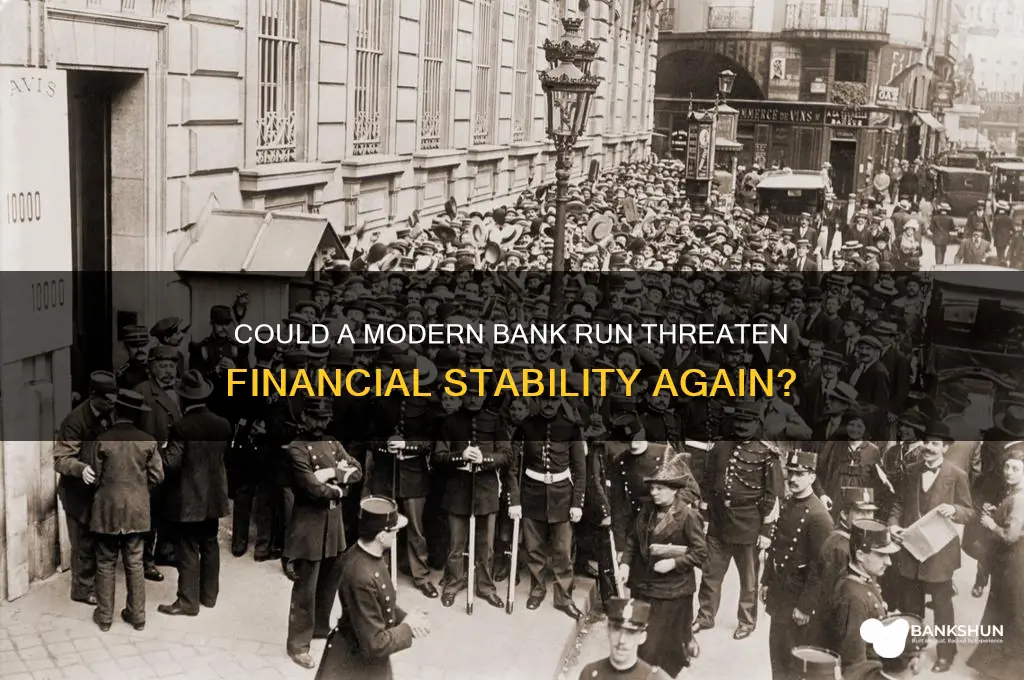

In recent years, the stability of the global financial system has been a topic of growing concern, prompting many to ask whether a run on the banks is possible in today's interconnected economy. A bank run occurs when a large number of customers withdraw their deposits simultaneously due to fears of insolvency, potentially leading to a self-fulfilling prophecy of financial collapse. While modern banking systems have safeguards like deposit insurance and central bank interventions to mitigate such risks, the rise of digital banking, rapid information dissemination, and economic uncertainties have introduced new vulnerabilities. Examining historical precedents, regulatory frameworks, and the role of technology is essential to understanding whether a bank run remains a plausible threat in the 21st century.

| Characteristics | Values |

|---|---|

| Current Economic Climate | Mixed signals: strong job market but persistent inflation, rising interest rates, and geopolitical tensions. |

| Bank Liquidity | Generally stable, with banks holding higher reserves post-2008 financial crisis. |

| Deposit Insurance | FDIC (US) insures deposits up to $250,000 per depositor, per insured bank, reducing panic withdrawal incentives. |

| Digital Banking | Faster withdrawal capabilities through online banking could accelerate a run, but also allows for quicker central bank intervention. |

| Central Bank Response | Central banks (e.g., Federal Reserve) have tools like lender-of-last-resort facilities and interest rate adjustments to stabilize banks. |

| Public Confidence | Largely intact, though sensitive to news of bank failures or economic downturns. |

| Regulatory Environment | Stricter regulations post-2008 (e.g., Dodd-Frank Act) aim to prevent systemic risks, but loopholes and new risks (e.g., shadow banking) exist. |

| Historical Precedents | Rare in recent decades due to improved safeguards, but examples like Silicon Valley Bank (2023) show vulnerabilities. |

| Global Interconnectedness | A run in one country could spread internationally due to globalized financial systems. |

| Market Sentiment | Volatile, influenced by media, social media, and economic indicators. |

| Probability of a Run | Low in the short term, but risks increase during severe economic shocks or loss of confidence in financial institutions. |

Explore related products

What You'll Learn

- Current banking regulations and their effectiveness in preventing bank runs

- Impact of digital banking on the likelihood of bank runs

- Historical examples of bank runs and their causes

- Role of central banks in stabilizing financial systems during crises

- Psychological factors driving panic and bank run behavior

![]()

Current banking regulations and their effectiveness in preventing bank runs

Bank runs, historically triggered by panic and a loss of confidence in a bank's solvency, have led to catastrophic economic consequences. The Great Depression of the 1930s is a stark reminder of the devastation caused by widespread bank failures. To prevent such crises, modern banking regulations have been implemented globally, aiming to fortify the financial system against runs. These regulations include capital adequacy requirements, deposit insurance schemes, and liquidity standards, all designed to ensure banks can withstand shocks and maintain depositor trust. But how effective are these measures in today’s complex financial landscape?

