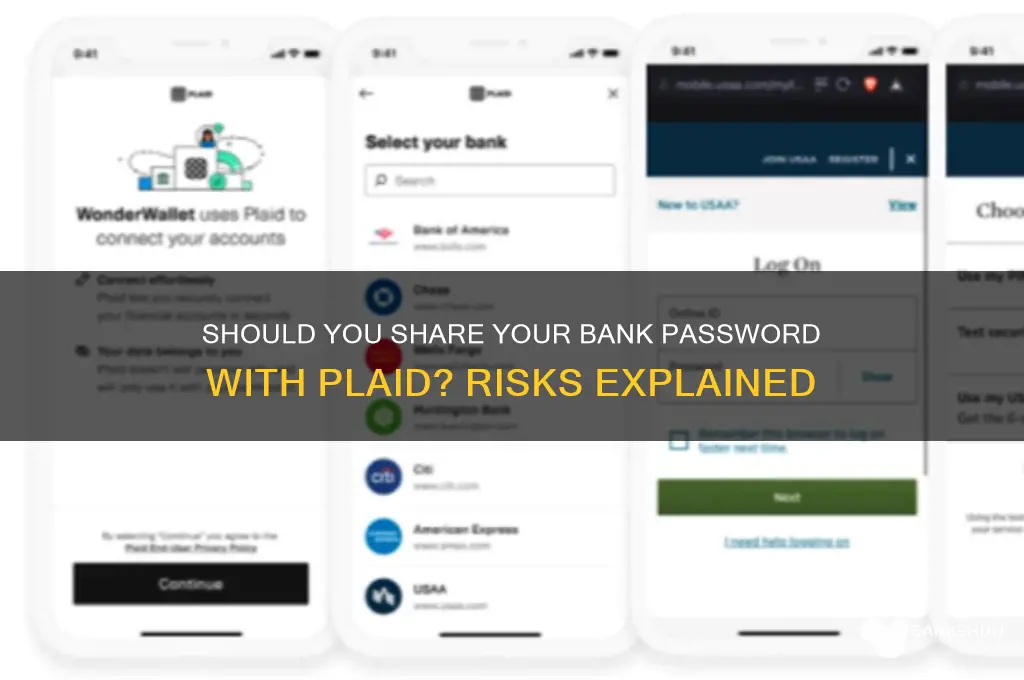

When considering whether to give Plaid access to your bank password, it’s essential to weigh the risks and benefits carefully. Plaid is a financial technology company that connects applications to your bank accounts, enabling services like budgeting apps, payment platforms, and investment tools. While Plaid does not store your bank login credentials, it uses them to securely access your financial data. However, sharing your password with any third-party service, even reputable ones, introduces potential security risks, such as unauthorized access or data breaches. To mitigate these risks, ensure the app using Plaid is trustworthy, enable two-factor authentication on your bank account, and monitor your transactions regularly. Alternatively, consider using Plaid’s bank connection methods that don’t require sharing your password, such as OAuth, if available. Ultimately, the decision depends on your comfort level with the app’s security practices and your willingness to trust Plaid’s encryption and data handling protocols.

| Characteristics | Values |

|---|---|

| Security Risks | Sharing bank passwords directly with any third-party service, including Plaid, is generally not recommended due to potential security risks. Plaid itself does not require your bank password; it uses secure APIs to connect to your bank. |

| Plaid's Process | Plaid uses secure, read-only connections to link your bank account. It does not store your bank login credentials. Instead, it generates a secure token to access account information. |

| Bank Policies | Most banks advise against sharing login credentials with third parties. Doing so may violate the bank's terms of service and void fraud protection guarantees. |

| Data Privacy | Plaid claims to prioritize data privacy and security, adhering to industry standards like SOC 2 and GDPR. However, sharing passwords directly undermines these protections. |

| Alternative Methods | Plaid typically uses secure methods like OAuth or secure APIs to connect to banks, eliminating the need for password sharing. |

| User Responsibility | Users should ensure they are using Plaid through a trusted application and avoid entering bank credentials on unverified platforms. |

| Expert Advice | Cybersecurity experts strongly advise against sharing bank passwords with any third-party service, including Plaid. |

| Regulatory Compliance | Plaid complies with financial regulations, but sharing passwords may expose users to unauthorized access or fraud. |

| Risk Mitigation | If a service explicitly asks for your bank password, it is likely a red flag. Plaid does not require this information. |

| Best Practice | Always use official banking apps or websites to link accounts with Plaid, and never share your bank password directly. |

Explore related products

What You'll Learn

![]()

Security Risks of Sharing Passwords

Sharing your bank password with any third-party service, including Plaid, exposes you to significant security risks. Passwords are the first line of defense for your financial accounts, and handing them over undermines this critical barrier. Once shared, you lose control over how that information is stored, transmitted, or used. Even if Plaid itself is secure, human error, insider threats, or vulnerabilities in their systems could lead to unauthorized access. For instance, a data breach at Plaid could expose your password, potentially compromising not just your bank account but any other accounts where you reuse that password.

