The question of whether the operating margin of banks is always negative is a nuanced one, as it depends on various factors such as economic conditions, bank size, business model, and operational efficiency. Operating margin, calculated as operating income divided by total revenue, reflects a bank's ability to manage costs relative to its income. While banks often face high operational costs due to regulatory compliance, technology investments, and staffing, many successfully maintain positive operating margins by leveraging economies of scale, diversifying revenue streams, and optimizing expenses. However, during economic downturns or periods of financial stress, banks may experience negative operating margins due to increased loan defaults, higher provisioning, and reduced interest income. Therefore, while not always negative, bank operating margins are highly sensitive to external and internal factors, making their performance context-dependent.

Explore related products

What You'll Learn

![]()

Factors Influencing Bank Operating Margins

Bank operating margins are not always negative, but they are subject to a complex interplay of factors that can push them into the red. One critical influence is the interest rate environment. When central banks lower rates, the spread between what banks earn on loans and pay on deposits narrows, squeezing margins. For instance, during the post-2008 era of near-zero rates, many European banks struggled with negative operating margins due to this compression. Conversely, rising rates can expand margins, but only if banks can reprice loans faster than deposits, a dynamic heavily influenced by market competition and customer behavior.

Another key factor is operating efficiency, measured by the cost-to-income ratio. Banks with bloated cost structures—excessive branch networks, outdated technology, or overstaffing—face higher expenses that erode margins. Digital-first banks like Revolut or Nubank demonstrate how lean operations can sustain healthier margins, even in low-rate environments. However, traditional banks often face legacy costs, making efficiency gains a slow and painful process. A 10% reduction in non-interest expenses, for example, can boost margins by 2-3 percentage points, but achieving this requires strategic discipline and investment in automation.

Asset quality also plays a pivotal role. High levels of non-performing loans (NPLs) force banks to set aside provisions, directly hitting profitability. During economic downturns, such as the 2020 pandemic, banks with exposure to vulnerable sectors (e.g., hospitality, retail) saw margins plummet as defaults spiked. Conversely, banks with robust risk management frameworks and diversified loan portfolios tend to weather such storms better. For instance, banks in Canada, with their conservative lending practices, maintained positive margins even during the 2008 crisis, while many U.S. peers did not.

Lastly, regulatory requirements impose both direct and indirect pressures on margins. Higher capital adequacy ratios, mandated post-2008, limit the amount of risk banks can take, capping potential returns. Similarly, compliance costs associated with anti-money laundering (AML) and cybersecurity regulations add to operational expenses. Banks in highly regulated markets, like the EU, often report thinner margins compared to peers in more lenient jurisdictions. However, these regulations also reduce systemic risk, potentially lowering the cost of future crises.

In conclusion, while bank operating margins are not inherently negative, they are highly sensitive to external and internal forces. Navigating these requires a delicate balance: adapting to rate shifts, slashing inefficiencies, managing credit risk, and complying with regulations. Banks that master this balance can sustain positive margins even in challenging environments, while those that falter risk slipping into the red.

Step-by-Step Guide to Activating SBH Internet Banking Easily

You may want to see also

Explore related products

$41.99 $55.99

![]()

