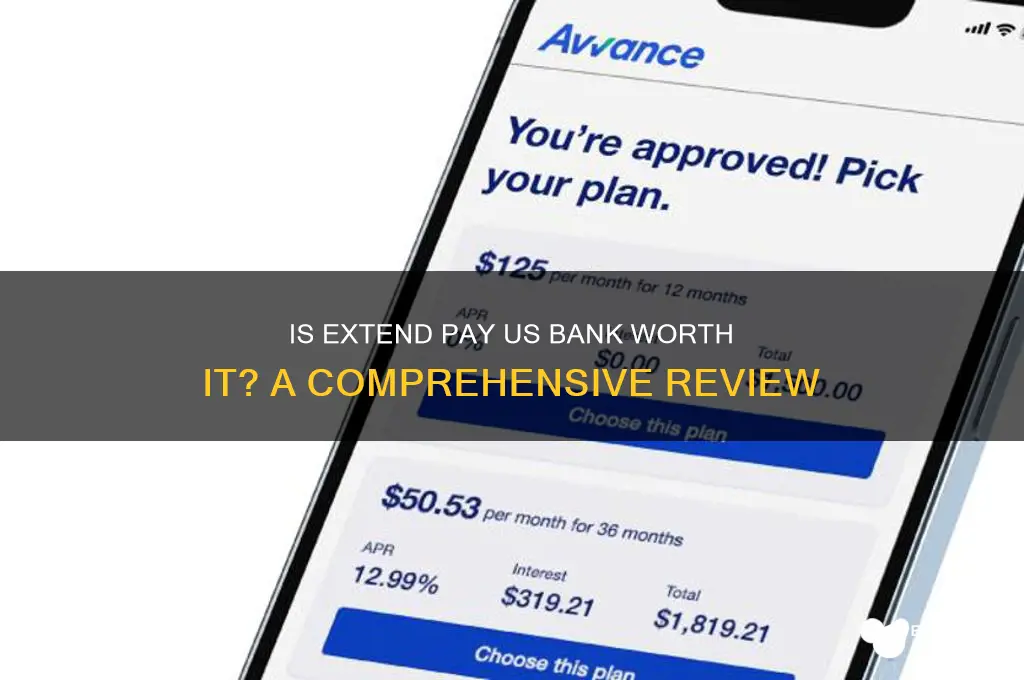

When considering whether Extend Pay through US Bank is worth it, it’s essential to evaluate its features, benefits, and potential drawbacks. Extend Pay is a service offered by US Bank that allows customers to split purchases into smaller, more manageable payments, often with no interest or fees, depending on the terms. This can be particularly appealing for those looking to budget large expenses or avoid high-interest credit card debt. However, its value depends on individual financial needs, spending habits, and the specific terms of the program. For those who struggle with lump-sum payments or prefer structured repayment plans, Extend Pay could be a useful tool. Yet, it’s crucial to compare it with other financing options, such as credit cards or personal loans, to ensure it aligns with your financial goals and doesn’t lead to overspending. Ultimately, whether Extend Pay is worth it hinges on how well it fits into your overall financial strategy.

Explore related products

What You'll Learn

![]()

Fees and Charges Overview

Understanding the fees and charges associated with Extend Pay US Bank is crucial for determining its value. Unlike traditional banks, Extend Pay operates on a subscription model, charging a flat monthly fee of $9.99 for its basic plan. This fee includes access to early paycheck deposits, budgeting tools, and overdraft protection up to $200. While this may seem straightforward, it’s essential to compare it to the hidden or variable fees of conventional banking. For instance, overdraft fees at major banks can range from $25 to $35 per transaction, quickly dwarfing Extend Pay’s monthly cost if you frequently overdraw.

Consider the scenario of a user who overdrafts twice in a month. At a traditional bank, this could result in $70 in fees, whereas Extend Pay’s $9.99 subscription covers the overdraft without additional charges. However, if you rarely overdraft or incur fees, the monthly subscription might feel unnecessary. To maximize value, assess your banking habits: do you frequently rely on overdraft protection, or do you maintain a stable balance? Extend Pay’s fee structure is most beneficial for those who need predictable, low-cost access to emergency funds.

Another critical aspect is the absence of transaction fees for basic services like transfers and ATM withdrawals. Extend Pay partners with Allpoint to provide fee-free access to over 55,000 ATMs nationwide. In contrast, out-of-network ATM fees at traditional banks average $3 to $5 per transaction, plus any fees charged by the ATM owner. If you frequently use ATMs outside your bank’s network, Extend Pay’s fee-free access could save you $15 to $25 monthly, offsetting the subscription cost.

