Investing in bank stocks can be a lucrative opportunity, but it requires careful consideration of various factors. Bank stocks are often seen as a stable, long-term investment due to the essential role banks play in the economy, offering services like lending, deposits, and financial products. However, their performance is closely tied to interest rates, economic conditions, and regulatory environments, which can introduce volatility. Additionally, banks’ financial health, including their loan portfolios and capital reserves, must be thoroughly evaluated. While dividends and potential for growth make bank stocks attractive, investors should weigh these benefits against risks like economic downturns or increased competition from fintech companies. Ultimately, whether buying bank stocks is a good decision depends on individual risk tolerance, investment goals, and market conditions.

Explore related products

What You'll Learn

- Bank Stock Pros: Stable dividends, long-term growth potential, and economic resilience make bank stocks attractive

- Market Volatility: Bank stocks can fluctuate with interest rates and economic downturns

- Regulatory Impact: Government policies and regulations significantly influence bank profitability and stock performance

- Financial Health: Strong balance sheets and low debt ratios indicate safer bank stock investments

- Dividend Yield: Banks often offer higher dividend yields compared to other sectors, appealing to income investors

![]()

Bank Stock Pros: Stable dividends, long-term growth potential, and economic resilience make bank stocks attractive

Bank stocks have long been a cornerstone of conservative investment portfolios, and for good reason. One of their most compelling attributes is the stable dividends they offer. Unlike growth-focused sectors that reinvest profits, banks typically distribute a significant portion of earnings to shareholders. For instance, JPMorgan Chase has consistently paid dividends for decades, even increasing payouts during economic downturns. This reliability makes bank stocks particularly attractive for income-seeking investors, such as retirees or those building passive income streams. A dividend yield of 3-5% is common among major banks, outpacing many fixed-income alternatives like bonds or savings accounts.

Beyond dividends, bank stocks boast long-term growth potential tied to the broader economy. Banks thrive as economies expand, since increased lending, deposits, and financial activity drive revenue. Historical data shows that bank stocks have delivered average annual returns of 8-10% over the past three decades, rivaling the S&P 500. For example, Wells Fargo’s stock price grew over 700% from 1990 to 2020, despite occasional setbacks. Investors with a buy-and-hold strategy can capitalize on this growth, especially when reinvesting dividends. However, it’s crucial to select banks with strong fundamentals, such as low non-performing loans and robust capital ratios, to maximize long-term gains.

Another advantage of bank stocks is their economic resilience, which stems from their central role in the financial system. During recessions, while many sectors suffer, banks often benefit from increased government support and policy measures aimed at stabilizing the economy. For instance, the 2008 financial crisis led to unprecedented bailouts and low-interest-rate environments, which ultimately bolstered bank profitability in the recovery phase. Additionally, banks’ diversified revenue streams—from mortgages and credit cards to investment banking—provide a buffer against sector-specific shocks. This resilience makes them a defensive play in volatile markets.

To maximize the benefits of bank stocks, investors should adopt a strategic approach. Start by diversifying across regional and national banks to mitigate risks tied to specific markets. For example, pairing a large multinational bank like Citigroup with a regional player like U.S. Bancorp can balance growth and stability. Second, monitor key metrics such as net interest margin, return on equity, and loan-to-deposit ratio to gauge a bank’s health. Finally, consider reinvesting dividends through DRIP (Dividend Reinvestment Plans) to compound returns over time. With disciplined research and a long-term perspective, bank stocks can be a cornerstone of a resilient and rewarding portfolio.

