When managing finances in QuickBooks, understanding the role of a bank is crucial. While a bank is not typically classified as a vendor in the traditional sense, it can be set up as a Bank account type within QuickBooks to track transactions such as deposits, withdrawals, and transfers. Vendors in QuickBooks are usually entities to whom payments are made for goods or services, whereas a bank account is used to manage cash flow and reconcile statements. However, in certain scenarios, such as paying bank fees or loan payments, the bank might be added as a vendor to facilitate these specific transactions. Properly distinguishing between a bank account and a vendor ensures accurate financial tracking and reporting in QuickBooks.

| Characteristics | Values |

|---|---|

| Definition | In QuickBooks, a vendor is typically defined as a supplier or service provider from whom you purchase goods or services. |

| Bank Role | A bank is generally not considered a vendor in QuickBooks unless it provides services beyond traditional banking, such as merchant services or financial consulting. |

| Transactions | Banks are usually categorized under "Banking" or "Financial Institutions" for transactions like loan payments, interest expenses, or bank fees. |

| Vendor Setup | If a bank provides vendor-like services (e.g., merchant services), it can be set up as a vendor in QuickBooks. Otherwise, it is not recommended. |

| Expense Tracking | Bank-related expenses (e.g., fees) are tracked under specific expense accounts, not under vendor accounts unless the bank is acting as a vendor. |

| Reconciliation | Bank accounts are reconciled separately in QuickBooks, distinct from vendor transactions. |

| Best Practice | Treat banks as financial institutions unless they provide vendor-specific services. Use appropriate expense accounts for bank-related costs. |

Explore related products

$55.55 $89.95

What You'll Learn

![]()

Defining Vendors in QuickBooks

In QuickBooks, a vendor is defined as any entity from which your business purchases goods or services. This includes suppliers, contractors, and service providers. However, the question of whether a bank qualifies as a vendor is nuanced. While banks primarily manage financial transactions, they can also provide services like merchant accounts, loans, or fees that your business pays for. If your business incurs expenses directly from a bank—such as monthly service charges, loan interest, or transaction fees—QuickBooks treats the bank as a vendor for tracking these costs.

To determine if a bank should be classified as a vendor in your QuickBooks setup, consider the nature of the transactions. For instance, routine deposits, withdrawals, or transfers between your accounts are not vendor transactions; they are handled through the banking module. Conversely, expenses like overdraft fees, wire transfer charges, or loan payments are vendor transactions because they represent costs incurred from the bank. Properly categorizing these ensures accurate financial reporting and simplifies tax preparation.