Consider the broader implications of password sharing. Many financial institutions explicitly prohibit sharing login credentials in their terms of service, and doing so could void fraud protections or warranties. Additionally, sharing passwords complicates accountability. If unauthorized transactions occur, your bank might deny liability, arguing that you violated their security policies. Even if Plaid is a trusted entity, the act of sharing passwords normalizes risky behavior, making you more likely to share credentials in less secure contexts.

From a technical standpoint, modern security practices emphasize the use of APIs and token-based authentication over password sharing. Plaid, for example, typically connects to bank accounts via secure APIs, which grant limited access without requiring your actual password. By bypassing this method and sharing your password directly, you’re circumventing safeguards designed to protect your account. This is akin to giving someone the keys to your house instead of installing a smart lock that grants temporary access.

To mitigate these risks, follow these practical steps: first, verify whether the service you’re using (like Plaid) requires your password or if it offers a more secure connection method. Second, enable two-factor authentication (2FA) on your bank account to add an extra layer of protection. Third, monitor your account regularly for suspicious activity. Finally, if you’ve already shared your password, change it immediately and review your account for any unauthorized changes. The takeaway is clear: sharing passwords, even with seemingly reputable services, is a gamble with your financial security.

Robinhood Bank Verification: Understanding the Timeframe for Account Approval

You may want to see also

Explore related products

![]()

Plaid’s Data Encryption Practices

Plaid, a financial technology company, employs robust data encryption practices to safeguard sensitive information, including bank login credentials. When you’re asked to provide your bank password to Plaid, it’s not stored in plaintext. Instead, Plaid uses end-to-end encryption, ensuring that your data is unreadable to unauthorized parties during transmission and storage. This process involves converting your password into a complex code using algorithms like AES-256, a standard trusted by governments and financial institutions worldwide. Understanding this technical layer is crucial for assessing whether sharing your credentials aligns with your security expectations.

Unlike traditional methods where passwords might be stored directly, Plaid’s encryption practices are designed to minimize risk. For instance, Plaid does not retain your actual bank login details; it generates tokens that serve as secure placeholders for your account. These tokens allow Plaid to access necessary financial data without exposing your credentials. This approach is akin to giving someone a keycard instead of your house key—they can enter, but they don’t know the master code. Such measures reduce the likelihood of data breaches, even if Plaid’s systems were compromised.

However, encryption alone isn’t foolproof. Plaid’s security also depends on compliance with industry standards, such as SOC 2 and GDPR, which mandate regular audits and updates to their encryption protocols. Users should verify that Plaid maintains these certifications, as they provide an external layer of accountability. Additionally, Plaid’s partnerships with major banks often require adherence to stricter security frameworks, further reinforcing their encryption practices. This multi-layered approach ensures that your data remains protected at every stage.

Practical tips for users include enabling two-factor authentication (2FA) on your bank account, even if Plaid doesn’t require it. This adds an extra barrier against unauthorized access. Also, monitor your account activity regularly for any anomalies. While Plaid’s encryption practices are robust, combining them with personal vigilance maximizes security. Remember, sharing credentials always carries inherent risk, but understanding Plaid’s encryption methods can help you make an informed decision.

Exploring Global Banking Density: Banks Per Capita Worldwide

You may want to see also

Explore related products

![]()

Alternatives to Password Sharing

Sharing your bank password with third-party services like Plaid raises significant security concerns. Fortunately, several alternatives exist that prioritize both convenience and safety. One such method is OAuth 2.0, a standardized protocol allowing users to grant limited access to their accounts without revealing credentials. Financial institutions increasingly support OAuth for secure data sharing, enabling services like budgeting apps or payment platforms to connect directly with banks via API integrations. This approach ensures that sensitive information remains encrypted and inaccessible to intermediaries.

Another viable alternative is tokenization, a process where sensitive data is replaced with unique identification symbols (tokens) that retain essential information without compromising security. For instance, instead of sharing your password, Plaid could generate a token specific to your account, valid only for the intended transaction or service. This minimizes exposure to potential breaches, as tokens are useless outside their designated context. Major payment processors like Visa and Mastercard already employ tokenization for secure transactions, setting a precedent for broader adoption in financial services.

For those seeking greater control, app-based authentication offers a password-free solution. Many banks now provide dedicated mobile apps with built-in features for third-party integrations. Users can authorize access directly within the app, often via biometric verification (fingerprint or facial recognition), ensuring that credentials never leave their device. This method not only eliminates password sharing but also leverages multi-factor authentication for added security.

Lastly, open banking frameworks, such as those mandated in the EU and UK, empower users to share financial data securely through regulated APIs. Under these systems, banks and third-party providers must adhere to strict security standards, ensuring that data is exchanged without requiring password disclosure. While open banking is region-specific, its principles are gaining traction globally, offering a blueprint for safer, password-free data sharing.

