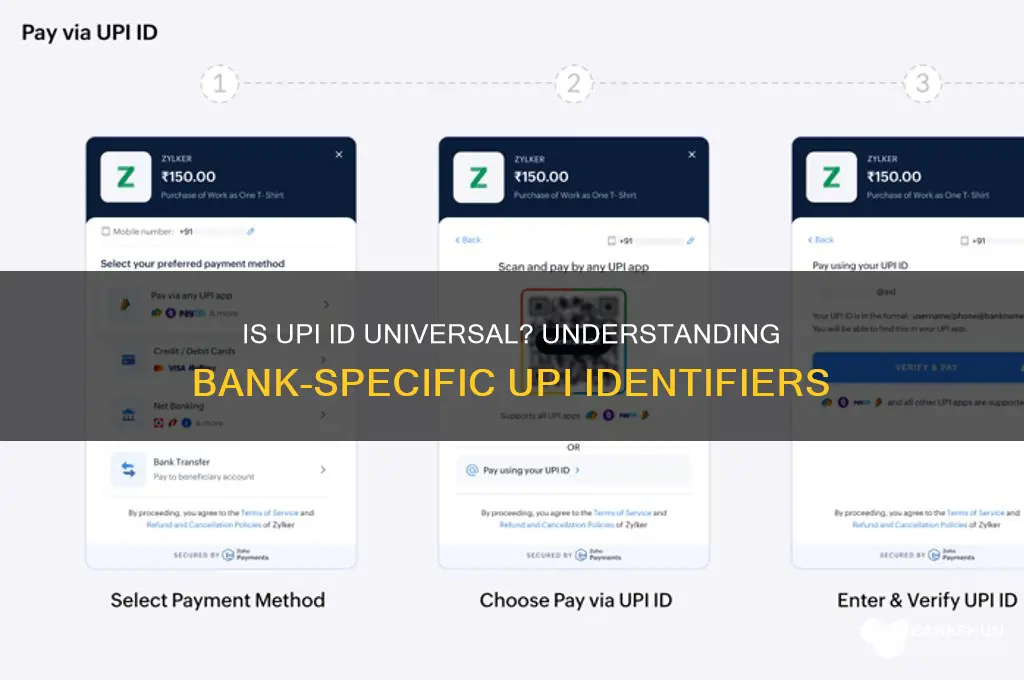

When discussing whether a UPI (Unified Payments Interface) ID is the same for all banks, it’s important to understand that a UPI ID is unique to each user and is typically linked to a specific bank account. While the format of a UPI ID (usually a combination of a virtual payment address like `username@bankname`) may vary slightly depending on the bank, the core principle is that each UPI ID is distinct and tied to an individual’s account. Therefore, a single user cannot have the same UPI ID across multiple banks, as it is designed to be a unique identifier for seamless transactions within the UPI ecosystem.

| Characteristics | Values |

|---|---|

| Is UPI ID same for all banks? | No, UPI ID is not the same for all banks. Each bank generates a unique UPI ID for its customers. |

| UPI ID Format | VPA (Virtual Payment Address), typically in the format username@bankname or mobilenumber@bankname. |

| Bank-Specific UPI IDs | Yes, UPI IDs are bank-specific and linked to the customer's account with that particular bank. |

| Interoperability | UPI IDs are interoperable across all banks and payment service providers (PSPs) in the UPI network. |

| Multiple UPI IDs | A user can have multiple UPI IDs linked to different bank accounts, even within the same bank. |

| Portability | UPI IDs are not portable across banks. Changing banks requires generating a new UPI ID. |

| Dependency on Bank | The UPI ID is dependent on the bank where the account is held and cannot be used with another bank's account. |

| Example | If a user has accounts in SBI and HDFC, they will have separate UPI IDs like username@sbi and username@hdfcbank. |

| Unified Interface | Despite different UPI IDs, the UPI interface remains unified for transactions across all banks. |

| Security | Each UPI ID is secured by a unique PIN, ensuring safety regardless of the bank. |

Explore related products

What You'll Learn

- UPI ID Structure: UPI IDs use a standard format: unique identifier@bankname, ensuring consistency across all banks

- Bank-Specific Variations: Some banks allow custom UPI IDs, but the format remains uniform for all

- Interoperability: UPI IDs work seamlessly across banks, enabling transactions without bank-specific restrictions

