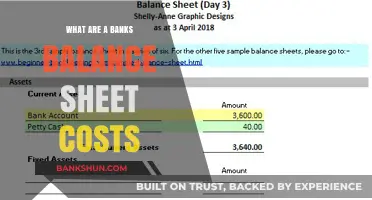

Bank and financial institution records encompass a wide array of documents and data that track financial transactions, account activities, and customer information. These records include bank statements, deposit and withdrawal slips, loan agreements, credit card statements, and investment account details. Financial institutions are required by law to maintain these records for regulatory compliance, audit purposes, and to ensure transparency in financial operations. They serve as critical tools for monitoring account balances, detecting fraudulent activities, and providing historical financial data for individuals and businesses. Additionally, these records are often used by law enforcement agencies, tax authorities, and legal entities to investigate financial crimes, resolve disputes, and enforce financial regulations. Understanding the nature and importance of these records is essential for both consumers and professionals in the financial sector.

| Characteristics | Values |

|---|---|

| Definition | Official documents maintained by banks and financial institutions tracking financial transactions and account activities. |

| Types of Records | Account statements, transaction histories, loan agreements, deposit slips, wire transfer records, mortgage documents, credit card statements, investment account records. |

| Purpose | Track financial activities, monitor account balances, detect fraud, comply with regulatory requirements, and provide proof of transactions. |

| Retention Period | Varies by jurisdiction and institution; typically 5–7 years for most records, but some (e.g., tax-related) may be kept longer. |

| Regulatory Compliance | Subject to laws like the Bank Secrecy Act (BSA), Anti-Money Laundering (AML) regulations, GDPR, and local financial reporting requirements. |

| Accessibility | Accessible to account holders, authorized representatives, and regulatory bodies upon request or legal mandate. |

| Formats | Physical (paper) or digital (electronic statements, online banking portals, PDFs). |

| Security Measures | Encrypted storage, access controls, audit trails, and compliance with data protection standards (e.g., PCI DSS). |

| Use in Investigations | Critical for legal proceedings, audits, tax assessments, and fraud investigations. |

| Examples of Data Included | Account numbers, transaction dates, amounts, payee/payer details, balances, interest rates, fees, and signatures. |

| Privacy Considerations | Protected under privacy laws; unauthorized access or sharing is prohibited. |

| Digital Transformation | Increasingly digitized, with many institutions offering paperless records and real-time transaction tracking. |

| Interoperability | Often shared between institutions for purposes like loan approvals, credit scoring, and cross-border transactions. |

| Historical Significance | Serve as a financial history for individuals and businesses, aiding in creditworthiness assessments and financial planning. |

Explore related products

What You'll Learn

- Types of Bank Records: Transaction histories, account statements, loan agreements, deposit slips, and wire transfer documents

- Financial Institution Compliance: Regulatory filings, audit reports, anti-money laundering (AML) records, and KYC documents

- Customer Data Storage: Personal information, account details, transaction logs, and digital banking activity records

- Investment Records: Portfolio statements, mutual fund transactions, stock trades, and bond holdings documentation

- Security & Fraud Monitoring: Suspicious activity reports (SARs), fraud alerts, cybersecurity logs, and breach records

![]()

Types of Bank Records: Transaction histories, account statements, loan agreements, deposit slips, and wire transfer documents

Bank records are the backbone of financial accountability, offering a detailed snapshot of an individual’s or entity’s monetary activities. Among these, transaction histories stand out as the most granular. They chronicle every debit and credit, from daily coffee purchases to large investments, often spanning months or years. For businesses, this record is critical for reconciling accounts and identifying discrepancies. For individuals, it serves as a personal finance ledger, revealing spending habits and areas for budgeting improvement. Most banks provide digital access to this data, allowing users to filter by date, amount, or merchant—a feature invaluable during tax season or fraud investigations.

While transaction histories focus on movement, account statements provide a periodic summary of financial health. Issued monthly or quarterly, these documents list opening and closing balances, accrued interest, fees, and a condensed transaction log. They are essential for verifying bank accuracy and detecting unauthorized activity. For instance, a sudden drop in savings might indicate a forgotten subscription or fraudulent withdrawal. Statements also serve as proof of income or assets when applying for loans or leases. Pro tip: Review statements within 30 days—most banks limit liability for unauthorized charges reported after this window.

Loan agreements represent a different breed of bank record, binding borrowers to repayment terms. These legally enforceable documents detail loan amounts, interest rates, repayment schedules, and penalties for default. For mortgages, they may include property descriptions and insurance requirements. Small business owners often scrutinize these agreements to ensure compliance with cash flow projections. A missed clause, such as a prepayment penalty, can cost thousands. Always request a copy for your records and consult a financial advisor if terms like "variable rate" or "balloon payment" are unclear.