In conclusion, alternatives to password sharing—OAuth 2.0, tokenization, app-based authentication, and open banking—provide robust solutions for secure financial data access. By adopting these methods, users can safeguard their credentials while still enjoying the benefits of integrated financial services. Always verify that your bank and third-party providers support these protocols before proceeding.

Adding WAV Supply Omni Bank: A Step-by-Step Guide for Beginners

You may want to see also

Explore related products

![]()

User Privacy Concerns with Plaid

Plaid, a financial technology company, acts as a bridge between your bank account and third-party apps like Venmo, Robinhood, or budgeting tools. To establish this connection, Plaid often requests your bank login credentials, raising a red flag for many users. This practice, while technically secure through encryption, inherently creates a privacy concern: you're handing over the keys to your financial fortress to a middleman.

While Plaid emphasizes its commitment to data security and user privacy, the very nature of their service necessitates collecting and storing sensitive financial information. This centralized repository becomes a lucrative target for hackers, potentially exposing your account details, transaction history, and even login credentials if breached.

Consider this analogy: imagine giving a trusted friend a copy of your house key to water your plants while you're away. While you trust your friend, the act of handing over the key inherently increases the risk of someone else gaining access. Similarly, sharing your bank login with Plaid, even with their security measures, introduces a new vulnerability.

A crucial distinction lies in the type of access Plaid typically requests. Unlike simply viewing your account balance, Plaid often seeks "read and write" access, allowing connected apps to potentially initiate transactions on your behalf. This level of access, while convenient for features like automatic bill payments, significantly amplifies the potential damage in case of unauthorized access.

Mitigating these risks requires a multi-faceted approach. Firstly, scrutinize the permissions requested by apps using Plaid. Does a budgeting app truly need "write" access to your account? Secondly, explore alternative authentication methods offered by some banks, such as OAuth, which grant limited access without revealing your actual login credentials. Finally, regularly monitor your bank statements for any suspicious activity and promptly report any discrepancies.

Ultimately, the decision to share your bank password with Plaid hinges on a personal risk-benefit analysis. While the convenience of seamless financial app integration is undeniable, it's crucial to weigh it against the potential privacy implications and take proactive steps to minimize vulnerabilities. Remember, in the digital age, safeguarding your financial data requires constant vigilance and informed decision-making.

Exploring Stellwagen Bank: Distance from Gloucester and Travel Tips

You may want to see also

Explore related products

![]()

Benefits of Linking Bank Accounts via Plaid

Linking your bank account via Plaid offers a streamlined way to manage finances across multiple apps and services. By providing read-only access to your account, Plaid eliminates the need to manually input transaction data, saving time and reducing errors. For instance, budgeting apps like Mint or investment platforms like Robinhood use Plaid to sync your financial information in real-time, giving you a comprehensive view of your money without the hassle of logging into multiple accounts. This efficiency is particularly valuable for individuals juggling multiple financial tools.

From a security standpoint, Plaid’s approach is designed to minimize risk. Instead of sharing your bank password directly with third-party apps, Plaid acts as an intermediary, using encryption and tokenization to protect your data. This means apps never store your login credentials, reducing the likelihood of unauthorized access. While no system is entirely foolproof, Plaid’s compliance with industry standards like SOC 2 and GDPR provides a layer of trust for users concerned about data breaches. Always verify that the app requesting access is reputable and has a clear privacy policy.

One of the most practical benefits of using Plaid is its ability to enable seamless financial transactions. For example, peer-to-peer payment apps like Venmo or Cash App use Plaid to verify bank accounts instantly, allowing you to send or receive money without delays. Similarly, loan or rental applications often require bank verification, which Plaid can expedite by providing a snapshot of your financial health. This not only speeds up processes but also reduces the need for physical documentation, making it ideal for tech-savvy users who prioritize convenience.

Finally, linking accounts via Plaid empowers you with better financial insights. Apps leveraging Plaid can analyze your spending patterns, identify recurring bills, and even predict future expenses. For instance, a savings app might suggest setting aside $50 weekly based on your income and outgoings. This data-driven approach helps users make informed decisions, whether they’re aiming to pay off debt, save for a goal, or invest wisely. By consolidating financial data in one place, Plaid transforms how you interact with your money, turning passive observation into active management.

Is Robb Banks Part of Rich Gang? Unraveling the Truth

You may want to see also

Frequently asked questions

No, you should never share your bank password with Plaid or any third-party service. Plaid uses secure connections to link your bank account without requiring your login credentials.

Plaid connects to your bank via secure APIs (Application Programming Interfaces) provided by the bank, ensuring your login credentials remain private and secure.

Yes, Plaid is a trusted financial technology company that uses encryption and secure protocols to protect your data. However, always ensure you’re using Plaid through a reputable app or service.

If you mistakenly share your password, immediately change your bank account credentials and contact your bank to report the issue. Plaid does not store or request passwords.

Plaid only accesses the data necessary for the service you’re using (e.g., balance, transactions). The scope of access is determined by the app or service using Plaid, and you can usually control permissions.