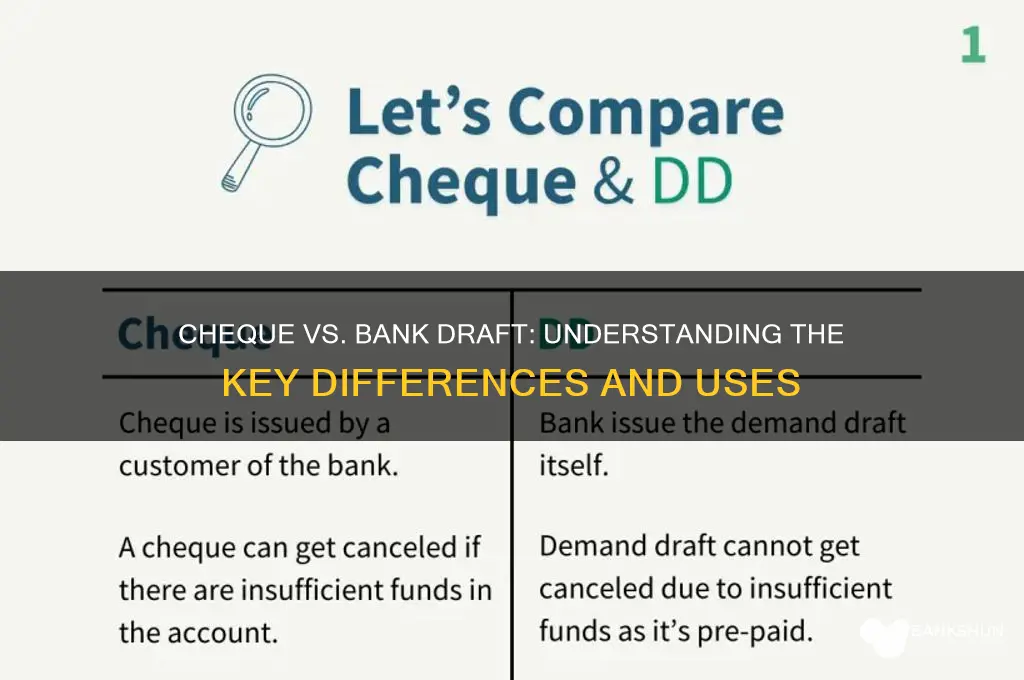

Cheques and bank drafts are both financial instruments used for making payments, but they are not the same. While both serve as secure alternatives to cash, a cheque is a written instruction from an account holder to their bank, authorizing the transfer of funds to the payee, and it is drawn on the payer's account. In contrast, a bank draft is issued and guaranteed by the bank itself, drawn on the bank's own funds, and is considered a more secure form of payment since it is pre-paid and cannot be returned due to insufficient funds. Understanding the differences between these two instruments is crucial for individuals and businesses to choose the appropriate method for their financial transactions.

Explore related products

What You'll Learn

- Definition and Purpose: Cheques and bank drafts differ in issuance, purpose, and security features

- Issuer Responsibility: Cheques are drawn by individuals; bank drafts are issued by banks directly

- Payment Guarantee: Bank drafts offer stronger guarantees compared to cheques, which can bounce

- Processing Time: Bank drafts clear faster than cheques due to bank-backed assurance

- Fees and Costs: Bank drafts typically incur higher fees than cheques for issuance

![]()

Definition and Purpose: Cheques and bank drafts differ in issuance, purpose, and security features

Cheques and bank drafts, though often confused, serve distinct financial purposes and operate under different mechanisms. A cheque is a written instruction from an account holder to their bank, authorizing the transfer of funds to a specified payee. In contrast, a bank draft is issued by the bank itself, guaranteeing payment to the recipient. This fundamental difference in issuance highlights their unique roles in financial transactions.

Consider the process of obtaining each instrument. To write a cheque, the account holder simply fills out a pre-printed form, ensuring sufficient funds are available in their account. Bank drafts, however, require the purchaser to pay the full amount upfront to the bank, which then issues a draft guaranteeing payment. This upfront payment underscores the bank draft’s role as a more secure and immediate form of payment, particularly in high-value transactions. For instance, when purchasing a car, a bank draft provides the seller with immediate assurance of funds, whereas a cheque carries the risk of bouncing if the account lacks sufficient balance.

Security features further differentiate the two. Cheques rely on the account holder’s signature and account details, making them susceptible to fraud, such as forgery or alteration. Bank drafts, on the other hand, incorporate advanced security measures like watermarks, holograms, and unique serial numbers, reducing the risk of counterfeiting. Additionally, since a bank draft is pre-paid, it eliminates the possibility of non-payment, offering greater peace of mind to recipients.

The purpose of each instrument also varies. Cheques are commonly used for everyday transactions, such as paying bills or transferring funds between individuals. Bank drafts, however, are typically employed in situations requiring guaranteed payment, like international trade, real estate transactions, or large purchases. For example, a business importing goods might use a bank draft to ensure the supplier receives payment promptly and securely, even across borders.