Consider the Basel III framework, a cornerstone of global banking regulation, which mandates higher capital reserves and stricter liquidity ratios. By requiring banks to hold more capital, regulators aim to absorb losses without collapsing. For instance, the Common Equity Tier 1 (CET1) ratio, a key metric, must be at least 4.5% of risk-weighted assets, with an additional 2.5% buffer for systemically important banks. This means a bank with $100 billion in risk-weighted assets must hold at least $6.5 billion in high-quality capital. While these requirements enhance resilience, they do not eliminate the risk of a run entirely. During times of extreme stress, even well-capitalized banks can face liquidity shortages if depositors withdraw en masse.

Deposit insurance schemes, such as the Federal Deposit Insurance Corporation (FDIC) in the U.S., play a critical role in preventing runs by guaranteeing deposits up to a certain limit—currently $250,000 per depositor, per insured bank. This assurance reduces the incentive for depositors to withdraw funds during a crisis. However, the effectiveness of such schemes depends on public trust in the government’s ability to honor these guarantees. For example, during the 2008 financial crisis, the FDIC’s role was pivotal in stabilizing the banking system, but smaller, uninsured depositors in some countries faced significant losses, highlighting the limitations of such programs.

Another regulatory tool is stress testing, which assesses banks’ ability to withstand adverse economic scenarios. Central banks, such as the Federal Reserve, conduct annual stress tests to ensure banks can maintain sufficient capital and liquidity under severe conditions. While these tests improve transparency and preparedness, they rely on assumptions that may not reflect real-world complexities. For instance, a sudden, unexpected event like a pandemic can expose vulnerabilities not captured in standard stress test scenarios.

Despite these regulations, the rise of digital banking and social media has introduced new challenges. Viral misinformation or rapid online withdrawals can accelerate a run, as seen in the 2023 collapse of Silicon Valley Bank, where a liquidity crisis was exacerbated by social media-driven panic. This incident underscores the need for regulators to adapt to technological advancements and ensure real-time monitoring of deposit flows.

In conclusion, current banking regulations have significantly reduced the likelihood of bank runs by enhancing capital buffers, guaranteeing deposits, and improving oversight. However, their effectiveness is not absolute. Regulators must continually evolve their approaches to address emerging risks, such as those posed by digital banking and systemic interconnectedness. While a run on the banks remains possible, the combination of robust regulations and proactive measures can mitigate its impact and safeguard the financial system.

How to Stop ECS in Kotak Bank: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Impact of digital banking on the likelihood of bank runs

Digital banking has fundamentally altered the mechanics of bank runs by accelerating the speed at which depositors can withdraw funds. In traditional banking, a run required physical presence and queues, creating a natural delay that allowed banks or regulators to intervene. Today, with mobile apps and online platforms, mass withdrawals can occur within minutes, triggered by a viral tweet or news alert. For instance, during the 2023 banking crisis, Silicon Valley Bank experienced a $42 billion withdrawal in just 10 hours—a pace unprecedented in pre-digital eras. This immediacy amplifies the risk of self-fulfilling panics, as depositors act preemptively to avoid being last in line.

However, digital banking also introduces tools to mitigate run dynamics. Advanced algorithms can detect unusual withdrawal patterns in real time, enabling banks to freeze accounts temporarily or alert regulators. Central banks can now inject liquidity faster through digital channels, as seen in the European Central Bank’s 2021 pilot of instant payment systems for crisis response. Additionally, open banking APIs allow for rapid collateralization of assets, providing banks with alternative funding sources before a run escalates. These technological safeguards, when paired with robust regulatory frameworks, can theoretically reduce the likelihood of a full-scale run.

A critical paradox emerges when considering the role of digital-only banks, which hold no physical branches. While their reliance on online platforms increases vulnerability to cyber-driven panics, their asset structures often differ from traditional banks. For example, neobanks like Revolut or Chime frequently invest in highly liquid, short-term assets, ensuring quicker access to cash reserves. Yet, their lack of physical presence removes a psychological barrier—depositors cannot "see" the bank’s stability, making them more susceptible to herd behavior. This duality highlights how digital banking both exacerbates and mitigates run risks depending on institutional design.