- VPA Uniqueness: Each UPI ID (VPA) is unique, linked to one bank account, regardless of the bank

- Cross-Bank Transactions: UPI IDs facilitate transactions between accounts of different banks using the same ID format

![]()

UPI ID Structure: UPI IDs use a standard format: unique identifier@bankname, ensuring consistency across all banks

UPI IDs are not the same across all banks, but they follow a standardized structure that ensures consistency and ease of use. This structure is designed to uniquely identify each user while clearly associating them with their respective bank. The format is straightforward: a unique identifier followed by the bank name, separated by the "@" symbol. For example, if your unique identifier is "john.doe" and your bank is HDFC, your UPI ID would be "john.doe@hdfcbank." This uniformity simplifies transactions, as users can easily recognize and verify the recipient’s bank, reducing errors and enhancing trust.

The unique identifier in a UPI ID is typically linked to the user’s mobile number or virtual payment address (VPA), which is created during the UPI registration process. This identifier is chosen by the user or auto-generated by the bank, ensuring it remains distinct within the UPI ecosystem. The "@bankname" portion is predefined and corresponds to the bank’s UPI handle, such as "ybl" for Yes Bank or "ubi" for Union Bank of India. This dual-component structure balances personalization with institutional clarity, making UPI IDs both user-friendly and institutionally verifiable.

One practical tip for users is to double-check the "@bankname" portion before initiating a transaction, as this ensures the payment is routed to the correct bank. For instance, "john.doe@icici" and "john.doe@kotak" are entirely different UPI IDs, despite the identical unique identifier. Additionally, users should avoid sharing their UPI IDs indiscriminately, as the unique identifier can sometimes be linked to personal information. Banks often provide options to create multiple VPAs for added security, allowing users to use different IDs for various purposes.

From a comparative perspective, the UPI ID structure stands out when contrasted with other payment systems. Unlike credit card numbers or IFSC codes, which are purely institutional and lack personalization, UPI IDs combine user-specific elements with bank identification. This hybrid approach not only streamlines transactions but also fosters a sense of ownership among users. Moreover, the "@bankname" format aligns with global email address conventions, making it intuitive for users familiar with digital communication tools.

In conclusion, while UPI IDs are not identical across banks, their standardized structure ensures uniformity and reliability. By adhering to the "unique identifier@bankname" format, UPI IDs strike a balance between personalization and institutional clarity, simplifying transactions and enhancing user confidence. Understanding this structure empowers users to navigate the UPI ecosystem more effectively, ensuring secure and error-free payments.

Why Breaking Up Big Banks Could Harm Financial Stability and Growth

You may want to see also

Explore related products

![]()

Bank-Specific Variations: Some banks allow custom UPI IDs, but the format remains uniform for all

While UPI IDs are universally structured as a unique handle followed by the '@' symbol and the bank's identifier (e.g., `username@ybl` for Yes Bank), banks introduce subtle variations in customization options. For instance, HDFC Bank allows users to create a custom UPI ID linked to their registered mobile number, while ICICI Bank offers the flexibility to set a preferred alias. These bank-specific variations cater to individual preferences without compromising the uniformity required for seamless transactions across the UPI network.

Consider the process of setting up a custom UPI ID. Most banks provide this option during the initial registration on their mobile banking app. For example, Axis Bank prompts users to choose a unique handle during UPI activation, ensuring it adheres to the standard format. However, not all banks offer this flexibility; some, like State Bank of India, auto-generate UPI IDs based on the account number or mobile number, leaving little room for personalization. Understanding these differences can help users navigate the setup process more effectively.

From a practical standpoint, the ability to customize UPI IDs enhances user experience by making transactions more intuitive. A personalized ID, such as `john.doe@okaxis`, is easier to remember and share compared to a generic, system-generated one. However, this customization must align with the UPI framework to ensure interoperability. For instance, the `@okaxis` suffix remains constant for Axis Bank users, ensuring the ID is recognized across all UPI-enabled platforms.

One cautionary note: while customization is convenient, it also raises security concerns. A unique UPI ID can be traced back to the user, potentially exposing personal information if shared carelessly. Banks mitigate this risk by allowing users to create multiple UPI IDs for different accounts or purposes, as seen with Kotak Mahindra Bank. Users should leverage this feature to maintain privacy, especially when transacting with unfamiliar parties.

