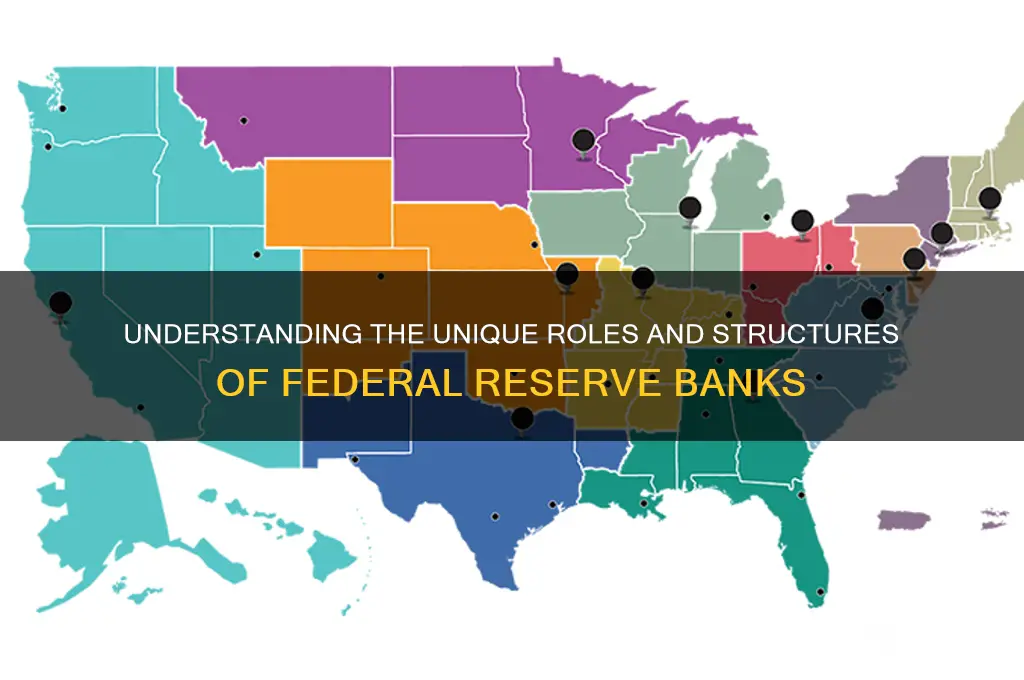

The Federal Reserve System, often referred to as the Fed, is the central banking system of the United States, comprising 12 regional Federal Reserve Banks spread across the country. While these banks share a common purpose of implementing monetary policy, supervising financial institutions, and providing financial services, they differ significantly in their geographic reach, economic focus, and operational nuances. Each Federal Reserve Bank serves a distinct region, known as a Federal Reserve District, and is uniquely attuned to the economic conditions, industries, and challenges specific to its area. For example, the Federal Reserve Bank of New York plays a pivotal role in international finance and monetary policy execution, while the Federal Reserve Bank of Dallas focuses on the energy sector and the economic dynamics of the Southwest. These differences are reflected in their leadership, research priorities, and engagement with local communities, making each bank a tailored institution that addresses the diverse needs of its respective region while contributing to the broader goals of the Federal Reserve System.

| Characteristics | Values |

|---|---|

| Number of Banks | 12 Federal Reserve Banks across the U.S. |

| Geographical Coverage | Each bank serves a specific region (e.g., New York, San Francisco, etc.). |

| Headquarters Locations | Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, San Francisco. |

| Governance Structure | Each bank has a Board of Directors with local representation. |

| Primary Functions | Supervise member banks, provide financial services, and implement monetary policy in their districts. |

| Monetary Policy Role | All banks contribute to monetary policy decisions through the Federal Open Market Committee (FOMC), but the New York Fed plays a unique role in executing open market operations. |

| Banking Supervision | Each bank oversees and regulates banks within its district. |

| Currency Issuance | All banks distribute currency, but the specific notes may vary by region. |

| Economic Research | Each bank conducts regional economic research and publishes reports. |

| Community Engagement | Banks engage with local communities to understand regional economic issues. |

| Size and Influence | The New York Fed is the largest and most influential due to its role in financial markets and international operations. |

| Reserve Requirements | All banks enforce reserve requirements for member banks in their districts. |

| Emergency Lending | Each bank can provide emergency lending to banks in its district under Section 13(3) of the Federal Reserve Act. |

| Payment System Oversight | All banks oversee payment systems and ensure financial stability in their regions. |

| Public Outreach | Banks conduct public outreach and education tailored to their districts. |

| Leadership | Each bank has a President appointed by its Board of Directors. |

| Unique Responsibilities | The New York Fed manages the System Open Market Account (SOMA) and represents the U.S. in international monetary organizations. |

