The question of whether a bookkeeper should prepare the bank reconciliation is a critical one for businesses aiming to maintain accurate financial records. Bank reconciliations are essential for identifying discrepancies between the company’s records and the bank’s statements, ensuring cash balances are correct, and detecting errors or fraudulent activities. While bookkeepers are often responsible for recording financial transactions, their role in preparing bank reconciliations depends on factors such as the organization’s size, internal controls, and the complexity of its financial operations. Assigning this task to a bookkeeper can streamline the process, provided they have the necessary skills and oversight. However, in larger organizations or those with stricter internal controls, this responsibility might be delegated to a more senior financial professional to ensure accuracy and independence. Ultimately, the decision should align with the company’s financial policies and risk management strategies.

| Characteristics | Values |

|---|---|

| Responsibility | Traditionally, the bookkeeper can prepare the bank reconciliation. |

| Oversight | Should be reviewed and approved by a higher authority (e.g., accountant or manager). |

| Accuracy | Ensures accuracy in recording transactions and identifying discrepancies. |

| Timeliness | Should be prepared regularly (monthly or as needed) to maintain up-to-date records. |

| Internal Controls | Helps in implementing and maintaining strong internal controls. |

| Fraud Detection | Assists in detecting errors, omissions, or fraudulent activities. |

| Reconciliation Process | Involves comparing the bank statement with the company’s records. |

| Documentation | Requires proper documentation of all adjustments and discrepancies. |

| Software Usage | Can be facilitated using accounting software for efficiency. |

| Compliance | Ensures compliance with accounting standards and company policies. |

| Skill Requirement | Requires basic accounting knowledge and attention to detail. |

| Segregation of Duties | Ideally, the bookkeeper should not also approve or authorize transactions. |

| Communication | Requires clear communication with the bank for unresolved discrepancies. |

| Training | Bookkeepers should be trained in bank reconciliation processes. |

| Risk Management | Reduces financial risks by identifying and correcting errors promptly. |

Explore related products

What You'll Learn

![]()

Importance of Bank Reconciliation

Bank reconciliation is a critical task that ensures the accuracy and integrity of a company’s financial records. By comparing the internal accounting records with the bank statement, discrepancies such as unrecorded transactions, errors, or fraudulent activities can be identified and corrected. For instance, a bookkeeper might notice an uncleared check from three months ago, prompting an investigation into whether it was lost or fraudulently cashed. This process acts as a safeguard, preventing small errors from snowballing into significant financial issues. Without regular reconciliation, businesses risk operating on incorrect financial data, which can lead to poor decision-making and compliance violations.

The bookkeeper is often the most qualified individual to handle bank reconciliation due to their familiarity with the company’s financial transactions and accounting software. They possess the detailed knowledge required to trace discrepancies back to their source, such as a vendor payment recorded twice or a deposit posted to the wrong account. For example, a bookkeeper might identify a $500 difference between the company’s records and the bank statement, trace it to a bank fee not yet recorded, and update the books accordingly. This hands-on expertise ensures that reconciliation is not just a mechanical task but a meaningful review of financial health.

From a compliance perspective, bank reconciliation is non-negotiable. Regulatory bodies and auditors often require businesses to maintain reconciled accounts as proof of financial transparency and accountability. For small businesses, this might mean avoiding penalties during tax audits, while for larger corporations, it could prevent legal repercussions tied to inaccurate financial reporting. A bookkeeper’s role in this process is pivotal, as they ensure the company adheres to accounting standards like GAAP or IFRS. For instance, reconciling accounts monthly—a best practice—provides a clear audit trail and reduces the risk of material misstatements in financial statements.

Beyond compliance, bank reconciliation offers practical benefits for cash flow management. By identifying outstanding checks, uncleared deposits, or unauthorized transactions, businesses can better forecast liquidity and avoid overdraft fees. For example, a bookkeeper might flag a recurring subscription charge that was canceled but still being deducted, saving the company hundreds of dollars annually. This proactive approach to financial management empowers businesses to allocate resources efficiently and respond swiftly to discrepancies. In essence, the bookkeeper’s role in reconciliation is not just about balancing numbers but about safeguarding the company’s financial stability.

