Online banking and traditional, in-person banking serve the same fundamental purpose—managing finances—but they differ significantly in their methods and user experience. Online banking leverages digital platforms, allowing customers to access accounts, transfer funds, pay bills, and monitor transactions from anywhere with internet connectivity, offering convenience and 24/7 accessibility. In contrast, traditional banking relies on physical branches, face-to-face interactions, and paper-based processes, which can provide a more personalized touch but often require adherence to specific operating hours and physical presence. While both systems have their advantages, online banking appeals to tech-savvy users seeking efficiency, while traditional banking remains preferred by those valuing human interaction and tangible processes. The choice between the two ultimately depends on individual preferences, lifestyle, and comfort with technology.

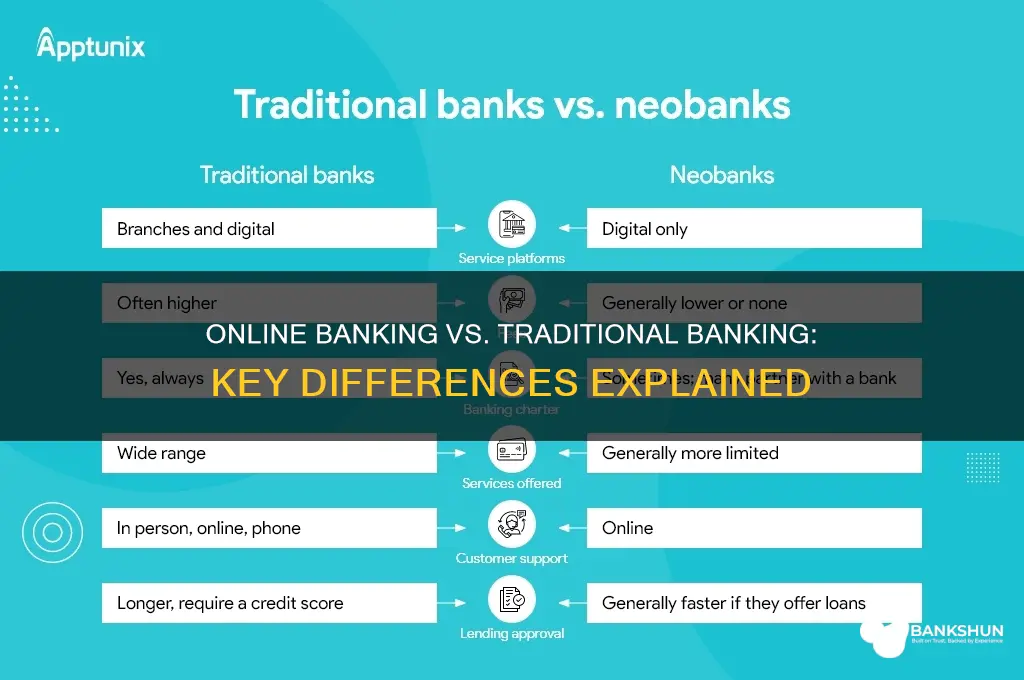

| Characteristics | Values |

|---|---|

| Accessibility | Online banking is accessible 24/7 via internet-connected devices, while traditional banking operates within branch hours. |

| Transaction Speed | Online banking offers instant or near-instant transactions; traditional banking may involve delays due to manual processing. |

| Physical Presence | Traditional banking requires visiting a physical branch; online banking does not. |

| Fees | Online banking often has lower or no fees for basic services; traditional banking may charge higher fees for certain transactions. |

| Security | Both use encryption, but online banking relies on digital security measures (e.g., two-factor authentication), while traditional banking uses physical security. |

| Personal Interaction | Traditional banking offers face-to-face interaction with bank representatives; online banking lacks this. |

| Account Management | Online banking allows real-time account monitoring and management; traditional banking may require waiting for statements or branch visits. |

| Geographical Limitations | Online banking is accessible globally; traditional banking is limited to branch locations. |

| Paperwork | Online banking minimizes paperwork with digital documentation; traditional banking often requires physical forms. |

| Service Range | Both offer similar services (e.g., deposits, loans), but online banking may have limited complex services like wealth management. |

| Technology Dependence | Online banking relies on internet connectivity and devices; traditional banking does not. |

| Environmental Impact | Online banking is more eco-friendly due to reduced paper usage; traditional banking generates more physical waste. |

| Customer Support | Traditional banking offers in-person support; online banking relies on phone, chat, or email support. |

| Fraud Risk | Online banking faces higher risks of phishing and cyberattacks; traditional banking faces risks like check fraud. |

| Cost Efficiency | Online banking is generally more cost-effective for banks and customers due to reduced overhead. |

| Customization | Online banking often provides personalized financial tools and insights; traditional banking may offer tailored advice in person. |

