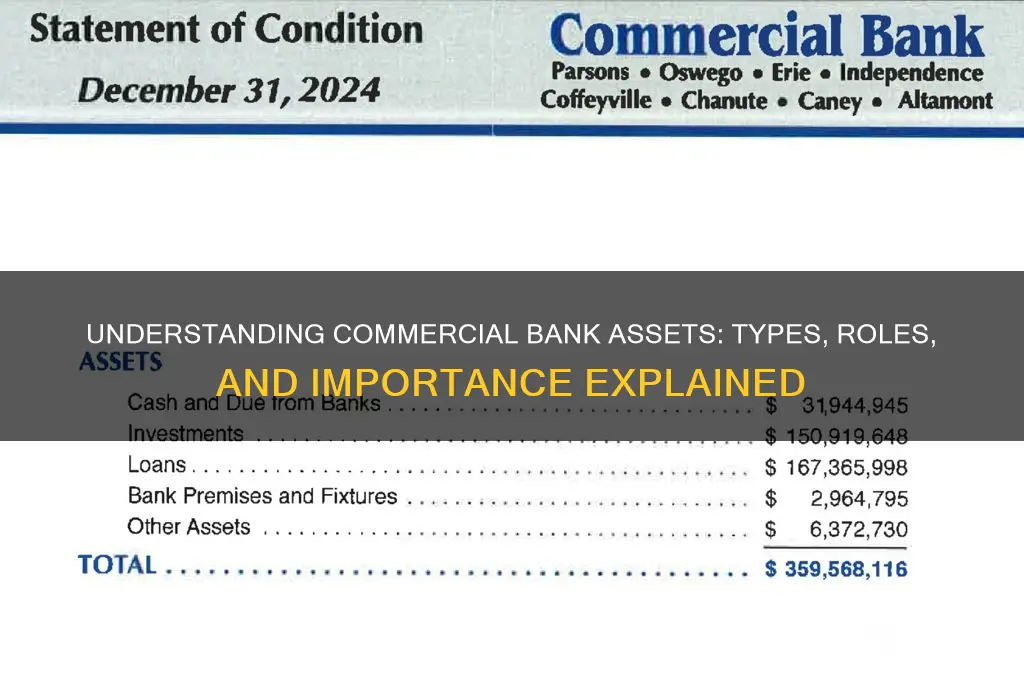

Assets for a commercial bank encompass a wide range of financial instruments and holdings that contribute to the bank's overall financial health and operational capabilities. These assets primarily include loans and advances to customers, which form the largest portion of a bank's balance sheet, as well as investments in securities like government bonds, treasury bills, and corporate debt. Additionally, cash reserves held in vaults or with central banks, along with physical properties and equipment, are also considered assets. These resources are crucial for generating income, maintaining liquidity, and ensuring the bank’s ability to meet its obligations while supporting economic activities through lending and investment.

Characteristics of Assets for a Commercial Bank

| Characteristics | Values |

|---|---|

| Definition | Resources owned by the bank with economic value, expected to provide future benefits. |

| Types | Cash & Cash Equivalents: Physical currency, reserves at central banks, highly liquid investments (e.g., treasury bills). Loans: Money lent to individuals, businesses, and governments with interest. Securities: Bonds, stocks, and other tradable financial instruments. < Fixed Assets: Physical property like buildings, land, and equipment used in bank operations. Other Assets: Intangible assets (e.g., goodwill), accrued interest, and other miscellaneous assets. |

| Liquidity | Varies depending on asset type. Cash is most liquid, loans are less liquid, and fixed assets are least liquid. |

| Risk | Varies depending on asset type and borrower creditworthiness. Loans carry higher risk than government bonds. |

| Return | Varies depending on asset type and risk. Loans typically offer higher returns than cash equivalents. |

| Maturity | Varies depending on asset type. Loans have specific maturities, while some securities may be perpetual. |

| Importance | Crucial for bank operations, lending, and generating revenue. |

Explore related products

What You'll Learn

- Cash Reserves: Physical currency and deposits held for liquidity and operational needs

- Loans & Advances: Funds lent to customers, generating interest income for the bank

- Securities Portfolio: Investments in government bonds, treasury bills, and other tradable assets

- Physical Assets: Buildings, equipment, and technology owned by the bank for operations