To minimize run risks in the digital age, banks and regulators must adopt a three-pronged strategy. First, implement behavioral nudges within banking apps, such as mandatory 24-hour cooling-off periods for large withdrawals or transparent dashboards displaying real-time liquidity ratios. Second, mandate stress testing for digital-only banks, focusing on their ability to handle algorithmic trading-induced volatility. Third, educate depositors through in-app simulations of run scenarios, emphasizing the role of deposit insurance schemes. By blending technology with behavioral economics, the financial system can harness digital banking’s efficiency without amplifying fragility.

South African Banking: Routing Numbers and You

You may want to see also

Explore related products

![]()

Historical examples of bank runs and their causes

Bank runs are not mere relics of financial history; they are recurring phenomena with deep-rooted causes. One of the most infamous examples is the Great Depression-era bank runs of the 1930s. During this period, widespread economic uncertainty and a lack of deposit insurance led panicked depositors to withdraw their funds en masse. For instance, in 1931, over 2,000 banks failed in the United States alone, as customers feared losing their savings. This collective action exacerbated the economic downturn, turning a financial crisis into a societal one. The takeaway? Without safeguards like deposit insurance, even solvent banks can collapse under the weight of depositor panic.

Contrast the Great Depression with the 2007–2008 global financial crisis, where bank runs took a modern twist. Northern Rock, a British bank, faced a liquidity crisis in 2007 as rumors of its financial instability spread. Customers lined up outside branches to withdraw their savings, a scene reminiscent of the 1930s but amplified by 24/7 media coverage. Unlike earlier runs, this event was fueled by real-time information dissemination, highlighting how technological advancements can accelerate financial contagion. Governments responded swiftly with bailouts and guarantees, but the episode underscored the fragility of even modern banking systems.

A lesser-known but instructive example is the Overend Gurney crisis of 1866 in the United Kingdom. This investment bank’s collapse triggered a widespread panic, leading to bank runs across London. The cause? Overend Gurney had overextended itself in risky loans, and when it sought to raise capital by calling in its own loans, it sparked a liquidity crisis. This event led to the closure of several banks and businesses, illustrating how excessive risk-taking and opaque financial practices can sow the seeds of a run. The crisis also prompted regulatory reforms, a pattern seen in many historical bank runs.

In more recent history, the 2023 collapse of Silicon Valley Bank (SVB) serves as a cautionary tale. SVB’s heavy exposure to long-term Treasury bonds and its concentration in the tech sector left it vulnerable to rising interest rates and a slowdown in venture capital funding. When depositors, primarily tech startups, began withdrawing funds, the bank’s liquidity dried up within days. This run was unique in its speed, driven by digital transactions and social media-fueled panic. It highlights how sector-specific risks and rapid technological changes can create new vulnerabilities in banking systems.

Analyzing these examples reveals a common thread: bank runs are often the result of a loss of confidence, whether due to economic uncertainty, risky practices, or external shocks. While regulatory measures like deposit insurance and central bank interventions have mitigated their frequency, they remain a possibility in today’s interconnected financial landscape. The key to prevention lies in transparency, robust risk management, and swift policy responses. History shows that ignoring these lessons can turn a bank run into a full-blown financial crisis.

Mastering the Art of Writing a Bank Confirmation Letter

You may want to see also

Explore related products

![]()

Role of central banks in stabilizing financial systems during crises

Central banks serve as the backbone of financial stability, particularly during crises when the risk of a bank run looms large. A bank run occurs when a large number of customers withdraw their deposits simultaneously due to fears of a bank’s insolvency, creating a self-fulfilling prophecy of collapse. Central banks counter this through lender-of-last-resort functions, providing liquidity to banks facing temporary shortages. For instance, during the 2008 global financial crisis, the U.S. Federal Reserve injected trillions of dollars into the banking system to prevent systemic failure. This immediate liquidity support ensures banks can meet withdrawal demands, restoring depositor confidence and halting the run.

Beyond liquidity provision, central banks employ monetary policy tools to stabilize financial systems. By lowering interest rates or engaging in quantitative easing, they reduce borrowing costs and stimulate economic activity, easing the strain on banks. During the COVID-19 pandemic, central banks worldwide slashed rates to near-zero levels and expanded asset purchase programs, preventing a potential wave of bank runs caused by economic uncertainty. These measures not only stabilize banks but also support broader economic recovery, demonstrating the dual role of central banks in financial and macroeconomic stability.