Accessing Past Bank Statements: A Step-by-Step Guide to Retrieving Older Records

You may want to see also

Explore related products

![]()

Market Volatility: Bank stocks can fluctuate with interest rates and economic downturns

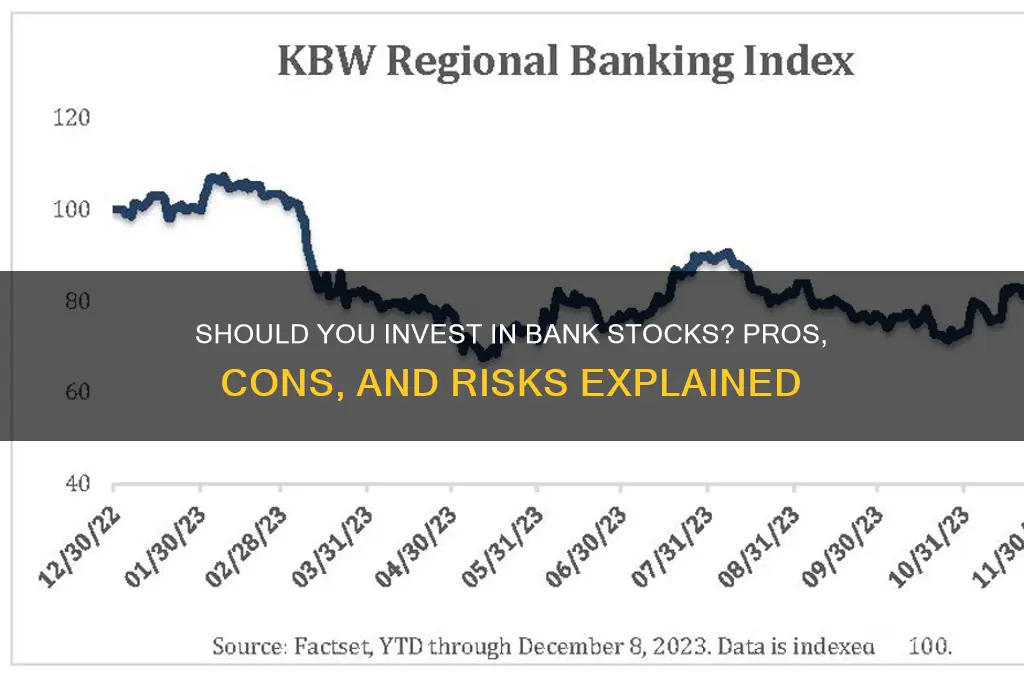

Bank stocks are inherently tied to the broader economic cycle, making them particularly sensitive to market volatility. Interest rates, set by central banks, act as a primary driver of this volatility. When rates rise, banks often benefit from higher net interest margins—the difference between what they earn on loans and pay on deposits. However, this dynamic can reverse during economic downturns, as higher rates may lead to reduced borrowing, increased loan defaults, and a contraction in credit demand. For instance, during the 2022 rate hikes by the Federal Reserve, regional bank stocks initially rallied but later faced pressure as recession fears mounted. Understanding this relationship is crucial for investors, as it highlights the dual-edged sword of interest rates on bank profitability.

To navigate this volatility, investors should adopt a proactive approach by monitoring economic indicators such as GDP growth, unemployment rates, and inflation data. These metrics provide early signals of potential shifts in monetary policy and economic health, which directly impact bank stocks. For example, a flattening yield curve—where short-term interest rates approach long-term rates—historically precedes recessions and can signal trouble for bank earnings. Tools like financial news platforms, economic calendars, and analyst reports can help investors stay informed. Additionally, diversifying across different types of banks (e.g., regional vs. national) and sectors can mitigate risks associated with interest rate fluctuations.

A comparative analysis of bank stocks during past economic cycles reveals valuable lessons. During the 2008 financial crisis, bank stocks plummeted due to widespread loan defaults and a collapse in housing markets. In contrast, the post-2020 recovery saw bank stocks surge as low interest rates fueled lending and economic growth. However, the subsequent rate hikes in 2022 introduced new challenges, such as deposit outflows and margin compression. This historical perspective underscores the cyclical nature of bank stocks and the importance of timing investments based on macroeconomic conditions. Investors who study these patterns can better anticipate how bank stocks might perform in different phases of the economic cycle.

Despite the risks, bank stocks offer long-term potential for investors willing to tolerate volatility. Dividend yields from established banks often exceed those of the broader market, providing a cushion during downturns. Moreover, banks with strong balance sheets and diversified revenue streams are better positioned to weather economic storms. Practical tips include focusing on banks with low loan-to-deposit ratios, robust capital reserves, and a history of prudent risk management. For younger investors with a longer time horizon, dollar-cost averaging into bank stocks during volatile periods can reduce entry risks. Conversely, older investors nearing retirement may prefer more stable, income-focused strategies, such as investing in preferred shares or bank-focused ETFs.