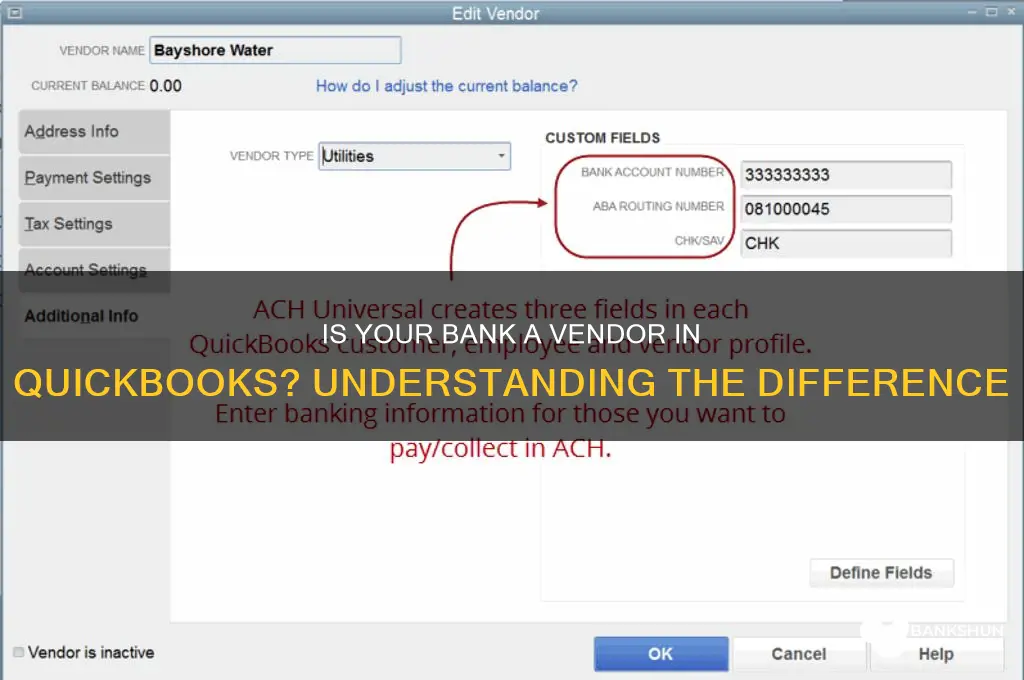

When setting up a bank as a vendor in QuickBooks, follow these steps: navigate to the "Vendors" menu, select "Vendor Center," and click "New Vendor." Enter the bank’s details, including name, address, and account number. Be specific in naming the vendor—for example, "Chase Bank – Business Services" to distinguish it from general banking activities. Assign the appropriate expense account for tracking payments, such as "Bank Fees" or "Loan Interest." This clarity prevents confusion and ensures expenses are allocated correctly.

One common mistake is conflating banking transactions with vendor payments. For example, transferring funds from a business checking account to a savings account is not a vendor payment; it’s an internal transfer. However, paying a bank-issued invoice for a service fee is a vendor transaction. Understanding this distinction is crucial for maintaining clean financial records. Regularly reconcile your accounts to verify that vendor payments to banks are accurately recorded and separate from standard banking activities.

Finally, leverage QuickBooks’ reporting tools to monitor vendor expenses, including those from banks. Run a "Vendor Expenses Detail" report to track how much your business spends on bank-related services over time. This data can highlight opportunities to negotiate lower fees or switch providers. By clearly defining and managing banks as vendors where appropriate, you enhance the accuracy and efficiency of your financial management in QuickBooks.

Maximize Your Commerce Bank Rewards: Easy Steps to Redeem Points

You may want to see also

Explore related products

![]()

Bank Transactions in QuickBooks

In QuickBooks, a bank is not categorized as a vendor, but understanding how bank transactions are managed is crucial for accurate financial tracking. Bank transactions in QuickBooks are primarily recorded through the banking module, where you connect your bank accounts to automatically import transactions. This process eliminates manual data entry, reducing errors and saving time. Once connected, transactions appear in the "For Review" tab, where you can categorize them, match them to existing records, or add new details before accepting them into your books. This streamlined approach ensures that your financial records remain up-to-date and accurate.

Analyzing bank transactions in QuickBooks reveals the importance of proper categorization. Each transaction must be assigned to the correct account, such as expenses, income, or transfers, to maintain accurate financial statements. For instance, a payment to a supplier should be categorized under the appropriate expense account, while a deposit from a client should be recorded as income. QuickBooks allows you to create rules for recurring transactions, automating the categorization process. This feature is particularly useful for businesses with consistent banking activities, such as monthly rent payments or regular client invoices.

A comparative look at manual vs. automated bank transaction management in QuickBooks highlights the efficiency gains of automation. Manually entering transactions is time-consuming and prone to errors, especially for businesses with high transaction volumes. In contrast, automated bank feeds not only save time but also provide real-time visibility into cash flow. However, it’s essential to periodically review automated entries for accuracy, as discrepancies can occur due to bank feed errors or mismatched transactions. Combining automation with regular reviews ensures a balance between efficiency and precision.

For businesses handling multiple bank accounts, QuickBooks offers a centralized dashboard to manage all transactions in one place. This feature is particularly beneficial for companies with separate accounts for operating expenses, payroll, or savings. By linking all accounts, you can easily transfer funds between them, track balances, and generate consolidated reports. For example, transferring $5,000 from a savings account to cover operating expenses can be recorded as a transfer transaction, maintaining clarity in your financial records. This centralized approach simplifies multi-account management and enhances overall financial oversight.

