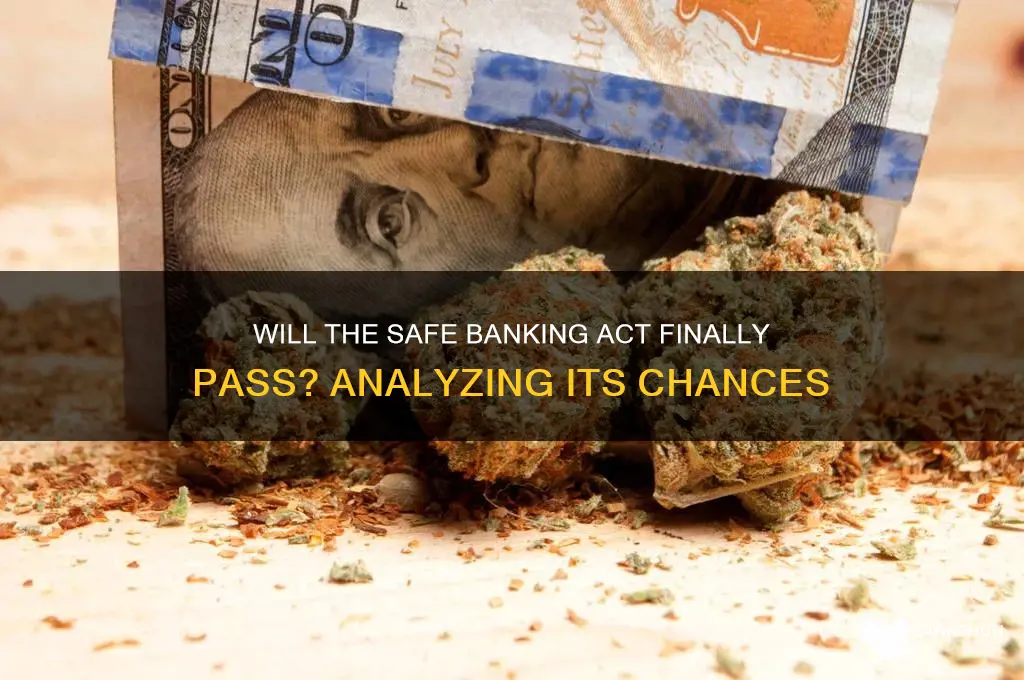

The Safe Banking Act, a bipartisan bill aimed at providing legal cannabis businesses access to traditional banking services, has been a topic of significant debate and interest in recent years. Despite widespread support across party lines and the growing legalization of cannabis at the state level, the bill has faced repeated hurdles in Congress, particularly in the Senate. Advocates argue that it would enhance public safety, reduce cash-related crimes, and legitimize a rapidly expanding industry, while opponents raise concerns about federal cannabis policy and the bill’s potential implications. As of now, its passage remains uncertain, with its fate hinging on broader legislative priorities, political dynamics, and ongoing negotiations. Whether the Safe Banking Act will finally pass remains a critical question for the cannabis industry, lawmakers, and stakeholders alike.

| Characteristics | Values |

|---|---|

| Current Status | The SAFE Banking Act has passed the House multiple times but remains stalled in the Senate as of 2023. |

| Key Objective | To provide legal access to banking services for cannabis businesses in states where it is legal. |

| Bipartisan Support | Yes, the bill has significant bipartisan support in the House. |

| Senate Obstacles | Opposition from key senators, including Senate Majority Leader Chuck Schumer, who prefers comprehensive cannabis reform. |

| Recent Developments | Included in the 2024 National Defense Authorization Act (NDAA) but later removed during negotiations. |

| Public Support | High, with strong backing from the cannabis industry, banking sector, and state governments. |

| Prospects for Passage | Uncertain, as it depends on Senate prioritization and potential inclusion in broader legislation. |

| Alternative Proposals | Comprehensive cannabis reform bills (e.g., CAOA) are being pushed as alternatives to the SAFE Act. |

| Industry Impact | If passed, would reduce reliance on cash transactions and improve safety and financial transparency. |

| Last House Passage | Passed in the House in April 2023 with a 321-101 vote. |

Explore related products

What You'll Learn

- Bipartisan Support: Cross-party backing increases chances of the Safe Banking Act passing in Congress

- State vs. Federal Law: Conflict between state and federal cannabis laws complicates Act’s progress

- Senate Hurdles: Potential roadblocks in the Senate may delay or block the Act’s approval

- Industry Impact: Passage would provide cannabis businesses access to traditional banking services, reducing risks