Capital One Cafés: Banking Meets Coffee Shops – Fact or Fiction?

You may want to see also

Explore related products

![LLC Beginner's Guide [All-in-One]: Start & Grow Your Business While Saving on Taxes – Insider Strategies, Bookkeeping Hacks & Smart Accounting Tips](https://m.media-amazon.com/images/I/61QksxYPu+L._AC_UY218_.jpg)

![]()

Bookkeeper’s Role in Reconciliation

Bank reconciliations are a critical control activity in financial management, ensuring that the company’s records align with external statements. While the task itself is straightforward—comparing the general ledger to the bank statement—its execution requires precision, attention to detail, and an understanding of accounting principles. Bookkeepers, often the first line of defense in maintaining accurate financial records, are ideally positioned to handle this process. Their daily involvement with transactions, from recording deposits to tracking expenses, provides them with the contextual knowledge needed to identify discrepancies efficiently. However, the question remains: should the bookkeeper prepare the bank reconciliation, or is this task better suited for someone else?

From a practical standpoint, delegating bank reconciliations to bookkeepers streamlines the process. They are already familiar with the company’s financial systems, transaction flows, and common discrepancies, such as uncleared checks or pending deposits. For instance, a bookkeeper who processes payroll will recognize recurring discrepancies related to direct deposits or tax payments, resolving them swiftly. This familiarity reduces the learning curve and minimizes errors compared to assigning the task to an external accountant or manager who may lack day-to-day exposure to the company’s finances. However, this approach assumes the bookkeeper has the necessary training and oversight to handle the task accurately.

Critics argue that allowing bookkeepers to prepare bank reconciliations creates a conflict of interest, as the same individual recording transactions would also be responsible for verifying their accuracy. This concern is valid, particularly in smaller organizations where segregation of duties is challenging. For example, if a bookkeeper inadvertently misclassifies an expense, they might overlook it during reconciliation, perpetuating the error. To mitigate this risk, companies should implement review processes, such as requiring a supervisor or external accountant to approve the reconciliation. This ensures accountability while still leveraging the bookkeeper’s expertise.

Ultimately, the bookkeeper’s role in reconciliation depends on the organization’s size, structure, and internal controls. In small businesses with limited staff, the bookkeeper is often the most qualified person to handle this task, provided they operate under proper oversight. Larger companies, however, may benefit from assigning reconciliations to a separate accounting team or internal auditor to maintain independence. Regardless of who performs the task, the key is to establish clear procedures, regular reviews, and a culture of transparency. When executed correctly, involving bookkeepers in bank reconciliations can enhance accuracy, efficiency, and financial integrity.

Ally Bank Fees: What You Need to Know

You may want to see also

Explore related products

![]()

