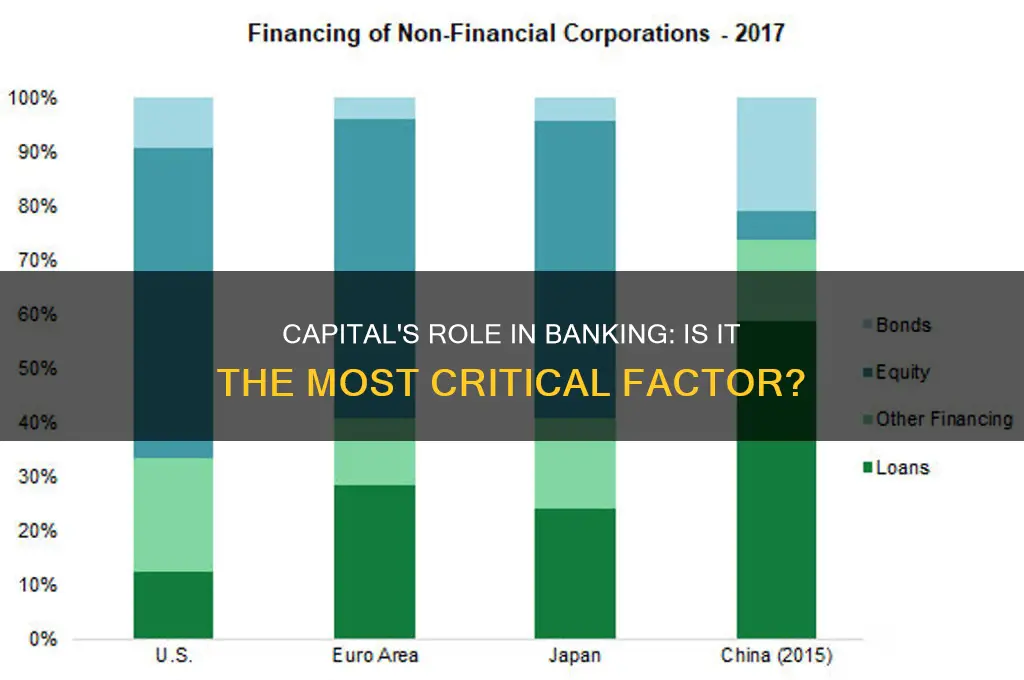

The question of whether capital is the most important factor in banking is a complex and multifaceted one, as it touches on the very foundation of financial stability and economic growth. While capital undoubtedly plays a critical role in a bank's ability to absorb losses, manage risks, and maintain confidence among depositors and investors, it is not the sole determinant of a bank's success or resilience. Other factors, such as liquidity, asset quality, management expertise, and regulatory oversight, also significantly influence a bank's performance and its capacity to withstand financial shocks. Moreover, the importance of capital can vary depending on the bank's size, business model, and the broader economic environment. Therefore, while capital is undeniably crucial, it is essential to consider it within a broader framework of factors that collectively contribute to the health and stability of the banking sector.

Explore related products

What You'll Learn

![]()

Role of Capital in Risk Management

Capital serves as the bedrock of risk management in banking, acting as a buffer against losses and ensuring financial stability. Without adequate capital, banks risk insolvency when faced with unexpected shocks, such as economic downturns or loan defaults. Regulatory frameworks like Basel III mandate minimum capital requirements, tying capital levels to risk-weighted assets. This ensures banks maintain sufficient reserves to absorb losses while continuing operations. For instance, a bank with a capital adequacy ratio of 12% can withstand a higher degree of risk compared to one at the regulatory minimum of 8%. This buffer not only protects the bank but also safeguards depositors and the broader financial system.

Consider the 2008 financial crisis, where undercapitalized banks amplified systemic risk. Institutions like Lehman Brothers, with thin capital cushions, collapsed under the weight of toxic assets, triggering a global crisis. In contrast, banks with robust capital bases, such as JPMorgan Chase, weathered the storm more effectively. This historical example underscores the critical role of capital in absorbing shocks and preventing contagion. Capital, therefore, is not just a regulatory requirement but a strategic tool for resilience.