- Off-Balance-Sheet Assets: Contingent assets like letters of credit and derivatives

![]()

Cash Reserves: Physical currency and deposits held for liquidity and operational needs

Commercial banks are required to maintain a certain level of cash reserves, which serve as a crucial buffer for liquidity and operational needs. These reserves consist of physical currency stored in vaults and deposits held at central banks, ensuring that the institution can meet its short-term obligations and maintain stability during unforeseen circumstances. For instance, a bank with $100 million in total assets might be mandated to keep at least 10% in cash reserves, translating to $10 million readily accessible for withdrawals, settlements, or emergencies. This regulatory requirement varies by jurisdiction, with central banks like the Federal Reserve in the U.S. setting specific reserve ratios to safeguard financial systems.

Analyzing the composition of cash reserves reveals a strategic balance between physical cash and central bank deposits. Physical currency is immediately available for customer withdrawals and daily operations, while deposits at central banks earn interest and provide a secondary layer of liquidity. Banks must carefully manage this mix to optimize returns without compromising accessibility. For example, a bank might allocate 60% of its reserves to central bank deposits and 40% to physical cash, ensuring both yield and operational readiness. This allocation strategy is dynamic, adjusting to factors like withdrawal patterns, market conditions, and regulatory changes.

From a persuasive standpoint, maintaining robust cash reserves is not just a regulatory obligation but a strategic imperative for commercial banks. Adequate reserves enhance a bank’s credibility, enabling it to honor customer demands during high-volume withdrawal periods or economic downturns. Consider the 2008 financial crisis, where banks with stronger reserves weathered the storm better than those operating on thinner margins. By prioritizing cash reserves, banks not only comply with regulations but also build resilience, fostering trust among depositors and investors alike.

Comparatively, cash reserves differ from other bank assets like loans or investments in their primary function and risk profile. While loans generate interest income and investments offer higher returns, cash reserves are held for stability rather than profit. This distinction underscores the importance of diversification in a bank’s asset portfolio. For instance, a bank with 70% of its assets in loans and investments might allocate 15% to cash reserves, striking a balance between growth and security. This comparative approach highlights the unique role of cash reserves in mitigating risk and ensuring operational continuity.

Practically, managing cash reserves involves regular monitoring and adjustments to align with operational demands and regulatory standards. Banks use sophisticated forecasting models to predict cash flows, ensuring reserves remain sufficient without being excessive. For example, a regional bank might analyze historical withdrawal data to determine optimal reserve levels for peak seasons, such as holidays or tax periods. Additionally, banks must stay informed about changes in reserve requirements, as central banks may adjust ratios in response to economic conditions. By adopting a proactive approach, banks can maintain liquidity while maximizing the efficiency of their asset base.

Mastering the Art of Writing a Bank Manager Application

You may want to see also

Explore related products

![]()

Loans & Advances: Funds lent to customers, generating interest income for the bank

Commercial banks thrive on the delicate dance of lending and borrowing. At the heart of this lies their most significant asset: loans and advances. These are not mere transactions; they are the lifeblood of a bank's profitability, fueling economic growth while generating substantial interest income.

Imagine a bank as a financial gardener, sowing seeds of capital in the form of loans. These seeds, when nurtured responsibly, blossom into thriving businesses, homes, and personal endeavors. The bank, in turn, reaps the reward of interest, a steady stream of revenue that sustains its operations and fuels further lending.

This symbiotic relationship is the cornerstone of modern banking. Loans and advances, meticulously structured and managed, transform idle deposits into productive capital, driving economic activity and individual aspirations.

However, this seemingly simple concept demands meticulous execution. Banks must navigate a complex landscape of risk assessment, tailoring loan terms to individual circumstances. A misstep, a loan default, can quickly turn a promising asset into a liability. Therefore, prudent underwriting, rigorous credit checks, and ongoing portfolio monitoring are essential.

Think of it as a high-stakes game of chess. Each loan is a calculated move, balancing potential returns against the ever-present specter of risk. Diversification across borrowers, industries, and loan types becomes the bank's strategic defense, mitigating potential losses and ensuring long-term stability.

