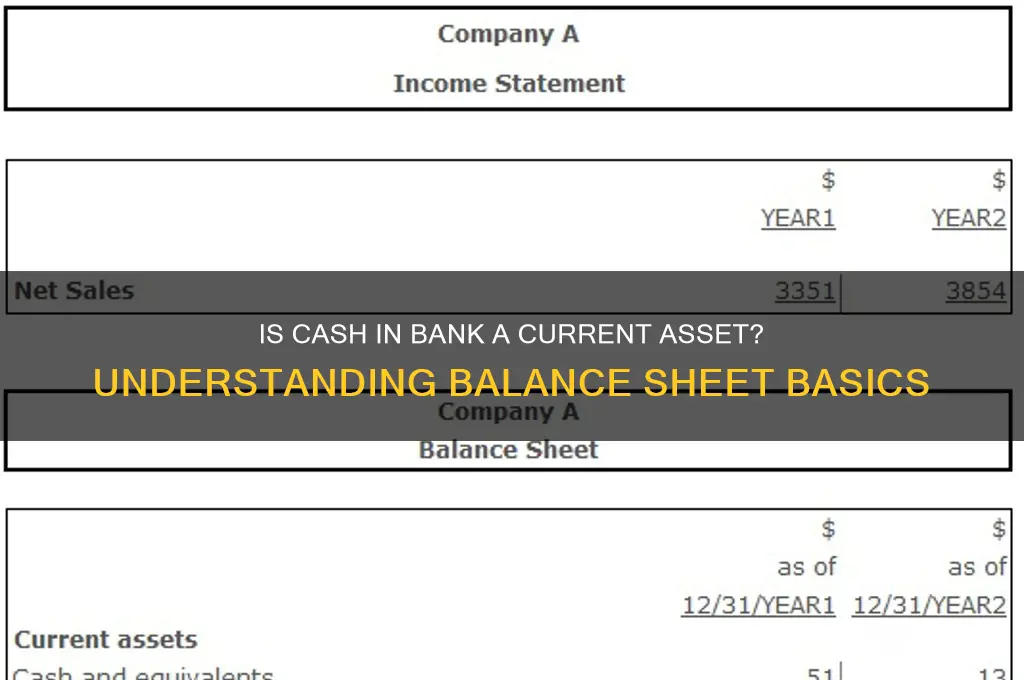

The classification of cash in bank as a current asset is a fundamental concept in accounting and financial reporting. Current assets are resources that a company expects to convert into cash or use up within one year or one operating cycle, whichever is longer. Cash in bank, which includes funds held in checking accounts, savings accounts, and other readily accessible accounts, is typically considered a current asset because it is highly liquid and can be easily converted into cash without significant loss of value. This classification is crucial for assessing a company's short-term financial health, liquidity, and ability to meet its immediate obligations. Understanding whether cash in bank qualifies as a current asset helps stakeholders, including investors and creditors, evaluate the company's financial stability and operational efficiency.

Explore related products

What You'll Learn

- Definition of Current Assets: Current assets include cash, equivalents, and resources expected to be consumed within a year

- Cash in Bank Classification: Cash in bank is a primary example of a current asset due to liquidity

- Liquidity and Accessibility: Bank cash is highly liquid, making it readily available for business operations

- Balance Sheet Presentation: Cash in bank is reported under current assets on the balance sheet

- Importance in Financial Analysis: It reflects a company’s short-term financial health and ability to meet obligations

![]()

Definition of Current Assets: Current assets include cash, equivalents, and resources expected to be consumed within a year

Cash in bank is unequivocally classified as a current asset, but understanding why requires dissecting the definition of current assets itself. At its core, the term "current assets" refers to resources a company owns, expects to use, or can convert into cash within one year or one operating cycle, whichever is longer. This includes tangible items like inventory and intangible ones like accounts receivable. Cash in bank falls under this umbrella because it is immediately available for use, requiring no conversion period. Unlike long-term assets such as property or equipment, which provide value over multiple years, cash in bank is liquid and ready for operational needs, debt repayment, or investment opportunities.