Impact of Interest Rates on Margins

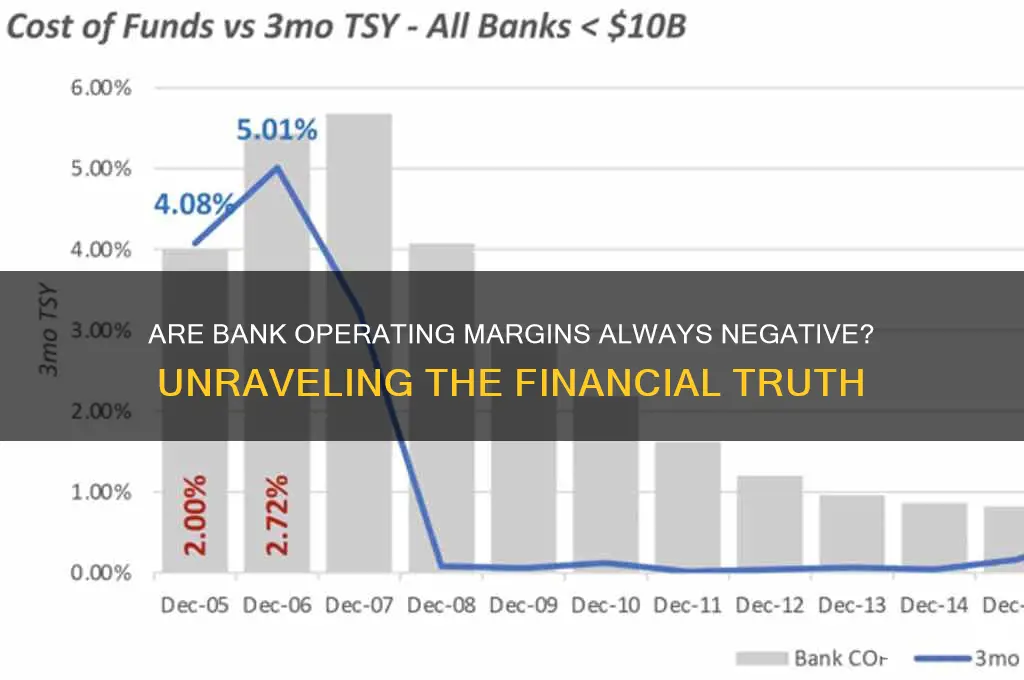

Interest rates wield significant influence over bank operating margins, often determining whether they sink into negative territory or thrive. When central banks raise rates, banks typically benefit from a steeper yield curve, earning more on loans than they pay on deposits. This widens the net interest margin (NIM), the primary driver of bank profitability. For instance, during the 2022 rate hikes, U.S. banks saw NIMs expand by an average of 20 basis points, boosting operating margins. Conversely, a low-rate environment compresses this spread, as seen in the Eurozone post-2008, where prolonged low rates pushed many banks’ margins below 1%, with some even turning negative.

However, the relationship isn’t linear. While higher rates improve NIMs, they also increase borrowing costs for customers, potentially leading to higher loan defaults. Banks must balance this trade-off, as rising defaults can erode non-interest income and increase provisioning costs, offsetting NIM gains. For example, during the 2008 financial crisis, U.S. banks faced a 30% surge in non-performing loans despite higher rates, dragging operating margins down. Thus, the impact of interest rates on margins depends on the broader economic context and a bank’s risk management practices.

To navigate this dynamic, banks employ hedging strategies, such as interest rate swaps or caps, to protect margins from rate volatility. For instance, a bank with a high proportion of fixed-rate loans might use swaps to convert them into floating-rate assets, aligning with rising rate environments. Additionally, diversifying revenue streams—such as expanding fee-based services or investing in digital banking—can reduce reliance on NIMs. A case in point is JPMorgan Chase, which offset NIM compression during the 2010s by growing its asset management and investment banking divisions, maintaining healthy operating margins.

Practical steps for banks include stress-testing portfolios under various rate scenarios, optimizing deposit pricing to minimize funding costs, and leveraging technology to reduce operational expenses. For instance, a regional bank might introduce tiered deposit rates to attract low-cost funding while offering competitive loan rates to borrowers. Similarly, adopting AI-driven credit scoring models can improve loan quality, reducing default risks associated with higher rates. By proactively managing these factors, banks can mitigate the negative impact of interest rate fluctuations on margins.

In conclusion, while interest rates are a critical determinant of bank operating margins, their effect is nuanced and contingent on multiple variables. Banks that anticipate rate shifts, manage risk effectively, and diversify revenue sources are better positioned to maintain positive margins, even in challenging environments. As the global economy continues to evolve, understanding this relationship is essential for both bankers and investors alike.