Explore related products

What You'll Learn

- User Interface Differences: Online banking uses digital platforms, while normal banking relies on physical branches

- Accessibility and Convenience: Online banking is 24/7; normal banking has limited branch hours

- Security Measures: Online banking uses encryption; normal banking relies on physical safeguards

- Transaction Speed: Online transactions are instant; normal banking may take longer

- Personal Interaction: Normal banking offers face-to-face service; online banking is self-service

![]()

User Interface Differences: Online banking uses digital platforms, while normal banking relies on physical branches

Online banking and traditional banking diverge sharply in their user interfaces, reflecting their distinct operational foundations. Digital platforms for online banking prioritize accessibility and efficiency, offering 24/7 access via smartphones, tablets, or computers. Users navigate through intuitive dashboards, where transactions, account summaries, and financial tools are just a few clicks away. In contrast, normal banking relies on physical branches, where interactions occur face-to-face with tellers or through ATMs. This tangible environment provides a structured, albeit time-bound, experience, often requiring adherence to branch hours and physical queues.

Consider the process of transferring funds. In online banking, users initiate transfers by entering recipient details and amounts directly into a secure app or website, with real-time confirmations and instant processing. Traditional banking, however, demands a visit to a branch, where a teller manually processes the request, or the use of an ATM, which may have limitations on transaction types and amounts. The digital interface streamlines tasks, reducing the need for physical presence and paperwork, while the physical branch offers a human touch that some users find reassuring.

The design of these interfaces also caters to different user preferences. Online banking platforms often incorporate personalization features, such as customizable alerts, budgeting tools, and transaction histories, empowering users to manage finances proactively. Physical branches, on the other hand, rely on standardized forms and procedures, which can feel rigid but provide clarity for those unfamiliar with digital systems. For instance, a senior citizen might prefer the familiarity of filling out a deposit slip at a branch, while a tech-savvy millennial may favor the convenience of mobile banking apps.

Security measures further highlight the interface differences. Online banking employs encryption, two-factor authentication, and biometric verification to protect user data, though it remains vulnerable to cyber threats like phishing. Traditional banking safeguards include locked safes, surveillance cameras, and in-person identity verification, which mitigate risks like fraud but cannot prevent physical theft or loss. Users must weigh these trade-offs, choosing the interface that aligns best with their comfort level and lifestyle.

Ultimately, the choice between online and traditional banking hinges on the user’s priorities. Digital platforms excel in convenience and speed, ideal for those seeking efficiency and flexibility. Physical branches offer a tactile, human-centric experience, suited for complex transactions or individuals who value face-to-face interaction. Understanding these interface differences allows users to leverage the strengths of each system, whether by adopting online banking for daily tasks or visiting branches for specialized needs.

Transitioning from Law to Banking: A Strategic Career Shift Guide

You may want to see also

Explore related products

$25.16 $42.99

$23.31 $29.99

![]()

Accessibility and Convenience: Online banking is 24/7; normal banking has limited branch hours

Online banking operates on your schedule, not the bank's. Need to transfer funds at 2 a.m.? Check your balance during a lunch break? Pay a bill while waiting for the bus? Online banking’s 24/7 accessibility eliminates the constraints of traditional branch hours, which typically run from 9 a.m. to 5 p.m., Monday through Friday, with limited weekend availability. This round-the-clock service is particularly beneficial for those with non-traditional work hours, frequent travelers, or anyone who values flexibility in managing their finances.

Consider the practical implications: a freelancer invoicing clients in different time zones can send payments instantly, regardless of the hour. A parent juggling work and childcare can handle banking tasks during late-night quiet hours. Even urgent needs, like replacing a lost card or disputing a transaction, can be addressed immediately without waiting for the next business day. This level of convenience isn’t just about saving time—it’s about reducing stress and providing peace of mind.

However, this convenience comes with a caveat. While online banking is always available, it may lack the personal touch of in-branch interactions. Complex issues, such as applying for a mortgage or resolving a dispute, might still require a visit to a physical branch or a phone call during business hours. Additionally, older adults or those less tech-savvy may find the digital interface challenging, highlighting the importance of maintaining both options.

