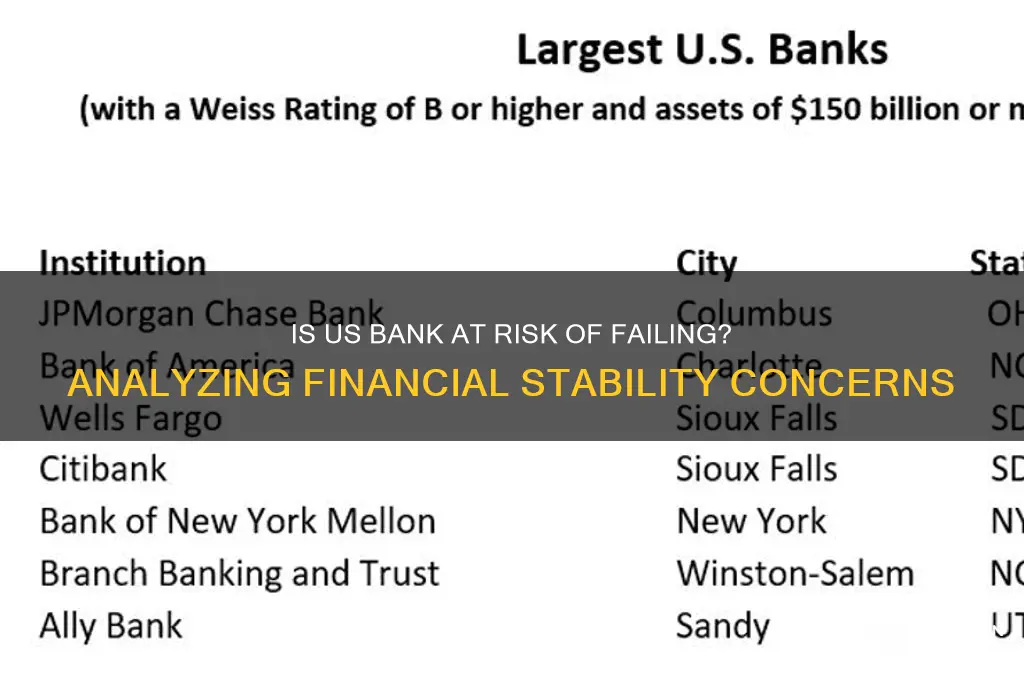

The financial stability of U.S. Bank, one of the largest banking institutions in the United States, has come under scrutiny amid broader concerns about the banking sector's resilience. Recent economic challenges, including rising interest rates, inflationary pressures, and geopolitical uncertainties, have raised questions about whether U.S. Bank is at risk of failing. While the bank has historically demonstrated strong financial performance and robust risk management practices, analysts and investors are closely monitoring its exposure to potential vulnerabilities, such as commercial real estate loans and consumer credit defaults. Regulatory oversight and the bank's capital adequacy ratios remain critical factors in assessing its ability to weather economic downturns, leaving stakeholders to weigh the institution's long-term viability in an increasingly volatile financial landscape.

Explore related products

What You'll Learn

![]()

US Bank's Financial Health Indicators

The financial health of US banks is a critical concern for investors, policymakers, and the general public alike. One key indicator to monitor is the Capital Adequacy Ratio (CAR), which measures a bank’s available capital against its risk-weighted assets. A CAR below 8% raises red flags, as it suggests the bank may struggle to absorb losses during economic downturns. For instance, during the 2008 financial crisis, several banks with CARs below this threshold faced severe liquidity issues or failed outright. Today, most US banks maintain CARs above 12%, reflecting stronger regulatory oversight post-crisis. However, regional banks with significant exposure to commercial real estate or volatile asset classes may warrant closer scrutiny.

Another vital metric is the Net Interest Margin (NIM), which reflects the difference between interest income generated and interest paid out relative to total interest-earning assets. In a rising interest rate environment, banks typically see NIM expand, boosting profitability. Conversely, a prolonged period of low or declining rates can compress NIM, straining revenue streams. For example, in 2023, some banks reported NIM contraction due to aggressive rate hikes by the Federal Reserve, prompting concerns about their ability to sustain earnings growth. Investors should track NIM trends quarterly to gauge a bank’s resilience to shifting monetary policies.

