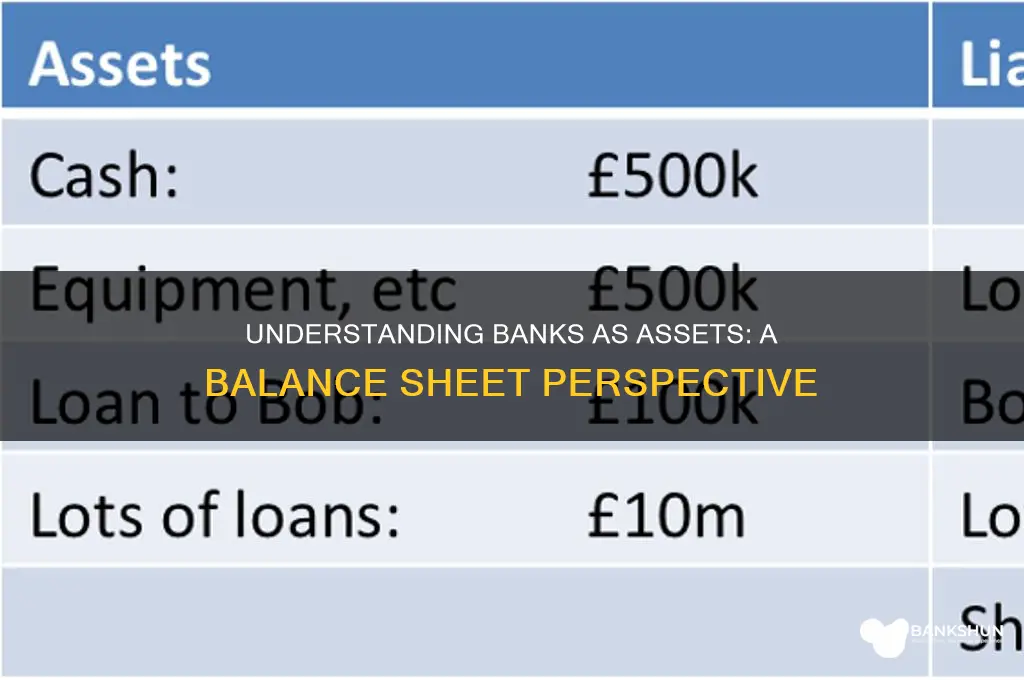

The question of whether a bank is considered an asset on a balance sheet is a nuanced one, as it depends on the perspective of the entity preparing the financial statement. From a bank's own balance sheet, its assets include cash, loans, securities, and other financial instruments it owns or controls, which are used to generate revenue. However, from the perspective of a customer or another institution, a bank account or a loan from a bank would be recorded as an asset on their balance sheet, representing the value they hold or the funds they have access to. This distinction highlights the dual role of banks in financial reporting, acting both as asset holders and as providers of assets to others.

Explore related products

What You'll Learn

- Bank Assets Overview: Cash, loans, securities, and other holdings banks own, reflecting financial strength

- Cash and Equivalents: Highly liquid assets like currency, deposits, and short-term investments

- Loans and Advances: Money lent to customers, a major asset generating interest income

- Securities Portfolio: Bonds, stocks, and other investments held for income or trading

- Fixed Assets: Physical properties, equipment, and long-term investments owned by the bank

![]()

Bank Assets Overview: Cash, loans, securities, and other holdings banks own, reflecting financial strength

Banks are not assets on a balance sheet; rather, they are entities that hold assets, which are crucial indicators of their financial health and operational capacity. A bank’s balance sheet is a snapshot of its financial position, divided into assets, liabilities, and equity. The asset side of this equation is particularly revealing, as it showcases what the bank owns and how it generates revenue. Among these assets, cash, loans, securities, and other holdings stand out as the primary components that define a bank’s financial strength and stability.

Cash and Cash Equivalents: The Liquidity Backbone

Cash is the most liquid asset a bank holds, encompassing physical currency, reserves held at central banks, and funds in short-term accounts. For instance, a bank might hold 5-10% of its total assets in cash to meet daily operational demands and regulatory requirements. This liquidity ensures the bank can honor withdrawals and settle transactions promptly. However, excessive cash holdings can indicate inefficiency, as idle cash generates minimal returns. Banks must strike a balance, often using tools like overnight lending to optimize cash utilization without compromising liquidity.