To maximize the benefits of online banking’s 24/7 accessibility, adopt a few practical habits. First, familiarize yourself with the platform’s features—most banks offer tutorials or customer support to guide you. Second, enable notifications for account activity to stay informed in real time. Finally, keep a list of emergency contacts (e.g., customer service numbers) handy for situations that require immediate attention outside of branch hours. By leveraging these tools, you can fully embrace the convenience of online banking while mitigating potential drawbacks.

In conclusion, the 24/7 nature of online banking represents a significant shift from the limited hours of traditional banking, offering unparalleled flexibility and accessibility. While it may not replace all in-branch services, its convenience makes it an indispensable tool for modern financial management. By understanding its strengths and limitations, you can tailor your banking habits to suit your lifestyle seamlessly.

Securely Storing Documents in Banks: Essential Tips for Safe Preservation

You may want to see also

Explore related products

![]()

Security Measures: Online banking uses encryption; normal banking relies on physical safeguards

Online banking and traditional banking differ fundamentally in how they protect your assets and information. While both aim for security, their methods reflect their distinct environments. Online banking, operating in the digital realm, relies heavily on encryption—a complex process that scrambles data into unreadable formats during transmission. This ensures that even if intercepted, your account details remain indecipherable to unauthorized parties. Normal banking, on the other hand, leans on physical safeguards like locked vaults, security personnel, and surveillance systems to deter theft and fraud. These tangible measures create a secure environment for cash, documents, and other physical assets.

Consider the process of transferring funds. In online banking, encryption protocols like SSL/TLS (Secure Sockets Layer/Transport Layer Security) act as digital locks, securing the connection between your device and the bank’s server. For instance, when you log in to your account, a 256-bit encryption key—akin to a combination lock with 2²⁵⁶ possible combinations—protects your data. In contrast, a traditional bank transfer involves physical checks, signatures, and secure storage of documents in fireproof safes. While both methods are effective, the digital approach prioritizes invisibility and complexity, whereas the physical approach emphasizes visibility and robustness.

From a practical standpoint, online banking’s encryption is not foolproof. Users must play an active role in maintaining security by using strong, unique passwords, enabling two-factor authentication (2FA), and avoiding public Wi-Fi for transactions. For example, a password manager can generate and store complex passwords, reducing the risk of breaches. Traditional banking, however, requires vigilance against physical threats like robbery or document tampering. Simple precautions, such as shredding sensitive documents and verifying the authenticity of bank personnel, can significantly enhance security.

The trade-off between these systems lies in their vulnerabilities. Online banking faces risks like phishing attacks and malware, which exploit human error rather than breaching encryption directly. Traditional banking, meanwhile, is susceptible to insider threats and physical breaches. For instance, a bank employee with access to the vault could misuse their privileges, whereas a hacker would need to bypass multiple layers of digital security. Understanding these risks allows users to tailor their behavior—whether by scrutinizing emails for phishing attempts or double-checking the identity of bank representatives.

Ultimately, the choice between online and traditional banking depends on your comfort with technology and risk tolerance. Online banking offers convenience and advanced security measures but demands digital literacy. Traditional banking provides tangible reassurance but may lack the flexibility of digital platforms. By understanding the security measures behind each, you can make informed decisions to protect your financial well-being. For instance, combining both methods—using online banking for routine transactions and traditional banking for large, sensitive operations—can offer a balanced approach to security.

Mastering the Art of Bank Heists in Jailbreak: A Strategic Guide

You may want to see also

Explore related products

![]()

Transaction Speed: Online transactions are instant; normal banking may take longer

Online banking transactions are nearly instantaneous, a stark contrast to the lag often experienced with traditional banking methods. When you transfer funds digitally, the process typically takes seconds to minutes, depending on the banks involved and the network. For instance, domestic transfers within the same bank are usually immediate, while those between different institutions might take up to a few hours, though still significantly faster than traditional methods. This speed is due to automated systems and digital networks that process data in real-time, eliminating manual intervention and physical paperwork.

Consider a scenario where you need to pay a bill urgently. With online banking, you can log in, initiate the payment, and receive confirmation within moments, ensuring the recipient gets the funds promptly. In contrast, writing a check or visiting a bank branch for a manual transfer can delay the process by days. Checks, for example, often take 2–3 business days to clear, and branch transactions are limited by operating hours and processing times. This delay can be critical in time-sensitive situations, such as avoiding late fees or ensuring a payment is processed before a deadline.

