The rise of U.S. banks to global dominance is a story of strategic expansion, regulatory influence, and financial innovation. Beginning in the late 20th century, American banks leveraged their access to the world’s largest economy, advanced financial markets, and a stable regulatory environment to outpace competitors. Through aggressive mergers, acquisitions, and international branch openings, institutions like JPMorgan Chase, Citigroup, and Goldman Sachs established a global footprint, becoming key players in cross-border transactions, investment banking, and asset management. Their dominance was further solidified by the dollar’s status as the global reserve currency, which ensured U.S. banks remained central to international trade and finance. Today, their influence extends across continents, shaping global financial systems and economies, often at the expense of local institutions and emerging markets.

Explore related products

What You'll Learn

![]()

Global Expansion Strategies

The rise of U.S. banks as global financial powerhouses wasn't accidental. It was a calculated march fueled by strategic acquisitions, regulatory arbitrage, and a relentless focus on international markets. This global expansion wasn't merely about planting flags on foreign soil; it was about capturing lucrative markets, diversifying revenue streams, and establishing dominance in the increasingly interconnected world of finance.

One key strategy was targeted acquisitions of foreign banks. Think JPMorgan Chase's acquisition of Bank One in 2004, which significantly bolstered its presence in Europe and Asia. This approach allowed U.S. banks to bypass the time-consuming process of building a customer base from scratch, instantly gaining access to established networks, local expertise, and regulatory approvals.

Another crucial tactic was leveraging regulatory differences. U.S. banks often exploited less stringent regulations in certain countries to offer products and services that might be restricted at home. This "regulatory arbitrage" allowed them to maximize profits and gain a competitive edge, though it also raised concerns about financial stability and consumer protection.

For instance, some U.S. banks established subsidiaries in tax havens, allowing them to minimize their global tax burden and channel profits through jurisdictions with favorable tax regimes. While legally permissible, such practices have sparked debates about fairness and the erosion of tax revenues in other countries.

Building strategic partnerships was another pillar of this expansion. U.S. banks formed alliances with local financial institutions in target markets, gaining access to their customer base and distribution networks while sharing risks and rewards. This approach allowed them to navigate complex local regulations and cultural nuances more effectively.

The success of these strategies is evident in the sheer scale of U.S. banks' global reach. Today, institutions like Citigroup, Bank of America, and Goldman Sachs operate in dozens of countries, managing trillions of dollars in assets worldwide. Their dominance has reshaped the global financial landscape, influencing everything from interest rates to investment trends.

However, this global expansion hasn't been without challenges. Cultural misunderstandings, regulatory hurdles, and economic downturns have all tested the resilience of U.S. banks' international ventures. The 2008 financial crisis, for example, exposed the vulnerabilities of a highly interconnected financial system, leading to increased scrutiny and tighter regulations globally.

Understanding Bank Reserves: A Step-by-Step Guide to Calculating Total Reserves

You may want to see also

Explore related products

![]()

Financial Deregulation Impact

Financial deregulation in the United States during the late 20th century unleashed a wave of expansion for American banks, transforming them from domestic powerhouses into global financial titans. The repeal of the Glass-Steagall Act in 1999, which had separated commercial and investment banking since the Great Depression, stands as a pivotal moment. This legislative change allowed banks like Citigroup and JPMorgan Chase to merge and offer a full spectrum of financial services, from traditional loans to complex investment products. Suddenly, these institutions had the scale and scope to compete internationally, leveraging their newfound freedom to acquire foreign banks, establish overseas branches, and dominate global markets.

Example: Citigroup's acquisition of Mexico's Banamex in 2001 marked a significant early victory in this global expansion, showcasing the appetite and capability of deregulated U.S. banks to penetrate emerging markets.

This deregulation-driven expansion wasn’t just about mergers and acquisitions; it fundamentally altered the global financial landscape. U.S. banks became architects of a new financial order, exporting their risk-taking culture and innovative—yet often opaque—financial instruments worldwide. The proliferation of derivatives, securitization, and other complex products, pioneered by Wall Street, became the lingua franca of global finance. However, this influence came at a cost. The 2008 financial crisis exposed the dangers of unchecked deregulation, as the collapse of U.S.-originated subprime mortgage securities triggered a global recession. Analysis: While deregulation enabled U.S. banks to dominate global markets, it also amplified systemic risks, revealing the double-edged sword of financial liberalization.