Finally, leveraging QuickBooks’ reconciliation tools is essential for ensuring bank transactions align with your records. Monthly reconciliation involves comparing your QuickBooks transactions to your bank statement to identify any discrepancies, such as missing or duplicate entries. To reconcile, navigate to the Banking menu, select Reconcile, and follow the prompts to match transactions. For instance, if a $300 expense is missing, you can add it during reconciliation to balance your books. Regular reconciliation not only maintains accuracy but also helps detect potential fraud or errors early, safeguarding your financial health.

Does Xoom Reveal Banking Details to Recipients? A Privacy Overview

You may want to see also

Explore related products

![]()

Bank as Payee vs. Vendor

In QuickBooks, distinguishing between a bank as a payee and a bank as a vendor is crucial for accurate financial tracking. When you record a transaction where a bank is the recipient of funds, such as a loan payment or a transfer, the bank is typically treated as a payee. This means the transaction is logged under the bank’s name in the "Payees" field, ensuring clarity in your expense or liability accounts. For instance, if you pay off a business credit card issued by a bank, the bank is the payee, and the transaction reduces your credit card liability.

Conversely, a bank becomes a vendor in QuickBooks when it provides a service or product for which you are billed. This is less common but can occur in scenarios like bank fees for wire transfers, account maintenance, or software subscriptions. In these cases, the bank is set up as a vendor, and the expense is categorized accordingly. For example, if your bank charges a monthly fee for using their payroll processing service, you would create a vendor record for the bank and record the expense under the appropriate account, such as "Bank Service Charges."

The key difference lies in the nature of the transaction. Payee transactions are typically one-sided, involving payments to the bank for loans, credit cards, or transfers. Vendor transactions, however, involve an exchange of services or products, requiring more detailed expense tracking. Misclassifying these can lead to confusion in financial reports, such as overstating liabilities or understating expenses.

To avoid errors, follow these practical steps:

- Review the transaction purpose: Determine if the bank is receiving funds (payee) or providing a service (vendor).

- Use consistent naming: Ensure the bank’s name is uniform across payee and vendor records to prevent duplicates.

- Categorize expenses carefully: Assign vendor expenses to the correct account (e.g., "Bank Fees" vs. "Loan Payments").

- Reconcile regularly: Cross-check bank statements with QuickBooks entries to ensure accuracy in both payee and vendor transactions.

By understanding this distinction, you can maintain a clean and organized QuickBooks ledger, ensuring financial transparency and compliance. Treat the bank as a payee for payments and as a vendor for services, and your bookkeeping will remain precise and efficient.

Step-by-Step Guide: Buying Bitcoin Easily with Simple Bank Account

You may want to see also

Explore related products

![QuickBooks Online for Beginners Bible Edition [2 Books in 1]: The Ultimate Fast Learning Guide for QBO, filled with Step-by-Step Illustrated Explanations, Practical Examples and Common Problem Solving](https://m.media-amazon.com/images/I/61WWhskpzAL._AC_UL320_.jpg)

![]()

Recording Bank Fees in QuickBooks

In QuickBooks, banks are typically treated as vendors when recording bank fees, a practice that simplifies expense tracking and ensures accurate financial reporting. This approach leverages QuickBooks’ vendor management system to categorize and monitor bank-related charges efficiently. By setting up your bank as a vendor, you can record fees such as monthly service charges, overdraft fees, or wire transfer costs in a structured manner, linking them directly to the appropriate expense accounts.

To begin, navigate to the Vendor Center in QuickBooks and add your bank as a new vendor. Include essential details such as the bank’s name, address, and account number. Once the bank is established as a vendor, you can record fees by creating an expense transaction. For instance, if your bank charges a $25 monthly service fee, enter this as a bill or expense, selecting the bank as the vendor and categorizing the expense under the appropriate account, such as “Bank Service Charges.” This method ensures consistency and makes it easier to generate reports on bank-related expenses.

A critical aspect of recording bank fees is maintaining clarity in expense categorization. QuickBooks allows you to assign specific expense accounts to different types of fees, such as “Overdraft Fees” or “Wire Transfer Charges.” This granularity not only aids in financial analysis but also helps identify trends in bank-related costs. For example, if overdraft fees are recurring, you can quickly spot this in reports and take corrective action, such as adjusting cash flow management practices.

