The terms bank rate and repo rate are often used in discussions about monetary policy and interest rates, but they are not the same. The bank rate, also known as the discount rate, is the interest rate at which a central bank lends money to commercial banks without any collateral, typically as a last resort to manage liquidity crises. On the other hand, the repo rate (repurchase rate) is the rate at which the central bank lends money to commercial banks against government securities, with an agreement to repurchase them at a later date. While both rates influence borrowing costs and liquidity in the banking system, they serve different purposes and operate under distinct mechanisms, making them distinct tools in a central bank's monetary policy toolkit.

Explore related products

What You'll Learn

- Definition Difference: Bank rate is lending rate to banks; repo rate is short-term borrowing rate

- Purpose Contrast: Bank rate controls long-term funds; repo rate manages liquidity daily

- Impact on Economy: Bank rate affects loans; repo rate influences inflation and cash flow

- Collateral Involvement: Repo rate involves securities; bank rate is unsecured lending

- Policy Tool Usage: Central banks adjust repo rate frequently; bank rate changes are rare

![]()

Definition Difference: Bank rate is lending rate to banks; repo rate is short-term borrowing rate

Central banks wield two critical tools to influence a nation's monetary policy: the bank rate and the repo rate. While both involve interest rates, their functions and impacts differ significantly. Understanding this distinction is crucial for anyone navigating the complexities of financial markets or simply seeking to grasp how central banks control money flow.

Bank rate, also known as the discount rate, is the interest rate at which a central bank lends money to commercial banks. This rate acts as a benchmark, influencing the interest rates banks charge their customers for loans. When the central bank raises the bank rate, borrowing becomes more expensive for banks, leading to higher loan rates for businesses and individuals. Conversely, a lower bank rate encourages banks to borrow more, potentially stimulating economic activity through increased lending.

Repo rate, short for repurchase rate, is the rate at which commercial banks borrow money from the central bank for short periods, typically overnight. This mechanism allows banks to meet their liquidity needs and maintain reserve requirements. Unlike the bank rate, which directly impacts long-term lending, the repo rate primarily affects short-term borrowing costs. A higher repo rate discourages banks from borrowing excessively, tightening the money supply and potentially curbing inflation. Conversely, a lower repo rate encourages borrowing, injecting liquidity into the system and stimulating economic growth.

In essence, the bank rate serves as a lever for controlling long-term interest rates and overall credit availability, while the repo rate acts as a fine-tuning tool for managing short-term liquidity and market stability. Both rates are interconnected, with changes in one often influencing the other. Central banks strategically adjust these rates to achieve specific economic objectives, such as controlling inflation, promoting growth, or stabilizing financial markets.

For instance, during an economic downturn, a central bank might lower both the bank rate and the repo rate to encourage borrowing, investment, and consumption. Conversely, in an overheating economy with rising inflation, the central bank might raise both rates to curb spending and cool down the economy. Understanding the distinct roles of bank rate and repo rate empowers individuals to decipher central bank actions and anticipate their impact on borrowing costs, investment opportunities, and overall economic conditions.

Promissory Notes: Are Banks Legally Bound to Accept Them?

You may want to see also

Explore related products

![]()

Purpose Contrast: Bank rate controls long-term funds; repo rate manages liquidity daily

Central banks wield two critical tools to steer economies: the bank rate and the repo rate. While both influence borrowing costs, their purposes diverge sharply. The bank rate, often called the discount rate, acts as a long-term anchor. Central banks adjust it to control the flow of credit over months or years, impacting investments, mortgages, and overall economic growth. Think of it as setting the baseline cost of money for extended periods. Conversely, the repo rate is a nimble instrument for daily liquidity management. It dictates the interest rate at which banks borrow from the central bank overnight, directly affecting short-term cash availability in the financial system. This rate is tweaked frequently to address immediate liquidity crunches or surpluses, ensuring stability in the banking sector.

Consider a scenario where an economy is overheating, with inflation rising due to excessive borrowing. The central bank might hike the bank rate, making long-term loans more expensive. This discourages businesses from taking on large projects and consumers from buying homes, thereby cooling down the economy over time. Simultaneously, if there’s a sudden liquidity shortage in the banking system, the central bank can lower the repo rate, encouraging banks to borrow more freely and maintain smooth operations. This dual approach allows central banks to address both structural and immediate financial challenges without over-relying on a single tool.