To understand the impact of deregulation, consider the role of U.S. banks in shaping international regulatory standards. Through their dominance in global markets, American financial institutions effectively exported their regulatory preferences, often favoring lighter oversight and greater flexibility. This influence was evident in the Basel Accords, where U.S. banks pushed for risk-based capital requirements that aligned with their business models. Takeaway: Financial deregulation not only allowed U.S. banks to expand globally but also positioned them as de facto regulators, shaping the rules of the game in ways that often prioritized their interests over broader financial stability.

For those navigating today’s financial landscape, the lessons of deregulation are clear: Steps to Mitigate Risk: 1) Diversify investments across regions and asset classes to reduce exposure to U.S.-centric financial shocks. 2) Advocate for stronger international regulatory cooperation to counterbalance the outsized influence of U.S. banks. 3) Stay informed about global financial trends, as the actions of U.S. institutions continue to ripple across borders. Cautions: Over-reliance on U.S. financial models can lead to vulnerabilities, as seen in the 2008 crisis. Conclusion: While U.S. banks’ global dominance is a product of deregulation, it also underscores the need for a more balanced and resilient international financial system.

Discovering Beaver Bank Dens: Essential Tips for Locating Their Hidden Homes

You may want to see also

Explore related products

$25.73 $44.95

![]()

Dollar Dominance in Trade

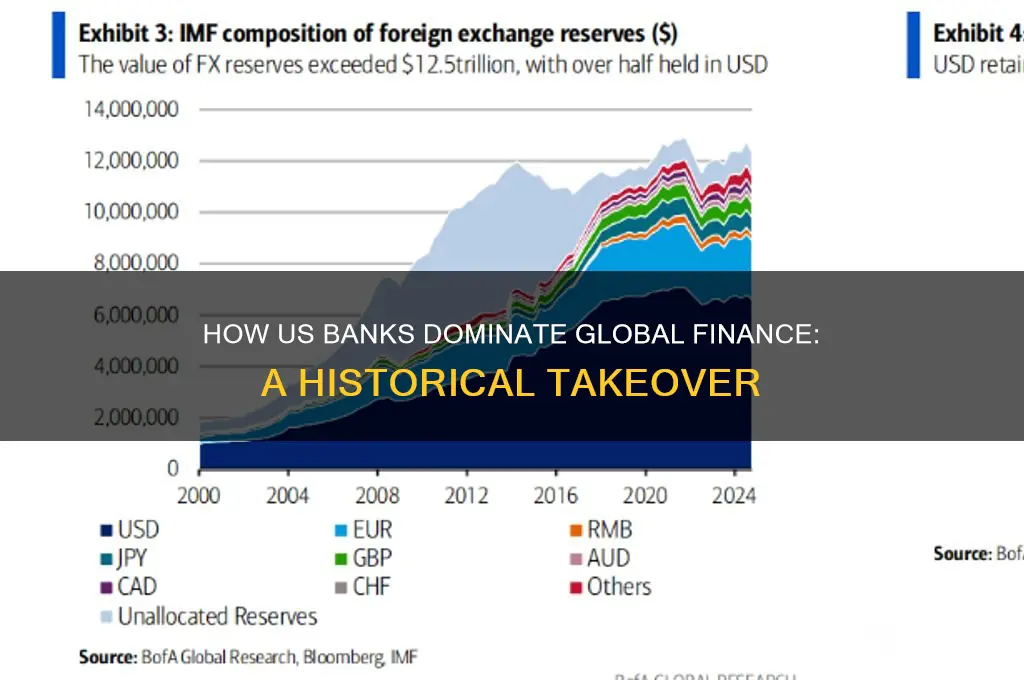

The US dollar's dominance in global trade is a phenomenon rooted in historical agreements and strategic economic policies. After World War II, the Bretton Woods system pegged major currencies to the dollar, which itself was convertible to gold. Though this gold standard ended in 1971, the dollar's centrality persisted due to its liquidity, stability, and the size of the US economy. Today, approximately 60% of global foreign exchange reserves are held in dollars, and it accounts for about 88% of all foreign exchange transactions. This primacy ensures that even transactions between non-US countries often rely on the dollar as an intermediary currency.

