The question of whether 531 represents a record for failed banks is a critical inquiry into the stability of the financial system. This number, often cited in discussions about banking crises, refers to the total number of bank failures during a specific period, typically a year or a multi-year span. To determine if 531 is indeed a record, it is essential to compare this figure to historical data from previous financial downturns, such as the Savings and Loan Crisis of the 1980s or the Great Recession of 2008. Analyzing factors such as economic conditions, regulatory environments, and the size of the banking sector during these periods provides context to assess whether 531 signifies an unprecedented collapse or aligns with past trends. Understanding this record is crucial for policymakers, economists, and the public to gauge the resilience of the banking system and implement measures to prevent future failures.

Explore related products

What You'll Learn

![]()

Historical context of bank failures

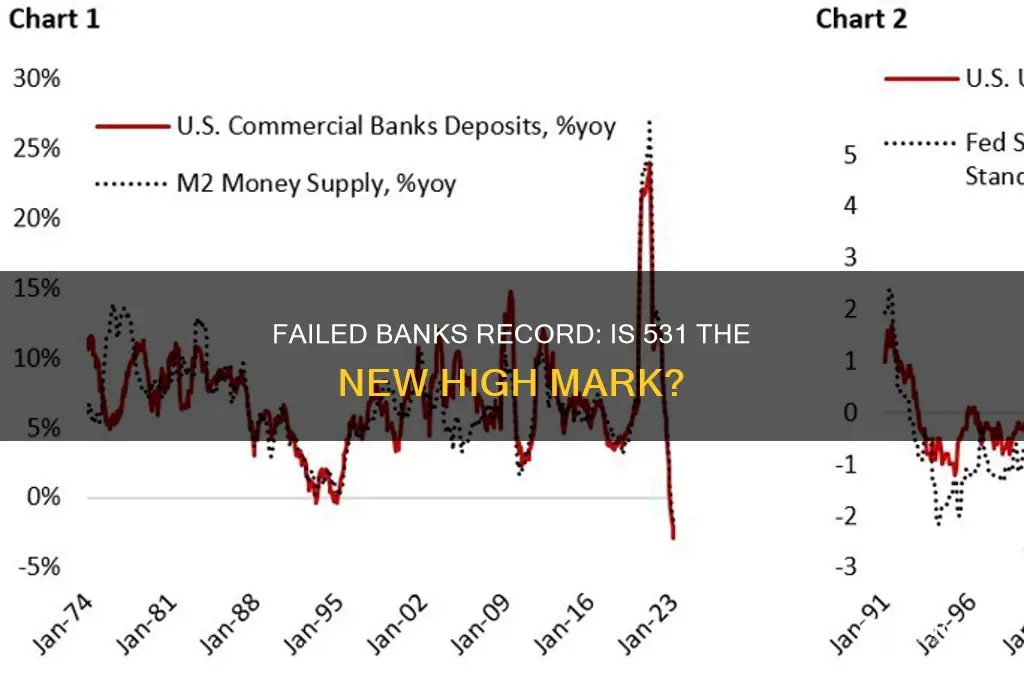

Bank failures are not a modern phenomenon; they have been a recurring theme throughout history, often serving as barometers of economic health and regulatory efficacy. The number 531, if indeed a record for failed banks, would likely refer to a specific period or event, such as the Great Depression or the 2008 financial crisis. To understand whether 531 is a record, one must first examine the historical context of bank failures, which reveals patterns of economic stress, regulatory shortcomings, and societal impacts. For instance, the 1930s saw over 9,000 bank failures in the U.S. alone, a stark reminder of the fragility of financial systems during severe economic downturns.

Analyzing historical bank failures requires a focus on causation. The Panic of 1907, for example, was triggered by a failed attempt to manipulate the stock market, leading to a liquidity crisis and the collapse of numerous banks. This event underscored the need for a central banking system, ultimately leading to the creation of the Federal Reserve in 1913. Similarly, the Savings and Loan Crisis of the 1980s, which resulted in the failure of over 1,000 institutions, was driven by deregulation, risky investments, and economic recession. These examples illustrate how bank failures are often the culmination of systemic vulnerabilities rather than isolated incidents.

To assess whether 531 is a record, one must consider the scale and impact of failures relative to the size of the banking system. During the Great Depression, bank failures accounted for a significant portion of all existing banks, devastating communities and eroding public trust. In contrast, the 2008 financial crisis saw fewer absolute failures but involved larger, systemically important institutions, necessitating massive government intervention. A record number like 531 would thus need to be contextualized by the era’s banking landscape, regulatory environment, and economic conditions to gauge its significance.

Practical takeaways from historical bank failures include the importance of robust regulatory frameworks, such as deposit insurance (introduced in the U.S. in 1933) and stress testing. For individuals, diversifying assets and staying informed about a bank’s health are critical steps to mitigate risk. Policymakers, meanwhile, must balance innovation with oversight to prevent the recurrence of past crises. Understanding the historical context of bank failures not only clarifies whether 531 is a record but also provides actionable insights for preventing future collapses.

