U.S. Bank, a subsidiary of U.S. Bancorp, is widely regarded as one of the largest banks in the United States, often categorized as a big bank due to its significant assets, extensive branch network, and broad range of financial services. With over $500 billion in assets and thousands of branches across the country, it ranks among the top five commercial banks in the U.S. Its size and influence are further evidenced by its membership in the Federal Reserve System and its role as a primary dealer in U.S. Treasury securities. Serving millions of customers, from individual consumers to large corporations, U.S. Bank’s scale and market presence firmly establish it as a major player in the banking industry.

Explore related products

What You'll Learn

- US Bank's Asset Size: Total assets exceed $500 billion, meeting big bank criteria

- Market Share: Ranks among top 10 US banks by deposits and customers

- Regulatory Classification: Designated as a systemically important financial institution (SIFI)

- Branch Network: Operates over 2,000 branches across the United States

- Revenue Scale: Annual revenue surpasses $20 billion, comparable to major banks

![]()

US Bank's Asset Size: Total assets exceed $500 billion, meeting big bank criteria

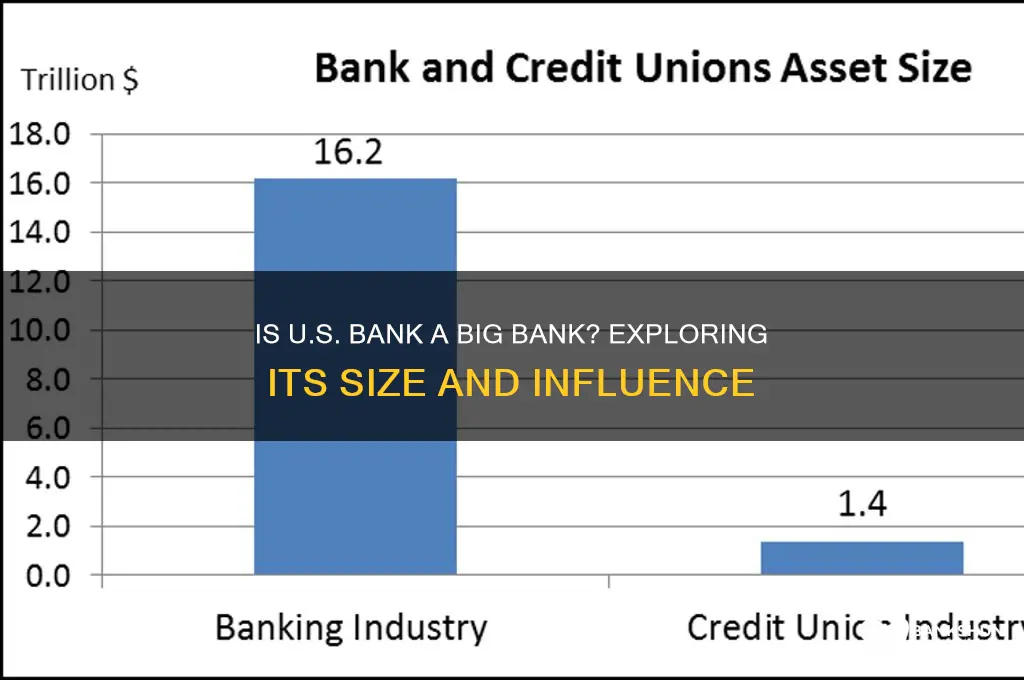

U.S. Bank's total assets exceed $500 billion, a threshold that unequivocally classifies it as a "big bank" under regulatory definitions. This figure, reported in its most recent financial disclosures, places it among the top 10 largest banks in the United States by asset size. To contextualize, this scale positions U.S. Bank alongside financial giants like JPMorgan Chase, Bank of America, and Wells Fargo, which dominate the industry with assets surpassing $2 trillion. While U.S. Bank’s asset size is smaller than these behemoths, it still meets the criteria set by the Dodd-Frank Act, which designates banks with over $50 billion in assets as systemically important financial institutions (SIFIs), and those above $500 billion as subject to enhanced regulatory scrutiny.