From a practical standpoint, understanding this distinction is crucial for investors and businesses. For instance, a rise in the bank rate signals tighter credit conditions ahead, which could dampen stock market returns and increase bond yields. Conversely, a repo rate cut might provide temporary relief to banks but doesn’t necessarily translate to lower long-term borrowing costs for businesses or individuals. Investors should monitor both rates but interpret them in their respective contexts: the bank rate for long-term economic trends and the repo rate for short-term market liquidity.

A comparative analysis reveals the complementary nature of these tools. While the bank rate influences the cost of long-term funds, shaping investment decisions and consumer behavior, the repo rate acts as a daily thermostat for liquidity, ensuring banks can meet their immediate obligations. For example, during the 2008 financial crisis, central banks slashed both rates: the bank rate to stimulate long-term borrowing and investment, and the repo rate to prevent a liquidity freeze in the banking system. This coordinated approach highlights how these tools work in tandem to stabilize economies under stress.

In conclusion, the bank rate and repo rate are not interchangeable but serve distinct purposes. The bank rate is a strategic lever for long-term economic management, while the repo rate is a tactical tool for daily liquidity control. By understanding their unique roles, stakeholders can better navigate financial markets and anticipate policy impacts. Whether you’re a policymaker, investor, or business owner, recognizing this purpose contrast is key to making informed decisions in an ever-changing economic landscape.

American Banks in Mexico: Where to Find Them

You may want to see also

Explore related products

![]()

Impact on Economy: Bank rate affects loans; repo rate influences inflation and cash flow

Bank rate and repo rate, though often mentioned together, serve distinct purposes in an economy. The bank rate, also known as the discount rate, is the interest rate at which a central bank lends money to commercial banks without any collateral. This rate directly impacts the cost of loans for businesses and individuals. When the bank rate increases, borrowing becomes more expensive, leading to reduced loan demand and slower economic growth. Conversely, a lower bank rate encourages borrowing, stimulating economic activity. For instance, a 1% increase in the bank rate can lead to a 5-10% decline in loan applications, particularly in sectors like housing and small businesses, which are highly sensitive to interest rate changes.

The repo rate, on the other hand, is the rate at which commercial banks borrow money from the central bank by selling securities, with an agreement to repurchase them at a later date. This tool is primarily used to control inflation and manage liquidity in the economy. A higher repo rate makes borrowing more costly for banks, reducing the money supply and curbing inflationary pressures. For example, during periods of high inflation, central banks often raise the repo rate by 0.5-1% to cool down the economy. This action can lead to a 2-3% decrease in inflation over a 6-12 month period, as observed in several emerging economies.

To illustrate the interplay, consider a scenario where a central bank raises both the bank rate and the repo rate simultaneously. The increased bank rate would make loans more expensive for consumers and businesses, potentially slowing down investment and consumption. Simultaneously, the higher repo rate would reduce the liquidity in the banking system, further tightening credit availability. This dual action could effectively curb inflation but might also risk stifling economic growth if not carefully calibrated. Central banks often use these tools in tandem, adjusting them in increments of 0.25-0.5% to balance inflation control and economic stability.

Practical tips for businesses and individuals include monitoring central bank announcements closely, as even small changes in these rates can have significant implications. For instance, if a repo rate hike is anticipated, businesses might consider securing short-term loans beforehand to avoid higher costs later. Similarly, individuals planning to take out mortgages should assess their financial flexibility, as bank rate increases can substantially raise monthly repayments. Financial planners often advise clients to maintain a buffer of 6-12 months’ worth of loan repayments to navigate such rate fluctuations.

In conclusion, while both the bank rate and repo rate are monetary policy tools, their impacts on the economy differ markedly. The bank rate directly influences the cost of loans, shaping consumer and business spending, whereas the repo rate primarily affects inflation and cash flow by controlling liquidity. Understanding these distinctions is crucial for policymakers, businesses, and individuals alike, as it enables better decision-making in response to central bank actions. By staying informed and proactive, stakeholders can mitigate risks and capitalize on opportunities arising from these rate changes.

