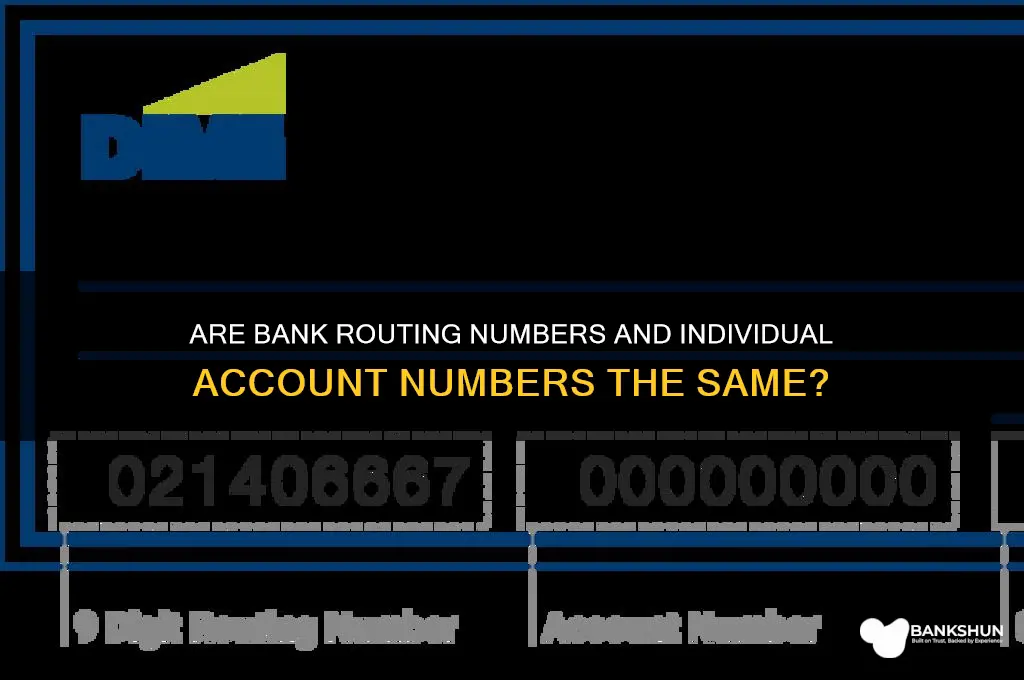

The question of whether a bank routing number and an individual account number are the same is a common point of confusion. A bank routing number, also known as an ABA routing number, is a nine-digit code used to identify the financial institution in the United States where an account is held. It is primarily used for processing transactions such as direct deposits, wire transfers, and automatic bill payments. On the other hand, an individual account number is a unique set of digits assigned to a specific account holder’s bank account, used to distinguish it from other accounts within the same bank. While both are essential for banking operations, they serve distinct purposes: the routing number identifies the bank, and the account number identifies the specific account within that bank. Therefore, they are not the same and must both be used together for accurate transaction processing.

Explore related products

What You'll Learn

- Routing Number Purpose: Identifies banks for transactions, not individuals; used for transfers, direct deposits, and bill payments

- Individual Account Number: Unique to account holders, linked to personal finances, not shared with routing numbers

- Routing vs. Account: Routing identifies the bank; account number identifies the specific account within the bank

- Security Differences: Routing numbers are public; account numbers are private and require protection to prevent fraud

- Usage in Transactions: Both are needed for transfers, but routing directs to the bank, and account specifies the recipient

![]()

Routing Number Purpose: Identifies banks for transactions, not individuals; used for transfers, direct deposits, and bill payments

A routing number, also known as an ABA routing transit number, is a nine-digit code that serves as a unique identifier for financial institutions in the United States. This number is crucial for facilitating various transactions, including transfers, direct deposits, and bill payments. However, it’s essential to understand that a routing number is tied to a bank, not an individual account holder. For instance, if you’re setting up a direct deposit for your paycheck, your employer will need your bank’s routing number and your specific account number. The routing number ensures the funds are directed to the correct bank, while your account number ensures they land in your personal account.

Consider the process of transferring money between banks. When you initiate an ACH (Automated Clearing House) transfer, the routing number acts as the address for the sending and receiving banks. Without it, the transaction would lack the necessary destination details, leading to delays or failures. For example, if you’re moving funds from a Chase account to a Bank of America account, the routing numbers for both institutions are critical to ensure the transfer is executed accurately. This system prevents errors and enhances the efficiency of electronic transactions, which now account for over 90% of all payments in the U.S.

From a practical standpoint, knowing your bank’s routing number is essential for everyday financial activities. For direct deposits, such as payroll or government benefits, the routing number ensures timely and accurate payments. Similarly, when paying bills electronically, the routing number is often required alongside your account number to authorize withdrawals. It’s worth noting that routing numbers can vary depending on the transaction type and location. For instance, wire transfers may use a different routing number than ACH transactions, so always verify the correct code with your bank.