Explore related products

What You'll Learn

- Ownership Structure: Federal Reserve Banks are owned by member banks, not the federal government

- Governance Model: Each bank has a unique board, distinct from the Federal Reserve Board

- Regional Focus: Serve specific regions, tailoring policies to local economic conditions

- Profit Distribution: Excess earnings are returned to the U.S. Treasury, not shareholders

- Operational Autonomy: Operate independently but coordinate under the Federal Reserve System

![]()

Ownership Structure: Federal Reserve Banks are owned by member banks, not the federal government

The Federal Reserve System, often referred to as "the Fed," operates under a unique ownership structure that sets it apart from typical government agencies. Unlike most central banks around the world, the Federal Reserve Banks are not owned by the federal government. Instead, they are owned by their member banks, which are primarily commercial banks in the United States. This ownership model is a cornerstone of the Fed’s independence and governance, ensuring that monetary policy decisions are insulated from direct political influence while maintaining accountability to the banking sector.

To understand this structure, consider the practical mechanics: member banks are required to purchase a specific amount of stock in their district’s Federal Reserve Bank, equivalent to 3% of their capital. For example, if a bank has $100 million in capital, it must invest $3 million in non-transferable Fed stock. This stock does not carry traditional ownership benefits like voting rights in corporate decisions or dividend payouts at market rates. Instead, dividends are capped at 6% annually, and member banks receive only one vote each in electing directors, regardless of their size or investment. This system prevents larger banks from dominating the Fed’s governance while ensuring all members have a stake in its operations.

This ownership structure serves a dual purpose. First, it fosters a sense of shared responsibility among member banks, aligning their interests with the stability of the financial system. Second, it preserves the Fed’s operational independence from the federal government, allowing it to make decisions based on economic data rather than political pressures. However, this independence is not absolute; the Fed is still accountable to Congress, which oversees its activities and can amend its mandate through legislation. This balance between autonomy and accountability is a key differentiator in the Fed’s design.

Critics argue that this ownership model creates a perception of conflict, as the Fed regulates the same banks that own it. To mitigate this, the Fed’s governance includes a mix of appointed and elected directors, with the Board of Governors in Washington, D.C., overseeing the system. Additionally, profits generated by the Fed—after covering expenses and dividends—are returned to the U.S. Treasury, reinforcing its public purpose. This hybrid structure ensures that while member banks have a voice, the Fed’s actions ultimately serve the broader economy.

In practice, this ownership structure influences how the Fed interacts with the banking system. For instance, during financial crises, the Fed’s ability to lend to member banks is both a tool for stabilizing the economy and a reflection of its commitment to its owners. However, this relationship also underscores the importance of transparency and ethical safeguards to prevent favoritism. For policymakers and financial professionals, understanding this dynamic is crucial for interpreting the Fed’s actions and their implications for monetary policy and financial regulation.

Efficient Coin Sorting: Tips to Organize Change for Bank Deposits

You may want to see also

Explore related products

![]()

Governance Model: Each bank has a unique board, distinct from the Federal Reserve Board

The Federal Reserve System’s governance structure is a masterclass in decentralized authority, with each of the 12 regional Federal Reserve Banks operating under its own unique board of directors. Unlike the centralized Federal Reserve Board in Washington, D.C., these regional boards are deeply embedded in their local economies, ensuring that monetary policy reflects the diverse needs of communities across the United States. Each board consists of nine members: six elected by member banks in the region and three appointed by the Federal Reserve Board. This hybrid structure balances local insight with national oversight, creating a system that is both responsive and accountable.

Consider the Federal Reserve Bank of New York, whose board includes representatives from Wall Street giants like JPMorgan Chase and Goldman Sachs, alongside appointees with expertise in labor and agriculture. In contrast, the Federal Reserve Bank of Minneapolis might feature board members from agricultural cooperatives or manufacturing firms, reflecting the Midwest’s economic priorities. This regional specificity allows each bank to tailor its operations to local conditions, whether addressing rural banking challenges or urban financial innovation. For instance, during the 2008 financial crisis, the New York Fed’s board played a pivotal role in stabilizing global markets, while the San Francisco Fed focused on supporting tech-driven industries in Silicon Valley.

However, this decentralized model is not without its challenges. Critics argue that the dominance of banking representatives on regional boards can skew priorities toward financial institutions rather than the broader public interest. To mitigate this, the three appointed members—one designated as the board’s chair—are required to represent the public, with at least one having expertise in labor or consumer issues. This ensures a counterbalance to banking interests, though the effectiveness of this safeguard varies by region. For example, the Kansas City Fed’s board has been praised for its inclusive approach, while the Dallas Fed has faced scrutiny for perceived bias toward energy sector interests.

