Your FICO score, a critical factor in determining your creditworthiness, is not directly dependent on any specific bank. Instead, it is calculated based on information from your credit reports, which are maintained by the three major credit bureaus: Equifax, Experian, and TransUnion. Banks and other lenders report your credit activity to these bureaus, and the FICO scoring model uses this data to generate your score. While different banks may use varying versions of the FICO scoring model or even their own proprietary scoring systems, the underlying data remains consistent across institutions. Therefore, your FICO score is an independent metric that reflects your overall credit health, rather than being influenced by any single bank's policies or practices.

Explore related products

$2.99 $17.99

What You'll Learn

![]()

FICO Score Calculation Basics

Your FICO score, a three-digit number ranging from 300 to 850, is a snapshot of your creditworthiness, but it’s not a one-size-fits-all metric. While banks and lenders use FICO scores to assess risk, the score itself isn’t dependent on any single bank. Instead, it’s calculated based on data from your credit reports, which are maintained by the three major credit bureaus: Equifax, Experian, and TransUnion. Each bureau may have slightly different information about your credit history, leading to variations in your FICO score across bureaus. This means your score can differ depending on which bureau’s data is used, but the calculation method remains consistent.

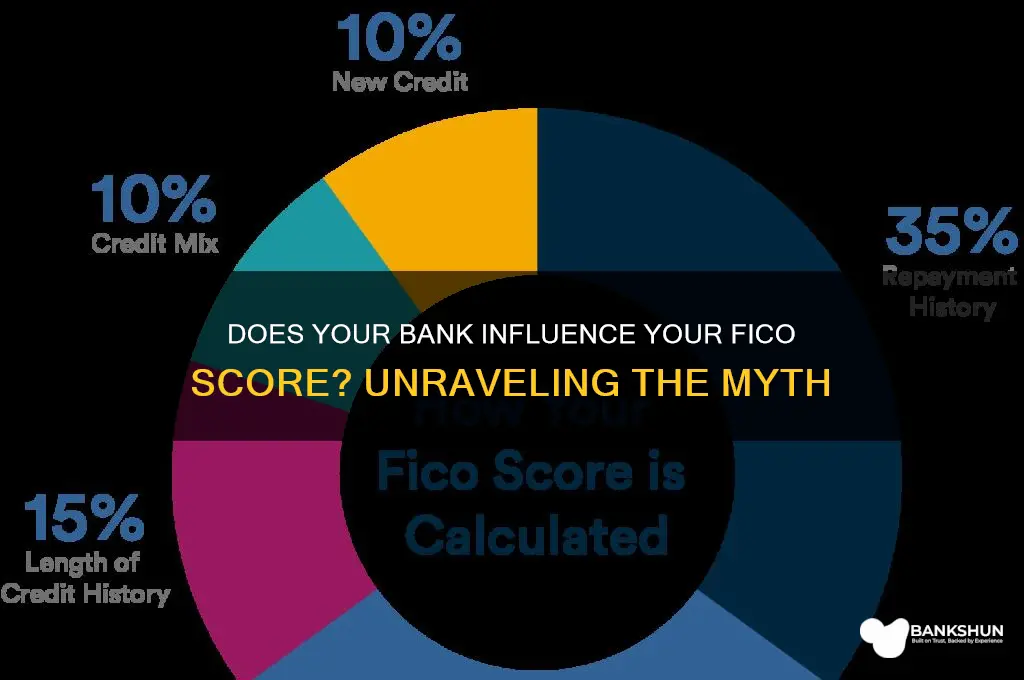

The FICO score calculation is rooted in five key factors, each weighted differently. Payment history carries the most weight at 35%, as it reflects your reliability in paying bills on time. Amounts owed account for 30%, focusing on your credit utilization ratio—ideally below 30% of your total available credit. Length of credit history (15%) rewards longer credit histories, while new credit (10%) considers recent credit inquiries and account openings. Finally, credit mix (10%) evaluates your ability to manage various types of credit, such as credit cards, loans, and mortgages. Understanding these factors empowers you to take targeted actions to improve your score.

A common misconception is that closing unused credit cards will boost your FICO score. In reality, this can harm your score by reducing your overall available credit, thereby increasing your credit utilization ratio. For example, if you have two cards with a combined limit of $10,000 and a balance of $2,000, your utilization is 20%. Closing one card with a $5,000 limit would raise your utilization to 40%, even if your spending remains the same. Instead, consider keeping older accounts open and using them sparingly to maintain a healthy credit mix and history.

While the FICO score calculation is standardized, lenders may use different FICO versions or scoring models tailored to specific credit products, such as auto loans or credit cards. For instance, a mortgage lender might use FICO Score 2, while a credit card issuer uses FICO Score 8. These versions weigh factors slightly differently, but the core principles remain unchanged. To navigate this, focus on universal best practices: pay bills on time, keep credit card balances low, avoid opening multiple accounts at once, and regularly monitor your credit reports for errors.