In practical terms, understanding these differences can help individuals and businesses choose the right instrument for their needs. For small, routine payments, a cheque may suffice, but for significant or sensitive transactions, a bank draft offers unparalleled security and reliability. By recognizing the unique issuance, purpose, and security features of cheques and bank drafts, one can navigate financial transactions with confidence and precision.

Understanding Bank Fees: How to Pay and Manage Charges Effectively

You may want to see also

Explore related products

![]()

Issuer Responsibility: Cheques are drawn by individuals; bank drafts are issued by banks directly

A cheque is a written instruction from an account holder to their bank, authorizing the transfer of funds to a specified payee. In contrast, a bank draft is a payment instrument issued directly by a bank, guaranteeing the availability of funds. This fundamental difference in issuer responsibility has significant implications for both the payer and the payee. When an individual writes a cheque, they are essentially making a promise that sufficient funds exist in their account to cover the amount. However, this promise is not foolproof, as the cheque can bounce if the account lacks adequate balance or if there are issues like a hold or freeze on the account. On the other hand, a bank draft assures the payee that the funds are already secured by the bank, reducing the risk of non-payment.

Consider a scenario where a homebuyer needs to make a down payment. Using a cheque introduces uncertainty for the seller, who must wait for the cheque to clear and risk it being returned due to insufficient funds. In contrast, a bank draft provides immediate assurance, as the bank has already debited the homebuyer’s account and guaranteed the payment. This example highlights how the issuer’s responsibility shifts the reliability of the payment instrument. For high-value transactions, bank drafts are often preferred precisely because the bank’s involvement minimizes the risk of default.

From a practical standpoint, understanding issuer responsibility helps individuals and businesses choose the right payment method. If you’re paying a utility bill, a cheque may suffice, as the amount is typically small and the risk of non-payment is low. However, for large transactions like purchasing a car or making a security deposit, a bank draft is advisable. It’s also worth noting that obtaining a bank draft usually involves a fee, as the bank is taking on the responsibility of guaranteeing the funds. This cost should be factored into the decision-making process.

A critical takeaway is that the issuer’s role directly impacts the perceived security of the payment. Cheques rely on the account holder’s integrity and financial stability, whereas bank drafts leverage the bank’s credibility and resources. For instance, international transactions often favor bank drafts because they eliminate concerns about foreign cheque clearance processes and currency fluctuations. Additionally, bank drafts are typically processed faster than cheques, which can take several days to clear, depending on the banking system.

In summary, while both cheques and bank drafts serve as payment instruments, their issuer responsibility sets them apart. Cheques depend on individual accountability, making them suitable for routine, low-risk transactions. Bank drafts, backed by the bank’s guarantee, are ideal for high-value or critical payments where certainty is paramount. Recognizing this distinction ensures that you select the most appropriate method for your financial needs, balancing convenience, cost, and security.

Step-by-Step Guide to Setting Up NAB Internet Banking Easily

You may want to see also

Explore related products

![]()

Payment Guarantee: Bank drafts offer stronger guarantees compared to cheques, which can bounce

A bounced cheque is a financial hiccup that can disrupt transactions and damage relationships. Bank drafts, however, eliminate this risk entirely. When you purchase a bank draft, the funds are immediately withdrawn from your account and held by the bank, guaranteeing the recipient receives the full amount. This process ensures the payment is secure and irrevocable, providing peace of mind for both parties involved.

Cheques, on the other hand, rely on the payer’s account having sufficient funds at the time of deposit. If the account is overdrawn or funds are insufficient, the cheque bounces, leaving the recipient unpaid and potentially incurring fees. For high-value transactions or when trust is paramount, this uncertainty makes cheques a less reliable option.

Consider a scenario where a buyer purchases a car from a private seller. Paying with a cheque introduces a delay, as the seller must wait for the cheque to clear before releasing the vehicle. If the cheque bounces, the seller is left without payment and the buyer without the car, creating a frustrating and costly situation. A bank draft, however, provides immediate assurance that the funds are available, streamlining the transaction and reducing risk.

To illustrate the difference in guarantees, imagine a contractor hired for a renovation project. The homeowner pays with a cheque, but later discovers the account lacks sufficient funds. The contractor is left unpaid, delaying the project and straining the professional relationship. Had the homeowner used a bank draft, the contractor would have received guaranteed payment upfront, avoiding this issue entirely.

When choosing between a cheque and a bank draft, assess the transaction’s value, the level of trust between parties, and the urgency of payment. For significant purchases, international transactions, or situations requiring immediate certainty, a bank draft’s stronger guarantee outweighs its slightly higher cost. Always verify the recipient’s acceptance of bank drafts, as some entities may have specific payment policies. By prioritizing payment security, you safeguard both your finances and your reputation.