The types of loans and advances offered by commercial banks are as diverse as the needs of their customers. From mortgages financing dream homes to business loans fueling entrepreneurial ventures, each product is designed to meet specific financial goals. Personal loans cater to individual needs, while trade finance facilitates international commerce. This diversity allows banks to tap into various market segments, spreading risk and maximizing their reach.

Ultimately, loans and advances are not just financial instruments; they are catalysts for progress. They empower individuals to achieve their dreams, businesses to expand their horizons, and economies to flourish. For commercial banks, they represent the core of their asset portfolio, a dynamic and powerful engine driving both profitability and societal development.

BB&T and Truist Bank: Understanding the Merger and Brand Evolution

You may want to see also

Explore related products

$24.95 $24.95

![]()

Securities Portfolio: Investments in government bonds, treasury bills, and other tradable assets

A commercial bank's securities portfolio is a cornerstone of its asset management strategy, offering both stability and liquidity. This portfolio primarily consists of government bonds, treasury bills, and other tradable assets, which serve as a buffer against market volatility while generating steady returns. Government bonds, for instance, are considered low-risk investments backed by the creditworthiness of the issuing government, making them a safe haven for banks. Treasury bills, with their short-term maturity (typically 3 months to 1 year), provide quick liquidity and predictable income, essential for meeting regulatory requirements and managing cash flow.

When constructing a securities portfolio, diversification is key. Banks must balance their holdings across different asset classes, maturities, and issuers to mitigate risk. For example, a portfolio heavily weighted toward long-term government bonds may expose the bank to interest rate risk, as bond prices inversely correlate with rates. Conversely, a portfolio dominated by short-term treasury bills might yield lower returns but offers greater flexibility in a rising rate environment. Practical tip: Banks should use duration analysis to measure interest rate sensitivity and adjust their portfolio accordingly, ensuring alignment with their risk appetite and liquidity needs.

The role of tradable assets extends beyond risk management—they are also a strategic tool for profit generation. Banks can capitalize on market inefficiencies by trading securities, leveraging their expertise in market analysis and timing. For instance, during periods of economic uncertainty, banks may increase their holdings in government securities, which are perceived as safer, while reducing exposure to riskier assets. However, this approach requires robust market intelligence and a disciplined trading strategy. Caution: Over-reliance on trading activities can lead to speculative risks, so banks must maintain a clear distinction between their core banking operations and trading activities.

A well-managed securities portfolio also enhances a bank's regulatory compliance. Central banks often mandate that commercial banks hold a certain percentage of their assets in liquid, low-risk securities to ensure financial stability. For example, under Basel III regulations, banks are required to maintain a liquidity coverage ratio (LCR) of at least 100%, which measures their ability to withstand a 30-day stress scenario. Government bonds and treasury bills are ideal for meeting these requirements due to their high liquidity and low default risk. Takeaway: By strategically allocating resources to their securities portfolio, banks can simultaneously achieve regulatory compliance, risk mitigation, and income generation.

In conclusion, a securities portfolio is not just a passive holding but an active instrument in a commercial bank's financial toolkit. By investing in government bonds, treasury bills, and other tradable assets, banks can navigate economic uncertainties, optimize returns, and fulfill regulatory obligations. The key lies in striking the right balance between risk and reward, leveraging market insights, and maintaining a disciplined approach to portfolio management. For banks aiming to thrive in a dynamic financial landscape, a thoughtfully curated securities portfolio is indispensable.

Install Pokémon Homebrew Bank GB: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Physical Assets: Buildings, equipment, and technology owned by the bank for operations

Commercial banks rely heavily on physical assets to facilitate their daily operations and deliver services to customers. These assets, which include buildings, equipment, and technology, form the backbone of a bank's infrastructure. A bank's headquarters, branches, and data centers are prime examples of physical assets that enable face-to-face interactions, secure storage of valuables, and efficient processing of transactions.

The Strategic Importance of Location

A bank's buildings are more than just structures; they are strategic investments. Prime locations in high-traffic areas or business districts enhance visibility and accessibility, driving foot traffic and customer acquisition. For instance, a branch in a bustling city center can serve thousands of customers daily, while a poorly located one may struggle to attract even a fraction of that number. Banks must balance the cost of premium real estate with the potential return on investment, often leveraging footfall analytics to make informed decisions.