For those considering upgrading to Extend Pay’s premium plan ($19.99/month), additional benefits include higher overdraft limits ($500) and cashback rewards on debit purchases. While this plan doubles the cost, it could be worth it if you utilize the increased overdraft protection and earn enough cashback to offset the fee. For example, earning 1% cashback on $2,000 in monthly debit spending yields $20, effectively covering the premium subscription cost.

In conclusion, Extend Pay’s fee structure is designed to offer transparency and predictability, particularly for users prone to overdrafts or reliant on ATM access. To determine if it’s worth it, calculate your potential savings on overdraft and ATM fees against the subscription cost. If the savings exceed the fee, or if you value the added benefits like early paycheck access, Extend Pay could be a cost-effective alternative to traditional banking. However, if your banking needs are minimal and you rarely incur fees, the subscription model may not align with your financial habits.

Elizabeth Banks Hosting Press Your Luck: Fact or Fiction?

You may want to see also

Explore related products

![]()

Interest Rates Comparison

Interest rates are the cornerstone of any financial decision, and Extend Pay US Bank is no exception. When evaluating whether this service is worth it, a meticulous comparison of interest rates is essential. Unlike traditional banks, Extend Pay often positions itself as a flexible payment solution, but flexibility can come at a cost. Start by comparing their annual percentage rates (APRs) with those of credit cards, personal loans, and buy-now-pay-later (BNPL) services. For instance, while BNPL options like Affirm or Klarna may offer 0% interest for short-term plans, Extend Pay’s rates could be higher for longer repayment periods. Always check if their rates are fixed or variable, as variable rates can fluctuate with market conditions, potentially increasing your costs over time.

Analyzing the fine print is crucial when comparing interest rates. Extend Pay may advertise low introductory rates to attract users, but these often revert to higher rates after a promotional period. For example, a 6-month 0% APR offer might jump to 18% or more afterward. Compare this to a standard credit card with a fixed 15% APR, which could be more predictable in the long run. Additionally, consider the effective annual rate (EAR), which accounts for compounding frequency. If Extend Pay compounds interest monthly, a 17% APR could translate to a higher EAR than a 17% APR compounded annually on a traditional loan.

For practical decision-making, calculate the total cost of borrowing under different scenarios. Suppose you’re financing a $1,000 purchase. With Extend Pay at 18% APR over 12 months, you’d pay approximately $92 in interest. Compare this to a personal loan at 12% APR, where the interest would be around $60. If you’re disciplined with payments, a lower-rate option like a personal loan or balance transfer credit card might save you money. However, if Extend Pay’s flexibility (e.g., deferred payments or no credit check) aligns with your financial situation, the higher interest rate might be a trade-off worth considering.

Persuasively, it’s worth noting that interest rates aren’t the only factor in determining value. Extend Pay may offer benefits like no late fees, no credit impact for missed payments, or seamless integration with your existing bank account. If these features outweigh the higher interest costs, it could still be a worthwhile option. For instance, someone with irregular income might prioritize the flexibility to pause payments over a slightly lower interest rate elsewhere. Ultimately, the decision hinges on your financial priorities and how Extend Pay’s interest rates fit into your broader budget.

In conclusion, a thorough interest rate comparison requires looking beyond the headline numbers. Evaluate Extend Pay’s rates against alternatives, scrutinize the terms for hidden costs, and calculate the total borrowing expense. While higher interest rates might seem like a deal-breaker, the added flexibility or convenience could justify the expense for certain users. Always align your choice with your financial goals and repayment capabilities.

Go Paperless with HSA Bank: A Step-by-Step Setup Guide

You may want to see also

Explore related products

![]()

Customer Service Quality

To evaluate whether Extend Pay US Bank’s customer service is worth it, consider their support channels. The bank offers phone, email, and live chat options, but the devil is in the details. Phone support, though immediate, often comes with hold times exceeding 20 minutes during peak hours. Live chat, on the other hand, is quicker but limited to basic inquiries, leaving customers with intricate issues stranded. Email support, while thorough, can take up to 48 hours for a response—an eternity for urgent matters. This tiered system may work for some, but it risks alienating those needing timely, comprehensive assistance.

A persuasive argument for Extend Pay US Bank’s customer service lies in its personalized approach—at least in theory. Account managers are assigned to premium customers, offering tailored support that goes beyond generic solutions. However, this perk comes at a cost, often requiring a minimum account balance or fee structure. For the average user, this level of service remains out of reach, leaving them to navigate the standard support system. This two-tiered model raises questions about inclusivity and whether the bank prioritizes profitability over universal customer satisfaction.

Comparatively, Extend Pay US Bank’s customer service holds its own against some competitors but lags behind others. For example, while it outperforms smaller regional banks in terms of availability (24/7 support vs. limited hours), it falls short when compared to digital-first banks that leverage AI and human agents seamlessly. The latter often resolve issues in real-time, setting a benchmark Extend Pay struggles to meet. This gap underscores the need for the bank to invest in technology and training to stay competitive.