In conclusion, bank-specific variations in UPI ID customization strike a balance between personalization and standardization. While the format remains uniform across banks, the degree of customization varies, offering users a tailored experience. By understanding these nuances, users can optimize their UPI usage, ensuring both convenience and security in their digital transactions.

Does PNC Bank Offer Free Coin Counting Services? Find Out Here

You may want to see also

Explore related products

$9.99 $13.99

![]()

Interoperability: UPI IDs work seamlessly across banks, enabling transactions without bank-specific restrictions

UPI IDs are not the same across all banks; each bank issues a unique ID tied to a user's account. However, the genius of UPI lies in its interoperability, allowing these IDs to function seamlessly across different banks. This means a UPI ID from one bank can send or receive money from any other UPI ID, regardless of the bank it’s linked to. For instance, a user with an HDFC Bank UPI ID can effortlessly transact with someone using an SBI UPI ID, without either party needing to know the other’s bank details. This eliminates the friction of traditional inter-bank transfers, which often required IFSC codes, account numbers, and lengthy processing times.

The interoperability of UPI IDs is built on a standardized framework that ensures compatibility across banks. When a user initiates a transaction, the UPI system routes the request through a centralized network, identifying the recipient’s bank and processing the transfer in real-time. This is made possible through the use of payment service providers (PSPs) and the National Payments Corporation of India (NPCI), which acts as the backbone of UPI. For example, if a user sends ₹500 from their ICICI UPI ID to a Kotak Bank UPI ID, the NPCI ensures the transaction is authenticated and settled instantly, without either party needing to switch banks or platforms.

To leverage this interoperability effectively, users should ensure their UPI IDs are correctly linked to their bank accounts and that their mobile devices are secure. Practical tips include enabling transaction limits to prevent unauthorized access and regularly updating the UPI app to benefit from the latest security features. For instance, setting a daily transaction limit of ₹10,000 can provide a safety net against fraud. Additionally, users should avoid sharing their UPI PIN or QR codes with unknown parties, as these are the primary keys to accessing their accounts.

Comparatively, traditional banking systems often restrict transactions to within the same bank or require additional steps for inter-bank transfers. UPI’s interoperability not only saves time but also reduces costs associated with such transactions. For businesses, this means faster payments and improved cash flow, while for individuals, it translates to convenience and flexibility. For example, a freelancer can receive payments from clients across different banks without needing to maintain multiple accounts or share sensitive bank details.

In conclusion, while UPI IDs are unique to each bank, their interoperability ensures a unified payment experience across the banking ecosystem. This seamless integration is a testament to UPI’s design, which prioritizes user convenience and efficiency. By understanding and utilizing this feature, users can maximize the benefits of UPI, making transactions smoother and more accessible than ever before. Whether it’s splitting a bill with friends or paying for online purchases, UPI’s interoperability ensures that bank-specific restrictions are a thing of the past.

A Beginner's Guide to Buying Bank Shares in Nigeria

You may want to see also

Explore related products

![]()

VPA Uniqueness: Each UPI ID (VPA) is unique, linked to one bank account, regardless of the bank

A UPI ID, also known as a Virtual Payment Address (VPA), is a unique identifier that simplifies digital transactions in India. One critical aspect of VPA uniqueness is its one-to-one linkage with a specific bank account, regardless of the bank. For instance, if you have a VPA like `john.doe@okaxis` and you switch from Axis Bank to HDFC Bank, you cannot retain the same VPA. Instead, you must create a new VPA linked to your HDFC Bank account, such as `john.doe@okhdfcbank`. This ensures that each VPA remains distinct and tied to a single account, preventing confusion or overlap across different banks.

From a practical standpoint, this uniqueness is both a feature and a rule to follow. When setting up a VPA, ensure it reflects your preferred handle (e.g., your name or initials) followed by the bank’s UPI handle (e.g., `@okicici` for ICICI Bank). Avoid using generic or easily guessable names, as VPAs are case-sensitive and must be unique across the UPI network. For example, `jane.smith@okaxis` and `Jane.Smith@okaxis` are treated as different VPAs. If your desired VPA is already taken, try adding numbers or variations (e.g., `jane.smith123@okaxis`).

