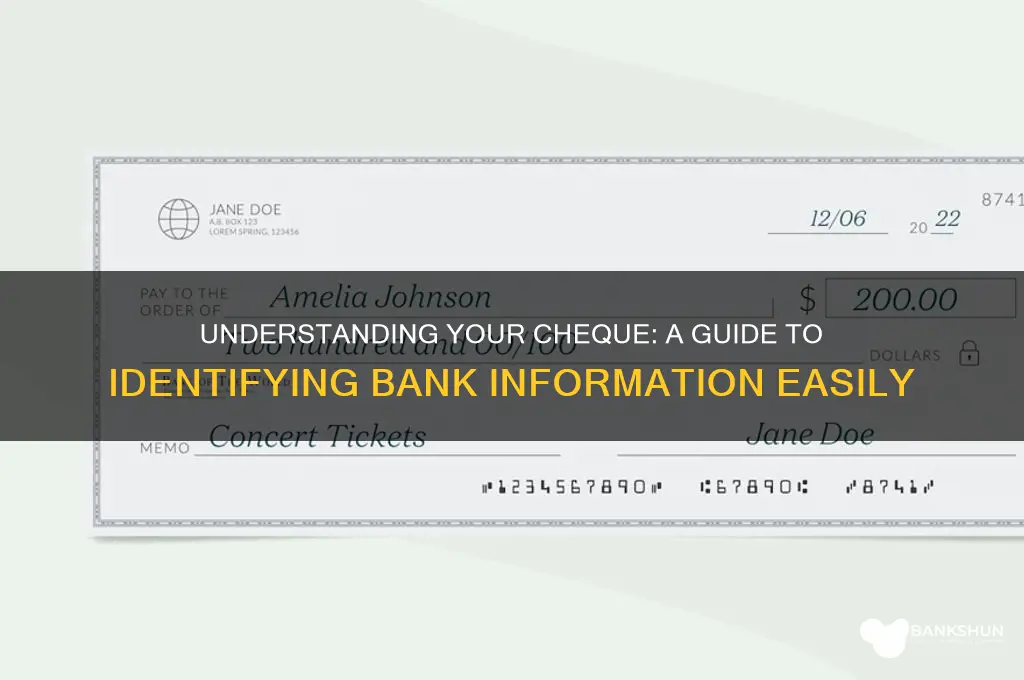

Understanding how to extract bank information from a cheque is essential for anyone managing personal or business finances. A cheque typically contains critical details such as the account holder’s name, bank name, branch address, account number, and routing or transit number, which are crucial for transactions like deposits, transfers, or setting up direct payments. By familiarizing yourself with the layout of a cheque, you can easily identify these key elements, ensuring accuracy and security in your financial dealings. This knowledge not only simplifies banking processes but also helps prevent errors or fraud by verifying the legitimacy of the information provided.

Explore related products

What You'll Learn

- Cheque Layout Basics: Understand the standard sections and their placement on a cheque for easy identification

- Bank Name Location: Spot the bank’s name, usually printed prominently at the top of the cheque

- Routing Number Explained: Locate and decode the routing number, which identifies the bank and branch

- Account Number Details: Identify the unique account number, typically found at the bottom of the cheque

- MICR Line Importance: Recognize the Magnetic Ink Character Recognition (MICR) line for bank info verification

![]()

Cheque Layout Basics: Understand the standard sections and their placement on a cheque for easy identification

A cheque's layout is a carefully designed blueprint, ensuring secure and accurate financial transactions. At first glance, it may appear as a simple slip of paper, but each section serves a distinct purpose. Understanding this layout is crucial for anyone handling cheques, from personal finance management to business accounting. Let's unravel the standard components and their strategic placement.

The Top Right Corner: A Bank's Signature

Imagine a cheque as a canvas, and the top right corner is where the bank's identity is boldly stamped. Here, you'll find the bank's logo, a visual marker of authenticity. Accompanying this is the bank's name and often a branch identifier, ensuring you know exactly which financial institution is involved. This section is like a signature, a unique mark that distinguishes one bank from another. For instance, a quick glance at this area can reveal whether the cheque is from a local credit union or a national bank, each with its own distinct branding.