Consider the practical implications for businesses engaged in international trade. When a German automaker sells vehicles to China, the transaction is typically priced in dollars, even though neither country uses it domestically. This practice reduces exchange rate risk and leverages the dollar's deep liquidity. However, it also means that central banks worldwide must maintain substantial dollar reserves to facilitate trade, effectively tying their economic stability to US monetary policy. For instance, during the 2008 financial crisis, the Federal Reserve's actions directly impacted non-US economies reliant on dollar-denominated trade.

Critics argue that dollar dominance grants the US disproportionate influence over global commerce. Sanctions, such as those imposed on Iran or Russia, can effectively cut targeted nations out of the international financial system by restricting their access to dollars. This weaponization of the currency underscores its dual role as both a tool of trade and a lever of geopolitical power. Meanwhile, emerging economies like China are actively seeking to reduce their dollar dependence, promoting alternatives like the yuan in bilateral trade agreements. Yet, the yuan accounts for less than 3% of global trade invoicing, highlighting the dollar's entrenched position.

For individuals and businesses, navigating this dollar-centric system requires strategic planning. Exporters in non-US countries can hedge against currency fluctuations by invoicing in dollars, but this exposes them to US interest rate changes. Conversely, importers may benefit from a strong domestic currency relative to the dollar but face risks during periods of dollar appreciation. Practical tips include diversifying currency holdings, using financial instruments like forward contracts, and staying informed about Federal Reserve policies. As the global economy evolves, understanding the mechanics of dollar dominance remains essential for anyone engaged in international trade.

Securely Delete Your Banking Details from ConEd: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Mergers and Acquisitions Growth

The rise of U.S. banks as global financial powerhouses is inextricably linked to their strategic use of mergers and acquisitions (M&A). Since the 1980s, American banks have leveraged M&A to expand their reach, consolidate market share, and diversify their service offerings. This growth strategy has allowed them to dominate not only domestic markets but also to establish a significant presence in international financial centers. By acquiring smaller banks, both domestically and abroad, U.S. financial institutions have created economies of scale, reduced operational costs, and gained access to new customer bases. For instance, the acquisition of Credit Suisse by UBS in 2023, though Swiss-led, exemplifies the broader trend of consolidation that U.S. banks have pioneered, often setting the pace for global financial integration.

Consider the playbook of JPMorgan Chase, one of the largest banks in the world. Its growth trajectory is a masterclass in M&A strategy. Starting with the merger of Chase Manhattan Corporation and J.P. Morgan & Co. in 2000, the bank has since acquired over 50 institutions, including Bear Stearns and Washington Mutual during the 2008 financial crisis. These acquisitions not only bolstered its balance sheet but also expanded its capabilities in investment banking, asset management, and retail banking. The result? A financial behemoth with a global footprint, capable of offering a full suite of services across multiple continents. This approach has been replicated by peers like Bank of America and Citigroup, further solidifying U.S. banks' dominance.

However, M&A growth is not without its pitfalls. Regulatory scrutiny, cultural integration challenges, and overleveraging are significant risks. The collapse of Wachovia, acquired by Wells Fargo in 2008, serves as a cautionary tale. Wachovia's risky mortgage portfolio became a liability, forcing Wells Fargo to navigate years of legal and financial repercussions. Similarly, cross-border acquisitions often face regulatory hurdles, as seen in the delayed approval of BBVA’s acquisition of Sunbelt Holdings due to compliance issues. To mitigate these risks, banks must conduct thorough due diligence, ensure regulatory alignment, and develop robust integration plans. A practical tip: focus on acquiring institutions with complementary strengths and a strong risk management framework.

Comparatively, U.S. banks' M&A strategies differ from those of European or Asian counterparts. While European banks often prioritize regional consolidation, U.S. banks have historically pursued a more global approach, targeting emerging markets and high-growth sectors. For example, Citigroup’s acquisition of Banamex in 2001 gave it a dominant position in Mexico’s banking sector. In contrast, Asian banks have focused on domestic growth, with limited cross-border M&A activity. This global ambition has allowed U.S. banks to diversify revenue streams and reduce reliance on any single market, a key factor in their resilience during economic downturns.