A common misconception is that a routing number can identify an individual, but this is not the case. While it specifies the bank, credit union, or financial institution, it does not provide any information about the account holder. This distinction is vital for security purposes, as it prevents unauthorized access to personal accounts. For example, if someone knows your bank’s routing number, they cannot use it to withdraw funds from your account without your specific account number and authorization. This separation of identifiers ensures that transactions remain secure and private.

In summary, the routing number is a foundational element of the U.S. banking system, enabling seamless transactions while safeguarding individual accounts. Whether you’re setting up direct deposits, transferring funds, or paying bills, understanding its purpose and limitations is key. Always double-check the routing number for accuracy, as errors can result in failed transactions or delays. By recognizing that it identifies banks, not individuals, you can navigate financial processes with confidence and clarity.

Where Can I Find Free ATMs at Bank of Idaho?

You may want to see also

Explore related products

![]()

Individual Account Number: Unique to account holders, linked to personal finances, not shared with routing numbers

A bank routing number and an individual account number serve distinct purposes in the financial system. While the routing number identifies the financial institution and its branch, the individual account number is a unique identifier tied exclusively to the account holder’s personal finances. This account number is critical for transactions like direct deposits, withdrawals, and transfers, ensuring funds are directed to the correct account within the bank’s system. Unlike routing numbers, which are standardized and often publicly available, individual account numbers are private and should never be shared indiscriminately to protect against fraud or unauthorized access.

Consider the analogy of a postal address: the routing number is akin to the city and ZIP code, guiding the mail to the right location, while the individual account number functions as the specific house number, pinpointing exactly where the mail should be delivered. This distinction is vital for security and accuracy in banking operations. For instance, when setting up direct deposit, employers require both the routing number and the individual account number to ensure wages are deposited into the correct account. Mistaking one for the other could result in funds being misdirected or delayed, highlighting the importance of understanding their separate roles.

Practical tips for safeguarding your individual account number include treating it with the same care as your Social Security number or password. Avoid sharing it via unsecured channels like email or text messages, and verify the legitimacy of any entity requesting it. Banks typically provide masked account numbers on statements or online portals, displaying only the last four digits to protect the full number. If you suspect your account number has been compromised, contact your bank immediately to freeze the account and prevent unauthorized transactions. Proactive measures like these are essential in maintaining the integrity of your personal finances.

From a comparative perspective, while routing numbers are shared across all accounts within a bank branch, individual account numbers are unique to each account holder, even within the same household. This uniqueness ensures that transactions are personalized and secure. For example, a family with multiple accounts at the same bank will have one shared routing number but distinct account numbers for each member’s savings, checking, or investment accounts. This system streamlines banking processes while maintaining individualized control over financial assets.

In conclusion, the individual account number is a cornerstone of personal banking, distinct from the routing number in both function and sensitivity. By understanding its role and taking steps to protect it, account holders can ensure their financial transactions remain secure and accurate. Treat this number as a key to your financial identity, and handle it with the care it deserves to safeguard your assets and peace of mind.

Axiom Bank's Workforce Size: Unveiling the Number of Employees

You may want to see also

Explore related products

![]()

Routing vs. Account: Routing identifies the bank; account number identifies the specific account within the bank

Bank transactions rely on two critical pieces of information: the routing number and the account number. These are not interchangeable; they serve distinct purposes. The routing number, a nine-digit code, acts as a bank’s unique identifier within the financial system. It ensures funds are directed to the correct institution, much like a postal code directs mail to the right city. Without it, transactions would lack a destination, causing delays or failures. For instance, when setting up direct deposit, the routing number tells the payer which bank to send the money to, while the account number specifies where within that bank the funds should land.

In contrast, the account number is a personal identifier, typically 10 to 12 digits long, tied to an individual’s or entity’s specific account. Think of it as an apartment number within a building—the routing number gets you to the building (bank), and the account number ensures delivery to the correct unit (account). Mistyping the account number can result in funds being deposited into someone else’s account, a costly and time-consuming error to rectify. For example, if two individuals at the same bank share similar names, their routing numbers will be identical, but their account numbers will differ, preventing confusion.

Practical scenarios highlight the importance of this distinction. When wiring money internationally, the routing number (or its equivalent, like a SWIFT code) ensures the funds reach the correct bank, while the account number guarantees they end up in the intended recipient’s possession. Similarly, when ordering checks, both numbers are printed on them: the routing number in the lower left corner and the account number to its right. Omitting or transposing these digits can render the check unusable, underscoring the need for accuracy.

To avoid errors, always double-check both numbers before initiating a transaction. Banks often provide digital tools or customer service support to verify these details. For added security, never share your account number unless necessary, and ensure the routing number matches the bank’s official records. Understanding the roles of these numbers not only streamlines transactions but also protects your financial assets from misdirection or fraud. In essence, the routing number is the bank’s address, while the account number is your personal mailbox within it.