Finally, comparing historical bank failures across different regions offers a global perspective. For instance, Japan’s banking crisis in the 1990s, characterized by non-performing loans and delayed government action, contrasts with the swift U.S. response to the 2008 crisis. Such comparisons highlight the role of cultural, political, and economic factors in shaping outcomes. If 531 is indeed a record, it would likely reflect a unique combination of these factors, making it a valuable case study for understanding the resilience of financial systems in the face of adversity.

Launching a Bank in Nepal: Essential Steps and Regulatory Insights

You may want to see also

Explore related products

![]()

Causes of 531 bank failures

The 531 bank failures in the United States during the 2008 financial crisis were not merely a number but a stark indicator of systemic vulnerabilities. To understand this record, one must dissect the multifaceted causes that led to such widespread collapse. At the core, these failures were the culmination of risky lending practices, inadequate regulatory oversight, and a housing market bubble that, when burst, sent shockwaves through the financial system. Banks, lured by the promise of short-term profits, extended subprime mortgages to borrowers with poor credit histories, setting the stage for default and foreclosure.

Consider the role of securitization in this debacle. Banks bundled these subprime mortgages into complex financial instruments, such as mortgage-backed securities (MBS) and collateralized debt obligations (CDOs), which were then sold to investors. This process obscured the underlying risk, as credit rating agencies often assigned these securities high ratings despite their shaky foundations. When homeowners began defaulting en masse, the value of these securities plummeted, leaving banks with toxic assets and depleted capital reserves. This chain reaction exposed the fragility of a system built on leverage and speculation.

Another critical factor was the lack of robust regulatory frameworks. Regulatory bodies, such as the Office of the Comptroller of the Currency (OCC) and the Federal Reserve, failed to curb excessive risk-taking or ensure sufficient capital buffers. The Gramm-Leach-Bliley Act of 1999, which repealed the Glass-Steagall Act, further blurred the lines between commercial and investment banking, enabling institutions to engage in riskier activities. Without stringent oversight, banks operated with impunity, amplifying the eventual fallout.

The psychological and behavioral aspects of the crisis cannot be overlooked. Herd mentality and overconfidence led banks to underestimate the risks associated with their investments. Executives and investors alike believed the housing market would continue to rise indefinitely, a belief that proved catastrophic. This collective delusion highlights the dangers of unchecked optimism in financial decision-making.

In retrospect, the 531 bank failures were not an isolated event but the result of interconnected failures—regulatory, institutional, and behavioral. To prevent future crises, policymakers must address these root causes by implementing stricter regulations, promoting transparency, and fostering a culture of accountability. Banks, too, must adopt more conservative risk management practices and prioritize long-term stability over short-term gains. The lessons of 531 failures serve as a cautionary tale, reminding us that the health of the financial system depends on vigilance, prudence, and a commitment to ethical practices.

Land Bank Legislation: How Many U.S. States Have Adopted It?

You may want to see also

Explore related products

![]()

Impact on the economy

The failure of 531 banks, if indeed a record, signals a profound disruption in the financial system, with ripple effects across the broader economy. Such a high number of bank failures typically indicates systemic issues—whether regulatory lapses, economic downturns, or a combination of both. When banks fail en masse, the immediate consequence is a contraction in credit availability. Small businesses, which rely heavily on bank loans for operations and expansion, face sudden funding shortages. This credit crunch can stifle entrepreneurship, delay investments, and slow economic growth. For instance, during the 2008 financial crisis, a surge in bank failures led to a 10% drop in small business lending within a year, according to Federal Reserve data.

Consider the domino effect on consumer confidence. Bank failures erode trust in the financial system, prompting individuals to reduce spending and increase savings. This behavioral shift can depress aggregate demand, leading to a slowdown in sectors like retail, real estate, and manufacturing. Historical data shows that economies with significant bank failures often experience a 2-3% decline in GDP growth within the subsequent 12 months. For example, Sweden’s banking crisis in the early 1990s saw consumer spending drop by 5% as households retrenched in response to financial instability.

A less obvious but equally critical impact is on the labor market. Bank failures often result in job losses within the financial sector, but the fallout extends to other industries as well. Reduced lending and economic uncertainty can force businesses to cut costs, including layoffs. During the savings and loan crisis of the 1980s, the U.S. lost over 50,000 banking jobs, but the unemployment rate also rose in construction and services due to reduced credit availability. Policymakers must act swiftly to mitigate this, potentially through stimulus measures or job retraining programs.

Finally, the fiscal burden of bank failures cannot be overlooked. Governments often step in to stabilize the financial system, either through bailouts or deposit insurance payouts. While these measures protect depositors and prevent panic, they strain public finances. For instance, the U.S. Troubled Asset Relief Program (TARP) allocated $700 billion to stabilize banks during the 2008 crisis. Such expenditures divert resources from other critical areas like healthcare or infrastructure, creating long-term economic trade-offs.

In summary, the impact of 531 bank failures on the economy is multifaceted, affecting credit markets, consumer behavior, employment, and public finances. Understanding these dynamics is crucial for crafting effective responses, whether through regulatory reforms, fiscal interventions, or targeted support for vulnerable sectors. The goal is not just to address the immediate crisis but to build resilience against future shocks.