- Public Opinion: Growing public support for cannabis legalization may influence lawmakers to pass the Act

![]()

Bipartisan Support: Cross-party backing increases chances of the Safe Banking Act passing in Congress

The Safe Banking Act, a bill aimed at providing legal cannabis businesses access to banking services, has long been a topic of debate in Congress. One of the most significant factors influencing its potential passage is the growing bipartisan support it has garnered. This cross-party backing is not just a symbolic gesture but a practical necessity, as it increases the bill’s chances of overcoming partisan gridlock and securing the necessary votes in both the House and Senate. Historically, legislation with bipartisan support is more likely to pass, as it demonstrates a shared commitment to addressing a pressing issue, in this case, the financial vulnerabilities faced by legal cannabis enterprises.

Analyzing the dynamics of this support reveals a strategic alignment of interests. Democrats have largely championed the bill as a matter of economic justice and public safety, arguing that allowing cannabis businesses to access banking services reduces the risk of crime associated with cash-only operations. Republicans, on the other hand, have increasingly come on board due to the bill’s potential to stimulate local economies and create jobs in states where cannabis is legal. This convergence of priorities, though rooted in different ideological frameworks, has created a rare opportunity for collaboration. For instance, in 2019, the House passed the Safe Banking Act with a resounding 321-103 vote, showcasing a broad coalition of supporters from both sides of the aisle.

However, bipartisan support alone is not a guarantee of passage. The bill still faces hurdles, particularly in the Senate, where procedural rules and competing priorities can stall progress. To maximize its chances, advocates must focus on two key strategies. First, they should emphasize the bill’s non-controversial nature by framing it as a public safety and economic issue rather than a debate on cannabis legalization itself. Second, they should leverage the success stories of states like Colorado and California, where legal cannabis industries have thrived despite banking challenges, to illustrate the potential benefits of federal action. Practical tips for supporters include contacting their senators, highlighting local economic impacts, and sharing data on reduced crime rates in states with legal cannabis banking.

A comparative look at similar bipartisan efforts provides further insight. The First Step Act, a criminal justice reform bill, passed in 2018 with strong bipartisan support by focusing on shared goals like reducing recidivism and addressing prison overcrowding. The Safe Banking Act can follow this model by emphasizing its role in addressing a practical, systemic issue rather than becoming mired in broader debates about cannabis policy. By doing so, it can appeal to lawmakers who may not support legalization but recognize the need for regulatory clarity and public safety.

In conclusion, bipartisan support is the Safe Banking Act’s strongest asset, but it must be strategically leveraged to navigate the complexities of Congress. By focusing on shared priorities, highlighting practical benefits, and learning from successful precedents, advocates can increase the bill’s chances of passage. This approach not only advances the specific goals of the Safe Banking Act but also sets a precedent for cross-party collaboration on other contentious issues, demonstrating that even in a polarized political climate, practical solutions can still prevail.

Calculating Z-Scores for Banks: A Step-by-Step Financial Analysis Guide

You may want to see also

Explore related products

![]()

State vs. Federal Law: Conflict between state and federal cannabis laws complicates Act’s progress

The clash between state and federal cannabis laws creates a legal minefield for the Secure and Fair Enforcement (SAFE) Banking Act, which aims to provide legal cannabis businesses access to traditional banking services. While 38 states have legalized cannabis in some form, it remains a Schedule I controlled substance under federal law, leaving banks caught between conflicting regulations.

This disconnect forces cannabis businesses to operate in a cash-only environment, creating safety risks, hindering tax collection, and stifling economic growth. The SAFE Banking Act seeks to address this by shielding financial institutions from federal penalties for serving state-legal cannabis businesses. However, its progress is hampered by the inherent conflict between state and federal authority.

Consider the practical implications. A Colorado dispensary, compliant with state regulations, cannot open a bank account without risking federal prosecution. This forces them to handle large sums of cash, making them targets for robbery and complicating tax payments. The SAFE Banking Act would allow this dispensary to access basic financial services, improving security and transparency. However, opponents argue that facilitating banking for cannabis businesses indirectly supports an industry still illegal under federal law, creating a moral and legal dilemma.

This conflict highlights the need for a nuanced approach. One potential solution is a federal framework that respects state autonomy while establishing clear guidelines for cannabis banking. This could involve descheduling or rescheduling cannabis, allowing states to regulate it like alcohol, and providing a legal pathway for financial institutions to serve the industry. Until then, the SAFE Banking Act remains a crucial, yet contested, step towards resolving the state-federal cannabis law conflict.