Another critical function is regulatory oversight and stress testing. Central banks enforce prudential regulations, such as capital adequacy ratios and liquidity coverage ratios, to ensure banks maintain sufficient buffers against shocks. Stress tests, like those conducted by the European Central Bank, simulate extreme scenarios to assess banks’ resilience. These measures reduce the likelihood of bank runs by ensuring banks are robust enough to withstand crises. For example, post-2008 reforms under Basel III significantly strengthened global banking standards, making systems less vulnerable to runs.

Finally, central banks act as communicators and coordinators, providing clarity and confidence during turbulent times. Clear, transparent messaging about policy actions and financial conditions can calm markets and prevent panic. During the 2023 banking turmoil involving Silicon Valley Bank, the Federal Reserve’s swift communication and coordinated response with other regulators helped contain the crisis. This role underscores the importance of central banks not just as policymakers but as trusted institutions capable of guiding the public and markets through uncertainty.

In summary, central banks are indispensable in stabilizing financial systems during crises, employing a combination of liquidity support, monetary policy, regulatory oversight, and communication strategies. Their actions mitigate the risk of bank runs by addressing immediate liquidity needs, strengthening systemic resilience, and fostering confidence. As financial systems grow more complex, the role of central banks in preventing and managing crises remains more critical than ever.

Easy Steps to Flatten a Banker's Box for Compact Storage

You may want to see also

Explore related products

![Collapse( How Societies Choose to Fail or Succeed)[COLLAPSE][Paperback]](https://m.media-amazon.com/images/I/71KdH5D8O4L._AC_UY218_.jpg)

![]()

Psychological factors driving panic and bank run behavior

Bank runs are not merely financial phenomena; they are deeply rooted in human psychology. At the core of such events lies herd behavior, a psychological tendency where individuals mimic the actions of others, assuming they possess more information. When a few customers withdraw funds due to uncertainty, others observe and follow suit, creating a self-perpetuating cycle. This behavior is amplified by cognitive biases like the availability heuristic, where recent news of bank failures makes such events seem more probable, even if statistically rare. For instance, during the 2008 financial crisis, media coverage of bank collapses triggered widespread panic, leading to runs on institutions like Northern Rock in the UK.

Another critical factor is information asymmetry, where depositors lack complete knowledge about a bank’s financial health. This uncertainty breeds anxiety, as individuals fear being the last to withdraw funds before a potential collapse. Psychologically, this is tied to loss aversion, a principle from behavioral economics where the pain of losing is twice as powerful as the pleasure of gaining. Depositors act preemptively to avoid losses, even if the bank is fundamentally sound. For example, during the Great Depression, rumors of bank insolvency spread rapidly, causing mass withdrawals despite federal assurances.

Social proof further exacerbates bank run behavior. When individuals see long lines outside banks or hear of others withdrawing funds, they interpret this as evidence of trouble, regardless of the bank’s actual condition. This phenomenon is particularly potent in the digital age, where social media accelerates the spread of panic. A single viral tweet or post can trigger a cascade of withdrawals, as seen in the 2023 collapse of Silicon Valley Bank, where online chatter fueled a rapid loss of depositor confidence.

To mitigate such behavior, banks and regulators must address these psychological drivers. Transparent communication is key; providing clear, timely information about a bank’s stability can reduce uncertainty and counteract herd behavior. For instance, during the 2008 crisis, governments that swiftly communicated bailout plans and deposit guarantees successfully calmed markets. Additionally, behavioral nudges can be employed, such as framing deposit insurance as a safety net rather than a last resort, reducing loss aversion. Finally, education plays a vital role; teaching the public about fractional reserve banking and the rarity of bank failures can temper irrational panic.

In conclusion, understanding the psychological factors behind bank runs—herd behavior, cognitive biases, information asymmetry, and social proof—is essential for preventing such events. By addressing these drivers through transparency, behavioral interventions, and education, financial institutions and policymakers can build resilience against the panic that fuels bank runs.

How to Easily View Your Commerce Bank PIN: A Quick Guide

You may want to see also

Frequently asked questions

Yes, a run on the banks is still possible, though modern safeguards like deposit insurance, central bank support, and stricter regulations reduce the likelihood. However, economic instability, loss of confidence, or systemic shocks could trigger such an event.

A run on the banks is typically caused by widespread fear or panic among depositors, who believe the bank may fail or be unable to meet withdrawal demands. Triggers include economic crises, rumors, or actual financial instability.

In many countries, bank deposits are protected up to certain limits by deposit insurance schemes (e.g., FDIC in the U.S.). However, during a severe run, there could be delays in accessing funds, and uninsured deposits may be at risk.

Governments and central banks can prevent a run by ensuring adequate liquidity, providing deposit insurance, communicating transparently to maintain public confidence, and implementing robust regulatory frameworks to stabilize the financial system.