In conclusion, market volatility in bank stocks is inextricably linked to interest rates and economic downturns, creating both opportunities and challenges. By staying informed, adopting strategic diversification, and learning from historical cycles, investors can navigate this volatility effectively. While bank stocks may not be suitable for all risk profiles, their potential for growth and income makes them a compelling option for those who approach them with careful consideration and a long-term perspective.

Recording Bank Chargebacks in QuickBooks: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Regulatory Impact: Government policies and regulations significantly influence bank profitability and stock performance

Government policies and regulations act as a double-edged sword for bank stocks. On one hand, stringent regulations like higher capital requirements (think Basel III accords mandating banks to hold more capital as a buffer against losses) can squeeze profitability by limiting lending capacity and increasing operational costs. This often translates to lower returns for shareholders. For instance, post-2008 financial crisis regulations led to a noticeable dip in bank stock valuations as institutions grappled with compliance costs and reduced risk-taking appetite.

On the other hand, well-designed regulations can foster stability and long-term growth. Deposit insurance schemes, for instance, bolster public confidence in the banking system, encouraging deposits and enabling banks to lend more. Similarly, regulations promoting transparency and fair lending practices can mitigate systemic risks, ultimately benefiting both banks and investors.

Consider the Dodd-Frank Act in the US, which imposed stricter oversight on systemic banks deemed "too big to fail." While initially viewed as a drag on profitability, it arguably contributed to a more resilient banking sector, as evidenced by the relatively muted impact of the 2020 pandemic on major US banks compared to their European counterparts. This highlights the importance of context: the same regulation can have vastly different effects depending on the economic environment and the specific bank's business model.

A regional bank heavily reliant on mortgage lending, for example, might be disproportionately affected by regulations tightening lending standards, while a diversified global bank with a strong investment banking arm could weather such changes more easily.

Therefore, investors eyeing bank stocks must meticulously analyze the regulatory landscape. This involves scrutinizing not just existing regulations but also anticipating potential policy shifts. Tracking central bank statements, legislative proposals, and international regulatory trends is crucial. Additionally, understanding a bank's specific exposure to regulatory risks based on its business model and geographic footprint is essential for making informed investment decisions.

Arvest Bank: Coin Counter Availability and Features

You may want to see also

Explore related products

![]()

Financial Health: Strong balance sheets and low debt ratios indicate safer bank stock investments

Bank stocks often attract investors seeking stability and dividend income, but not all banks are created equal. A critical factor in assessing their investment potential lies in their financial health, particularly the strength of their balance sheets and debt ratios. These metrics serve as vital signs, revealing a bank’s ability to weather economic storms and sustain long-term growth. For instance, during the 2008 financial crisis, banks with robust balance sheets and conservative debt levels, like JPMorgan Chase, outperformed their peers, demonstrating resilience in turbulent times. This historical example underscores the importance of scrutinizing these financial indicators before committing capital.

To evaluate a bank’s financial health, start by examining its balance sheet. A strong balance sheet is characterized by a high proportion of liquid assets, such as cash and government securities, relative to illiquid assets like loans. This liquidity ensures the bank can meet its short-term obligations without resorting to costly emergency measures. Additionally, look for a healthy loan-to-deposit ratio, ideally below 80%, which indicates the bank funds its lending activities primarily through customer deposits rather than borrowed capital. Banks like Wells Fargo have historically maintained such ratios, contributing to their stability.

Equally important is the bank’s debt ratio, a measure of its leverage. A low debt-to-equity ratio, typically below 10%, signals that the bank relies more on equity than debt to finance its operations, reducing financial risk. For example, Bank of America’s focus on deleveraging post-2008 has strengthened its balance sheet, making it a safer bet for investors. Conversely, banks with high debt ratios are more vulnerable to interest rate hikes and economic downturns, as seen with smaller regional banks during the 2023 banking sector turmoil.