Aspiration Bank: International Transaction Fees Explained

You may want to see also

Explore related products

![]()

Collateral Involvement: Repo rate involves securities; bank rate is unsecured lending

The repo rate and bank rate, though both monetary policy tools, differ fundamentally in their collateral requirements. The repo rate operates within a secured lending framework, where the borrower—typically a commercial bank—pledges government securities as collateral to the central bank. This arrangement minimizes risk for the central bank, ensuring that even in default, the securities can be liquidated to recover funds. In contrast, the bank rate involves unsecured lending, where the central bank extends credit to commercial banks without requiring collateral. This distinction highlights the repo rate’s role in managing liquidity with a safety net, while the bank rate reflects a higher degree of trust and systemic stability.

Consider the mechanics of a repo transaction: a commercial bank sells securities to the central bank with an agreement to repurchase them at a later date, usually overnight or within a short term. The difference between the sale and repurchase prices represents the interest paid, effectively the repo rate. This process is akin to a pawnshop transaction but with high-quality securities as the pawned item. The bank rate, however, operates more like an unsecured personal loan, where the central bank relies on the borrower’s creditworthiness rather than tangible assets. For instance, if a bank borrows ₹100 crore at a 5% bank rate, it owes ₹105 crore without posting any collateral, whereas a repo transaction would require securities worth, say, ₹110 crore as a buffer.

This collateral involvement has practical implications for banks and the broader economy. When the central bank adjusts the repo rate, it directly influences the cost of secured borrowing, which banks use to manage short-term liquidity needs. A lower repo rate encourages banks to borrow more, injecting liquidity into the system, while a higher rate tightens liquidity. The bank rate, being unsecured, is less frequently adjusted and primarily serves as a benchmark for other lending rates. For example, a central bank might raise the bank rate to curb inflation, signaling to commercial banks to reduce lending, even though this lending is unsecured and riskier.

From a strategic perspective, central banks use these tools differently. The repo rate is a more precise instrument for fine-tuning liquidity, given its collateralized nature and short-term focus. It allows central banks to respond swiftly to market fluctuations without exposing themselves to undue risk. The bank rate, by contrast, is a blunt tool, used sparingly to send broad signals about monetary policy stance. For banks, understanding this distinction is crucial: relying on repo transactions for short-term funding needs while factoring in the bank rate’s impact on long-term borrowing costs.

In practice, banks must balance their use of repo and bank rate facilities based on their liquidity profiles and risk appetites. For instance, a bank with a surplus of eligible securities might prefer repo transactions to optimize costs, while another with limited collateral may turn to the bank rate despite its higher cost. Policymakers, meanwhile, must calibrate these rates carefully to avoid unintended consequences. A steep repo rate hike could squeeze liquidity excessively, while a high bank rate might stifle credit growth. Ultimately, the collateralized nature of the repo rate and the unsecured character of the bank rate make them complementary yet distinct tools in the central bank’s arsenal.

Can Employers Legally Access Your Bank Account? Privacy Concerns Explained

You may want to see also

Explore related products

![]()

Policy Tool Usage: Central banks adjust repo rate frequently; bank rate changes are rare

Central banks wield a variety of tools to influence a nation's economy, with the repo rate and bank rate being two of the most prominent. While both are interest rates set by central banks, their functions, frequencies of adjustment, and impacts differ significantly. The repo rate, short for repurchase rate, is the rate at which commercial banks borrow money from the central bank by selling securities with an agreement to repurchase them at a later date. This rate is adjusted frequently, often in response to inflation, economic growth, and monetary policy objectives. In contrast, the bank rate, also known as the discount rate, is the interest rate charged by the central bank on loans to commercial banks without the need for collateral. Changes to the bank rate are rare, typically occurring only in response to severe economic conditions or systemic risks.

Consider the Reserve Bank of India (RBI), which adjusts its repo rate multiple times a year to manage inflation and stimulate economic activity. For instance, during the COVID-19 pandemic, the RBI reduced the repo rate from 5.15% in February 2020 to 4.00% by May 2020 to inject liquidity into the economy. Conversely, the bank rate remained unchanged at 4.65% during this period, reflecting its role as a more stable and less frequently adjusted tool. This example illustrates how central banks prioritize the repo rate for fine-tuning monetary policy while reserving bank rate changes for more critical or unusual circumstances.

The frequency of repo rate adjustments stems from its direct impact on lending rates and liquidity in the banking system. By lowering the repo rate, central banks encourage commercial banks to borrow more, which in turn increases the money supply and reduces borrowing costs for businesses and consumers. Conversely, raising the repo rate tightens liquidity, helping to curb inflation. This flexibility makes the repo rate an ideal tool for addressing short-term economic fluctuations. On the other hand, the bank rate serves as a backstop, providing a floor for lending rates and ensuring financial stability during crises. Its infrequent adjustments underscore its role as a last-resort measure rather than a routine policy tool.