Practical implications of this governance model are far-reaching. Regional boards influence monetary policy by providing input to the Federal Open Market Committee (FOMC), where each bank president votes on interest rates and other critical decisions. Additionally, these boards oversee the supervision and regulation of local banks, ensuring compliance with federal laws while considering regional economic nuances. For instance, the Richmond Fed’s board might focus on the impact of manufacturing declines, while the Atlanta Fed addresses housing market volatility in the Southeast.

In conclusion, the unique board structure of each Federal Reserve Bank is a cornerstone of its decentralized governance model. By blending local expertise with national oversight, this system fosters a monetary policy that is both adaptable and inclusive. While challenges remain, particularly in balancing banking and public interests, the regional boards’ role in shaping economic policy underscores their importance in maintaining the Fed’s dual mandate of price stability and maximum employment. Understanding this structure is essential for anyone seeking to grasp the complexities of the U.S. financial system.

Step-by-Step Guide to Making Payments with NBT Bank Easily

You may want to see also

Explore related products

$18.75 $18.75

$55.35 $100

![]()

Regional Focus: Serve specific regions, tailoring policies to local economic conditions

The Federal Reserve System's regional structure is a cornerstone of its ability to address diverse economic landscapes across the United States. Unlike a centralized banking model, the Fed's 12 regional banks act as local economic sentinels, each with a unique mandate to monitor and respond to the specific needs of their respective districts. This decentralized approach allows for a level of granularity in policy implementation that a one-size-fits-all strategy could never achieve.

Consider the contrasting economic profiles of the Boston and Dallas Federal Reserve Districts. Boston, with its concentration of biotechnology and higher education, faces distinct challenges compared to Dallas, a hub for energy and agriculture. The Boston Fed might focus on fostering innovation and managing the impact of a highly skilled labor market, while the Dallas Fed could prioritize stability in commodity-dependent sectors and address the unique financial needs of a rapidly growing population. This regional focus enables the Fed to tailor its monetary policy tools, such as lending rates and reserve requirements, to the specific conditions of each district, ensuring a more nuanced and effective response to local economic fluctuations.

The benefits of this regional approach are particularly evident during economic crises. For instance, during the 2008 financial crisis, the regional Feds played a crucial role in stabilizing local economies. The New York Fed, given its proximity to Wall Street, took a leading role in addressing the liquidity crisis in financial markets, while the San Francisco Fed focused on supporting the technology sector and managing the impact of the housing market collapse in California. This coordinated yet localized response allowed the Fed to mitigate the crisis's effects more effectively than a uniform national strategy could have.

However, this regional focus also presents challenges. Balancing the needs of diverse districts can be complex, and ensuring consistent policy implementation across regions requires careful coordination. The Federal Open Market Committee (FOMC), comprising representatives from each regional bank, serves as the central decision-making body, ensuring that regional perspectives are integrated into national monetary policy. This structure fosters a dynamic dialogue, allowing regional insights to inform broader policy decisions while maintaining a unified approach to achieving the Fed's dual mandate of price stability and maximum employment.

In essence, the Federal Reserve's regional structure is a powerful tool for navigating the economic complexities of a vast and diverse nation. By empowering regional banks to tailor policies to local conditions, the Fed can address the unique challenges and opportunities of each district, fostering a more resilient and inclusive national economy. This regional focus is a key differentiator, setting the Fed apart from centralized banking systems and contributing to its effectiveness in maintaining economic stability across the United States.

Cord Blood Banking: A Lifesaving Resource in Cancer Treatment

You may want to see also

Explore related products

![]()

Profit Distribution: Excess earnings are returned to the U.S. Treasury, not shareholders

The Federal Reserve Banks operate under a unique profit distribution model that sets them apart from traditional commercial banks. Unlike private institutions, where profits are distributed to shareholders, the Federal Reserve returns excess earnings to the U.S. Treasury. This mechanism ensures that the benefits of the central banking system accrue to the public rather than private individuals or entities. In 2022, for instance, the Federal Reserve returned approximately $107 billion to the Treasury, a figure that underscores the scale of this public financial contribution.

This profit distribution model is rooted in the Federal Reserve’s mandate as a public institution. Established by the Federal Reserve Act of 1913, its primary goals include stabilizing the economy, managing inflation, and ensuring maximum employment. By returning excess earnings to the Treasury, the Fed aligns its financial operations with these broader public objectives. This contrasts sharply with commercial banks, which prioritize shareholder returns and profit maximization. For example, while JPMorgan Chase distributed $12 billion in dividends to shareholders in 2022, the Federal Reserve’s excess earnings were entirely redirected to public coffers.

