Understanding your bank's billing cycle is crucial for managing your finances effectively, as it determines when transactions are posted, interest is accrued, and payments are due. A billing cycle typically refers to the period between two consecutive statements, usually lasting 25 to 31 days, though this can vary by bank. To identify your specific cycle, review your monthly statement, which often indicates the start and end dates, or log into your online banking account where this information is usually displayed. Knowing your billing cycle helps you optimize payments, avoid late fees, and maximize grace periods, ensuring you stay on top of your financial obligations.

| Characteristics | Values |

|---|---|

| Check Bank Statement | Look for the "Billing Cycle" or "Statement Period" dates on the statement. |

| Online Banking Portal | Log in to your account and navigate to the account summary or statement section. |

| Mobile Banking App | Check the account details or transaction history for billing cycle dates. |

| Contact Customer Service | Call or chat with your bank’s customer service to inquire about the billing cycle. |

| Review Account Terms | Refer to the account agreement or terms and conditions provided by the bank. |

| Monthly Statements | Most banks send monthly statements, which typically align with the billing cycle. |

| Credit Card Accounts | Billing cycles for credit cards are usually 25-30 days, but check for specifics. |

| Debit Card Accounts | Billing cycles may align with monthly statement periods or vary by bank. |

| Frequency of Statements | Statements are usually issued monthly, indicating the billing cycle period. |

| Grace Period | Some accounts have a grace period within the billing cycle for payments. |

| Due Date | The payment due date is often near the end of the billing cycle. |

| Transaction Cutoff Date | Transactions after this date may roll over to the next billing cycle. |

| Account Type | Billing cycles may differ for checking, savings, or credit card accounts. |

| Bank-Specific Policies | Each bank may have unique policies regarding billing cycles. |

| Annual Percentage Rate (APR) | For credit cards, the APR may be tied to the billing cycle. |

| Rewards or Points Calculation | Rewards are often calculated based on the billing cycle for credit cards. |

Explore related products

What You'll Learn

- Understanding Billing Cycle Basics: Learn what a billing cycle is and how it affects your bank account

- Identifying Cycle Start/End Dates: Locate and interpret the start and end dates of your billing cycle

- Checking Bank Statements: Use monthly statements to confirm your billing cycle details accurately

- Contacting Customer Service: Reach out to your bank for direct information on your billing cycle

- Using Online Banking Tools: Access digital banking platforms to view and track your billing cycle

![]()

Understanding Billing Cycle Basics: Learn what a billing cycle is and how it affects your bank account

A billing cycle is the period between two consecutive bank statements, typically ranging from 28 to 31 days, though some institutions use fixed calendars (e.g., the 1st to the last day of each month). Knowing this timeframe is crucial because it dictates when transactions are grouped for billing, affecting interest calculations, payment due dates, and credit utilization ratios. For instance, a purchase made on the first day of a cycle will accrue interest for the entire period if not paid in full by the due date, while one made near the cycle’s end has less time to accumulate interest.

To identify your bank’s billing cycle, start by reviewing your most recent statement. The cycle’s start and end dates are usually listed at the top, often labeled as "Statement Period." If unclear, log into your online banking portal or mobile app, where this information is typically found under the "Account Summary" or "Statements" section. Alternatively, contact customer service directly—they can provide the exact dates and clarify any inconsistencies. Pro tip: Set a recurring calendar alert for the last day of your cycle to ensure timely payments and avoid late fees.

Understanding your billing cycle empowers smarter financial decisions. For example, if you’re carrying a balance, making payments just before the cycle closes reduces the average daily balance used to calculate interest. Conversely, if aiming to maximize rewards or grace periods, time large purchases immediately after the cycle ends to delay interest accrual. This strategic approach can save hundreds annually, especially on high-interest accounts like credit cards.

A common misconception is that billing cycles align with monthly calendars, but this isn’t always true. Some banks use rolling cycles, meaning the start date shifts each month based on account activity. For instance, if your first statement began on the 15th, subsequent cycles will also start mid-month. This can catch users off guard, leading to missed payments or unexpected fees. Always verify your specific cycle pattern to avoid such pitfalls.

Finally, leverage your billing cycle to optimize cash flow. If your income aligns poorly with payment due dates, request a cycle change from your bank—many institutions accommodate such requests. Additionally, automate payments to ensure they post before the cycle closes, maintaining a positive payment history. By mastering these basics, you’ll not only manage debt more effectively but also align your spending habits with your financial goals.