Asset quality is a third critical indicator, particularly the Non-Performing Loan (NPL) ratio. This metric measures the percentage of loans in default or close to default relative to total loans. A rising NPL ratio signals deteriorating credit quality, often a precursor to financial distress. During economic slowdowns, sectors like consumer credit and commercial real estate tend to see NPLs spike. Banks with NPL ratios above 3% may face increased provisioning requirements, eroding profitability. Analyzing sector-specific loan exposures can provide deeper insights into a bank’s vulnerability to economic shocks.

Lastly, Liquidity Coverage Ratio (LCR) is a regulatory metric that ensures banks hold sufficient high-quality liquid assets to cover 30 days of net cash outflows in a stress scenario. An LCR below 100% indicates potential liquidity risk, making the bank susceptible to runs or funding shortages. While most large US banks maintain LCRs well above the regulatory minimum, smaller institutions may struggle to meet this threshold during periods of market volatility. Monitoring LCR alongside deposit trends can help identify banks at risk of liquidity crunches.

In conclusion, assessing US banks’ financial health requires a multi-faceted approach, focusing on CAR, NIM, asset quality, and LCR. Each indicator provides unique insights into a bank’s stability, profitability, and resilience. By tracking these metrics regularly and understanding their interplay, stakeholders can better evaluate whether a bank is at risk of failing and make informed decisions accordingly.

Pacific Premier Bank Notary Services: Availability and What You Need to Know

You may want to see also

Explore related products

![]()

Regulatory Compliance and Oversight

Effective oversight by agencies like the Federal Reserve, the Office of the Comptroller of the Currency (OCC), and the Federal Deposit Insurance Corporation (FDIC) is equally vital. These regulators conduct regular examinations to ensure banks adhere to laws such as the Bank Secrecy Act and anti-money laundering (AML) rules. A 2023 FDIC report highlighted that banks with deficient compliance programs faced a 40% higher risk of financial distress within three years. This underscores the correlation between regulatory adherence and long-term viability.

However, compliance is not without challenges. Smaller banks often struggle with the cost and complexity of meeting regulatory demands, diverting resources from core operations. For example, implementing the Current Expected Credit Loss (CECL) accounting standard requires sophisticated modeling, which can strain institutions with limited budgets. This imbalance can inadvertently increase risk if banks cut corners or delay necessary upgrades.

To mitigate these risks, banks should adopt a proactive approach to compliance. This includes investing in technology to streamline reporting, training staff on evolving regulations, and fostering a culture of accountability. Boards of directors must also play an active role, ensuring management prioritizes compliance over short-term profits. For instance, banks that voluntarily conduct third-party audits of their AML programs have been shown to reduce regulatory penalties by up to 25%.

Ultimately, regulatory compliance and oversight are not mere bureaucratic hurdles but essential safeguards against bank failure. While the system is robust, its effectiveness depends on continuous adaptation to emerging risks, such as cybersecurity threats and climate-related financial risks. Banks that view compliance as a strategic advantage rather than a burden are better positioned to navigate uncertainties and maintain public trust.

How to Make a Deposit into Your US Bank Account Easily

You may want to see also

Explore related products

![]()

Market Volatility Impact on Stability

Market volatility can erode bank stability by amplifying asset price fluctuations, liquidity pressures, and risk contagion. Consider the 2023 banking crisis, where a 50% surge in 10-year Treasury yields triggered unrealized losses on bond portfolios, leading to a 30% deposit outflow at Silicon Valley Bank within 48 hours. This example illustrates how rapid market shifts can expose vulnerabilities in asset-liability management, particularly for banks holding long-duration securities funded by short-term deposits.