The process of returning excess earnings is systematic and transparent. Each Federal Reserve Bank first covers its expenses, including operational costs and dividends to member banks (capped at 6% of paid-in capital). Any remaining profits are then transferred to the Treasury. This structure ensures that the Fed’s financial activities do not enrich private parties but instead support government operations. For instance, funds returned to the Treasury can be allocated to reduce the federal deficit, fund public programs, or address national priorities, such as infrastructure or healthcare.

Critics might argue that this model limits the Fed’s ability to retain capital for operational flexibility. However, the system is designed to prioritize public accountability over financial autonomy. By forgoing shareholder distributions, the Federal Reserve avoids conflicts of interest and maintains its independence from private influence. This is particularly crucial in monetary policy decisions, where impartiality is essential. For example, during the 2008 financial crisis, the Fed’s ability to act decisively was not hindered by concerns over shareholder returns, allowing it to focus solely on stabilizing the economy.

In practical terms, this profit distribution model serves as a financial buffer for the federal government. During periods of economic stability, the Fed’s contributions can offset other budgetary shortfalls. Conversely, in times of crisis, the Treasury can rely on these funds to support emergency measures. For individuals and businesses, this system indirectly benefits the economy by ensuring that central banking profits are reinvested in public welfare rather than siphoned off to private shareholders. Understanding this mechanism highlights the Federal Reserve’s role not just as a monetary authority but also as a public financial steward.

Where to Find 50 Cent Pieces: Banks or Collectors?

You may want to see also

Explore related products

$28.81 $44.95

![]()

Operational Autonomy: Operate independently but coordinate under the Federal Reserve System

The Federal Reserve System’s 12 regional banks embody a delicate balance: operational autonomy paired with centralized coordination. Each bank operates as a self-contained entity, governed by its own board of directors and responsible for executing monetary policy within its district. This autonomy allows them to tailor their actions to the unique economic conditions of their regions, whether it’s addressing agricultural challenges in the Midwest or tech sector fluctuations in Silicon Valley. For instance, the Federal Reserve Bank of Dallas might focus on energy sector stability, while the New York Fed monitors global financial markets due to its district’s role as a financial hub.

This independence, however, is not unchecked. The Federal Reserve System’s structure ensures coordination through mechanisms like the Federal Open Market Committee (FOMC), where regional bank presidents participate in setting national monetary policy. While only five regional presidents vote at any given time, all 12 contribute to discussions, ensuring local insights inform broader decisions. This dual structure prevents the system from becoming either too fragmented or overly centralized, striking a balance that has been critical to its effectiveness since its inception in 1913.

To illustrate, consider the response to the 2008 financial crisis. Regional banks independently implemented emergency lending programs tailored to their districts’ needs, such as the New York Fed’s efforts to stabilize Wall Street. Simultaneously, they coordinated under the FOMC’s umbrella to execute quantitative easing and interest rate adjustments uniformly across the nation. This blend of autonomy and coordination allowed the Fed to address both localized shocks and systemic risks effectively.

Practical takeaways for understanding this dynamic lie in recognizing the system’s design as a safeguard against one-size-fits-all policies. Policymakers and analysts must appreciate how regional banks’ autonomy enables them to act as economic first responders, while their integration into the broader system ensures national coherence. For businesses and investors, this means monitoring both national Fed announcements and regional bank reports to gauge localized economic trends and potential policy shifts.

In conclusion, the operational autonomy of Federal Reserve Banks is not a license for isolation but a strategic tool for responsive, region-specific action within a unified framework. This structure exemplifies a rare institutional achievement: preserving diversity of thought and action while maintaining collective purpose. It’s a model worth studying for any organization seeking to balance local flexibility with global alignment.

Liberty Bank's Currency Exchange: Dollars to Euros Conversion Explained

You may want to see also

Frequently asked questions

The Federal Reserve System consists of 12 regional Federal Reserve Banks, each serving a specific geographic district. These districts are defined by the Federal Reserve Act and cover different states or parts of states, ensuring localized oversight of the banking system and economic conditions.

The Federal Reserve Banks implement and execute monetary policy, supervise and regulate member banks, and provide financial services within their districts. In contrast, the Federal Reserve Board, based in Washington, D.C., sets overall monetary policy, regulates the banking system nationally, and oversees the entire Federal Reserve System.

Each Federal Reserve Bank has its own president and board of directors, appointed locally, who oversee operations and contribute to monetary policy decisions. The Federal Reserve Board, however, is led by appointed governors who set national policy and coordinate system-wide activities.

While all Federal Reserve Banks participate in monetary policy discussions, the Federal Reserve Bank of New York plays a unique role due to its proximity to financial markets. It executes open market operations and represents the U.S. in international financial matters, whereas other banks focus more on regional economic conditions.

Each Federal Reserve Bank serves as a banker’s bank for commercial banks within its district, providing services like check clearing, electronic payments, and loans. The specific interactions and services may vary slightly based on the needs of the region and the banks operating within it.