In conclusion, mergers and acquisitions have been a cornerstone of U.S. banks' global dominance. By strategically acquiring institutions, they have expanded their reach, diversified their offerings, and achieved economies of scale. Yet, this growth must be managed carefully to avoid regulatory pitfalls and financial overexposure. For banks looking to replicate this success, the lesson is clear: prioritize acquisitions that align with long-term strategic goals, ensure regulatory compliance, and integrate seamlessly. Done right, M&A can transform a regional player into a global leader, as U.S. banks have demonstrated time and again.

Is Internet Banking in Australia Secure? A Comprehensive Safety Analysis

You may want to see also

Explore related products

![]()

Influence on International Policy

The U.S. dollar’s dominance as the global reserve currency is no accident—it’s a direct result of strategic policies and institutions like the Federal Reserve and Wall Street banks. Since the Bretton Woods Agreement in 1944, the dollar has been tethered to international trade, with over 60% of global foreign exchange reserves still held in USD. This primacy allows U.S. banks to project influence by controlling the flow of capital, effectively dictating terms for nations reliant on dollar-denominated transactions. For instance, countries like Venezuela and Iran have faced severe economic isolation due to U.S.-imposed sanctions, demonstrating how financial systems can be weaponized as tools of foreign policy.

Consider the role of institutions like the International Monetary Fund (IMF) and World Bank, where U.S. influence is disproportionate due to its largest shareholder status. These organizations often prescribe austerity measures and market liberalization policies in exchange for loans, reshaping recipient nations’ economies to align with U.S. interests. A case in point is the 1997 Asian Financial Crisis, where IMF bailouts came with conditions that opened local markets to U.S. financial institutions, solidifying their global footprint. This pattern repeats across emerging economies, where debt dependency becomes a lever for policy control.

To understand the mechanics, examine how U.S. banks operate as both lenders and advisors to foreign governments. Through syndicated loans and sovereign bond issuances, they embed themselves in national financial systems, gaining insider access to policy formulation. For example, Goldman Sachs’ involvement in Greece’s pre-2008 debt structuring highlights how private banks can shape fiscal decisions with global repercussions. Such entanglements blur the line between private profit and public policy, often at the expense of local economic sovereignty.

A cautionary note: this influence isn’t without backlash. The rise of alternative payment systems like China’s CIPS (Cross-Border Interbank Payment System) and the increasing use of cryptocurrencies challenge the dollar’s hegemony. Nations are exploring de-dollarization strategies, as seen in Brazil and Russia’s recent trade agreements in local currencies. For policymakers and businesses, diversifying currency exposure and fostering regional financial alliances could mitigate overreliance on U.S.-dominated systems.

In practical terms, countries seeking to reduce this influence should prioritize three steps: first, develop robust domestic capital markets to lessen dependency on foreign banks; second, negotiate trade in local currencies or through multilateral platforms; and third, invest in financial literacy to navigate complex global systems. While U.S. banks’ dominance remains formidable, proactive measures can reclaim degrees of autonomy in an interconnected world.

Tesco Bank Outage: How Long Will Services Remain Unavailable?

You may want to see also

Frequently asked questions

U.S. banks gained global dominance through the strength of the U.S. economy, the U.S. dollar's status as the world's reserve currency, and the expansion of multinational corporations and financial markets post-World War II. Institutions like JPMorgan Chase, Citigroup, and Goldman Sachs leveraged their size, innovation, and regulatory advantages to establish a global footprint.

The U.S. dollar's role as the primary global reserve currency allowed U.S. banks to facilitate international trade, lending, and investments. This dominance enabled them to set financial standards, control key markets, and act as intermediaries in global transactions, solidifying their influence worldwide.

Yes, U.S. banks faced challenges such as regulatory hurdles in foreign markets, competition from local and international banks, and financial crises (e.g., 2008). However, their adaptability, technological advancements, and government support helped them overcome these obstacles and maintain their global leadership.