Consider a small business with $50,000 in a checking account. This cash is not earmarked for long-term projects but is instead used to cover payroll, purchase supplies, or manage short-term liabilities. Its liquidity and accessibility make it a cornerstone of current assets, ensuring the business can meet its immediate financial obligations. For instance, if the business has $30,000 in accounts payable due within 30 days, the cash in bank directly supports settling these debts without disrupting operations. This example underscores the practical role of cash in bank as a current asset, serving as a financial buffer for day-to-day activities.

However, not all cash is treated equally in financial statements. While cash in bank is straightforward, "cash equivalents" broaden the definition. These are highly liquid investments, such as Treasury bills or money market funds, that can be readily converted to cash within 90 days. For example, a company holding $100,000 in a money market account would list this as a current asset alongside its bank cash. This distinction is crucial for investors and analysts, as it provides a clearer picture of a company’s short-term financial health and liquidity position.

A comparative analysis highlights the importance of this classification. Imagine two companies with identical total assets but differing cash positions. Company A has $200,000 in cash in bank, while Company B has only $50,000, with the remainder tied up in long-term investments. Despite similar asset values, Company A’s higher cash reserves indicate greater liquidity and flexibility to address immediate needs. This comparison illustrates why cash in bank is not just a current asset but a critical indicator of a company’s ability to navigate short-term challenges.

In conclusion, cash in bank is a current asset because it meets the defining criteria: it is liquid, accessible, and expected to be used within a year. Its role extends beyond mere bookkeeping, serving as a lifeline for businesses to manage obligations and seize opportunities. By understanding this classification, stakeholders can better assess a company’s financial stability and operational readiness. Whether it’s a startup managing cash flow or a multinational corporation balancing global operations, cash in bank remains a fundamental component of current assets, anchoring short-term financial strategies.

Step-by-Step Guide to Banking a Cheque in Kenya Easily

You may want to see also

Explore related products

![]()

Cash in Bank Classification: Cash in bank is a primary example of a current asset due to liquidity

Cash in bank is unequivocally classified as a current asset, primarily because it represents the most liquid form of an organization’s resources. Liquidity, the ease with which an asset can be converted into cash without significant loss of value, is the cornerstone of this classification. Bank cash meets this criterion perfectly—it is immediately accessible for paying expenses, settling debts, or funding short-term obligations. Unlike inventory or prepaid expenses, which require time or additional steps to convert into usable funds, cash in bank is ready for deployment at a moment’s notice. This immediacy makes it a cornerstone of a company’s working capital, ensuring operational continuity and financial stability.

To understand why cash in bank is a current asset, consider its role in the balance sheet. Current assets are defined as those expected to be consumed or converted into cash within one year or one operating cycle, whichever is longer. Cash in bank inherently meets this definition since it is already in its most liquid form. For instance, a retail company’s cash reserves in its business account are used daily to pay suppliers, cover payroll, and manage overhead costs. Without this readily available cash, the company would struggle to meet its short-term financial obligations, underscoring its critical role as a current asset.

A practical example illustrates this classification further. Imagine a small e-commerce business with $50,000 in its bank account. This cash is not earmarked for long-term investments or capital expenditures; instead, it is used to purchase inventory, cover shipping costs, and handle unexpected expenses. In financial reporting, this $50,000 would be listed under current assets, reflecting its immediate availability and short-term utility. Contrast this with a long-term investment in property or equipment, which would be classified as a non-current asset due to its illiquid nature and long-term use.

However, it’s essential to distinguish between cash in bank and other forms of cash equivalents, such as treasury bills or short-term certificates of deposit. While these are also highly liquid, they may not be immediately accessible without incurring penalties or waiting for maturity. Cash in bank, on the other hand, faces no such restrictions. For businesses, this distinction is crucial for accurate financial planning and reporting. Misclassifying cash in bank could distort liquidity ratios, such as the current ratio or quick ratio, which investors and creditors rely on to assess a company’s financial health.

In conclusion, cash in bank is a primary example of a current asset due to its unparalleled liquidity and immediate availability. Its classification is not merely a technicality but a reflection of its vital role in sustaining day-to-day operations and meeting short-term obligations. For businesses, understanding this classification is essential for maintaining accurate financial records and ensuring strategic resource allocation. By recognizing cash in bank as a current asset, companies can better manage their liquidity, plan for contingencies, and present a transparent financial picture to stakeholders.