In conclusion, Extend Pay US Bank’s customer service quality is a double-edged sword. While it offers potential value through personalized support for premium users and multiple contact channels, it falters in consistency and accessibility for the average customer. Practical tips for users include leveraging live chat for quick questions, avoiding peak hours for phone calls, and escalating unresolved issues to a supervisor. Ultimately, whether the service is "worth it" depends on individual needs and patience—but for now, it’s a gamble rather than a guarantee.

Exploring Abay Bank's Reach: Total Number of Branches Revealed

You may want to see also

Explore related products

![]()

Account Features Analysis

Extend Pay US Bank's account features cater to a specific niche: those seeking a second chance at traditional banking. Their flagship offering, the Extend Pay Checking Account, boasts a unique combination of accessibility and financial management tools.

Unlike traditional banks with stringent credit checks, Extend Pay prioritizes inclusivity, making it an attractive option for individuals with past financial missteps. This account doesn't require a minimum deposit to open, removing a common barrier to entry.

A standout feature is the built-in budgeting tool. This tool allows users to categorize transactions, set spending limits, and track their progress towards financial goals. For individuals struggling with budgeting, this feature provides a structured framework for responsible money management. Additionally, the account offers early direct deposit, a perk that can be crucial for those living paycheck to paycheck, providing access to funds up to two days earlier than traditional banks.

While Extend Pay offers a compelling suite of features, it's important to consider the fee structure. The monthly maintenance fee, while not exorbitant, can add up over time. However, the fee is waived for customers who maintain a minimum balance or set up direct deposits, incentivizing responsible financial habits.

For those seeking a fresh start and willing to utilize the budgeting tools, Extend Pay US Bank presents a viable option. The combination of accessibility, early direct deposit, and budgeting assistance makes it a strong contender for individuals looking to rebuild their financial standing. However, careful consideration of the fee structure and a commitment to utilizing the account's features are essential for maximizing its benefits.

Step-by-Step Guide to Applying for SSY in ICICI Bank

You may want to see also

Explore related products

![]()

Pros and Cons Summary

Pro: Flexibility in Payment Scheduling

Extend Pay US Bank allows users to split large purchases into smaller, manageable payments, often with no interest for a set period. For instance, a $500 purchase could be divided into four $125 payments over two months. This feature is particularly beneficial for unexpected expenses or high-ticket items, providing financial breathing room without the immediate strain of a lump-sum payment. However, this flexibility hinges on strict adherence to payment schedules—miss one, and late fees or penalties can negate the benefit.

Con: Limited Merchant Acceptance

While Extend Pay US Bank offers convenience, its usability is constrained by merchant partnerships. Currently, only select retailers and service providers accept this payment method, which may exclude users from leveraging it for everyday or niche purchases. For example, if your favorite grocery store or utility provider isn’t on the list, the service’s value diminishes significantly. Always verify merchant compatibility before relying on this option.

Pro: Potential for Building Credit

When used responsibly, Extend Pay US Bank can contribute positively to your credit score. On-time payments are reported to credit bureaus, which can improve your credit history over time. This is especially advantageous for individuals with limited or poor credit, as it provides a structured way to demonstrate financial reliability. However, this benefit requires disciplined use—late payments can harm your credit instead.

Con: Risk of Overspending

The ease of splitting payments can create a psychological trap, encouraging users to spend beyond their means. For example, a $1,000 purchase might feel more affordable when broken into $250 installments, but multiple such transactions can quickly accumulate, leading to financial strain. To mitigate this, set a budget for Extend Pay usage and avoid using it for non-essential purchases.

Takeaway: Context Determines Value

Extend Pay US Bank is worth it for individuals who need short-term financial flexibility, have a history of on-time payments, and shop at participating merchants. However, it’s not ideal for those prone to overspending or lacking merchant compatibility. Assess your spending habits, financial goals, and the service’s terms before committing. Used strategically, it can be a valuable tool; misused, it becomes a liability.

Exploring the Global Reach: How Many International Banks Exist Worldwide?

You may want to see also

Frequently asked questions

Extend Pay US Bank can be worth it if you need flexibility in managing your credit card payments, as it offers options like splitting purchases into smaller payments. However, it’s important to review fees and terms to ensure it aligns with your financial goals.

Extend Pay US Bank may charge fees depending on the plan or service you choose. Compare these fees with potential interest savings or alternative payment methods to determine if it’s cost-effective for you.

Extend Pay US Bank itself does not directly improve your credit score, but using it responsibly to manage payments and avoid late fees can indirectly support better credit management.

Extend Pay US Bank can be useful for large purchases by breaking them into smaller, manageable payments. However, ensure the terms and fees are favorable compared to other financing options like 0% APR offers or personal loans.