Loans: The Revenue Engine

Loans are the lifeblood of a bank’s profitability, typically comprising 50-70% of its assets. These include mortgages, personal loans, business loans, and credit card debt. Each loan carries a risk-return trade-off; for example, mortgages are generally low-risk but low-yield, while business loans offer higher returns but come with greater default risk. Banks employ credit scoring models and diversification strategies to manage this risk. A healthy loan portfolio reflects robust underwriting standards and a strong economy, while rising defaults can signal financial distress.

Securities: Diversification and Stability

Securities, such as government bonds, corporate bonds, and equities, provide banks with diversification and a stable income stream. For instance, U.S. Treasury bonds are considered risk-free and offer predictable returns, making them a staple in bank portfolios. However, securities are subject to market fluctuations; a sudden rise in interest rates can devalue bond holdings. Banks must carefully manage their securities portfolio to align with their risk appetite and regulatory capital requirements, often using duration analysis to mitigate interest rate risk.

Other Holdings: The Strategic Buffer

Beyond cash, loans, and securities, banks hold other assets like property, equipment, and intangible assets (e.g., software, intellectual property). While these represent a smaller portion of total assets (typically <10%), they serve strategic purposes. For example, owning branch locations enhances customer accessibility, while investments in technology improve operational efficiency. These holdings are less liquid and harder to value but contribute to the bank’s long-term growth and competitive edge.

Takeaway: A Balanced Portfolio Reflects Financial Strength

A bank’s asset composition is a delicate balance of liquidity, profitability, and risk management. Cash ensures operational readiness, loans drive revenue, securities provide stability, and other holdings support strategic goals. Investors and regulators scrutinize this mix to assess a bank’s resilience and growth potential. For instance, a bank with a high cash ratio might be perceived as conservative but underperforming, while one heavily weighted in loans could face heightened credit risk. Understanding these dynamics is key to evaluating a bank’s financial strength and its ability to weather economic uncertainties.

Does Citizen Bank Charge Cancellation Fees? What You Need to Know

You may want to see also

Explore related products

![]()

Cash and Equivalents: Highly liquid assets like currency, deposits, and short-term investments

Banks, as financial institutions, play a unique role in the economy, and their balance sheets reflect this distinct function. One of the most critical components of a bank's balance sheet is Cash and Equivalents, which encompasses highly liquid assets such as currency, deposits, and short-term investments. These assets are the lifeblood of a bank’s operations, ensuring it can meet immediate obligations and maintain liquidity. Unlike other businesses, where cash might represent a smaller portion of assets, banks rely heavily on these liquid resources to facilitate transactions, manage reserves, and maintain trust in the financial system.

Consider the practical implications: a bank’s cash and equivalents are not merely idle funds but active tools for stability and growth. For instance, a bank’s deposits with central banks, such as the Federal Reserve, are part of this category and serve as a buffer against liquidity crises. Similarly, short-term investments like Treasury bills or certificates of deposit provide a quick return while remaining easily convertible to cash. These assets are typically held for three months or less, ensuring they remain highly liquid. For investors and stakeholders, understanding this segment of the balance sheet is crucial, as it directly reflects a bank’s ability to withstand financial shocks and support lending activities.

From an analytical perspective, the proportion of cash and equivalents on a bank’s balance sheet can reveal its strategic priorities. A higher ratio might indicate a conservative approach, focusing on risk mitigation and regulatory compliance, while a lower ratio could suggest a more aggressive stance, prioritizing lending and investment opportunities. However, this balance is delicate. Excessive reliance on cash and equivalents can limit profitability, as these assets yield lower returns compared to loans or long-term investments. Conversely, insufficient liquidity can expose a bank to significant risk during economic downturns. Striking the right balance is an art, requiring careful monitoring of market conditions and regulatory requirements.

For individuals and businesses, understanding a bank’s cash and equivalents can inform decision-making. For example, a bank with robust liquidity is more likely to offer stable services, such as uninterrupted access to deposits and reliable loan approvals. Conversely, a bank with strained liquidity might impose restrictions or increase fees to manage its cash flow. Practical tips include reviewing a bank’s financial statements, particularly the liquidity coverage ratio (LCR), which measures its ability to cover short-term obligations. A higher LCR generally indicates stronger liquidity, though it’s essential to consider this in the context of the bank’s overall financial health and market conditions.