Is the Grand Banks Genealogy Site Offline? What Happened?

You may want to see also

Explore related products

![]()

Liquidity and Accessibility: Bank cash is highly liquid, making it readily available for business operations

Cash held in a bank account is the epitome of liquidity, a critical attribute for businesses navigating the unpredictable currents of commerce. Unlike inventory, which ties up capital and requires time to convert into cash, or accounts receivable, which depend on customer payment timelines, bank cash is immediately accessible. This immediacy ensures that businesses can swiftly respond to opportunities—whether it’s capitalizing on a discounted bulk purchase, covering unexpected expenses, or meeting payroll obligations. For instance, a small retailer with $50,000 in a business checking account can instantly transfer funds to secure a limited-time inventory deal, a flexibility that directly impacts profitability.

However, liquidity is a double-edged sword. While bank cash is readily available, it often yields minimal returns compared to other investments. Businesses must balance the need for accessibility with the opportunity cost of holding idle cash. A practical approach is to maintain a liquidity buffer equivalent to 3–6 months of operating expenses, ensuring stability without sacrificing growth potential. For example, a tech startup with monthly expenses of $20,000 should aim for $60,000–$120,000 in liquid assets, allowing it to weather cash flow fluctuations while exploring higher-yielding investments for surplus funds.

The accessibility of bank cash also hinges on the type of account. Business checking accounts offer unlimited transactions and immediate access, ideal for day-to-day operations. In contrast, savings accounts or money market accounts may impose withdrawal limits or penalties, making them less suitable for urgent needs. A mid-sized manufacturer, for instance, might use a checking account for payroll and supplier payments while parking excess funds in a high-yield savings account to earn modest interest without compromising liquidity.

To maximize the benefits of liquid bank cash, businesses should adopt disciplined cash management practices. Regularly monitoring cash flow, reconciling accounts, and forecasting short-term needs can prevent liquidity shortages. Tools like cash flow projections or automated alerts for low balances can provide early warnings, enabling proactive decision-making. For example, a service-based business with seasonal revenue fluctuations could use these tools to identify slow periods and adjust spending or secure short-term financing in advance.

In essence, bank cash serves as the lifeblood of business operations, offering unparalleled liquidity and accessibility. While it may not generate significant returns, its role in ensuring financial agility and stability is indispensable. By strategically managing this asset—maintaining adequate reserves, choosing the right account types, and employing robust cash management practices—businesses can harness its full potential to navigate challenges and seize opportunities with confidence.

Banking Careers and ADHD: Challenges, Opportunities, and Success Strategies

You may want to see also

Explore related products

![]()

Balance Sheet Presentation: Cash in bank is reported under current assets on the balance sheet

Cash in bank is unequivocally classified as a current asset on the balance sheet, a fundamental principle in financial reporting. This classification stems from its liquidity—cash in bank is readily available for immediate use in business operations, debt settlement, or investment within the operating cycle, typically one year. Unlike fixed assets, which are long-term and illiquid, cash in bank represents the most liquid form of current assets, ensuring a company’s ability to meet short-term obligations. This categorization is not arbitrary but adheres to accounting standards such as GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards), providing consistency and comparability across financial statements.

The presentation of cash in bank under current assets serves multiple purposes. Firstly, it offers stakeholders a clear snapshot of a company’s short-term financial health. Investors, creditors, and analysts scrutinize this line item to assess liquidity and solvency. For instance, a high cash balance relative to current liabilities signals robust liquidity, while a low balance may raise concerns about cash flow management. Secondly, it aids in calculating key financial ratios, such as the current ratio (current assets/current liabilities) and quick ratio (current assets minus inventory/current liabilities), which are critical for evaluating a company’s ability to cover short-term debts.

However, not all cash is treated equally in this category. Restricted cash, earmarked for specific purposes like loan collateral or legal settlements, is often disclosed separately or noted in the footnotes. This distinction is crucial, as unrestricted cash directly contributes to operational flexibility, while restricted cash may not be available for day-to-day activities. Companies must clearly differentiate between these types to avoid misleading stakeholders. For example, a tech startup with $1 million in cash but $800,000 restricted for R&D would report only $200,000 as readily available cash in bank, impacting its perceived liquidity.