Donate to Liverpool Food Banks: Simple Steps to Make a Difference

You may want to see also

Explore related products

![]()

Security Differences: Routing numbers are public; account numbers are private and require protection to prevent fraud

Routing numbers and account numbers serve distinct purposes in banking, but their security implications couldn’t be more different. A routing number, also known as an ABA number, is a nine-digit code that identifies the financial institution handling a transaction. It’s public information, readily available on checks, bank websites, and even federal databases. Think of it as the bank’s address—necessary for directing funds but not sensitive enough to compromise your personal finances. In contrast, your account number is the key to your specific holdings. It’s private, tied directly to your individual or business account, and must be safeguarded to prevent unauthorized access. This fundamental difference in exposure highlights why one is shared freely while the other demands strict protection.

Consider the practical implications of this distinction. If someone knows your routing number, they can’t withdraw funds from your account or commit fraud in your name. It’s a piece of the puzzle but lacks the power to unlock your assets. However, if your account number falls into the wrong hands, the consequences can be severe. Scammers can initiate unauthorized transfers, drain your balance, or even impersonate you in fraudulent schemes. This is why banks emphasize keeping account numbers confidential, often requiring additional verification steps like security questions or two-factor authentication when accessed digitally. The routing number’s public nature simplifies transactions, while the account number’s privacy ensures your financial security.

To illustrate, imagine sending a wire transfer. You’ll need both your routing number and account number, but their roles differ significantly. The routing number ensures the funds reach the correct bank, while the account number specifies where within that bank the money should go. Here’s a tip: When sharing banking details for legitimate purposes, such as direct deposits or bill payments, only provide the routing number if it’s the sole requirement. Never disclose your account number unless absolutely necessary, and always verify the recipient’s identity. For added safety, use secure channels like encrypted emails or trusted banking portals instead of unencrypted text messages or public Wi-Fi networks.

The security protocols surrounding these numbers also reflect their differing risks. Routing numbers are embedded in everyday transactions, from payroll deposits to online purchases, without raising security concerns. Account numbers, however, are treated with far greater caution. Banks employ encryption, firewalls, and monitoring systems to protect them, and customers are advised to shred documents containing this information. Even when storing account details digitally, use password managers or encrypted files to minimize exposure. A single breach of an account number can lead to identity theft or financial loss, making its protection a critical aspect of personal cybersecurity.

In summary, while routing numbers and account numbers are both essential in banking, their security differences are stark. One is a public identifier, facilitating transactions without risk, while the other is a private gateway to your funds, requiring vigilant protection. Understanding this distinction empowers you to share information wisely, adopt secure practices, and mitigate the risk of fraud. Treat your routing number as a necessary tool and your account number as a guarded secret—your financial safety depends on it.

How to Generate MMID for Allahabad Bank: A Step-by-Step Guide

You may want to see also

Explore related products

$29.62 $42.99

![]()

Usage in Transactions: Both are needed for transfers, but routing directs to the bank, and account specifies the recipient

In financial transactions, both the bank routing number and the individual account number are indispensable, yet they serve distinct roles. The routing number, a nine-digit code, acts as a GPS for funds, guiding them to the correct financial institution. Without it, transfers would lack direction, akin to mailing a letter without an address. Conversely, the account number, typically 10 to 12 digits, identifies the specific recipient within that bank. Together, they ensure money reaches its intended destination, much like a city name paired with a street address.

Consider a wire transfer as an example. When initiating the transaction, the sender must provide both the routing number and the recipient’s account number. The routing number directs the funds to the recipient’s bank, while the account number ensures the money lands in the correct individual’s account. Omitting either number would result in delays or failures—the routing number alone would leave the funds stranded at the bank, and the account number alone would lack the necessary bank identifier. This dual requirement underscores their complementary, non-interchangeable roles.

From a practical standpoint, understanding this distinction is crucial for error-free transactions. For instance, when setting up direct deposits or automatic bill payments, double-checking both numbers can prevent common pitfalls. A misplaced digit in the routing number could send funds to the wrong bank, while an error in the account number might deposit money into an unintended account. Financial institutions often provide these numbers on checks (routing number first, account number second) or via online banking portals, making verification straightforward.

A persuasive argument for their importance lies in the consequences of misuse. Fraudsters often exploit confusion between these numbers to redirect funds illicitly. By educating oneself on their functions, individuals can safeguard their finances. For instance, if a scammer obtains only the routing number, they cannot access an account without the corresponding account number. This layered security highlights why both pieces of information are required for legitimate transactions but also why they must be protected separately.

In summary, while the routing number and account number are both essential for transfers, their functions diverge sharply. The routing number navigates funds to the bank, while the account number pinpoints the recipient. This partnership ensures accuracy and security in financial exchanges, making it imperative to handle both with care. Whether transferring funds domestically or internationally, recognizing their unique roles streamlines processes and mitigates risks, turning complex transactions into routine tasks.

Does Florida Capital Bank Refund ATM Fees? What You Need to Know

You may want to see also

Frequently asked questions

No, a bank routing number identifies the financial institution, while an individual's account number identifies the specific account held by the customer at that bank.

No, a bank routing number is not unique to an individual; it is shared by all customers of the same bank or branch.

No, the routing number on a check identifies the bank, while a personal identification number (PIN) is a separate security code used for accessing accounts.

Yes, typically, an individual will have the same routing number for all accounts held at the same bank or branch, unless the accounts are in different regions.