In conclusion, cash and equivalents are not just a line item on a bank’s balance sheet but a cornerstone of its operational resilience. They embody the bank’s ability to navigate uncertainty, support economic activity, and maintain trust. Whether you’re an investor, a customer, or a financial professional, recognizing the significance of these highly liquid assets provides valuable insights into a bank’s stability and strategic direction. By focusing on this critical component, one can better assess a bank’s capacity to fulfill its role in the financial ecosystem.

Is Scoring 60 on Section Banks Good Enough for Success?

You may want to see also

Explore related products

![]()

Loans and Advances: Money lent to customers, a major asset generating interest income

Banks, unlike traditional businesses, have a unique balance sheet structure where their primary assets are not physical goods or inventory but financial instruments. Among these, loans and advances stand out as the cornerstone of a bank’s asset portfolio. These represent money lent to customers, whether individuals, businesses, or governments, with the expectation of repayment plus interest. This category is not just a line item on the balance sheet; it is the lifeblood of a bank’s revenue stream, generating the bulk of its interest income. For instance, in 2022, loans and advances accounted for over 60% of total assets for major U.S. banks, underscoring their critical role in banking operations.

To understand the significance of loans and advances, consider their dual function: they serve as a tool for economic growth by providing liquidity to borrowers while simultaneously acting as a profit engine for banks. When a bank extends a loan, it creates an asset that earns interest over time. This interest income is a predictable and stable revenue source, making loans and advances a preferred asset class for banks. However, this asset is not without risk. The quality of the loan portfolio—measured by factors like creditworthiness of borrowers, loan-to-value ratios, and repayment terms—directly impacts a bank’s financial health. For example, a mortgage loan with a 20% down payment is generally considered less risky than an unsecured personal loan, as the former is backed by collateral.

From a strategic perspective, banks must carefully manage their loans and advances to balance risk and reward. Diversification is key; lending across various sectors (e.g., real estate, small businesses, corporate loans) and borrower profiles (e.g., prime vs. subprime) can mitigate concentration risk. Additionally, banks employ stringent underwriting standards and continuous monitoring to ensure loan quality. For instance, a bank might use credit scoring models to assess borrower reliability or require collateral for larger loans. These practices not only protect the asset’s value but also ensure a steady flow of interest income.

A practical takeaway for stakeholders is that loans and advances are not just a reflection of a bank’s lending activity but a critical indicator of its financial performance and stability. Investors, regulators, and customers alike should scrutinize this asset category when evaluating a bank’s health. High growth in loans and advances, for example, could signal aggressive lending practices, while a sudden decline might indicate economic distress or tightening credit standards. By understanding the dynamics of this asset, one can gain deeper insights into a bank’s operational strategy and risk exposure.

In conclusion, loans and advances are far more than a balance sheet entry; they are a dynamic asset class that drives bank profitability and supports economic activity. Their management requires a delicate balance of risk assessment, diversification, and strategic foresight. As the primary source of interest income, they underscore the unique role banks play in the financial ecosystem, bridging the gap between surplus and deficit units of the economy. Whether you’re an investor, a regulator, or a borrower, recognizing the importance of this asset is essential to navigating the complexities of banking.

Do Banks Process Transactions on Sundays? What You Need to Know

You may want to see also

Explore related products

![]()

Securities Portfolio: Bonds, stocks, and other investments held for income or trading

Banks hold securities portfolios as a strategic asset class, comprising bonds, stocks, and other investments. These holdings serve dual purposes: generating income through dividends, interest, or capital gains, and facilitating trading activities to capitalize on market fluctuations. Unlike traditional loans, securities offer diversification, liquidity, and the potential for higher returns, albeit with varying degrees of risk. For instance, U.S. Treasury bonds are considered low-risk, income-generating assets, while equity investments in volatile sectors like technology can yield significant but unpredictable returns.

Analyzing a bank’s securities portfolio reveals its risk appetite and liquidity management strategy. Bonds, particularly government or investment-grade corporate issues, provide stable cash flows and act as a buffer during economic downturns. Conversely, stocks and riskier assets like derivatives or mortgage-backed securities amplify exposure to market volatility but can enhance profitability in favorable conditions. Regulatory frameworks, such as the Basel III accords, impose capital requirements on these holdings to mitigate systemic risks, ensuring banks maintain sufficient reserves against potential losses.