Analyzing U.S. Bank’s asset composition reveals a diversified portfolio that includes loans, securities, and cash reserves. Approximately 60% of its assets are tied to loans, primarily in commercial and industrial sectors, mortgages, and consumer credit. This diversification mitigates risk but also reflects its role as a full-service bank catering to both retail and corporate clients. Comparatively, smaller regional banks often have a higher concentration of assets in local markets, whereas U.S. Bank’s national footprint allows it to spread risk across broader economic regions. This asset structure not only underscores its size but also its operational complexity, a hallmark of big banks.

From a regulatory perspective, U.S. Bank’s asset size triggers specific oversight requirements. Banks exceeding $500 billion in assets must adhere to stricter capital and liquidity standards, stress testing, and resolution planning under the Federal Reserve’s Large Institution Supervision Coordinating Committee (LISCC). These measures aim to ensure financial stability and prevent systemic risk. For customers, this heightened regulation translates to greater safety but may also mean less flexibility in product offerings compared to smaller banks. For instance, U.S. Bank’s compliance with Basel III capital requirements limits its ability to engage in high-risk lending practices, prioritizing stability over aggressive growth.

Persuasively, U.S. Bank’s classification as a big bank carries both advantages and challenges. On one hand, its size enables it to offer a wide range of services, from wealth management to corporate banking, and to invest in cutting-edge technology like digital banking platforms. On the other hand, its scale invites scrutiny from regulators, activists, and the public, particularly in the aftermath of financial crises. For investors, U.S. Bank’s asset size signals stability and market influence, but it also demands vigilance regarding regulatory compliance and operational efficiency. Practical advice for stakeholders: monitor its asset growth trends, as sustained expansion could lead to further regulatory constraints, while stagnation might indicate competitive pressures.

In conclusion, U.S. Bank’s total assets exceeding $500 billion firmly establish it as a big bank, with all the implications that come with this designation. Its diversified asset portfolio, regulatory obligations, and market position highlight its role as a key player in the U.S. financial system. Whether viewed through the lens of a customer, investor, or regulator, understanding its asset size provides critical insights into its operations, risks, and opportunities. This classification is not merely a label but a defining characteristic that shapes its strategy, reputation, and impact on the broader economy.

Bank of England Meeting Frequency: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Market Share: Ranks among top 10 US banks by deposits and customers

U.S. Bank holds a significant position in the American banking landscape, consistently ranking within the top 10 U.S. banks by both deposits and customer base. As of recent data, it manages over $500 billion in deposits, placing it among financial giants like JPMorgan Chase, Bank of America, and Wells Fargo. This substantial market share is a testament to its broad reach and the trust it has cultivated among consumers and businesses alike. With more than 12 million retail customers and over 1 million business customers, U.S. Bank’s footprint spans 26 states, making it a key player in regional and national banking.

Analyzing its market share reveals a strategic focus on both retail and commercial banking. While it may not rival the sheer scale of the "Big Four" banks, U.S. Bank’s position in the top 10 underscores its ability to compete effectively in a crowded market. Its deposit base, for instance, accounts for roughly 3% of the total U.S. banking deposits, a figure that highlights its relevance in the industry. This ranking is further bolstered by its diverse product offerings, including mortgages, credit cards, and wealth management services, which cater to a wide range of customer needs.

To understand U.S. Bank’s standing, consider its comparative advantage in regional markets. Unlike some of its larger competitors, U.S. Bank has carved out a niche by focusing on Midwest and Western states, where it often ranks as the top or second-largest bank by deposits. This regional dominance allows it to maintain a strong customer base while avoiding the overexposure risks associated with national saturation. For example, in states like Minnesota, Ohio, and Wisconsin, U.S. Bank holds a market share exceeding 20%, a level of local influence that few other banks can match.

For consumers and businesses evaluating banking options, U.S. Bank’s top-10 ranking offers practical benefits. Its size ensures financial stability and access to a wide array of services, while its regional focus often translates to personalized customer service. However, it’s essential to weigh these advantages against potential drawbacks, such as fewer branch locations in certain areas compared to truly national banks. To maximize value, customers should assess their specific banking needs—whether it’s low fees, specialized lending, or digital tools—and compare U.S. Bank’s offerings to those of competitors.