Enroll in Zelle with Huntington Bank: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Role of Non-Interest Income in Banks

Banks often grapple with the challenge of maintaining positive operating margins, especially in low-interest-rate environments. Non-interest income emerges as a critical lever in this context, serving as a buffer against the compression of net interest margins. Unlike interest income, which is directly tied to lending and deposit rates, non-interest income derives from fees, commissions, trading activities, and other services. This diversification is not merely a supplementary strategy but a necessity for banks to sustain profitability when traditional revenue streams falter.

Consider the case of JPMorgan Chase, which reported $52.6 billion in non-interest revenue in 2022, accounting for nearly 40% of its total revenue. This included income from investment banking fees, asset management, and credit card fees. Such examples underscore how non-interest income acts as a stabilizing force, particularly during periods of economic uncertainty or when central banks adopt accommodative monetary policies that squeeze lending margins. For smaller banks, the proportion of non-interest income may be lower, but its role remains pivotal in offsetting operational costs and regulatory expenses.

However, reliance on non-interest income is not without risks. Banks must carefully balance the pursuit of fee-based revenues with customer satisfaction and regulatory scrutiny. Excessive fees can lead to reputational damage and customer attrition, as evidenced by the backlash against overdraft charges in the U.S. market. Moreover, volatile income sources like trading revenues can introduce unpredictability into earnings, making it imperative for banks to adopt a diversified approach within their non-interest income portfolio.

To optimize non-interest income, banks should focus on three strategic pillars: product innovation, customer segmentation, and digital transformation. For instance, introducing tailored wealth management services for high-net-worth individuals can unlock fee-based revenues while enhancing customer loyalty. Similarly, leveraging data analytics to identify cross-selling opportunities—such as offering credit card rewards programs to mortgage customers—can maximize fee income without alienating clients. Digital platforms, meanwhile, reduce the cost of service delivery, enabling banks to offer competitive pricing while maintaining healthy margins.

In conclusion, non-interest income is not just a supplementary revenue stream but a strategic imperative for banks navigating the complexities of modern finance. By diversifying income sources, managing risks, and embracing innovation, banks can transform non-interest income from a buffer into a driver of sustainable profitability. As interest rates fluctuate and economic landscapes shift, this adaptability will distinguish resilient banks from those that falter under pressure.

Enable Screenshot Functionality Securely in Your Banking App: A Guide

You may want to see also

Explore related products

![]()

Effect of Operational Costs on Margins

Operational costs are the silent architects of a bank's profitability, often determining whether its operating margin sinks into the red or stays afloat. These costs, encompassing everything from employee salaries to technology infrastructure, directly erode the revenue generated from interest and fees. For instance, a regional bank with a 3% net interest margin might see its operating margin plummet to -1% if operational costs consume 4% of its revenue. This inverse relationship underscores why banks obsessively monitor and manage expenses, as even a slight uptick in costs can tip the scales toward negativity.

Consider the case of a mid-sized bank that invested heavily in digital transformation to compete with fintech disruptors. While the initiative boosted customer acquisition, it also inflated operational costs by 15% year-over-year. Without a commensurate increase in revenue, the bank’s operating margin dipped into negative territory. This example illustrates a critical trade-off: innovation can drive growth but must be balanced against cost discipline. Banks must meticulously assess the ROI of such investments, ensuring they don’t outpace revenue growth.

To mitigate the impact of operational costs, banks employ strategies like process automation and branch consolidation. Automation, for instance, can reduce manual labor costs by up to 30%, freeing resources for higher-margin activities. Similarly, closing underperforming branches can slash real estate and staffing expenses. However, these measures aren’t without risks. Over-reliance on automation may alienate customers, while branch closures can erode local market presence. The key lies in strategic implementation—identifying areas where cost-cutting won’t compromise long-term value.