The humble deposit slip is often overlooked but plays a vital role in cash management. This receipt confirms the amount and date of funds added to an account, whether via cash, check, or electronic transfer. For businesses handling large volumes of cash, deposit slips are critical for reconciling daily sales with bank deposits. They also serve as evidence in disputes over missing funds. Keep these slips for at least a year, especially if you frequently deposit checks, as they can expedite re-deposits in case of bank errors.

Wire transfer documents are the international passport of bank records, facilitating cross-border transactions. These forms require sender and recipient details, currency amounts, and transfer fees, often with SWIFT or routing codes. Businesses rely on them for supplier payments or overseas investments, while individuals use them for remittances or property purchases abroad. A single mistake in the recipient’s account number can result in irreversible loss, so double-checking details is non-negotiable. Retain these records for at least three years, as they may be requested during audits or tax assessments.

Each of these record types serves a distinct purpose, yet together they form a comprehensive financial narrative. Transaction histories and account statements track day-to-day activities, loan agreements outline long-term commitments, deposit slips verify cash inflows, and wire transfer documents manage global exchanges. Understanding their nuances empowers individuals and businesses to maintain accuracy, resolve disputes, and plan for the future. Treat these records as more than paperwork—they are tools for financial mastery.

Plainscapital Bank's Branch Network: A Comprehensive Overview of Locations

You may want to see also

Explore related products

![]()

Financial Institution Compliance: Regulatory filings, audit reports, anti-money laundering (AML) records, and KYC documents

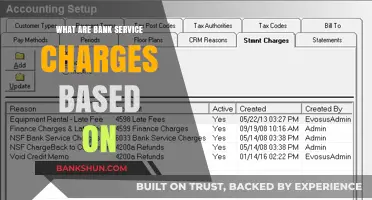

Financial institutions are required to maintain a labyrinth of records to ensure compliance with regulatory standards, a task that is both critical and complex. Among these, regulatory filings stand as the backbone of transparency, providing authorities with a clear view of an institution's financial health, operations, and adherence to laws. For instance, in the United States, banks must file the Call Report (FFIEC 031, 041, or 051) quarterly, detailing assets, liabilities, and equity. This document is not just a formality; it serves as a diagnostic tool for regulators to identify potential risks and ensure stability in the financial system. Similarly, the Suspicious Activity Report (SAR) is a critical filing that helps in the early detection of fraudulent activities, requiring meticulous documentation and timely submission.

Audit reports, another cornerstone of compliance, offer an independent evaluation of a financial institution's operations, internal controls, and risk management practices. These reports are not merely for internal review; they are often shared with regulatory bodies to demonstrate accountability and integrity. For example, external audits conducted by firms like Deloitte or PwC assess whether a bank’s financial statements are free from material misstatement, providing stakeholders with confidence in the institution’s reliability. Internal audits, on the other hand, focus on operational efficiency and compliance with internal policies, often uncovering vulnerabilities before they escalate into regulatory issues. Together, these audits form a dual layer of assurance that safeguards both the institution and its customers.

Anti-money laundering (AML) records are a non-negotiable component of compliance, designed to prevent financial institutions from being exploited for illicit activities. These records include transaction monitoring logs, customer due diligence files, and documentation of flagged suspicious activities. For instance, banks must retain AML records for a minimum of five years, as mandated by the Bank Secrecy Act (BSA) in the U.S. Failure to comply can result in severe penalties, such as the $1.5 billion fine imposed on Danske Bank in 2022 for AML violations. Effective AML compliance requires robust systems that can detect unusual patterns, such as large cash deposits or frequent international transfers, and trigger investigations when necessary.

Know Your Customer (KYC) documents are the first line of defense in compliance, ensuring that financial institutions understand their customers’ identities, financial behaviors, and potential risks. These documents typically include government-issued IDs, proof of address, and source of wealth statements. For high-risk customers, such as politically exposed persons (PEPs), enhanced due diligence (EDD) measures are required, involving deeper investigations into their financial backgrounds. KYC is not a one-time process; it demands ongoing monitoring to detect any changes in customer behavior or risk profiles. For example, a sudden increase in transaction volume or a shift to high-risk jurisdictions should prompt a review of the customer’s KYC file.