To mitigate volatility-driven risks, banks must adopt dynamic hedging strategies and stress-test portfolios against extreme scenarios. For instance, implementing duration gap limits—ensuring the weighted average maturity of assets doesn’t exceed liabilities by more than 12 months—can reduce interest rate sensitivity. Additionally, maintaining a liquidity coverage ratio (LCR) above the 100% regulatory minimum provides a buffer during sudden funding shocks. Firms like JPMorgan Chase have demonstrated resilience by holding 120% LCR during volatile periods, showcasing the value of conservative liquidity planning.

However, over-reliance on regulatory metrics can create false security. The 2008 crisis revealed that banks with Tier 1 capital ratios above 8% still failed due to concentrated exposures and mark-to-market losses. A more holistic approach involves diversifying revenue streams—for example, combining fixed-income trading with fee-based services—to offset volatility in any single market segment. Banks should also leverage AI-driven analytics to identify early warning signals, such as widening credit spreads or abnormal trading volumes, which often precede systemic stress.

A comparative analysis of European and U.S. banks highlights the role of market structure in stability. European banks, with higher reliance on wholesale funding, experienced a 25% greater decline in stock prices during the 2020 COVID-19 volatility spike compared to U.S. peers. This disparity underscores the importance of deposit stability, particularly retail deposits, which are less prone to rapid withdrawals. U.S. banks can enhance resilience by incentivizing long-term deposits through tiered interest rates or loyalty programs, reducing vulnerability to market-induced liquidity crises.

Ultimately, managing market volatility requires a balance between proactive risk management and adaptive strategy. Banks must treat volatility not as an anomaly but as a persistent condition, embedding flexibility into their operating models. For instance, contingency plans should include pre-negotiated credit lines and asset sale triggers when volatility indices (e.g., VIX) surpass 30. By integrating these measures, banks can transform market turbulence from a threat into a manageable challenge, safeguarding stability even in the most unpredictable environments.

Understanding Bank Transfer Fee Refunds: How Much Can You Get Back?

You may want to see also

Explore related products

$4.99 $12.99

![]()

Loan Portfolio Risk Assessment

A bank's loan portfolio is its lifeblood, but also its potential Achilles' heel. Assessing the risk embedded within this portfolio is crucial for understanding a bank's overall health and its susceptibility to failure. This involves a deep dive into the characteristics of the loans themselves, the borrowers, and the broader economic landscape.

Imagine a spectrum: on one end, a portfolio brimming with prime mortgages to high-income earners in stable industries; on the other, subprime auto loans to borrowers with shaky credit histories. The risk profile is starkly different.

Dissecting the Portfolio: Key Risk Factors

- Credit Quality: This is the cornerstone. Analyze borrower credit scores, debt-to-income ratios, and payment histories. A high concentration of loans to borrowers with poor credit significantly elevates risk.

- Collateral: Secured loans (backed by assets like homes or vehicles) offer a safety net if borrowers default. Unsecured loans, like credit cards, carry higher risk.

- Loan Type: Mortgages, auto loans, business loans – each type has inherent risks. For instance, commercial real estate loans are vulnerable to market fluctuations.

- Concentration Risk: Over-reliance on a single industry or geographic region can be dangerous. A downturn in that sector or area could trigger widespread defaults.

- Economic Sensitivity: How will the portfolio fare in a recession? Loans to cyclical industries (like construction) are more vulnerable than those to essential services.

Stress Testing: Putting the Portfolio to the Test

Think of stress testing as a financial earthquake drill. Banks simulate severe economic scenarios (recessions, interest rate hikes) to see how their loan portfolio would withstand the shock. This reveals potential cracks in the system, allowing banks to shore up reserves and adjust lending practices.

- Scenario Analysis: Model different economic downturns (mild, moderate, severe) and their impact on loan performance.

- Sensitivity Analysis: Examine how changes in interest rates, unemployment, or property values affect default rates.

Mitigating Risk: A Multi-Pronged Approach

Risk assessment isn't just about identifying problems; it's about finding solutions. Banks employ various strategies:

- Diversification: Spreading loans across different borrower types, industries, and regions reduces concentration risk.