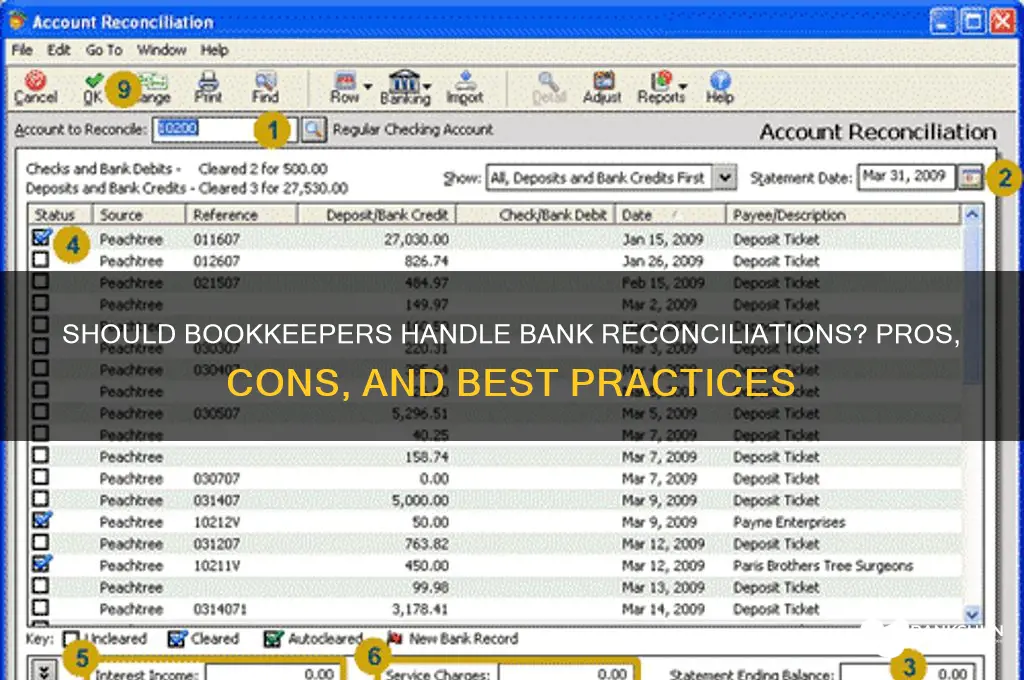

Steps to Prepare Reconciliation

Bank reconciliation is a critical task that ensures the accuracy of financial records by comparing the company's books with bank statements. While some argue that this responsibility should fall on accountants or financial managers, a skilled bookkeeper is often the ideal candidate for this task due to their familiarity with day-to-day transactions. Here’s a structured approach to preparing a bank reconciliation effectively.

Step 1: Gather Documents

Begin by collecting the necessary documents: the company’s general ledger (or accounting software records) and the latest bank statement. Ensure both are for the same period. For example, if reconciling April, align the ledger transactions from April 1 to April 30 with the bank statement covering the same dates. Missing even a single day can lead to discrepancies, so double-check the date ranges.

Step 2: Compare and Identify Discrepancies

Start by matching transactions in the ledger with those on the bank statement. Highlight unmatched items, such as uncleared checks, unrecorded deposits, or bank fees. For instance, if a $500 deposit appears on the bank statement but not in the ledger, investigate whether it was overlooked or not yet recorded. This step requires meticulous attention to detail, as small errors can compound over time.

Step 3: Adjust for Timing Differences

Not all discrepancies indicate errors. Timing differences, such as deposits in transit or outstanding checks, are common. For example, a check issued on April 28 may not clear the bank until May. Note these items as reconciling adjustments rather than errors. Use a separate section in your reconciliation worksheet to track them, ensuring clarity and organization.

Step 4: Investigate and Correct Errors

Once timing differences are accounted for, address remaining discrepancies. Common issues include data entry errors, omitted transactions, or bank mistakes. For instance, a $1,200 payment recorded as $120 in the ledger requires immediate correction. Document each error and its resolution to maintain transparency. If the bank made an error, contact them promptly to rectify it.

Step 5: Finalize and Document

After reconciling all items, ensure the adjusted book balance matches the bank statement balance. Prepare a reconciliation report detailing unmatched items, adjustments, and corrections. This document serves as a reference for future audits or reviews. For added efficiency, use accounting software with built-in reconciliation tools to streamline the process and reduce manual errors.

By following these steps, a bookkeeper can ensure accurate and reliable financial records, reinforcing their role as a key contributor to a company’s financial health.

When Did BMO Bank Integrate Zelle for Customers?

You may want to see also

Explore related products

![]()

Common Reconciliation Errors

Bank reconciliations are a critical task for maintaining accurate financial records, yet they are prone to errors that can lead to discrepancies between the books and bank statements. One common mistake is failing to record outstanding checks or deposits in a timely manner. For instance, a bookkeeper might overlook a check issued to a vendor that hasn’t cleared the bank yet, or a deposit made late in the month that isn’t reflected in the statement. These omissions create mismatches that complicate reconciliation and distort cash flow visibility. To avoid this, bookkeepers should maintain a detailed schedule of outstanding items and cross-reference it with the bank statement regularly.

Another frequent error is misclassifying transactions, which occurs when entries are posted to the wrong account or category. For example, a reimbursement to an employee might be mistakenly recorded as a business expense instead of an owner’s draw. Such misclassifications not only skew financial reports but also make it harder to trace discrepancies during reconciliation. Bookkeepers can mitigate this by implementing a robust chart of accounts and double-checking transaction details before posting. Additionally, using accounting software with automated categorization features can reduce human error.