Huntington Bank Locations: A Comprehensive Guide to Their Nationwide Presence

You may want to see also

Explore related products

![]()

Senate Hurdles: Potential roadblocks in the Senate may delay or block the Act’s approval

The Senate's filibuster rule, requiring 60 votes to advance most legislation, poses a significant hurdle for the SAFE Banking Act. With the Senate currently split 50-50 between Democrats and Republicans, securing 10 Republican votes is a daunting task. This rule has historically been a major obstacle for cannabis-related legislation, as it allows a determined minority to block progress. The Act's proponents must either convince a substantial number of Republicans to support the bill or pursue a filibuster reform, which is an uphill battle in itself.

One potential roadblock is the lack of consensus among Senate Republicans. While some, like Sen. Cory Gardner (R-CO), have expressed support for cannabis banking reform, others remain staunchly opposed. Sen. Chuck Grassley (R-IA), for instance, has consistently voted against cannabis-related measures, citing concerns over increased drug use and impaired driving. To overcome this hurdle, proponents must engage in targeted lobbying efforts, highlighting the Act's potential to improve public safety, boost economic growth, and create jobs. A comprehensive educational campaign, backed by data and success stories from states with legal cannabis industries, could help sway skeptical Republicans.

Another challenge lies in the Senate's crowded legislative calendar. With pressing issues like infrastructure, climate change, and social justice competing for attention, the SAFE Banking Act may struggle to gain traction. To increase its chances of passage, advocates should emphasize the Act's bipartisan appeal and its potential to generate significant tax revenue. By framing the bill as a pragmatic solution to a pressing problem, rather than a partisan issue, proponents can attract support from moderate Democrats and Republicans alike. Additionally, tying the Act to broader economic recovery efforts could help prioritize its consideration.

A comparative analysis of past cannabis-related legislation reveals a pattern of Senate resistance. The CARERS Act, which aimed to protect state-legal medical cannabis programs, stalled in the Senate despite passing the House in 2015. Similarly, the STATES Act, which would have allowed states to determine their own cannabis policies, failed to gain traction in the Senate. These examples underscore the importance of strategic coalition-building and messaging. By learning from past failures, proponents of the SAFE Banking Act can develop a more effective strategy, focusing on building bridges with Senate Republicans and highlighting the bill's potential to address pressing concerns like public safety and economic growth.

To navigate these Senate hurdles, proponents should consider a multi-pronged approach. First, they should prioritize building relationships with key Senate Republicans, particularly those from states with established cannabis industries. Second, they should develop a targeted messaging campaign, emphasizing the Act's potential to improve public safety, create jobs, and generate tax revenue. Finally, they should explore alternative legislative vehicles, such as attaching the SAFE Banking Act to a must-pass bill like the National Defense Authorization Act. By combining these strategies, advocates can increase the likelihood of Senate approval, paving the way for a safer, more regulated cannabis banking system.

Renaming Guild Bank Tabs: A Step-by-Step Guide for Gamers

You may want to see also

Explore related products

![]()

Industry Impact: Passage would provide cannabis businesses access to traditional banking services, reducing risks

The passage of the SAFE Banking Act would fundamentally alter the operational landscape for cannabis businesses by granting them access to traditional banking services, a privilege currently denied due to federal prohibition. This shift would eliminate the need for cash-only transactions, which expose businesses to heightened risks of theft, fraud, and logistical inefficiencies. For instance, a 2022 report by the Marijuana Policy Project highlighted that 70% of cannabis dispensaries operate without bank accounts, forcing them to manage millions in cash, often stored in makeshift vaults or transported in unmarked vehicles. Such practices not only endanger employees but also create opportunities for organized crime and money laundering.

From a risk management perspective, integrating cannabis businesses into the banking system would provide them with tools like electronic payment processing, payroll services, and lines of credit, which are standard for other industries. This normalization would reduce the operational vulnerabilities that currently plague the sector. Consider the case of a Colorado dispensary that lost $50,000 in a single robbery in 2021—a scenario that could have been mitigated with access to secure banking channels. By enabling these businesses to operate within the financial mainstream, the SAFE Banking Act would not only protect assets but also enhance transparency, allowing regulators to monitor transactions and ensure compliance with state laws.

Critics argue that passing the SAFE Banking Act alone is insufficient, as it does not address broader federal cannabis legalization. However, this incremental step would still deliver immediate, tangible benefits. For example, a 2021 study by the Wharton School estimated that access to banking could reduce operational costs for cannabis businesses by up to 10%, freeing up capital for reinvestment in growth and innovation. Moreover, it would encourage more financial institutions to serve the industry, fostering competition and potentially lowering fees over time. This would be particularly beneficial for small and minority-owned businesses, which often face disproportionate barriers to entry due to limited capital.