A comparative analysis of global banks reveals that those with the highest operating margins often operate in markets with lower regulatory compliance costs. For example, banks in Scandinavia, known for their streamlined regulatory environments, consistently report operating margins above 30%. In contrast, banks in highly regulated markets like the U.S. and Europe often struggle to maintain margins above 10%. This disparity highlights the external factors that amplify the effect of operational costs, suggesting that banks in stringent regulatory regimes must be even more vigilant in cost management.

In conclusion, operational costs are not merely an expense line item but a critical determinant of a bank’s financial health. By understanding their dynamics and implementing targeted strategies, banks can navigate the fine line between investment and efficiency. The goal isn’t to eliminate costs but to optimize them, ensuring they align with revenue growth and strategic objectives. After all, in the banking sector, the difference between a positive and negative operating margin often hinges on how well a bank manages its operational footprint.

How to Easily Generate MMID for Yes Bank Transactions

You may want to see also

Explore related products

![]()

Comparison of Global Bank Margins

Operating margins in the banking sector are not universally negative, but they vary significantly across regions, bank types, and economic cycles. A comparison of global bank margins reveals distinct trends influenced by regulatory environments, market competition, and operational efficiencies. For instance, North American banks, such as JPMorgan Chase and Bank of America, consistently report higher operating margins (often above 30%) due to their diversified revenue streams and advanced cost management practices. In contrast, European banks like Deutsche Bank and HSBC often struggle with lower margins (around 20-25%) due to stricter regulations, negative interest rates, and fragmented markets. Emerging market banks, such as ICBC in China, exhibit margins closer to 35-40%, driven by rapid economic growth and higher net interest income.

Analyzing these disparities highlights the role of macroeconomic factors. In regions with stable economies and favorable monetary policies, banks tend to achieve healthier margins. For example, the U.S. Federal Reserve’s rate hikes in recent years have boosted net interest margins for American banks, while the European Central Bank’s prolonged low-rate environment has compressed margins for eurozone banks. Additionally, digital transformation plays a pivotal role. Banks that invest heavily in technology, like Canada’s Royal Bank, achieve cost efficiencies that elevate their margins compared to peers reliant on traditional brick-and-mortar models.

A comparative study of global bank margins also underscores the impact of business models. Universal banks, which combine retail and investment banking, often outperform specialized banks due to their ability to cross-sell products and diversify income sources. For instance, UBS in Switzerland leverages its wealth management division to offset lower margins in retail banking. Conversely, regional banks in Asia and Africa, despite operating in high-growth markets, may face margin pressures due to limited scale and higher operational costs.

To benchmark and improve operating margins, banks should adopt a three-pronged strategy. First, optimize cost structures through automation and outsourcing non-core functions. Second, diversify revenue streams by expanding into fee-based services like asset management or insurance. Third, leverage data analytics to enhance customer segmentation and pricing strategies. For example, BBVA in Spain has successfully reduced costs by 20% through digital transformation while increasing fee income by 15% through targeted product offerings.

In conclusion, the comparison of global bank margins reveals that while not always negative, they are highly sensitive to regional dynamics, regulatory frameworks, and strategic choices. Banks aiming to strengthen their margins must adapt to local conditions while embracing innovation and diversification. By studying these global trends, financial institutions can identify actionable insights to enhance profitability in an increasingly competitive landscape.

HSBC vs. Other Banks: Unique Features and Global Banking Advantages

You may want to see also

Frequently asked questions

No, the operating margin of banks is not always negative. It can vary depending on factors like revenue growth, cost management, and economic conditions. Banks typically aim for positive operating margins to ensure profitability.

A bank's operating margin may be negative due to high operating expenses, low interest income, significant loan losses, or economic downturns that reduce revenue while costs remain elevated.

A bank with a negative operating margin may face financial challenges, but its overall stability depends on other factors like capital reserves, asset quality, and liquidity. Temporary negative margins do not always indicate long-term instability.