Smart Strategies to Reduce Your Car Payment with Your Bank

You may want to see also

Explore related products

![]()

Identifying Cycle Start/End Dates: Locate and interpret the start and end dates of your billing cycle

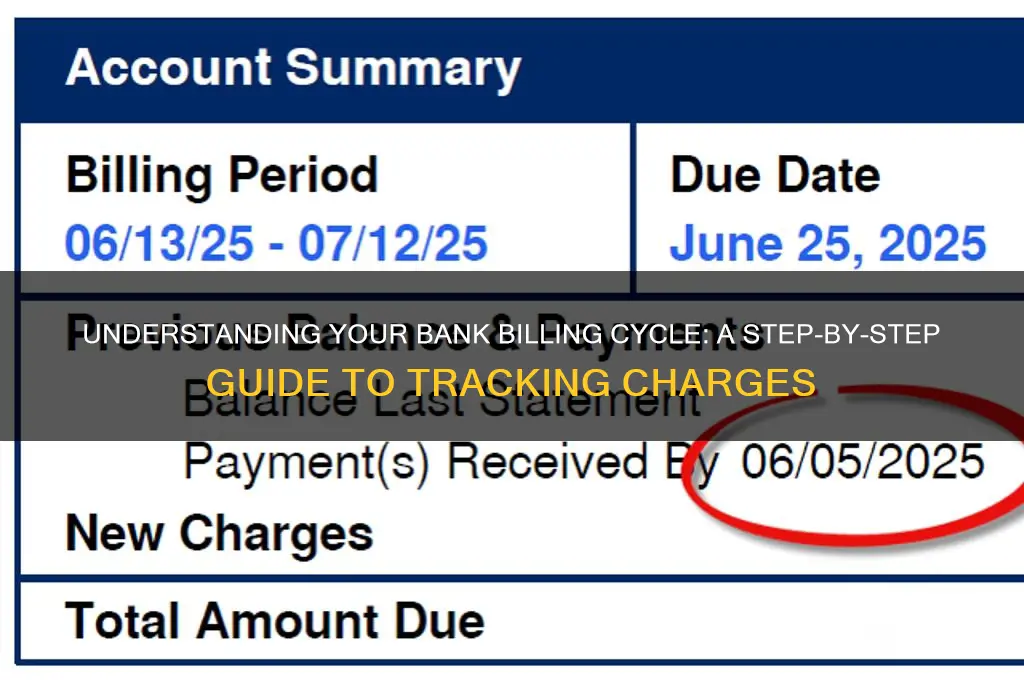

Understanding your bank's billing cycle is akin to deciphering a financial calendar, and pinpointing the start and end dates is the first step in this process. These dates are not arbitrary; they dictate when transactions are grouped for billing, affecting interest calculations and payment due dates. For instance, a credit card billing cycle might begin on the 15th of each month and end on the 14th of the following month, meaning any purchases made on the 16th of one month will appear on the next statement. This knowledge is crucial for managing cash flow and avoiding late fees.

To locate these dates, start by reviewing your most recent bank statement. Most financial institutions clearly label the billing cycle period at the top of the statement, often in a format like "Statement Period: MM/DD/YYYY – MM/DD/YYYY." If this information isn’t immediately visible, log into your online banking portal. Navigate to the account summary or statement section, where the cycle dates are typically displayed alongside transaction details. For mobile banking users, this information is often found under the "Account Details" or "Statements" tab. If all else fails, contact customer service—they can provide the exact dates and explain any nuances specific to your account.

Interpreting these dates requires understanding their impact on your financial habits. For example, if your billing cycle ends on the 5th of each month, any large purchases made on the 6th will roll into the next cycle, potentially delaying interest accrual if you carry a balance. Conversely, paying off your balance a few days before the cycle ends can minimize interest charges. This strategic timing can save you money and improve your credit utilization ratio, a key factor in credit scoring.

A practical tip is to align recurring payments with your billing cycle. If your cycle starts on the 1st, schedule subscriptions or automatic transfers for the same day to ensure they’re included in the current statement. This practice simplifies tracking expenses and helps avoid overdrafts. Additionally, mark these dates on your calendar or set reminders to review transactions before the cycle ends, allowing you to dispute any errors promptly.

In summary, identifying and interpreting your billing cycle start and end dates is a foundational skill for financial management. It empowers you to optimize payments, minimize interest, and maintain a clear overview of your spending. By leveraging this knowledge, you can transform your billing cycle from a passive financial event into an active tool for fiscal responsibility.

How to Stop Payment with Commerce Bank: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Checking Bank Statements: Use monthly statements to confirm your billing cycle details accurately

Your bank statement is a treasure trove of information, and one of its most valuable secrets is your billing cycle. This cycle dictates when your transactions are grouped for billing, affecting interest charges, payment due dates, and overall financial planning. To decipher this crucial detail, simply scrutinize your monthly statements.

Look for a section labeled "Billing Period" or "Statement Period." This clearly outlines the start and end dates of the cycle, revealing when your bank considers transactions for billing. For instance, a statement might indicate a billing period from the 15th of one month to the 14th of the next, meaning any purchases made within this timeframe will be included in that month's bill.

This seemingly simple detail holds significant power. Understanding your billing cycle allows you to strategically time purchases, maximize grace periods for interest-free payments, and avoid late fees. For example, knowing your cycle ends on the 14th, you could schedule a large purchase for the 15th, effectively pushing its billing date to the next cycle and potentially gaining an extra month to pay without accruing interest.

Additionally, analyzing past statements can reveal patterns in your spending habits within each cycle. This awareness can be a powerful tool for budgeting and identifying areas for financial improvement.