The uniqueness of VPAs also enhances security. Since each VPA is tied to one bank account, it minimizes the risk of errors in transactions. For instance, if you send money to `raj.kumar@okaxis`, the funds will go directly to Raj Kumar’s Axis Bank account, not to another Raj Kumar’s account in a different bank. This precision is particularly useful for businesses or individuals handling multiple transactions daily. To further secure your VPA, avoid sharing it publicly and periodically review your linked accounts in your UPI app.

Comparatively, this system differs from traditional banking identifiers like account numbers and IFSC codes, which are bank-specific but not user-specific. A VPA, however, is tailored to the user, making it easier to remember and share. For example, instead of sharing a 15-digit account number and IFSC code, you can simply provide your VPA like `maria.g@oksbi`. This simplicity, combined with uniqueness, positions VPAs as a user-friendly alternative for digital payments.

In conclusion, the uniqueness of VPAs is a cornerstone of UPI’s efficiency and security. By linking each VPA to one bank account, regardless of the bank, the system ensures clarity, reduces errors, and enhances user experience. Whether you’re a first-time user or a frequent transactor, understanding and leveraging this uniqueness can streamline your digital payment journey. Always verify your VPA details before transactions and keep your UPI app updated to enjoy seamless and secure payments.

Is Santander Bank in Bastrop, Texas? A Location Guide

You may want to see also

Explore related products

![]()

Cross-Bank Transactions: UPI IDs facilitate transactions between accounts of different banks using the same ID format

UPI IDs are not the same across all banks, but their standardized format is what enables seamless cross-bank transactions. Each UPI ID is unique to an individual’s bank account and follows a consistent structure: a string of characters (e.g., `username@bankname`) linked to a specific bank’s Virtual Payment Address (VPA). This uniformity ensures that users can send or receive money without needing to know the recipient’s bank details, account number, or IFSC code. For example, a user with an SBI account (`john.doe@sbi`) can effortlessly transact with someone using HDFC (`jane.smith@hdfc`), as the UPI system recognizes and routes the transaction based on the VPA.

The key to this interoperability lies in the UPI infrastructure, which acts as a bridge between banks. When a transaction is initiated, the sender’s bank communicates with the UPI network, which then identifies the recipient’s bank via their UPI ID. This process eliminates the need for traditional inter-bank protocols, making transactions faster and more efficient. For instance, a payment from an ICICI account to a Kotak account takes seconds, whereas older methods like NEFT or RTGS could take hours or even days. This speed is particularly beneficial for small, frequent transactions, such as splitting bills or paying for online purchases.

To leverage this feature, users must first link their bank account to a UPI ID through their bank’s app or a third-party UPI app like Google Pay or PhonePe. Once set up, the same UPI ID can be used across all supported platforms, ensuring consistency. However, it’s crucial to verify the recipient’s UPI ID before initiating a transaction, as errors in the ID can lead to failed payments. Additionally, users should enable transaction alerts to monitor their account activity and ensure security.

One practical tip for maximizing the utility of UPI IDs is to create a unique, memorable ID that’s easy to share. Most banks allow users to customize their VPA during setup, so choosing a simple handle (e.g., `firstname.lastname@bankname`) reduces the risk of typos. For businesses, using a branded UPI ID (e.g., `payments@companyname`) enhances professionalism and customer trust. By understanding and optimizing the use of UPI IDs, individuals and businesses can fully harness the convenience of cross-bank transactions.

In conclusion, while UPI IDs are not identical across banks, their standardized format and the UPI network’s architecture enable frictionless transactions between accounts of different banks. This system not only simplifies payments but also democratizes access to digital banking, making it a cornerstone of India’s financial ecosystem. Whether for personal or business use, mastering the nuances of UPI IDs can significantly enhance one’s financial efficiency and security.

Sasha Banks' Role in The Mandalorian

You may want to see also

Frequently asked questions

No, UPI ID is not the same for all banks. Each UPI ID is unique to the user and is linked to a specific bank account, but the format (e.g., `mobilenumber@bankname` or `username@bankname`) may vary depending on the bank or UPI app used.

No, a UPI ID is typically linked to one bank account. However, you can create multiple UPI IDs using different bank accounts or mobile numbers if needed.

Yes, if you switch banks, your UPI ID will change because it is tied to your bank account. You will need to create a new UPI ID with the new bank.