Practical tips for investors include comparing a bank’s financial ratios to industry benchmarks and its historical performance. Tools like Morningstar or Bloomberg provide these metrics, enabling a side-by-side analysis. Additionally, consider the bank’s net interest margin (NIM), which reflects its profitability from lending activities. A stable or improving NIM, coupled with strong capital adequacy ratios (above 10%), further reinforces the bank’s financial health. For instance, U.S. Bancorp’s consistent NIM and capital ratios have made it a favorite among income-focused investors.

In conclusion, investing in bank stocks requires a meticulous focus on financial health, with strong balance sheets and low debt ratios serving as key indicators of safety. By prioritizing these metrics, investors can identify banks better positioned to deliver stable returns, even in challenging economic environments. As with any investment, diversification is crucial, but within the banking sector, financial health is the cornerstone of a safer portfolio.

Is Bank of the West Being Sold? Latest Updates and Insights

You may want to see also

Explore related products

![]()

Dividend Yield: Banks often offer higher dividend yields compared to other sectors, appealing to income investors

Bank stocks have long been a staple in income-oriented portfolios, and one of their most attractive features is their dividend yield. On average, banks offer dividend yields that outpace those of many other sectors, often ranging between 3% and 5%, compared to the S&P 500’s historical average of around 2%. This disparity makes them particularly appealing to investors seeking steady income streams, especially retirees or those nearing retirement who prioritize cash flow over capital appreciation. For instance, JPMorgan Chase and Wells Fargo consistently rank among the top dividend-paying banks, with yields that have historically exceeded broader market averages.

However, it’s not just the yield itself that matters—it’s the sustainability of those dividends. Banks’ ability to maintain or grow payouts hinges on their financial health, which is closely tied to economic conditions. During economic expansions, banks thrive on increased lending activity and higher interest margins, bolstering their dividend-paying capacity. Conversely, downturns can strain balance sheets, leading to dividend cuts or suspensions, as seen during the 2008 financial crisis. Income investors must therefore assess a bank’s capital adequacy ratios, loan quality, and stress test results to gauge the reliability of its dividend.

To maximize the benefits of bank dividends, investors should adopt a strategic approach. Diversification across multiple banks can mitigate risks associated with any single institution’s performance. Additionally, reinvesting dividends through dividend reinvestment plans (DRIPs) can compound returns over time, turning a steady income stream into a growing equity position. For example, an investor who reinvested dividends from Bank of America over the past decade would have seen their holdings grow significantly, even amid periods of volatility.

Despite their allure, bank dividends aren’t without drawbacks. Regulatory scrutiny often limits how much capital banks can return to shareholders, particularly during uncertain economic times. Moreover, high yields can sometimes signal undervaluation or market skepticism about a bank’s prospects. Investors should thus balance yield considerations with fundamental analysis, examining metrics like price-to-book ratios and return on equity to ensure they’re not chasing yield at the expense of quality.

In conclusion, bank stocks’ higher dividend yields make them a compelling option for income investors, but this advantage comes with caveats. By focusing on dividend sustainability, adopting strategic investment practices, and conducting thorough due diligence, investors can harness the income potential of bank stocks while managing associated risks. As with any investment, the key lies in aligning the opportunity with one’s financial goals and risk tolerance.

Mastering Online Banking: A Guide to Secure Internet Transactions

You may want to see also

Frequently asked questions

Bank stocks can be a good long-term investment due to their potential for steady dividends, strong balance sheets, and exposure to economic growth. However, they are sensitive to interest rates and economic cycles, so diversification is key.

Bank stocks are generally more vulnerable during recessions due to increased loan defaults and reduced lending activity. However, well-managed banks with strong fundamentals may weather downturns better than others.

Yes, bank stocks often perform well in a rising interest rate environment because higher rates can increase their net interest margins, boosting profitability. However, this depends on the pace and magnitude of rate hikes.

Beginners can invest in bank stocks as they are relatively easy to understand and often provide stable returns. However, it’s important to research individual banks, understand their financial health, and consider broader market conditions before investing.