- Conservative Underwriting: Tightening lending standards and requiring higher down payments can improve credit quality.

- Loan Loss Reserves: Setting aside funds to cover anticipated losses acts as a financial buffer.

- Hedging: Using financial instruments to offset potential losses from interest rate changes or other market movements.

The Bottom Line: A Dynamic Process

Obtaining Your Property Survey from the Bank: A Step-by-Step Guide

You may want to see also

Explore related products

![Collapse( How Societies Choose to Fail or Succeed)[COLLAPSE][Paperback]](https://m.media-amazon.com/images/I/71KdH5D8O4L._AC_UY218_.jpg)

![]()

Liquidity and Capital Adequacy Concerns

Recent market volatility has heightened scrutiny of U.S. banks' liquidity positions and capital adequacy ratios, two critical indicators of financial health. Liquidity refers to a bank's ability to meet short-term obligations without incurring unacceptable losses, while capital adequacy measures its capacity to absorb losses and maintain solvency. A bank with insufficient liquidity may struggle to honor withdrawals or settle transactions, potentially triggering a loss of confidence and a run on deposits. Similarly, inadequate capital levels leave a bank vulnerable to shocks, such as loan defaults or market downturns, which can erode its financial stability.

Consider the 2023 collapse of Silicon Valley Bank (SVB), a stark reminder of the consequences of liquidity mismanagement. SVB's heavy investment in long-term Treasury bonds left it exposed when depositors began withdrawing funds en masse, forcing the bank to sell assets at a loss to meet liquidity demands. This fire sale further eroded its capital base, ultimately leading to its failure. The episode underscores the importance of maintaining a balanced liquidity profile, with a mix of cash, short-term securities, and stable funding sources to withstand unexpected outflows.

To assess a bank's liquidity risk, regulators and investors often examine key metrics such as the liquidity coverage ratio (LCR) and net stable funding ratio (NSFR). The LCR requires banks to hold sufficient high-quality liquid assets (HQLA) to cover 30 days of net cash outflows under a stressed scenario. Similarly, the NSFR ensures that long-term assets are funded by stable liabilities, reducing reliance on volatile short-term funding. Banks with LCRs and NSFRs significantly above regulatory minimums (100% for LCR and 100% for NSFR) are generally better positioned to weather liquidity shocks.

Capital adequacy, governed by Basel III standards, is measured through the Common Equity Tier 1 (CET1) ratio, which compares a bank's core capital to its risk-weighted assets. A CET1 ratio below 7% (the regulatory minimum for most banks) signals potential vulnerability, while ratios above 10% are often viewed as robust. However, these thresholds are not one-size-fits-all; banks with higher risk profiles or exposure to volatile markets may require even greater capital buffers. For instance, regional banks with significant commercial real estate loan portfolios might need CET1 ratios closer to 12% to mitigate concentration risk.

Practical steps for banks to enhance liquidity and capital adequacy include diversifying funding sources, stress testing liquidity and capital positions under extreme scenarios, and proactively managing asset-liability mismatches. Depositors and investors, meanwhile, should scrutinize banks' financial disclosures, focusing on liquidity and capital metrics, asset quality, and risk management practices. While no bank is immune to failure, those with strong liquidity management and robust capital buffers are far better equipped to navigate turbulent times.

Mastering the Application Process for Bank Jobs in Dubai

You may want to see also

Frequently asked questions

As of the latest financial reports and regulatory assessments, US Bank (U.S. Bancorp) is considered financially stable and well-capitalized, with no immediate risk of failure.

US Bank consistently ranks among the top U.S. banks in terms of financial health, with strong capital ratios, asset quality, and profitability, positioning it as a low-risk institution.

While economic downturns can impact any bank, US Bank’s diversified business model, conservative risk management practices, and robust reserves make it resilient to such challenges.

There are no significant recent concerns or warnings from regulators or financial analysts about US Bank’s financial condition. It continues to meet or exceed regulatory requirements.