Understanding Bank Maintenance Fees and Their Application

You may want to see also

Explore related products

![A Summary of Savings Banks That Have Failed in the State of New York, by Willis S. Paine 1906 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Regulatory responses to failures

The 531 bank failures in the U.S. between 2008 and 2012 exposed critical weaknesses in regulatory oversight, prompting a wave of reforms aimed at preventing future collapses. The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 stands as the cornerstone of this response, introducing stricter capital requirements, stress testing for large institutions, and the Volcker Rule to limit proprietary trading. These measures sought to address the root causes of the crisis, such as excessive risk-taking and inadequate liquidity buffers, by imposing tighter controls on banks’ activities and ensuring they could withstand economic shocks.

However, regulatory responses to bank failures are not one-size-fits-all. Smaller banks, for instance, often face disproportionate compliance burdens compared to their larger counterparts. Recognizing this, the Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018 provided targeted relief to community banks, raising the asset threshold for enhanced supervision from $50 billion to $250 billion. This example highlights the importance of tailoring regulatory responses to the size, complexity, and risk profile of institutions, ensuring that rules are effective without stifling economic growth.

A comparative analysis of global regulatory responses reveals varying approaches to bank failures. While the U.S. focused on systemic risk mitigation, the European Union implemented the Bank Recovery and Resolution Directive (BRRD), emphasizing resolution frameworks to manage failing banks without taxpayer bailouts. The BRRD introduced tools like bail-in mechanisms, where creditors bear losses instead of taxpayers, and mandated recovery plans for banks. These contrasting strategies underscore the need for international cooperation to harmonize standards and prevent regulatory arbitrage.

Persuasively, the success of regulatory responses hinges on proactive enforcement and continuous monitoring. Post-2008, U.S. regulators increased on-site inspections and penalties for non-compliance, signaling a zero-tolerance approach to violations. For instance, Wells Fargo faced a $3 billion fine in 2020 for widespread consumer abuses, demonstrating the consequences of regulatory breaches. Yet, challenges remain, such as keeping pace with financial innovation and ensuring regulators have sufficient resources to oversee an evolving industry.

Instructively, banks and policymakers can adopt practical steps to enhance resilience. Stress testing should incorporate diverse scenarios, including cyberattacks and climate risks, to reflect modern threats. Boards must prioritize risk culture, ensuring employees at all levels understand their role in maintaining stability. Additionally, regulators should leverage technology, such as AI-driven analytics, to detect early warning signs of distress. By combining robust frameworks with adaptive strategies, regulatory responses can effectively mitigate the risk of future bank failures.

Step-by-Step Guide to Applying for an OD in HDFC Bank

You may want to see also

Explore related products

![]()

Recovery and lessons learned

The 531 bank failures during the 2008 financial crisis serve as a stark reminder of systemic vulnerabilities. Recovery from such widespread collapse required a multi-pronged approach, combining government intervention, industry restructuring, and a renewed focus on risk management. The Troubled Asset Relief Program (TARP) injected $700 billion into struggling institutions, providing a crucial lifeline. However, this was just the first step. Banks had to fundamentally re-evaluate their lending practices, prioritizing stability over aggressive growth.

The aftermath of the crisis saw a wave of mergers and acquisitions, as stronger banks absorbed weaker ones, consolidating the industry and reducing overall risk. This period also witnessed a regulatory overhaul, with the Dodd-Frank Act imposing stricter capital requirements and consumer protections. These measures aimed to prevent a recurrence of the reckless lending and speculative practices that fueled the crisis.

A key lesson learned was the importance of transparency and accountability. The opacity of complex financial instruments like mortgage-backed securities had obscured the true extent of risk within the system. Post-crisis regulations mandated greater disclosure and standardized reporting, allowing regulators and investors to better assess banks' financial health. Stress testing became a regular feature, simulating extreme economic scenarios to ensure banks could withstand future shocks.

While these measures have strengthened the banking system, challenges remain. The rise of shadow banking and the increasing complexity of financial products demand constant vigilance. Regulators must adapt to evolving risks, ensuring that the lessons of the past are not forgotten.

For individuals, the crisis highlighted the importance of financial literacy and diversification. Understanding the risks associated with different investment products and spreading assets across various asset classes can mitigate potential losses. The 531 bank failures serve as a cautionary tale, reminding us of the fragility of the financial system and the need for constant vigilance and responsible practices at all levels.

Does Regions Bank Support QuickPay with Zelle? Find Out Now

You may want to see also

Frequently asked questions

No, 531 is not a record for the number of failed banks in a single year. The highest number of bank failures in the U.S. occurred in 1989, with 534 banks failing during the savings and loan crisis.

The number 531 does not represent a specific record or milestone for failed banks. It may be a misinterpretation or a reference to a different dataset or event.

No, there has not been a year where exactly 531 banks failed in the United States. The closest record is 534 failures in 1989.

The number 531 is not directly associated with any major banking crisis or event. It appears to be a non-specific figure and not tied to historical banking data.

Yes, 531 could be a typo or misreference. The actual record for bank failures in a single year is 534, which occurred in 1989 during the savings and loan crisis.