From a practical standpoint, banks must balance capital retention with profitability. Holding excessive capital can dilute returns on equity, while insufficient capital exposes the bank to risk. A dynamic approach, such as stress testing, helps banks assess capital needs under adverse scenarios. For example, a bank might simulate a 20% decline in asset values to determine if its capital can cover potential losses. Such proactive measures ensure capital adequacy without sacrificing growth. Additionally, diversifying funding sources, like issuing long-term debt, can complement capital in managing liquidity risk.

Persuasively, capital’s role extends beyond internal risk management to shaping market confidence. Investors and counterparties view high capital levels as a sign of financial strength, reducing funding costs and enhancing credibility. For instance, banks with Tier 1 capital ratios above 15% often enjoy lower borrowing rates compared to peers. This market-driven incentive aligns with regulatory goals, creating a self-reinforcing mechanism for stability. Capital, thus, is not merely a defensive measure but a strategic asset that drives competitive advantage.

In conclusion, capital is the linchpin of risk management in banking, offering protection, enabling growth, and fostering trust. While not the sole determinant of banking success, its importance cannot be overstated. Banks must adopt a holistic approach, integrating regulatory compliance, stress testing, and market dynamics to optimize capital use. By doing so, they not only safeguard themselves but also contribute to a more resilient financial ecosystem.

Easy Steps to Withdraw $1000 from Your HSBC Bank Account

You may want to see also

Explore related products

![]()

Capital Requirements vs. Profitability in Banks

Capital requirements and profitability in banks are often viewed as competing priorities, yet their interplay is critical to a bank’s stability and growth. Regulators mandate minimum capital levels to ensure banks can absorb losses during economic downturns, but these requirements can constrain lending and reduce short-term profits. For instance, Basel III increased Tier 1 capital requirements to 6% of risk-weighted assets, limiting banks’ ability to leverage their balance sheets aggressively. While this enhances resilience, it also pressures banks to balance compliance with profit generation, often leading to strategic trade-offs.

Consider the analytical perspective: higher capital requirements reduce the risk of bank failure but lower return on equity (ROE) by diluting shareholders’ returns. A bank with a 10% ROE before new capital rules might see this drop to 8% post-compliance, assuming a 25% increase in capital. This tension forces banks to optimize capital allocation, often by shedding low-margin business lines or raising capital through equity issuances, which can dilute existing shareholders. The challenge lies in maintaining profitability while adhering to regulatory demands, a delicate act that requires precise financial modeling and strategic foresight.

From a comparative standpoint, banks in jurisdictions with stricter capital rules often exhibit lower profitability but greater stability. For example, European banks, subject to more stringent regulations than their U.S. counterparts, typically report lower ROE but have weathered crises like 2008 more robustly. Conversely, U.S. banks, with higher leverage ratios, achieve greater short-term profits but face elevated risk during downturns. This trade-off highlights the need for banks to tailor their strategies to regulatory environments, balancing growth ambitions with risk management imperatives.

Practically, banks can mitigate the impact of capital requirements on profitability through several strategies. First, they can focus on fee-based income, such as wealth management or advisory services, which require less capital than traditional lending. Second, optimizing risk-weighted assets (RWAs) through securitization or off-balance-sheet structures can free up capital for higher-return activities. Third, adopting advanced risk models under Basel III’s Internal Ratings-Based (IRB) approach can reduce RWA calculations, thereby lowering capital needs. These steps, while complex, offer a pathway to reconcile regulatory compliance with profit goals.

Ultimately, the relationship between capital requirements and profitability is not zero-sum but symbiotic. Adequate capital ensures long-term survival, while profitability drives growth and shareholder value. Banks that master this balance—through strategic capital management, diversified revenue streams, and robust risk frameworks—position themselves for sustained success. The key lies in viewing capital not as a constraint but as a foundation for resilient, profitable banking.