The speed of online transactions also extends to international transfers, though with some caveats. Services like SWIFT or modern fintech platforms (e.g., TransferWise, PayPal) can complete cross-border transactions within hours or a day, compared to traditional methods that may take 3–5 business days. However, factors like time zones, currency conversion, and intermediary banks can still introduce delays. For instance, a transfer from the U.S. to Europe might be faster than one to a developing country with less robust banking infrastructure.

To maximize transaction speed, follow these practical tips: use banks or platforms known for efficient processing, ensure your account details are accurate to avoid errors, and schedule transfers during peak banking hours (typically weekdays, 9 a.m.–5 p.m. in the recipient’s time zone). Additionally, leverage instant payment systems like Zelle or Venmo for peer-to-peer transfers, which are often immediate. For larger amounts, confirm if your bank offers real-time gross settlement (RTGS) systems, which prioritize speed over cost.

The takeaway is clear: online banking’s transaction speed offers unparalleled convenience and efficiency, making it ideal for urgent or time-sensitive financial needs. While traditional banking still has its place, particularly for complex or high-value transactions requiring human oversight, the immediacy of digital transactions is a game-changer for everyday financial management. Understanding these differences allows you to choose the right method for your specific needs, balancing speed, security, and practicality.

Locate Bank Details on a Cheque: A Step-by-Step Guide

You may want to see also

Explore related products

$135.09 $148

![]()

Personal Interaction: Normal banking offers face-to-face service; online banking is self-service

One of the most noticeable differences between normal banking and online banking lies in the nature of personal interaction. Traditional banking thrives on face-to-face service, where customers engage with tellers, loan officers, or financial advisors in a physical branch. This human connection fosters trust, allows for nuanced discussions about financial needs, and provides immediate problem-solving. For instance, a customer unsure about a mortgage option can sit down with a loan officer who can explain terms, compare rates, and tailor advice to their specific situation. This level of personalized interaction is a cornerstone of traditional banking, particularly valued by older generations or those handling complex financial matters.

In contrast, online banking operates on a self-service model, minimizing direct human interaction. Customers manage their accounts through digital platforms, performing tasks like transferring funds, paying bills, or applying for loans independently. While this approach offers convenience and speed—imagine resolving a simple issue in minutes without leaving home—it lacks the immediacy and emotional reassurance of face-to-face communication. For example, a customer confused about a transaction might need to navigate FAQs or wait for a chatbot response, which can feel impersonal or frustrating. Online banking prioritizes efficiency over empathy, making it ideal for tech-savvy users comfortable with digital tools.

However, the self-service nature of online banking isn’t entirely devoid of human touch. Many digital platforms now incorporate live chat, video calls, or AI-driven assistants to bridge the interaction gap. These features attempt to replicate the personalized advice of traditional banking while maintaining the convenience of online access. For instance, a customer can video call a financial advisor to discuss retirement planning, combining the best of both worlds. Yet, these solutions still fall short for those who prefer the tangible experience of walking into a branch and speaking with someone in person.

The choice between face-to-face service and self-service ultimately depends on individual preferences and financial complexity. For routine transactions like checking balances or depositing checks, online banking’s self-service model is undeniably efficient. However, for significant decisions like taking out a loan or planning for retirement, the human insight provided by traditional banking remains invaluable. Practical tip: Assess your financial needs and comfort with technology before deciding which banking method suits you best. If you value personal connections and tailored advice, traditional banking may be your go-to. If convenience and autonomy are priorities, online banking is the way to go.

Quick Pay with TCF Bank: Simplify Your Transactions Effortlessly

You may want to see also

Frequently asked questions

Online banking offers many of the same services as traditional banking, such as checking balances, transferring funds, and paying bills, but it is accessed digitally through websites or mobile apps instead of physical branches.

Online banking uses advanced encryption and security measures to protect transactions, but it also requires users to take precautions like using strong passwords and secure networks. Both methods have their own security considerations.

Online banking typically does not allow cash deposits directly. For cash transactions, you would still need to visit a physical bank branch or use an ATM.

Yes, one of the key differences is that online banking is accessible 24/7, whereas traditional banking is limited to branch operating hours.

Fees can vary, but online banking often has lower or no fees for certain services, such as account maintenance or transfers, compared to traditional banking, which may charge for similar services.