Account and Routing Numbers: The Numerical Code

Below the bank's logo, a series of numbers takes center stage. These are not random; they are the account and routing numbers, the cheque's unique identifiers. The account number, typically longer, is specific to the account holder, while the routing number (or sort code) directs the transaction to the correct bank and branch. These numbers are the cheque's DNA, providing essential information for processing. For instance, in the US, the routing number is a 9-digit code, while in the UK, it's a 6-digit sort code, both serving the same critical function.

Date and Payee Line: Directing the Funds

Moving downwards, the left side of the cheque introduces the date line, a simple yet vital element. This is where the cheque writer specifies the transaction date, ensuring the payment's timeliness. Adjacent to it is the payee line, a critical field where the recipient's name is written. This section is where the purpose of the cheque becomes clear—who is receiving the funds and when. For instance, a cheque for rent might have "Landlord Co." written here, immediately indicating the payment's intent.

Amount Fields: Dual Representation

The centre of the cheque features two amount fields, a numerical and a written one. The numerical field is straightforward, requiring the amount in digits. However, the written field demands a more descriptive approach, spelling out the amount in words. This dual representation is a security measure, making it harder to alter the cheque's value. For example, "$1,000.00" would be written as "One Thousand and 00/100" in the adjacent field, providing a clear and secure instruction for payment.

Signature Strip: The Final Authorization

The bottom right corner is reserved for the cheque writer's signature, a personal mark of approval. This signature strip is a critical security feature, ensuring the cheque's authenticity and the account holder's consent. Without this signature, the cheque is considered invalid. It's a simple yet powerful element, transforming a piece of paper into a legally binding financial instrument.

In summary, a cheque's layout is a meticulously organized system, where each section plays a unique role in facilitating secure transactions. From the bank's branding to the account holder's signature, every element is strategically placed to provide essential information and ensure the cheque's integrity. Understanding this layout empowers individuals to navigate the world of cheques with confidence, whether for personal or business use.

Exploring Bank United's Network: Total Number of Branches Revealed

You may want to see also

Explore related products

![]()

Bank Name Location: Spot the bank’s name, usually printed prominently at the top of the cheque

The bank's name is often the most prominent feature on a cheque, serving as a beacon for anyone trying to identify the financial institution. Typically, it is emblazoned across the top, either centered or aligned to the left, in bold, clear lettering. This placement is no accident—it ensures that the bank’s identity is immediately recognizable, even at a glance. For instance, on a cheque from Chase Bank, the name "Chase" is usually displayed in large, capitalized letters, often accompanied by the bank’s logo. This strategic positioning is a universal design standard, making it the first place to look when deciphering bank information.

Analyzing this design choice reveals its practicality. By placing the bank’s name at the top, cheque designers prioritize clarity and efficiency. This is especially useful in financial transactions, where accuracy is critical. For example, if you’re verifying a cheque’s legitimacy, the bank name acts as a quick reference point. It also aligns with cognitive processing—our eyes naturally scan from top to bottom, so placing the most important information first reduces the risk of error. This layout is consistent across most cheques, regardless of the bank or country, making it a reliable starting point.

To spot the bank name effectively, follow these steps: first, hold the cheque horizontally and focus on the uppermost area. Ignore any decorative elements or borders, as the name is usually set apart in a distinct font or color. If the cheque includes a logo, it often appears alongside or within the bank name, providing additional confirmation. For example, Bank of America cheques feature the name in bold, blue letters, with the logo integrated seamlessly. If the name is unclear or partially obscured, compare it with known examples or use a magnifying tool for better visibility.

While the bank name’s location is generally consistent, there are exceptions. Some cheques, particularly older or custom-designed ones, may place the name in less conventional spots, such as the upper right corner or even the middle. In such cases, scanning the entire cheque systematically is essential. Additionally, be cautious of fraudulent cheques, where the bank name might be misspelled or poorly replicated. Always cross-reference the name with other details, like the routing number or branch address, to ensure authenticity.