In practice, your FICO score isn’t tied to a specific bank but is influenced by your financial behaviors and how they’re reported to the credit bureaus. For instance, paying off a high credit card balance can quickly improve your score by lowering your credit utilization. Similarly, disputing inaccuracies on your credit report can remove negative marks that unfairly lower your score. By understanding the basics of FICO score calculation, you gain control over this critical financial metric, ensuring it accurately reflects your creditworthiness regardless of which lender or bureau is evaluating it.

Claiming Bank Charges in GST: A Step-by-Step Guide for Businesses

You may want to see also

Explore related products

![]()

Bank Reporting Practices Impact

Your FICO score, a critical measure of creditworthiness, is not directly dependent on any single bank. However, bank reporting practices significantly influence its calculation. Each bank reports your credit activity to the three major credit bureaus—Experian, Equifax, and TransUnion—but inconsistencies in reporting frequency, accuracy, and completeness can lead to variations in your score. For instance, one bank might report monthly, while another reports quarterly, causing delays in reflecting positive changes like paid-off balances. These discrepancies highlight the importance of understanding how banks handle your credit data.

Analyzing the impact of reporting frequency reveals a practical example: if Bank A reports your credit card balance on the 15th of each month, but Bank B reports on the 1st, a large purchase made on the 2nd could inflate your credit utilization ratio in Bank B’s report. This temporary spike might lower your FICO score, even if you pay off the balance before Bank A’s reporting date. To mitigate this, monitor your credit utilization and consider paying down balances before the statement closing date, ensuring a lower reported balance across all banks.

Accuracy in reporting is another critical factor. Errors in reported account statuses, balances, or payment histories can unfairly penalize your score. For example, a bank might mistakenly report a late payment that never occurred. Such errors are not uncommon; the Federal Trade Commission found that 26% of consumers identified errors on their credit reports. To address this, regularly review your credit reports for inaccuracies and dispute them promptly with both the bank and the credit bureau. Tools like annualcreditreport.com allow free access to your reports, making this a straightforward but essential habit.

Comparing banks’ reporting practices also shows that some institutions are more diligent than others. For instance, credit unions often report more consistently and accurately compared to larger banks, which may prioritize volume over precision. If you notice recurring issues with a particular bank’s reporting, consider consolidating accounts with institutions known for better practices. Additionally, using a single credit card for most transactions can simplify monitoring and reduce the risk of discrepancies across multiple banks.

In conclusion, while your FICO score isn’t bank-dependent, bank reporting practices wield considerable influence. By understanding reporting frequencies, ensuring accuracy, and strategically managing accounts, you can minimize negative impacts and maintain a healthier credit profile. Proactive monitoring and informed account management are key to navigating this often-overlooked aspect of credit health.

Recording Bank Fees in GnuCash: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Credit Card Influence on FICO

Your FICO score, a critical determinant of creditworthiness, is not directly dependent on any single bank. However, the credit cards you hold and how you manage them can significantly influence your score. This influence stems from the five key factors that FICO considers: payment history, amounts owed, length of credit history, new credit, and credit mix. Credit cards play a role in each of these categories, making their management a pivotal aspect of maintaining or improving your score.

Payment History (35% of FICO Score): The most substantial impact comes from your payment history. Late or missed payments on credit cards can severely damage your score. Conversely, consistently paying your credit card bills on time and in full demonstrates reliability, boosting your score over time. For instance, a single missed payment can drop a good credit score (680–719) by 60–110 points. To mitigate this, set up automatic payments or reminders to ensure timely payments, especially if you have multiple cards with varying due dates.

Amounts Owed (30% of FICO Score): Credit utilization—the ratio of your credit card balances to your credit limits—is a critical factor. A general rule of thumb is to keep utilization below 30%, but the lower, the better. For example, if you have a credit card with a $1,000 limit, aim to keep the balance under $300. High balances across multiple cards can signal financial strain, even if you pay them off monthly. Consider paying down balances mid-cycle or requesting a credit limit increase to improve this ratio, but only if you trust yourself not to overspend.

Length of Credit History (15% of FICO Score): The age of your credit accounts matters. Closing old credit cards can shorten your credit history, negatively impacting your score. For instance, if you’ve had a card for 10 years, keeping it open and active (even with minimal use) contributes positively to this factor. Avoid frequent account closures, especially if you’re planning a major purchase like a home or car, as lenders prefer to see a longer credit history.

New Credit (10% of FICO Score): Applying for multiple credit cards in a short period can temporarily lower your score due to hard inquiries. Each application typically reduces your score by 5–10 points, but the impact diminishes over time. However, opening several new accounts simultaneously can also increase your overall credit limit, potentially lowering your utilization ratio if managed properly. Balance the need for new credit with the potential short-term score impact, especially if you’re nearing a significant financial decision.

Credit Mix (10% of FICO Score): While credit cards are a type of revolving credit, having a mix of credit types (e.g., installment loans, mortgages) can positively influence your score. However, opening new accounts solely for diversification is not advisable. Instead, focus on managing your existing credit cards effectively. For example, if you have both a credit card and a personal loan, paying both on time demonstrates your ability to handle different credit types responsibly.