One common pitfall to avoid is recording bank fees as part of a bank reconciliation instead of using the vendor system. While reconciling accounts, users often mistakenly enter fees directly into the reconciliation window, which can lead to uncategorized expenses and muddy financial records. Instead, always record fees through the vendor system, ensuring they are properly classified and traceable. This practice also aligns with accounting best practices, providing a clear audit trail for all bank-related transactions.

Finally, consider setting up recurring transactions for predictable bank fees, such as monthly service charges. QuickBooks allows you to automate these entries, saving time and reducing the risk of oversight. By treating your bank as a vendor and leveraging QuickBooks’ features, you can streamline the recording of bank fees, enhance financial accuracy, and gain deeper insights into your banking costs. This structured approach transforms a mundane task into a strategic tool for financial management.

DIY Ice Bank Chiller: Efficient Cooling for Sustainable Food Storage

You may want to see also

Explore related products

![]()

Bank Integration with Vendor Lists

In QuickBooks, banks are not typically classified as vendors in the traditional sense, but their integration with vendor lists can streamline financial management significantly. When you connect your bank account to QuickBooks, transactions such as payments to vendors are automatically imported, reducing manual data entry. This integration allows you to categorize expenses directly within the platform, ensuring that payments to vendors are accurately recorded in your vendor list. For instance, if you pay a supplier via direct deposit, QuickBooks can match the transaction to the corresponding vendor, maintaining a clear audit trail.

Analyzing this process reveals its efficiency in maintaining financial accuracy. By linking bank transactions to vendor profiles, QuickBooks minimizes errors that often arise from manual input. For example, if you regularly pay a vendor like "ABC Supplies," the system learns to recognize and categorize these transactions automatically. This not only saves time but also ensures consistency in your financial records. However, it’s crucial to periodically review these automated categorizations to catch any discrepancies, such as a payment mistakenly assigned to the wrong vendor.

To implement bank integration effectively, follow these steps: First, connect your bank account to QuickBooks via the "Banking" tab. Next, enable automatic transaction downloads, ensuring that new entries appear daily. Then, set up rules for categorizing transactions, such as assigning payments to specific vendors based on payee names. Finally, reconcile your accounts monthly to verify that all transactions are correctly matched to your vendor list. Pro tip: Use the "Rules" feature in QuickBooks to automate repetitive categorizations, such as recurring payments to utilities or suppliers.

A comparative analysis highlights the advantages of this integration over manual methods. Without bank integration, tracking vendor payments requires cross-referencing bank statements with QuickBooks entries, a time-consuming process prone to errors. In contrast, automated integration provides real-time updates, allowing you to monitor cash flow and vendor expenses seamlessly. For small businesses, this can mean the difference between spending hours on bookkeeping and focusing on core operations.

In conclusion, while banks are not vendors in QuickBooks, their integration with vendor lists is a powerful tool for financial management. By automating transaction categorization and reducing manual effort, this feature enhances accuracy and efficiency. Whether you’re a small business owner or a financial manager, leveraging bank integration can transform how you track and manage vendor payments, ultimately contributing to better financial health.

Mastering Bank Reconciliation: Tips to Balance Statements Seamlessly

You may want to see also

Frequently asked questions

Yes, a bank can be set up as a vendor in QuickBooks if you need to track payments, fees, or other transactions related to the bank.

Adding your bank as a vendor allows you to record bank fees, loan payments, or other expenses associated with the bank in a structured way.

Yes, you can connect your bank account directly to QuickBooks for automatic transaction downloads, but adding the bank as a vendor is separate and used for tracking specific expenses.

Go to the Vendor Center, click "New Vendor," and enter the bank’s details. Ensure to categorize transactions appropriately when using the bank as a vendor.

![Quicken Classic Deluxe for New Subscribers| 1 Year [PC/Mac Online Code]](https://m.media-amazon.com/images/I/61ypcFpjCuL._AC_UL320_.jpg)

![Quickbooks Online For Beginners [10 In 1]: The Complete Visual Guide to Mastering QuickBooks Fast. Automate Your Finances, Stay Tax-Ready, and Take Control of Your Business in 30 Days or Less.](https://m.media-amazon.com/images/I/718cpZEH4-L._AC_UL320_.jpg)