In conclusion, U.S. Bank’s consistent ranking among the top 10 U.S. banks by deposits and customers solidifies its status as a major player in the industry. Its ability to balance regional strength with national relevance positions it as a viable alternative to larger institutions, particularly for those in its core markets. By understanding its market share dynamics, customers can make informed decisions about whether U.S. Bank aligns with their financial goals and preferences.

How to Add Syndicate Bank in PhonePe: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Regulatory Classification: Designated as a systemically important financial institution (SIFI)

U.S. Bank's designation as a Systemically Important Financial Institution (SIFI) by the Financial Stability Oversight Council (FSOC) places it in a regulatory category reserved for banks whose failure could pose a threat to the entire financial system. This classification, established under the Dodd-Frank Act, subjects U.S. Bank to heightened oversight and stricter capital requirements compared to smaller institutions. The criteria for SIFI designation include size, interconnectedness, and complexity, all of which U.S. Bank meets as the fifth-largest commercial bank in the United States by assets. This regulatory framework ensures that U.S. Bank maintains sufficient buffers to absorb losses during economic downturns, thereby reducing the likelihood of taxpayer-funded bailouts.

From a practical standpoint, being a SIFI means U.S. Bank must adhere to stress testing, liquidity coverage ratios, and resolution planning requirements. Stress tests, for instance, evaluate the bank's ability to withstand severe economic scenarios, such as a sharp rise in unemployment or a housing market crash. The liquidity coverage ratio mandates that U.S. Bank hold high-quality liquid assets equivalent to 100% of its net cash outflows over a 30-day stress period. Resolution planning, or "living wills," requires the bank to outline a strategy for an orderly failure without disrupting the broader economy. These measures not only safeguard U.S. Bank but also protect the financial ecosystem from systemic risks.

Critics argue that SIFI designation can stifle growth by imposing excessive compliance costs and limiting risk-taking. However, proponents counter that the benefits of financial stability outweigh these drawbacks. For customers, U.S. Bank's SIFI status offers reassurance that their deposits and investments are backed by a resilient institution. For investors, it signals a commitment to long-term sustainability, even if it means slower profit growth in the short term. This balance between stability and innovation is a hallmark of SIFIs and underscores U.S. Bank's role as a "big bank" in both size and regulatory scrutiny.

Comparatively, U.S. Bank's SIFI classification aligns it with peers like JPMorgan Chase, Bank of America, and Wells Fargo, which also face similar regulatory demands. Unlike smaller regional banks, U.S. Bank must navigate a dual regulatory environment, answering to both federal and state authorities. This complexity further cements its status as a major player in the financial sector. For policymakers, U.S. Bank's SIFI designation serves as a case study in managing systemic risk without hindering economic growth, highlighting the delicate trade-offs inherent in financial regulation.

In conclusion, U.S. Bank's SIFI designation is not merely a regulatory label but a testament to its scale, influence, and responsibility within the financial system. By adhering to stringent oversight, the bank reinforces its position as a "big bank" capable of weathering economic storms while contributing to broader financial stability. For stakeholders, understanding this classification provides insight into U.S. Bank's operational priorities and its role in safeguarding the economy. As the regulatory landscape evolves, U.S. Bank's SIFI status will remain a key indicator of its systemic importance and commitment to resilience.

NatWest and RBS: One Bank, Two Brands

You may want to see also

Explore related products

![]()

Branch Network: Operates over 2,000 branches across the United States

U.S. Bank's branch network of over 2,000 locations is a physical manifestation of its scale and ambition. This extensive footprint places it firmly within the top tier of American banks, rivaling the likes of Wells Fargo and Bank of America in terms of brick-and-mortar presence. While digital banking continues to rise, these branches serve as critical touchpoints for customers who value face-to-face interactions, complex transactions, or simply the reassurance of a physical institution.

U.S. Bank's branch density is particularly notable in the Midwest, where it dominates markets like Minnesota, Wisconsin, and Ohio. This regional stronghold allows for deeper customer relationships and a more personalized banking experience, a strategic advantage in an increasingly commoditized industry. However, the bank's branch network also extends to 28 states, providing a national reach that few regional banks can match.