While online banking platforms often display billing cycle information, relying solely on digital interfaces can be risky. Technical glitches or updates might temporarily obscure this data. Your monthly statement, a physical or digital document, serves as a reliable and permanent record, ensuring you always have access to this critical information.

Mastering Guild Wars 2: Your Guide to Accessing the Royal Bank

You may want to see also

Explore related products

![]()

Contacting Customer Service: Reach out to your bank for direct information on your billing cycle

One of the most straightforward ways to determine your bank's billing cycle is to contact customer service directly. This method ensures you receive accurate, up-to-date information tailored to your specific account. Most banks offer multiple channels for communication, including phone, email, and live chat, making it convenient to reach out. When calling, have your account number and personal identification details ready to expedite the process. A quick conversation with a representative can clarify not only the billing cycle dates but also any associated fees or policies that may impact your account.

Analyzing the benefits of this approach reveals its efficiency and reliability. Unlike scouring through generic FAQs or deciphering complex statements, speaking directly with a customer service agent provides clarity in real time. For instance, if your billing cycle recently changed due to a policy update, a representative can immediately inform you of the new dates and explain any adjustments to your payment due dates. This direct communication also allows you to ask follow-up questions, such as how holidays or weekends affect billing deadlines, ensuring you have a comprehensive understanding.

However, there are a few cautions to keep in mind when using this method. First, be aware of peak hours when calling customer service, as wait times can be lengthy. Early mornings or late evenings often yield shorter wait times. Second, while most representatives are knowledgeable, occasional errors can occur, so it’s wise to verify the information provided by cross-referencing it with your account statement or online banking portal. Lastly, if you’re using email or live chat, response times may vary, so allow for a day or two for a reply, especially for non-urgent inquiries.

To maximize the effectiveness of this approach, prepare a list of specific questions before reaching out. For example, ask about the exact start and end dates of your billing cycle, how payments are applied during this period, and whether there are any upcoming changes to the cycle. If you’re unsure about certain terms or policies, don’t hesitate to ask for clarification. Additionally, take notes during the conversation or request a follow-up email summarizing the details discussed. This ensures you have a record to refer back to, reducing the likelihood of confusion or missed payments.

In conclusion, contacting customer service is a direct and reliable way to determine your bank’s billing cycle. By leveraging this method, you gain personalized information and the opportunity to address any related concerns. While there are minor drawbacks, such as potential wait times or occasional inaccuracies, the benefits far outweigh these issues. With a bit of preparation and follow-through, this approach empowers you to manage your finances more effectively and stay informed about your account’s billing structure.

Step-by-Step Guide to Adding a Beneficiary in Federal Bank

You may want to see also

Explore related products

![]()

Using Online Banking Tools: Access digital banking platforms to view and track your billing cycle

Online banking platforms are your go-to resource for understanding your bank’s billing cycle. Most banks provide a digital dashboard that clearly displays your statement closing date, payment due date, and transaction history within the current cycle. Log in to your account, navigate to the "Account Summary" or "Statements" section, and look for a calendar or timeline feature that highlights these key dates. This real-time visibility eliminates guesswork and ensures you’re always aligned with your bank’s schedule.

For those who prefer a proactive approach, setting up alerts within your online banking portal can be a game-changer. Many platforms allow you to receive notifications when your billing cycle begins, when your statement is ready, or when your payment is due. These reminders are particularly useful for avoiding late fees and staying on top of your financial obligations. Customize alert preferences to match your communication style—whether via email, text, or in-app notifications—and let technology do the heavy lifting.

A lesser-known but highly effective tool is the transaction categorization feature available on many digital banking platforms. By organizing your purchases into categories like "Groceries," "Utilities," or "Entertainment," you can analyze spending patterns within each billing cycle. This not only helps you budget more effectively but also identifies areas for potential savings. For instance, if you notice a spike in dining out expenses mid-cycle, you can adjust your spending habits before the next statement closes.

While online banking tools offer unparalleled convenience, it’s crucial to cross-reference digital information with physical statements periodically. Occasionally, discrepancies may arise due to pending transactions or system updates. By comparing your online dashboard with mailed or downloadable statements, you ensure accuracy and maintain a comprehensive understanding of your billing cycle. This dual-check method bridges the gap between digital efficiency and traditional reliability.

Maximize Your Earnings: A Guide to State Bank Reward Points

You may want to see also

Frequently asked questions

A bank billing cycle, also known as a statement cycle, is the period of time between two consecutive billing statements. It’s important because it determines when transactions are grouped for your statement, when payments are due, and how interest is calculated on balances.

You can find your bank’s billing cycle by checking your monthly statement, logging into your online banking account, or contacting your bank’s customer service. The start and end dates of the cycle are usually listed on your statement.

Indirectly, yes. Your billing cycle impacts when your credit utilization (the percentage of your credit limit you’re using) is reported to credit bureaus. High utilization at the end of a billing cycle can negatively affect your credit score, so it’s important to manage balances accordingly.