In conclusion, financial institution compliance is a multifaceted discipline that hinges on the meticulous management of regulatory filings, audit reports, AML records, and KYC documents. Each of these elements plays a unique yet interconnected role in maintaining the integrity of the financial system. By adhering to these requirements, institutions not only avoid regulatory penalties but also build trust with customers and stakeholders. Practical tips for success include investing in advanced compliance technologies, fostering a culture of accountability, and staying abreast of evolving regulatory landscapes. Ultimately, compliance is not just about meeting legal obligations—it’s about upholding the ethical standards that underpin the financial industry.

Uncovering Bank Operating Expenses: A Step-by-Step Guide to Calculation

You may want to see also

Explore related products

![The Life of a Showgirl[Sweat & Vanilla Perfume Orange Glitter Vinyl]](https://m.media-amazon.com/images/I/911UuOv5wEL._AC_UY218_.jpg)

![]()

Customer Data Storage: Personal information, account details, transaction logs, and digital banking activity records

Banks and financial institutions are custodians of vast amounts of customer data, a treasure trove that includes personal information, account details, transaction logs, and digital banking activity records. This data is the backbone of financial services, enabling institutions to manage accounts, detect fraud, and comply with regulatory requirements. However, the storage of such sensitive information comes with significant responsibilities, particularly in ensuring data security and privacy.

Personal Information: The Foundation of Trust

At the core of customer data storage lies personal information—names, addresses, dates of birth, Social Security numbers, and contact details. This data is critical for identity verification and customer onboarding. For instance, when opening an account, a bank must verify the customer’s identity to comply with Know Your Customer (KYC) regulations. This information is often stored in encrypted databases, with access restricted to authorized personnel. A practical tip for customers is to regularly update their contact details to ensure seamless communication and avoid potential security risks, such as misdirected statements or alerts.

Account Details: The Blueprint of Financial Activity

Account details, including account numbers, balances, and linked services, form the blueprint of a customer’s financial activity. This data is essential for processing transactions, managing loans, and providing tailored financial products. For example, a mortgage application relies on account details to assess creditworthiness. Financial institutions must ensure this data is stored in secure, segmented systems to prevent unauthorized access. Customers should monitor their account details regularly, using tools like mobile banking apps, to detect any discrepancies or unauthorized changes promptly.

Transaction Logs: The Digital Footprint of Financial Behavior

Transaction logs are the digital footprint of every financial interaction, from ATM withdrawals to online purchases. These records are invaluable for dispute resolution, tax reporting, and fraud detection. For instance, a suspicious transaction pattern might trigger an alert for potential fraud. Banks often retain transaction logs for 5–7 years, depending on regulatory requirements. Customers can leverage this data by reviewing monthly statements to track spending habits and identify areas for financial improvement. A practical tip is to categorize transactions using budgeting apps linked to bank accounts for better financial management.

Digital Banking Activity Records: The Pulse of Modern Finance

With the rise of digital banking, activity records—such as login times, device usage, and app interactions—have become critical. These records help institutions personalize services, enhance user experience, and strengthen security. For example, a bank might flag an unusual login from a new device as a potential security threat. However, this data also raises privacy concerns, necessitating transparent policies and robust encryption. Customers should enable two-factor authentication (2FA) and use secure networks when accessing digital banking services to protect their activity records.

In conclusion, customer data storage in banks and financial institutions is a complex, multifaceted process that balances utility with responsibility. By understanding the types of data stored and their purposes, both institutions and customers can take proactive steps to ensure security, compliance, and financial well-being.

Step-by-Step Guide to Applying for Union Bank Job Opportunities

You may want to see also

Explore related products

![KPop Demon Hunters (Soundtrack from the Netflix Film)[LP]](https://m.media-amazon.com/images/I/51dC+jRm3sL._AC_UY218_.jpg)

![]()

Investment Records: Portfolio statements, mutual fund transactions, stock trades, and bond holdings documentation

Investment records are the backbone of financial transparency, offering a detailed snapshot of an individual’s or entity’s financial health and activity. Among these, portfolio statements stand out as comprehensive summaries of all holdings, including stocks, bonds, mutual funds, and other assets. Typically issued quarterly or annually, they provide a consolidated view of asset allocation, performance, and market value. For instance, a portfolio statement might reveal that 60% of your assets are in equities, 30% in fixed income, and 10% in cash, helping you assess risk exposure and diversification. These statements are critical for tax planning, as they document capital gains, dividends, and interest income, which are taxable events.