Practical considerations arise when preparing the balance sheet. Accountants must ensure accuracy by reconciling bank statements with internal records to account for outstanding checks, deposits in transit, and bank fees. Small discrepancies can distort the reported cash balance, affecting financial ratios and stakeholder confidence. Additionally, multinational companies must address currency fluctuations, as cash held in foreign bank accounts may need to be adjusted for exchange rate differences at the reporting date. These steps are essential for maintaining the integrity of the balance sheet and ensuring compliance with accounting standards.

In conclusion, reporting cash in bank under current assets is more than a procedural requirement—it is a critical indicator of a company’s liquidity and short-term financial stability. By adhering to established accounting principles and providing transparent disclosures, companies enable stakeholders to make informed decisions. Whether analyzing a small business or a global corporation, understanding this classification is indispensable for interpreting financial statements accurately.

Track Your World Bank Internship Application: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Importance in Financial Analysis: It reflects a company’s short-term financial health and ability to meet obligations

Cash in the bank is unequivocally a current asset, and its presence on a company’s balance sheet serves as a vital indicator of liquidity. In financial analysis, this line item is more than just a number—it’s a snapshot of a company’s ability to cover immediate expenses, seize short-term opportunities, and weather unexpected financial storms. For instance, a tech startup with $500,000 in cash reserves is better positioned to fund payroll, pay suppliers, or invest in urgent R&D than a competitor with only $50,000, even if both have similar revenue streams. This liquidity gap can determine survival during downturns or rapid growth phases.

Analyzing cash in the bank requires context. A manufacturing firm holding $2 million in cash might appear robust, but if its accounts payable total $1.8 million due within 30 days, the net liquidity is minimal. Conversely, a retail company with $500,000 in cash and $200,000 in payables has a healthier short-term position. The key is to compare cash levels to current liabilities and operational burn rates. For small businesses, a rule of thumb is to maintain at least 3–6 months of operating expenses in cash, while larger corporations may aim for 1–2 months, depending on industry norms and risk tolerance.

From a persuasive standpoint, investors and creditors prioritize cash in the bank as a safety net. A company with ample cash reserves is less likely to default on loans or dilute equity through emergency fundraising. For example, during the 2020 pandemic, companies with strong cash positions, like Apple ($195 billion in cash and equivalents), navigated disruptions more effectively than those reliant on debt. This underscores why financial analysts scrutinize cash levels: it’s a tangible measure of resilience, not just a line item.

Comparatively, cash in the bank differs from other current assets like inventory or accounts receivable. Inventory may depreciate or become obsolete, and receivables can take weeks or months to convert into cash. Cash, however, is immediately accessible. Consider a scenario where a company has $1 million in inventory but only $50,000 in cash. If a sudden expense arises, liquidating inventory at full value is uncertain, whereas cash provides instant flexibility. This distinction highlights why cash is often referred to as the "king" of current assets.

In practice, financial analysts use ratios like the current ratio (current assets/current liabilities) and quick ratio (cash + receivables/current liabilities) to assess short-term health. A current ratio below 1 signals potential liquidity issues, but a quick ratio below 0.5 is particularly alarming, as it indicates insufficient cash and near-cash assets to cover obligations. For instance, a company with $1 million in cash, $500,000 in receivables, and $2 million in current liabilities has a quick ratio of 0.75—better than 0.5 but still a red flag. The takeaway? Cash in the bank isn’t just a current asset; it’s the cornerstone of a company’s ability to meet obligations and sustain operations.

How Banks Profit from a Hot Housing Market

You may want to see also

Frequently asked questions

Yes, cash in bank is classified as a current asset because it is highly liquid and can be readily converted into cash within one year or the operating cycle of a business.

Cash in bank is categorized as a current asset because it represents funds that are immediately available for use in business operations, payments, or investments.

No, cash in bank includes not only physical cash but also funds held in checking accounts, savings accounts, and other bank accounts that are accessible on demand.

Cash in bank is reported under the "Current Assets" section of the balance sheet, often listed as "Cash and Cash Equivalents" or simply "Cash."

No, cash in bank cannot be classified as a non-current asset because it is inherently liquid and accessible within the short term, meeting the definition of a current asset.