Practical management of a securities portfolio involves balancing yield and risk. Banks often categorize holdings into "held-to-maturity" (long-term income) and "available-for-sale" (trading or short-term gains) buckets. For example, a regional bank might allocate 60% of its portfolio to government bonds for stability, 30% to blue-chip stocks for moderate growth, and 10% to high-yield corporate bonds for added income. Regular portfolio rebalancing ensures alignment with market conditions and strategic objectives, while stress testing evaluates resilience under adverse scenarios.

A persuasive argument for securities portfolios lies in their role as a counterbalance to traditional banking activities. While loans tie up capital for extended periods, securities provide liquidity and flexibility. For instance, during the 2020 market downturn, banks with diversified portfolios could sell government bonds to meet withdrawal demands, avoiding liquidity crises. However, over-reliance on volatile assets can erode shareholder value, as seen in the 2008 financial crisis when toxic securities led to massive write-downs. Thus, prudent diversification and risk assessment are paramount.

In conclusion, a bank’s securities portfolio is a dynamic asset class that enhances income, liquidity, and risk management. By strategically allocating to bonds, stocks, and other investments, banks can optimize returns while safeguarding stability. However, this requires rigorous oversight, adherence to regulatory standards, and a clear understanding of market dynamics. For stakeholders, transparency in portfolio composition and risk exposure is essential to assess a bank’s financial health and resilience.

Activate China Bank Mobile Banking: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Fixed Assets: Physical properties, equipment, and long-term investments owned by the bank

Banks, like any other business, maintain a balance sheet that reflects their financial health. A critical component of this balance sheet is fixed assets, which encompass physical properties, equipment, and long-term investments owned by the bank. These assets are not held for resale but are essential for the bank’s operations and long-term growth. Unlike liquid assets such as cash or short-term investments, fixed assets are tangible or intangible items with a useful life extending beyond a single accounting period. Understanding their role provides insight into a bank’s stability and strategic direction.

Physical properties, such as bank branches, corporate offices, and data centers, form the backbone of a bank’s operational infrastructure. These assets are capitalized on the balance sheet and depreciated over time to reflect their decreasing value. For instance, a newly constructed branch building might be depreciated over 25–30 years, aligning with its expected useful life. Equipment, including ATMs, servers, and security systems, is another category of fixed assets. These items are vital for delivering services efficiently and securely. Banks must regularly update and maintain this equipment to stay competitive and compliant with regulatory standards.

Long-term investments, while not always tangible, are equally significant. These include stakes in subsidiaries, joint ventures, or strategic partnerships that align with the bank’s growth objectives. For example, a bank might invest in a fintech startup to enhance its digital banking capabilities. Such investments are recorded at cost or fair value, depending on accounting standards, and are reviewed periodically for impairment. Unlike physical assets, these investments generate returns through dividends, capital gains, or strategic synergies, contributing to the bank’s overall profitability.

Analyzing fixed assets provides a window into a bank’s operational efficiency and strategic priorities. A high proportion of fixed assets relative to total assets may indicate significant investment in infrastructure, which could signal expansion plans or modernization efforts. Conversely, a low ratio might suggest a focus on lean operations or reliance on third-party services. Investors and stakeholders should scrutinize the composition and depreciation schedules of these assets to assess the bank’s ability to generate long-term value.

In practice, managing fixed assets requires careful planning and oversight. Banks must balance capital expenditures with operational needs, ensuring that investments in properties, equipment, and long-term ventures align with their strategic goals. Regular audits and impairment tests are essential to maintain the accuracy of the balance sheet. For instance, a bank might reassess the value of a branch in a declining market area and adjust its carrying value accordingly. By effectively managing fixed assets, banks can optimize their resource allocation, enhance operational resilience, and position themselves for sustained growth.

Does Walden Savings Bank Drug Test Employees? What You Need to Know

You may want to see also

Frequently asked questions

No, a bank itself is not an asset on a balance sheet. However, a company’s cash held in a bank account is recorded as an asset on its balance sheet.

Cash in a bank account is classified as an asset because it represents a resource owned by the company that has future economic value and can be used to settle liabilities or fund operations.

No, a bank’s customers’ deposits are recorded as liabilities on the bank’s balance sheet, not assets. The bank’s assets include loans, securities, and cash reserves.

A bank is a financial institution that provides services like holding deposits and issuing loans. It is not an asset itself but rather a custodian of assets (e.g., cash) that a company may hold in its accounts.

Yes, a bank’s loans are considered assets on its balance sheet because they represent amounts owed to the bank by borrowers, which generate interest income and have future economic value.