While portfolio statements offer a broad overview, mutual fund transactions and stock trades provide granular insights into buying and selling activity. Mutual fund transaction records detail purchases, redemptions, and dividend reinvestments, often accompanied by expense ratios and fund performance metrics. For example, a record might show a $5,000 investment in an S&P 500 index fund with a 0.05% expense ratio, highlighting both the cost and potential return. Stock trade records, on the other hand, capture individual transactions, including purchase price, date, and quantity. These are essential for calculating cost basis and capital gains, especially in taxable accounts. For instance, selling 100 shares of Apple at $150 each, purchased at $100, would result in a $5,000 capital gain, subject to taxation.

Bond holdings documentation is equally vital, particularly for fixed-income investors. These records include details such as bond issuer, maturity date, coupon rate, and face value. For example, a $10,000 corporate bond with a 5% coupon rate pays $500 annually until maturity. Such documentation is crucial for tracking interest income and assessing credit risk. Unlike stocks, bonds often have specific tax treatments, such as municipal bonds, which may offer tax-exempt interest. Accurate bond records ensure compliance with tax laws and help investors evaluate the safety and yield of their fixed-income portfolio.

Maintaining these investment records is not just a best practice—it’s a necessity. For practical tips, consider digitizing all documents for easy access and backup. Use financial software like Quicken or Excel to track transactions and reconcile them with brokerage statements. Review records annually to identify errors or discrepancies, such as missing trades or incorrect cost basis. For retirees or those nearing retirement, ensure records are organized to facilitate required minimum distributions (RMDs) from retirement accounts. Finally, consult a financial advisor or tax professional to optimize tax strategies and ensure compliance with regulations. By treating investment records as a living document, you empower yourself to make informed decisions and secure your financial future.

Understanding MAB Calculation in HDFC Bank: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Security & Fraud Monitoring: Suspicious activity reports (SARs), fraud alerts, cybersecurity logs, and breach records

Banks and financial institutions are treasure troves of sensitive data, making them prime targets for fraudsters and cybercriminals. To combat this, a robust security infrastructure is essential, with Suspicious Activity Reports (SARs), fraud alerts, cybersecurity logs, and breach records forming the backbone of fraud monitoring and prevention.

SARs, mandated by law, are confidential reports filed by financial institutions to alert authorities about potentially illegal activities like money laundering or terrorist financing. These reports, while not proof of wrongdoing, trigger investigations and can lead to the dismantling of criminal networks. Think of them as silent alarms, discreetly signaling trouble to the authorities.

Fraud alerts, on the other hand, are proactive measures. They act as early warning systems, notifying customers of potentially unauthorized transactions on their accounts. A sudden large purchase in a foreign country, for example, might trigger an alert, prompting the customer to verify its legitimacy. This real-time notification system empowers individuals to act swiftly, minimizing potential losses.

Behind the scenes, cybersecurity logs paint a detailed picture of network activity. These logs record every login attempt, file access, and system change, providing a digital footprint of all interactions. By analyzing these logs, security teams can identify anomalies like repeated failed login attempts from unfamiliar locations, potentially indicating a brute-force attack. Think of these logs as a digital surveillance system, constantly monitoring for suspicious behavior.

Breach records, unfortunately, document the aftermath of successful attacks. They detail the nature of the breach, the data compromised, and the steps taken to mitigate the damage. While a breach is a setback, these records are invaluable for learning from mistakes, strengthening defenses, and complying with data breach notification laws. They serve as stark reminders of the ever-present threat and the need for constant vigilance.

The synergy between these elements is crucial. SARs provide intelligence to law enforcement, fraud alerts empower customers, cybersecurity logs offer real-time monitoring, and breach records inform future defenses. Together, they form a multi-layered security net, constantly adapting to evolving threats. By diligently maintaining and analyzing these records, financial institutions can safeguard their customers' assets and maintain trust in the financial system.

Understanding the Mortgage Process: How Banks Approve and Fund Home Loans

You may want to see also

Frequently asked questions

Bank and financial institution records are documents and data maintained by banks, credit unions, investment firms, and other financial entities that detail transactions, account activities, and customer information.

These records are crucial for tracking financial activities, ensuring compliance with regulations, detecting fraud, resolving disputes, and providing transparency in financial transactions for both individuals and businesses.

They typically include account holder details, transaction histories, deposits, withdrawals, loan information, interest earned, fees charged, and any other financial activities associated with the account.

Retention periods vary by jurisdiction and institution but generally range from 5 to 7 years. Some records, especially those related to taxes or legal matters, may be kept longer.

Access is typically restricted to the account holder, authorized representatives, and financial institution employees. Law enforcement or government agencies may access these records with proper legal authorization, such as a court order or subpoena.