To maximize the impact of the SAFE Banking Act, stakeholders should focus on education and collaboration. Financial institutions, for instance, could develop tailored compliance programs to navigate the complexities of serving cannabis businesses, while industry associations could provide resources to help businesses transition from cash-based operations. Policymakers, meanwhile, should consider pairing the act with measures like expunging past cannabis convictions, which would further level the playing field. By addressing these complementary issues, the industry can ensure that the benefits of banking access are widely and equitably distributed.

In conclusion, the passage of the SAFE Banking Act represents a critical step toward legitimizing and stabilizing the cannabis industry. While it does not solve all challenges, it directly addresses one of the most pressing: the lack of access to safe, reliable banking services. By reducing risks associated with cash-heavy operations, the act would not only protect businesses and their employees but also enhance the industry’s overall integrity and sustainability. As the legislative debate continues, stakeholders must remain focused on the practical, transformative potential of this measure.

Police Tactics: Swift Response Strategies to Bank Robberies Explained

You may want to see also

Explore related products

![]()

Public Opinion: Growing public support for cannabis legalization may influence lawmakers to pass the Act

Public opinion is a powerful force in shaping legislative outcomes, and the Safe Banking Act is no exception. Recent polls reveal a significant shift in attitudes toward cannabis legalization, with over 68% of Americans now supporting it. This growing acceptance isn’t just a cultural trend—it’s a political catalyst. Lawmakers, ever attuned to their constituents’ views, are increasingly likely to back the Act as a practical step toward aligning financial regulations with public sentiment. When voters demand change, representatives often follow suit, making this surge in support a critical factor in the Act’s potential passage.

Consider the practical implications of this shift. In states where cannabis is legal, businesses face a cash-only dilemma due to federal banking restrictions. This not only hampers economic growth but also poses safety risks for employees handling large sums of cash. Public support for legalization translates into pressure on lawmakers to address these issues. For instance, a 2022 survey found that 72% of voters believe cannabis businesses should have access to banking services. This isn’t just about ideology—it’s about solving real-world problems, and the Safe Banking Act offers a solution that resonates with a majority of Americans.

However, translating public opinion into legislative action isn’t automatic. Lawmakers must navigate partisan divides and competing priorities. While Democrats largely support the Act, some Republicans remain skeptical, citing concerns about federal drug laws. Here’s where public opinion becomes a strategic tool: advocates can highlight bipartisan support among voters to bridge these divides. For example, in conservative states like Oklahoma, where medical cannabis is legal, even Republican voters overwhelmingly back banking access for these businesses. This data-driven approach can sway hesitant lawmakers by demonstrating broad-based demand for the Act.

To maximize the impact of public opinion, advocates should focus on actionable steps. First, amplify grassroots campaigns that connect voters directly with their representatives. Second, leverage social media to share personal stories of how banking restrictions affect cannabis businesses and their communities. Third, collaborate with industry groups to provide lawmakers with clear, concise data on the economic benefits of passing the Act. By turning public support into organized advocacy, proponents can create an environment where lawmakers feel compelled to act.

In conclusion, the growing public support for cannabis legalization isn’t just a cultural shift—it’s a legislative lever. By understanding and harnessing this momentum, advocates can increase the likelihood of the Safe Banking Act’s passage. Lawmakers may be the ones casting votes, but it’s the voices of their constituents that will ultimately tip the scales.

Has the Bank of Spain Ever Been Robbed? Unveiling the Truth

You may want to see also

Frequently asked questions

The SAFE Banking Act (Secure and Fair Enforcement) is a proposed legislation in the United States aimed at providing safe harbor for financial institutions that provide services to cannabis-related businesses in states where cannabis is legal.

As of October 2023, the SAFE Banking Act has not yet been passed into law, but it continues to gain bipartisan support in Congress. Its passage remains uncertain and depends on legislative priorities and political negotiations.

The main obstacles include differing opinions on cannabis legalization, concerns about regulatory oversight, and the need to address broader cannabis reform issues, such as social equity and descheduling cannabis from the Controlled Substances Act.

The SAFE Banking Act would allow cannabis businesses to access traditional banking services, reducing their reliance on cash transactions, improving safety, and enabling better financial transparency and tax compliance.

Yes, the SAFE Banking Act has been included in various legislative packages, such as the National Defense Authorization Act (NDAA), but it has not yet been successfully passed as part of these larger bills. Its inclusion in future packages remains a possibility.