In conclusion, the bank name’s prominent placement at the top of a cheque is a deliberate and functional design choice. It simplifies identification and reduces errors in financial transactions. By understanding this layout and following a systematic approach, you can quickly and accurately extract the bank’s identity. Whether you’re processing payments, verifying documents, or simply curious, this knowledge is a practical tool in navigating the world of cheques.

Step-by-Step Guide to Adding Bank Details in Your EPFO Account

You may want to see also

Explore related products

![]()

Routing Number Explained: Locate and decode the routing number, which identifies the bank and branch

A cheque is a treasure map for financial details, and the routing number is your X marks the spot. This nine-digit code, typically found at the bottom left corner of a cheque, is the key to identifying the bank and branch associated with the account. It’s not just a random string of numbers; it’s a structured system designed to streamline transactions. The first four digits represent the bank’s Federal Reserve routing symbol, the next four identify the specific branch or processing center, and the last digit is a checksum to ensure accuracy. Understanding this structure allows you to decode the routing number with precision, turning a cryptic sequence into actionable information.

Locating the routing number is straightforward once you know where to look. On a cheque, it’s the first set of numbers printed on the MICR (Magnetic Ink Character Recognition) line at the bottom, positioned to the left of the account number. For digital banking users, this number can also be found in online banking portals, mobile apps, or by contacting the bank directly. A practical tip: if you’re using a cheque from a book, ensure it’s the most recent one, as routing numbers can change if a bank undergoes mergers or restructuring. Always double-check the number against official bank documents to avoid errors in transactions.

Decoding the routing number reveals more than just the bank’s identity; it provides insights into the institution’s geographic location and operational scope. For instance, routing numbers beginning with “01” through “12” are typically assigned to banks in the northeastern U.S., while those starting with “11” or “12” often indicate banks in the New York or Chicago regions. This regional coding helps financial systems route transactions efficiently. Additionally, the branch identifier within the routing number can distinguish between branches of the same bank, ensuring funds are directed to the correct location. This level of specificity is crucial for both domestic and international transactions.

While the routing number is essential for direct deposits, wire transfers, and automatic payments, it’s not the only piece of information needed. It works in tandem with the account number and, in some cases, the SWIFT code for international transactions. A common mistake is confusing the routing number with the account number or the cheque number, which are adjacent on the MICR line. To avoid this, remember the routing number is always nine digits and appears first. For added security, never share your routing number unless it’s for a legitimate financial transaction, as it can be misused for fraudulent activities like unauthorized withdrawals.

In conclusion, the routing number is more than a sequence of digits—it’s a critical component of the financial ecosystem. By understanding its structure, location, and significance, you can navigate banking transactions with confidence. Whether you’re setting up direct deposits, transferring funds, or verifying account details, the routing number serves as your compass in the complex world of finance. Treat it with care, and it will guide you to your financial destination seamlessly.

Access Family Bank Mobile Banking: A Step-by-Step Guide for Users

You may want to see also

Explore related products

![]()

Account Number Details: Identify the unique account number, typically found at the bottom of the cheque

The account number is a critical piece of information on a cheque, serving as a direct link to the specific bank account associated with the transaction. Typically located at the bottom of the cheque, this number is part of the Magnetic Ink Character Recognition (MICR) line, which also includes the routing number and the cheque number. The account number is usually 7 to 12 digits long, though this can vary by bank and country. Identifying it correctly is essential for tasks like setting up direct deposits, automatic payments, or verifying transactions.

To locate the account number, start by examining the bottom left corner of the cheque. The MICR line is printed in a special font using magnetic ink, making it machine-readable. The account number is the second set of digits in this line, positioned between the routing number (which identifies the bank) and the cheque number (which identifies the individual cheque). For example, in the MICR line `123456789⏺️0987654321⏺️101`, `0987654321` would be the account number. If you’re unsure, compare it with the account number listed on your bank statement or online banking portal to confirm accuracy.

One common mistake is confusing the account number with the routing number or cheque number. To avoid this, remember the order: routing number (first), account number (second), and cheque number (third). Some banks may include additional symbols or spacing in the MICR line, but the account number remains distinct. If the cheque design includes a separate box or label for the account number, use that as a secondary reference. Always double-check the digits, as transposing numbers can lead to errors in financial transactions.