Equipment as the Operational Engine

Equipment such as ATMs, safes, and teller systems are critical to a bank's functionality. ATMs, for example, handle up to 90% of cash transactions in some markets, reducing the need for human tellers and operating 24/7. Safes and vaults, often reinforced with advanced security features like biometric locks and alarm systems, protect cash reserves and sensitive documents. Regular maintenance and upgrades of this equipment are essential to prevent downtime and security breaches, which can erode customer trust.

Technology: The Invisible Asset Driving Efficiency

Technology is arguably the most dynamic physical asset in a bank's portfolio. Servers, networking equipment, and software systems power online banking, mobile apps, and internal operations. A single data center can process millions of transactions daily, but it requires significant investment in cooling systems, cybersecurity measures, and disaster recovery protocols. For example, a Tier IV data center, the highest standard, guarantees 99.995% uptime, ensuring uninterrupted service even during equipment failures or power outages.

Balancing Investment and Depreciation

Physical assets depreciate over time, making their management a delicate balance between investment and replacement. A bank’s IT infrastructure, for instance, may become obsolete within 3–5 years due to rapid technological advancements. To mitigate this, banks often adopt a hybrid approach, leasing certain equipment (like ATMs) while owning core infrastructure (like data centers). Regular audits and depreciation schedules help banks allocate funds for upgrades, ensuring assets remain efficient and secure without straining the balance sheet.

By strategically managing buildings, equipment, and technology, commercial banks can optimize their physical assets to enhance operational efficiency, improve customer experience, and maintain a competitive edge in the financial landscape.

Second-Time Car Loans: How Banks Approach Repeat Auto Financing

You may want to see also

Explore related products

![]()

Off-Balance-Sheet Assets: Contingent assets like letters of credit and derivatives

Commercial banks manage a spectrum of assets, but not all are explicitly recorded on their balance sheets. Off-balance-sheet assets, particularly contingent assets like letters of credit and derivatives, play a critical role in a bank’s operations and risk profile. These instruments are not directly owned but represent potential future claims or obligations, often tied to specific conditions or events. Understanding their nature is essential for assessing a bank’s true financial health and exposure.

Letters of credit, for instance, are a prime example of off-balance-sheet contingent assets. They serve as guarantees issued by a bank on behalf of a client to ensure payment to a third party, typically in international trade. While the bank is not immediately liable, it assumes a contingent obligation if the client defaults. This asset is not recorded on the balance sheet unless the bank’s liability becomes probable. However, it still impacts the bank’s risk management, as it ties up capital reserves and requires careful monitoring to avoid unexpected losses. For banks, managing letters of credit involves assessing client creditworthiness and setting appropriate fees to compensate for the risk.

Derivatives, another category of off-balance-sheet assets, are financial contracts whose value is derived from an underlying asset, such as interest rates, currencies, or commodities. Banks use derivatives for hedging, speculation, or to meet client needs. For example, an interest rate swap allows a bank to manage exposure to fluctuating rates without holding the underlying assets or liabilities on its balance sheet. While derivatives can enhance profitability, they also introduce complexity and risk. Their off-balance-sheet nature can obscure a bank’s true leverage, making it crucial for regulators and investors to scrutinize these instruments through disclosures and stress tests.

The takeaway is that off-balance-sheet contingent assets like letters of credit and derivatives are powerful tools for banks but require meticulous oversight. They enable banks to facilitate trade, manage risk, and generate income without directly impacting their balance sheets. However, their contingent nature means they can quickly become liabilities under adverse conditions. Banks must maintain robust risk management frameworks, including scenario analysis and capital adequacy assessments, to ensure these assets do not undermine financial stability. For stakeholders, transparency and understanding of these instruments are key to evaluating a bank’s resilience.

Bank of Dave's Progress: Assessing Its Performance and Impact Today

You may want to see also

Frequently asked questions

Assets for a commercial bank are economic resources owned by the bank that have future economic value. These include cash, loans, securities, buildings, and other items that can generate income or be converted into cash.

Assets are crucial for a commercial bank because they represent the bank's ability to generate revenue, provide loans, and maintain liquidity. They also serve as a measure of the bank's financial strength and stability.

The main types of assets held by a commercial bank include cash reserves, loans (e.g., mortgages, business loans), securities (e.g., government bonds, corporate bonds), and physical assets like buildings and equipment.