In summary, credit cards are a double-edged sword in the FICO scoring system. They offer opportunities to build credit through responsible use but can also lead to score declines if mismanaged. By focusing on timely payments, low utilization, maintaining older accounts, pacing new applications, and managing a balanced credit mix, you can maximize the positive influence of credit cards on your FICO score. Remember, consistency and discipline are key—small, sustained efforts yield significant long-term benefits.

Albert Banking App's Journey: A Timeline of Its Existence and Growth

You may want to see also

Explore related products

![]()

Loan Types and Score Effects

Your FICO score, a critical factor in loan approval and interest rates, isn’t directly dependent on the bank itself but rather on the type of loan you’re seeking. Different loan categories—mortgages, auto loans, personal loans, and credit cards—weigh FICO score components differently. For instance, mortgage lenders prioritize payment history and credit utilization more heavily than credit card issuers, who may focus on recent inquiries and account diversity. This variance means a single FICO score can have distinct implications depending on the loan type.

Consider auto loans: lenders often use industry-specific FICO Auto Scores, which emphasize past auto loan behavior. A score of 700 might secure a competitive rate for a car loan but fall short for a mortgage, where lenders typically require 740 or higher for the best terms. Conversely, credit card issuers may approve applicants with scores as low as 670, though at higher interest rates. Understanding these nuances helps borrowers target loans aligned with their score strengths.

Personal loans illustrate another layer of complexity. Since they’re unsecured, lenders scrutinize overall creditworthiness more than collateral-backed loans. A FICO score of 680 might suffice, but expect higher APRs compared to secured loans like mortgages or auto loans. Additionally, some lenders use VantageScore instead of FICO, further complicating score dependency. Always verify which scoring model a lender uses before applying.

To maximize loan approval odds, tailor your strategy to the loan type. For mortgages, focus on reducing debt-to-income ratio and maintaining a pristine payment history. For credit cards, keep utilization below 30% and limit new applications. Auto loan seekers should review their Auto Score specifically, available through myFICO.com, and address any discrepancies. Personal loan applicants should shop around, as online lenders often have more flexible criteria than traditional banks.

The takeaway? Your FICO score isn’t bank-dependent, but its impact varies by loan type. Research lender preferences, monitor your score across models, and align your financial habits with the requirements of your target loan. This proactive approach ensures you’re not just chasing a number but optimizing it for the specific credit product you need.

Mastering Test Bank NAPLEX Login: A Step-by-Step Guide for Success

You may want to see also

Explore related products

![]()

Bank Errors and Score Disputes

Bank errors can silently erode your FICO score, often without your immediate knowledge. A misplaced decimal, a duplicated entry, or a misreported late payment can shave off precious points, impacting loan approvals, interest rates, or even job prospects. For instance, a bank might report a $500 credit card balance as $5,000, skewing your credit utilization ratio—a factor that accounts for 30% of your FICO score. Such errors are more common than you’d think, with the Consumer Financial Protection Bureau (CFPB) receiving thousands of credit reporting complaints annually. Vigilance is your first line of defense; regularly review your bank statements and credit reports to catch discrepancies early.

Disputing a bank error requires precision and persistence. Start by gathering evidence: screenshots of transactions, account statements, and correspondence with the bank. File a dispute directly with the bank and the credit bureaus (Equifax, Experian, TransUnion) using certified mail to create a paper trail. Under the Fair Credit Reporting Act (FCRA), bureaus must investigate disputes within 30 days, and banks must correct inaccuracies promptly. If the bank resists, escalate the issue to the CFPB or consult a consumer law attorney. Remember, time is critical—unresolved errors can linger, compounding damage to your score.

Not all bank errors are created equal, and their impact on your FICO score varies. A minor discrepancy, like a $10 overcharge, might be negligible, but a falsely reported loan default can plummet your score by 100 points or more. Context matters: errors affecting payment history (35% of your score) or credit utilization (30%) carry heavier consequences than those tied to credit mix or inquiries. Prioritize disputes based on potential score impact, and monitor your credit report post-correction to ensure the error is fully resolved.

Preventing bank errors begins with proactive account management. Set up transaction alerts to flag unusual activity, and reconcile your accounts monthly against bank statements. Opt for paperless statements to reduce manual entry errors, and maintain a low credit utilization ratio to buffer against reporting mistakes. If you use multiple banks, centralize your financial tracking with tools like Mint or Personal Capital to spot inconsistencies across accounts. While banks are responsible for accuracy, taking ownership of your financial data minimizes the risk of errors slipping through the cracks.

Bank Draft vs. Overdraft: Understanding Key Differences and Uses

You may want to see also

Frequently asked questions

No, your FICO score is not dependent on the bank you use. It is calculated based on information in your credit reports from the three major credit bureaus (Equifax, Experian, and TransUnion), not by individual banks.

Yes, different banks may use different versions of the FICO scoring model or pull data from different credit bureaus, which can result in slight variations in your FICO score. However, the core factors influencing your score remain consistent.

No, your bank account activity (like deposits, withdrawals, or balances) does not directly impact your FICO score. FICO scores are based on credit-related information, such as payment history, credit utilization, and length of credit history, not banking behavior.