For those handling cheques in a professional setting, such as accounting or payroll, it’s crucial to standardize the process of identifying account numbers. Create a checklist that includes verifying the MICR line, cross-referencing with other documents, and confirming the account type (e.g., personal, business, savings). Additionally, educate clients or colleagues on how to locate their account number to streamline processes like direct deposit setup. In digital banking, account numbers are often required for online transfers, making this knowledge universally applicable.

In summary, the account number on a cheque is a unique identifier found in the MICR line at the bottom. Its correct identification ensures seamless financial transactions and prevents errors. By understanding its position, format, and importance, individuals and professionals can navigate cheque-related tasks with confidence. Always verify the number against other sources and stay vigilant to avoid mistakes that could impact financial operations.

Creative Ways to Repair and Restore Your Broken Piggy Bank

You may want to see also

Explore related products

![]()

MICR Line Importance: Recognize the Magnetic Ink Character Recognition (MICR) line for bank info verification

The MICR line, a sequence of numbers and symbols at the bottom of a cheque, is not just a random assortment of characters. It’s a critical security feature encoded in magnetic ink, designed to be read by machines with precision. This line contains three key pieces of information: the bank’s routing number, the account number, and the cheque number. Understanding its structure is the first step in verifying bank details accurately. For instance, the routing number (usually 9 digits in the U.S.) identifies the bank, while the account number links to the specific account holder.

Analyzing the MICR line reveals its dual purpose: efficiency and fraud prevention. Unlike standard printing, magnetic ink ensures that machines can read the data even if the cheque is damaged or soiled. This reliability speeds up transaction processing, reducing errors in automated systems. Simultaneously, the specialized ink and encoding format make it difficult for fraudsters to replicate, as standard printers cannot reproduce MICR-encoded characters. Banks and financial institutions rely on this technology to verify cheque authenticity swiftly.

To recognize the MICR line effectively, look for its distinct appearance: a series of numbers and symbols printed in a uniform, machine-readable font, typically at the bottom left of the cheque. The characters are often darker and thicker than other printed text, with a slight sheen under certain lighting. A practical tip is to compare the MICR line with the pre-printed account and routing numbers elsewhere on the cheque. Discrepancies could indicate tampering or forgery, warranting further scrutiny.

While the MICR line is a cornerstone of cheque verification, it’s not infallible. Advances in printing technology have made it easier for sophisticated fraudsters to mimic magnetic ink. Therefore, relying solely on visual inspection is risky. Financial institutions use MICR readers to validate the magnetic properties of the ink, ensuring the data is genuine. For individuals, cross-referencing MICR details with digital banking records or contacting the bank directly provides an additional layer of verification.

In conclusion, the MICR line is a powerful tool for bank info verification, blending technology and security to safeguard financial transactions. Its unique encoding and magnetic properties make it a reliable identifier of cheque details. However, awareness of its limitations and complementary verification methods ensures its effectiveness in an evolving landscape of financial fraud. Recognizing and understanding the MICR line is not just a technical skill—it’s a practical safeguard for anyone handling cheques.

How Banks Verify and Validate Your Transactions: A Comprehensive Guide

You may want to see also

Frequently asked questions

The bank name is usually printed at the top of the cheque, often in a prominent position, and may also be accompanied by the bank's logo.

The account number is typically located at the bottom of the cheque, printed in MICR (Magnetic Ink Character Recognition) font. It is a series of numbers, often preceded by a symbol or a short code.

The routing or transit number is a unique code that identifies the bank and the branch where the account is held. It is usually found at the bottom left corner of the cheque, also printed in MICR font, and is typically 9 digits long.

In some cases, the type of account may be indicated on the cheque, often near the account number or in the memo line. However, this is not always the case, and you may need to contact the bank or account holder to confirm the account type.

To verify the authenticity of bank information, you can contact the bank directly using the customer service number provided on their official website. Do not use any contact information printed on the cheque itself, as it may be fraudulent. Additionally, you can use online cheque verification services or consult with a financial institution to confirm the validity of the cheque and the associated bank information.