Maintaining such a vast network is not without challenges. Operational costs, staffing requirements, and the need for consistent customer service across diverse markets are significant hurdles. U.S. Bank addresses these through standardized processes, technology integration, and a focus on cross-selling products within branches. For instance, a customer visiting a branch for a simple transaction might be introduced to mortgage or investment services, maximizing the value of each interaction.

The strategic placement of these branches is equally important. U.S. Bank prioritizes high-traffic areas, such as urban centers and suburban shopping districts, ensuring visibility and accessibility. This approach not only attracts walk-in customers but also reinforces the bank's brand presence in key markets. For example, a branch located in a bustling downtown area can serve as a hub for both personal and business banking, catering to a diverse clientele.

In an era where digital banking is often prioritized, U.S. Bank's commitment to its branch network signals a balanced approach. While online and mobile platforms handle routine transactions, branches remain essential for complex needs, relationship-building, and serving customers who prefer traditional banking methods. This dual strategy positions U.S. Bank as a comprehensive financial institution capable of meeting diverse customer preferences.

Ultimately, the sheer scale of U.S. Bank's branch network is a testament to its status as a big bank. It provides a tangible connection to customers, fosters trust, and enables a level of service that purely digital banks cannot replicate. By strategically managing this network, U.S. Bank leverages its physical presence to differentiate itself in a competitive market, solidifying its position among the nation's banking giants.

Does Granada Banks Accept 100 USD Bills? A Quick Guide

You may want to see also

Explore related products

![]()

Revenue Scale: Annual revenue surpasses $20 billion, comparable to major banks

U.S. Bank's annual revenue consistently surpasses $20 billion, placing it firmly within the financial league of major banks. This threshold is significant because it reflects not just size but also operational complexity, market influence, and resource capacity. For context, institutions like JPMorgan Chase and Bank of America operate at similar scales, generating revenues in the hundreds of billions. U.S. Bank’s ability to sustain this level of income signals its competitive positioning in a sector dominated by a handful of giants.

Analyzing this revenue scale reveals strategic advantages. With over $20 billion annually, U.S. Bank can invest heavily in technology, such as digital banking platforms and cybersecurity, to enhance customer experience and operational efficiency. It also enables diversification across product lines—from commercial lending to wealth management—reducing reliance on any single revenue stream. For instance, while smaller banks might allocate 5-10% of revenue to innovation, U.S. Bank’s scale allows for 15-20% investment, accelerating its adaptability in a rapidly evolving financial landscape.

However, revenue alone doesn’t define "bigness." While U.S. Bank’s income rivals major banks, its asset size ($580 billion as of recent reports) trails behind JPMorgan’s $3.7 trillion. This disparity highlights a critical distinction: revenue measures income-generating capability, while assets reflect total resources. Still, the $20 billion revenue mark is a practical benchmark for operational scale, as it correlates with capabilities like nationwide branch networks, extensive ATM systems, and robust customer support—features typically associated with big banks.

To leverage this scale effectively, U.S. Bank must balance growth with customer-centric strategies. For example, allocating 5% of revenue to community reinvestment programs can mitigate the perception of being "too big" while fostering local goodwill. Additionally, segmenting services—such as offering tailored products for small businesses or high-net-worth individuals—maximizes revenue potential without alienating niche markets.

In conclusion, U.S. Bank’s $20 billion-plus revenue is more than a financial metric; it’s a strategic asset. It positions the bank as a major player, capable of competing on innovation, scale, and service diversity. Yet, to fully embody the "big bank" label, it must also address asset size and public perception. For customers, this scale translates to reliability, advanced services, and broader accessibility—hallmarks of banking at its most impactful.

Effortlessly Import Bank Data into Quicken: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Yes, U.S. Bank is considered one of the largest banks in the United States, ranking among the top 10 by asset size.

U.S. Bank is smaller than the "Big Four" banks (JPMorgan Chase, Bank of America, Wells Fargo, and Citigroup) but is still a significant player with over $500 billion in assets.

Yes, U.S. Bank operates in all 50 states, offering a wide range of financial services, including retail banking, commercial banking, and wealth management.

Yes, U.S. Bank is the primary subsidiary of U.S. Bancorp, a publicly traded financial services holding company, further solidifying its status as a major bank.