Step-by-Step Guide to Securely Logout of Kotak Net Banking

You may want to see also

Explore related products

![]()

Processing Time: Bank drafts clear faster than cheques due to bank-backed assurance

Bank drafts and cheques may seem interchangeable, but their processing times differ significantly due to the underlying assurances they carry. A bank draft is essentially a cheque drawn by a bank on its own funds, guaranteeing payment to the recipient. This bank-backed assurance streamlines the clearing process, as the funds are already verified and secured. In contrast, a cheque is drawn on an individual’s or entity’s account, requiring additional verification steps to ensure sufficient funds. This fundamental difference explains why bank drafts clear faster—often within 24 to 48 hours—while cheques can take 3 to 5 business days or longer, depending on the bank and transaction complexity.

Consider a scenario where a business needs to make a time-sensitive payment. Using a bank draft ensures the recipient receives the funds almost immediately, reducing the risk of delays or bounced payments. For instance, if a company is purchasing inventory from an international supplier, a bank draft can expedite the transaction, ensuring the goods are shipped without delay. Cheques, however, introduce uncertainty, as the clearing process involves multiple steps, including fund verification and interbank transfers. This delay can be critical in situations where timing is crucial, such as meeting contractual deadlines or securing limited stock.

From a practical standpoint, understanding these processing times can help individuals and businesses choose the right payment method for their needs. For high-value or urgent transactions, bank drafts are the preferred choice due to their speed and reliability. However, they often come with a fee, typically ranging from $5 to $25, depending on the bank and transaction amount. Cheques, while slower, are cost-effective for routine payments where time is not a pressing factor. For example, paying rent or settling small invoices can be done via cheque without incurring additional costs.

A key takeaway is that the faster processing of bank drafts is directly tied to the bank’s guarantee, which eliminates the need for extensive verification. This makes bank drafts a more efficient tool for transactions requiring immediate fund availability. However, it’s essential to weigh the cost of the bank draft fee against the urgency of the payment. For instance, if a freelancer needs to pay a vendor within 48 hours to avoid penalties, the $10 fee for a bank draft might be a worthwhile investment. Conversely, if the payment deadline is flexible, a cheque could suffice, saving both parties unnecessary expenses.

In summary, while both bank drafts and cheques serve as payment instruments, their processing times reflect their structural differences. Bank drafts clear faster due to the bank’s assurance, making them ideal for urgent or high-value transactions. Cheques, though slower, remain a practical option for routine payments. By understanding these nuances, individuals and businesses can make informed decisions, ensuring their financial transactions align with their timing and budgetary needs.

Grand Banks 32: Kindly Sea Vessels

You may want to see also

Explore related products

![]()

Fees and Costs: Bank drafts typically incur higher fees than cheques for issuance

Bank drafts and cheques may seem interchangeable, but their fee structures tell a different story. While both serve as payment instruments, bank drafts typically come with higher issuance fees. This disparity arises from the distinct processes involved: a bank draft guarantees funds by debiting the payer’s account immediately, whereas a cheque relies on the payer’s account balance at the time of deposit. This added assurance of cleared funds for the recipient justifies the premium cost of a bank draft.

Consider a practical scenario: a landlord requests a security deposit. Opting for a bank draft ensures the funds are immediately available, reducing the risk of bounced payments. However, this convenience comes at a price—banks often charge between $5 and $15 for a bank draft, compared to minimal or no fees for issuing a cheque. For individuals or businesses managing cash flow, this cost difference can be significant, especially when multiple transactions are involved.

From a financial planning perspective, understanding these fees is crucial. For instance, if you’re making a large payment, such as a down payment on a car, a bank draft might be preferred for its reliability, despite the higher fee. Conversely, for routine payments where trust exists between parties, a cheque suffices, saving you money. The key is to weigh the cost against the need for guaranteed funds.

To minimize expenses, explore alternatives. Some banks offer discounted or waived fees for premium account holders, while others may bundle services. Additionally, consider digital payment methods like wire transfers or e-transfers, which often have lower fees and faster processing times. By comparing options, you can make an informed decision that balances cost and convenience.

In conclusion, while bank drafts provide the advantage of guaranteed funds, their higher fees make them a costlier choice compared to cheques. By evaluating your specific needs and exploring alternatives, you can navigate this financial trade-off effectively, ensuring both security and savings in your transactions.

Counting 20p Coins: Understanding the Quantity in a Standard Bank Bag

You may want to see also

Frequently asked questions

No, a cheque and a bank draft are not the same. A cheque is a written instruction from an account holder to their bank to pay a specified amount to the payee, while a bank draft is a payment instrument issued by a bank, guaranteeing the availability of funds.

A bank draft is generally considered more secure than a cheque because it is issued by a bank after verifying and deducting funds from the payer’s account, ensuring the payment is guaranteed. A cheque, however, depends on the payer’s account having sufficient funds at the time of deposit.

Cheques can typically be canceled by the issuer before they are deposited or cleared, but bank drafts are more difficult to cancel as they are prepaid and guaranteed by the bank. Cancellation of a bank draft usually requires a formal request and may involve fees or conditions.