Seamlessly Integrate Receipt Bank with QBO: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Impact of Regulatory Capital Standards

Regulatory capital standards, such as Basel III, mandate banks to maintain a minimum level of capital relative to their risk-weighted assets. These requirements are designed to ensure banks can absorb losses during economic downturns without collapsing. For instance, a bank with $100 billion in assets might be required to hold 8% in Tier 1 capital, equating to $8 billion. This buffer protects depositors, taxpayers, and the broader financial system from the fallout of bank failures, as seen in the 2008 financial crisis.

However, the impact of these standards extends beyond mere loss absorption. Higher capital requirements reduce banks’ ability to lend, as a larger portion of their resources is tied up in reserves. This can stifle economic growth, particularly in credit-dependent sectors like small businesses and real estate. For example, a study by the International Monetary Fund found that a 1% increase in capital ratios could reduce bank lending by up to 2.5%. Policymakers must therefore balance financial stability with the need to support economic activity, often adjusting requirements during crises to encourage lending.

Another unintended consequence of stringent capital standards is the potential for regulatory arbitrage. Banks may shift risky activities to less regulated entities or use complex financial instruments to circumvent rules. For instance, shadow banking—non-bank financial intermediaries—has grown significantly since Basel III’s implementation, raising concerns about systemic risks outside the regulatory perimeter. Regulators must continually adapt to close loopholes and ensure standards address evolving risks.

Despite these challenges, regulatory capital standards have undeniably strengthened the banking sector. Banks today are better capitalized and more resilient than in the pre-2008 era. For example, the average Tier 1 capital ratio for global systemically important banks (G-SIBs) rose from 7.8% in 2007 to 14.7% in 2021. This increased resilience was evident during the COVID-19 pandemic, when banks were able to absorb shocks and continue lending, unlike during the 2008 crisis.

In conclusion, while regulatory capital standards are not without trade-offs, their role in safeguarding financial stability is undeniable. Banks, regulators, and policymakers must work collaboratively to refine these standards, ensuring they remain effective without unduly constraining economic growth. Practical steps include stress testing capital adequacy under various scenarios, promoting transparency in risk-weighting methodologies, and fostering international cooperation to prevent regulatory arbitrage. By doing so, capital standards can continue to serve as a cornerstone of a robust banking system.

Master QuickBooks Bank Invoicing: A Step-by-Step Guide to Issuing Invoices

You may want to see also

Explore related products

$16.51 $37.5

![]()

Capital Adequacy and Financial Stability

Capital adequacy is the backbone of financial stability, ensuring banks can absorb shocks without collapsing. Regulatory frameworks like Basel III mandate minimum capital requirements, typically 8% of risk-weighted assets, to safeguard against losses. For instance, during the 2008 financial crisis, banks with higher capital buffers weathered the storm better than those operating on thin margins. This historical lesson underscores why capital adequacy isn’t just a regulatory checkbox but a critical buffer against systemic risk.

Consider the role of capital as a bank’s financial immune system. Just as a strong immune system fights off infections, adequate capital reserves protect banks from loan defaults, market volatility, and economic downturns. For example, a bank with a 12% capital adequacy ratio has more resilience than one at the bare minimum of 8%. However, striking the right balance is key. Excessive capital requirements can stifle lending, choking economic growth, while insufficient capital leaves banks vulnerable to failure. Policymakers must calibrate these ratios carefully, factoring in economic conditions and risk profiles.

A persuasive argument for capital adequacy lies in its ability to restore trust in the financial system. Depositors and investors are more confident when banks maintain robust capital levels. Take the case of JPMorgan Chase, which maintained a capital ratio well above regulatory requirements during the COVID-19 pandemic, reassuring stakeholders of its stability. Conversely, banks like Lehman Brothers, with inadequate capital, faced catastrophic failure, triggering a global crisis. Trust, once lost, is hard to regain, making capital adequacy a non-negotiable pillar of banking integrity.

Comparatively, capital adequacy differs from liquidity management, though both are vital. While liquidity ensures banks can meet short-term obligations, capital adequacy focuses on long-term solvency. For instance, a bank might have ample liquid assets but insufficient capital to cover unexpected losses. The 2008 crisis highlighted this distinction: many banks had liquidity but lacked the capital to absorb mortgage-backed securities losses. Banks must therefore prioritize both, but capital adequacy remains the ultimate safeguard against insolvency.