Duplicate entries are a third common pitfall, often arising from manual data entry or system glitches. For instance, a bookkeeper might record a payment twice, either in the accounting system or by mistakenly including it in both the current and previous month’s reconciliations. These duplicates inflate expenses or income, throwing off the balance. To prevent this, bookkeepers should reconcile transactions chronologically and use software tools that flag potential duplicates. A quick review of transaction amounts and dates can also catch these errors before they compound.

Lastly, ignoring bank fees or interest can lead to unresolved differences between the books and the bank statement. Small charges like monthly maintenance fees or interest earned on deposits are often overlooked, especially in businesses with high transaction volumes. These minor discrepancies accumulate over time, making reconciliation more challenging. Bookkeepers should scrutinize bank statements for such entries and ensure they are recorded in the accounting system. Setting up automated alerts for bank fees can also help in catching these items promptly.

In conclusion, while bank reconciliations are essential, they are susceptible to errors that require vigilance and systematic approaches to avoid. By addressing outstanding items, ensuring proper classification, preventing duplicates, and accounting for all bank-related charges, bookkeepers can maintain accurate financial records and streamline the reconciliation process.

Does Union Bank of California Offer Zelle for Customers?

You may want to see also

Explore related products

![]()

Tools for Efficient Reconciliation

Efficient bank reconciliation hinges on leveraging the right tools to streamline the process and minimize errors. Modern accounting software like QuickBooks, Xero, or FreshBooks integrates bank feeds directly into the platform, automatically importing transactions and flagging discrepancies. These tools reduce manual data entry, saving time and decreasing the likelihood of human error. For instance, QuickBooks allows users to match transactions with existing records, categorize new entries, and reconcile accounts with just a few clicks. However, reliance on automation requires vigilance—regularly review imported data to ensure accuracy, as even automated systems can misinterpret transactions.

Beyond software, spreadsheet tools like Microsoft Excel or Google Sheets remain invaluable for reconciling complex or non-standard accounts. Customizable templates can be tailored to specific business needs, allowing for detailed tracking of uncleared checks, deposits in transit, and outstanding debits or credits. For example, a dynamic formula in Excel can automatically calculate the adjusted bank balance by subtracting outstanding checks and adding unrecorded deposits. While spreadsheets demand more manual effort, they offer flexibility for businesses with unique reconciliation requirements. Pairing these tools with a structured process ensures consistency and thoroughness.

For businesses handling multiple accounts or currencies, specialized reconciliation software like AutoRec or BlackLine can be a game-changer. These platforms automate advanced tasks such as multi-currency matching, high-volume transaction processing, and variance analysis. BlackLine, for instance, uses machine learning to identify patterns and anomalies, reducing the time spent investigating discrepancies. While these tools come with a higher cost, they are essential for larger organizations where manual reconciliation is impractical. Implementing such software requires upfront training but pays dividends in efficiency and accuracy.

Finally, no tool can replace the importance of clear documentation and organizational practices. Maintain a centralized repository for bank statements, receipts, and invoices, either physically or digitally, to ensure all necessary information is readily accessible. Establish a consistent schedule for reconciliation—monthly, at minimum—to prevent discrepancies from compounding. Pair these practices with periodic audits to validate the effectiveness of your tools and processes. By combining technology with disciplined habits, bookkeepers can transform reconciliation from a tedious chore into a seamless, error-free task.

Step-by-Step Guide to Generate Your Maharashtra Bank ATM PIN

You may want to see also

Frequently asked questions

Yes, the bookkeeper is typically responsible for preparing the bank reconciliation as part of their role in maintaining accurate financial records and ensuring transactions match between the company’s books and bank statements.

If the bookkeeper does not prepare the bank reconciliation, it can lead to undetected errors, fraud, or discrepancies in financial records, potentially causing cash flow issues and inaccurate financial reporting.

While someone else, such as an accountant or manager, can prepare the bank reconciliation, it is generally best practice for the bookkeeper to handle it to ensure consistency and familiarity with the company’s transactions. However, an independent review is recommended to maintain checks and balances.