For businesses and individuals, understanding these distinctions is crucial for financial planning. Frequent repo rate changes can directly affect loan EMIs, savings account interest, and investment returns, making it essential to monitor central bank announcements. For instance, a 25-basis-point reduction in the repo rate could lower monthly EMI payments on a ₹10 lakh home loan by approximately ₹150–₹200, depending on the loan tenure. In contrast, bank rate changes, though rare, can signal broader economic challenges, such as a credit crunch or financial instability, warranting a more cautious approach to borrowing and spending.

In conclusion, while both the repo rate and bank rate are central to monetary policy, their usage reflects distinct strategic priorities. The repo rate’s frequent adjustments make it a dynamic tool for managing inflation and economic growth, whereas the bank rate’s rarity of change highlights its role as a safeguard against systemic risks. By recognizing these differences, stakeholders can better navigate the economic landscape and make informed financial decisions.

Understanding Yes Bank's Share Count: A Comprehensive Overview

You may want to see also

Frequently asked questions

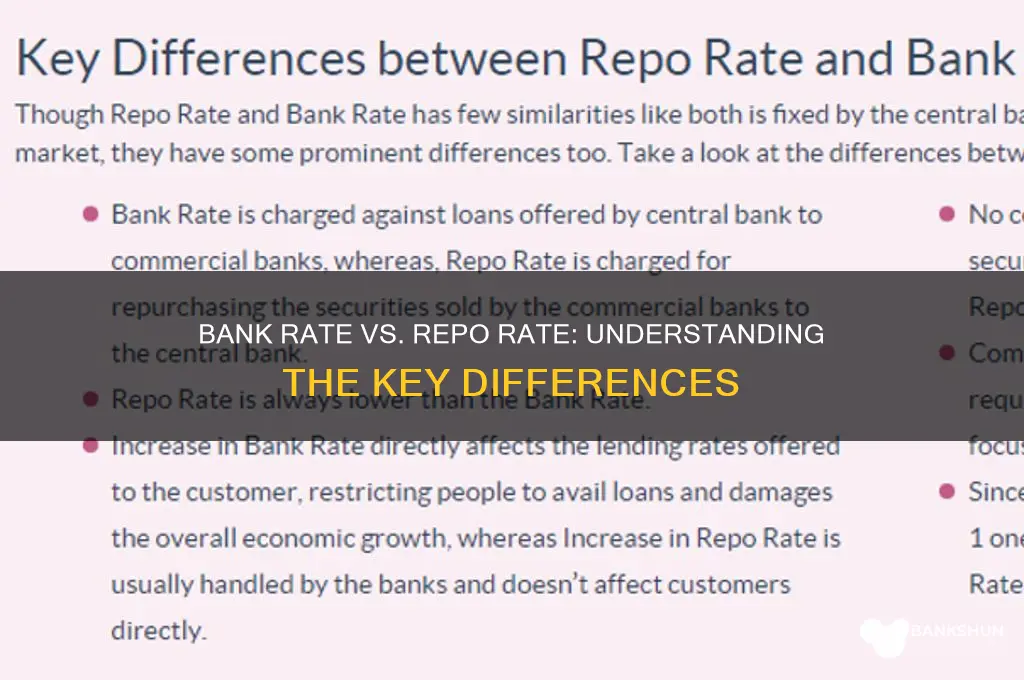

No, bank rate and repo rate are not the same. Bank rate is the interest rate at which the central bank lends money to commercial banks without any collateral, while repo rate is the rate at which the central bank lends money to commercial banks against government securities.

The primary difference is that bank rate involves unsecured lending (no collateral required), whereas repo rate involves secured lending (backed by government securities).

Bank rate directly influences the cost of borrowing for banks, which can affect lending rates for consumers and businesses. Repo rate, on the other hand, primarily controls liquidity in the banking system and influences short-term interest rates.

No, central banks use bank rate and repo rate for different purposes. Repo rate is more commonly used for liquidity management, while bank rate is often used as a signaling tool for broader monetary policy.

Yes, changes in both rates can indirectly affect loan interest rates. An increase in repo rate or bank rate typically leads to higher borrowing costs for banks, which may be passed on to consumers in the form of higher loan rates.