In practice, achieving capital adequacy requires strategic planning. Banks can bolster capital through retained earnings, issuing equity, or reducing risk-weighted assets. For example, a bank might sell high-risk loans or invest in safer assets to lower its capital requirements. However, these actions come with trade-offs. Issuing equity dilutes shareholder value, while reducing risk-weighted assets may limit profitability. Banks must navigate these challenges thoughtfully, ensuring capital adequacy without compromising growth. Ultimately, a well-capitalized bank isn’t just compliant—it’s a pillar of financial stability.

Community Bank Rewards: Do Your Purchases Earn You Benefits?

You may want to see also

Explore related products

![]()

Alternatives to Capital in Banking Operations

While capital remains a cornerstone of banking stability, its primacy is increasingly challenged by innovative alternatives. One such alternative lies in risk management sophistication. Banks are leveraging advanced analytics and machine learning to predict and mitigate risks with unprecedented precision. For instance, stress testing models now incorporate real-time market data and scenario analysis, enabling banks to optimize capital allocation dynamically. A 2022 study by McKinsey found that banks employing AI-driven risk management reduced their capital requirements by up to 15% without compromising safety. This shift underscores that intelligent risk management can be as critical as capital in ensuring financial resilience.

Another emerging alternative is the strategic use of liquidity management. Banks are increasingly focusing on maintaining robust liquidity buffers and diversifying funding sources to reduce reliance on capital. For example, the rise of central bank digital currencies (CBDCs) and peer-to-peer lending platforms has opened new avenues for liquidity generation. A case in point is the European Central Bank’s TLTRO program, which provided long-term funding to banks at favorable rates, effectively reducing their need for high capital reserves. By prioritizing liquidity, banks can sustain operations during market downturns without over-relying on capital.

Operational efficiency also emerges as a viable alternative to capital. Banks are investing heavily in digital transformation to streamline processes, reduce costs, and enhance productivity. Automation of back-office functions, such as loan processing and compliance, has yielded significant savings. For instance, JPMorgan Chase’s implementation of AI-driven systems reduced operational costs by $1.2 billion annually. Such efficiencies free up resources that can be redirected to support lending and growth, diminishing the need for additional capital.

Lastly, partnerships and collaboration are reshaping the banking landscape. Banks are increasingly forming alliances with fintech firms, insurers, and even competitors to share risks and resources. For example, syndicated lending allows banks to distribute loan exposure across multiple institutions, reducing individual capital requirements. Similarly, co-branded credit cards and joint venture projects enable banks to expand their reach without proportionally increasing capital. These collaborative models demonstrate that shared expertise and risk can be as valuable as capital in driving banking operations.

In conclusion, while capital remains indispensable, its dominance in banking is being complemented—and in some cases, rivaled—by alternatives like advanced risk management, liquidity optimization, operational efficiency, and strategic partnerships. These innovations not only reduce reliance on capital but also enhance the overall resilience and agility of banking operations. As the industry evolves, banks that embrace these alternatives will likely thrive in an increasingly complex financial ecosystem.

Send Money Easily: Zelle with Huntington Bank Step-by-Step Guide

You may want to see also

Frequently asked questions

While capital is crucial for a bank's stability and risk management, it is not the only important factor. Liquidity, asset quality, management expertise, and regulatory compliance also play critical roles in a bank's success.

Capital is essential because it acts as a buffer against losses, ensures solvency, and builds trust among depositors and investors. It also helps banks meet regulatory requirements and supports lending activities.

No, a bank cannot survive without sufficient capital. Inadequate capital increases the risk of insolvency, especially during financial crises, and can lead to loss of depositor confidence and regulatory intervention.

Capital and profitability are both critical, but they serve different purposes. Capital ensures stability and risk absorption, while profitability drives growth and shareholder value. A balance between the two is necessary for long-term success.