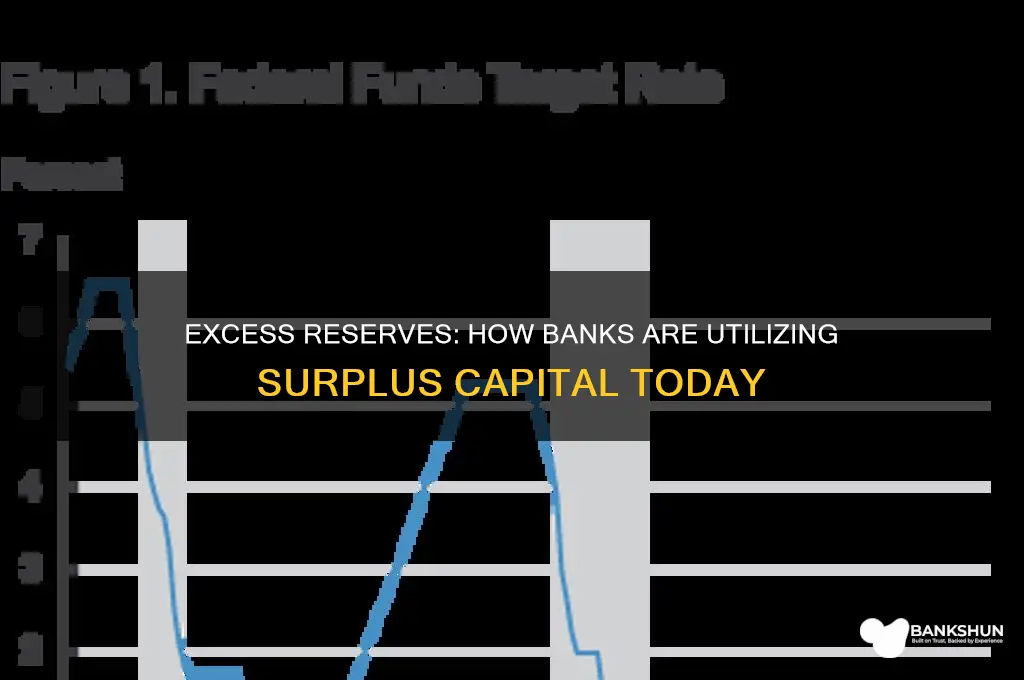

Banks are currently holding unprecedented levels of excess reserves, a phenomenon largely driven by quantitative easing policies and economic uncertainties. These reserves, which exceed regulatory requirements, have sparked debates about their implications for the financial system and broader economy. While some argue that excess reserves could fuel inflation or distort lending practices, others contend that they serve as a buffer against financial shocks and support monetary policy effectiveness. Central banks, such as the Federal Reserve, are closely monitoring these reserves and adjusting their strategies to manage liquidity and interest rates. Understanding how banks utilize excess reserves is crucial for assessing their impact on credit availability, market stability, and the overall economic recovery.

Explore related products

What You'll Learn

- Investing in Government Securities: Banks purchase low-risk government bonds to earn interest on excess reserves

- Lending to Businesses: Excess reserves are used to fund loans for business expansion and operations

- Consumer Lending Growth: Banks increase personal loans, mortgages, and credit card offerings using surplus funds

- Maintaining Liquidity Buffers: Excess reserves ensure banks meet regulatory requirements and manage cash flow needs

- Parking Funds at Central Banks: Banks deposit excess reserves with central banks for safety and modest returns

![]()

Investing in Government Securities: Banks purchase low-risk government bonds to earn interest on excess reserves

Banks often turn to government securities as a safe haven for their excess reserves, a strategy that balances risk and return in an uncertain economic landscape. These institutions, flush with liquidity, seek to put their idle funds to work without exposing themselves to the volatility of riskier assets. Government bonds, backed by the full faith and credit of the issuing government, offer a reliable stream of interest income, making them an attractive option for banks aiming to preserve capital while generating modest returns. This approach is particularly appealing during periods of economic uncertainty, when the stability of government securities provides a buffer against market fluctuations.

Consider the mechanics of this investment: when a bank purchases a government bond, it essentially lends money to the government in exchange for periodic interest payments and the return of the principal at maturity. For instance, a 10-year U.S. Treasury bond with a 3% yield provides the bank with a predictable income stream over the bond’s term. This predictability is crucial for banks, as it allows them to forecast cash flows accurately and maintain liquidity. Moreover, government securities are highly liquid, meaning banks can sell them quickly in the secondary market if they need to access their funds, adding another layer of security to this investment strategy.

However, this approach is not without its trade-offs. While government bonds offer safety, their yields are typically lower than those of riskier assets like corporate bonds or equities. For banks, this means accepting a lower return on their excess reserves in exchange for minimizing risk. During periods of low interest rates, as seen in recent years, the returns on government securities can be particularly modest, sometimes barely outpacing inflation. Banks must weigh this against the potential losses they could incur by investing in higher-yielding but more volatile assets.

To maximize the effectiveness of this strategy, banks often employ laddering techniques, distributing their investments across bonds with varying maturities. This approach ensures a steady stream of income and reduces the impact of interest rate changes on their portfolio. For example, a bank might allocate 20% of its excess reserves to short-term bonds (1–3 years), 50% to medium-term bonds (4–7 years), and 30% to long-term bonds (8–10 years). This diversification helps smooth out cash flows and provides flexibility to adapt to shifting economic conditions.

In conclusion, investing in government securities is a prudent way for banks to manage excess reserves, offering a balance of safety, liquidity, and predictable returns. While the yields may be modest, the stability and reliability of these investments make them a cornerstone of conservative financial management. By strategically allocating their funds across different maturities, banks can optimize this approach, ensuring they remain well-positioned to navigate economic uncertainties while generating steady income from their idle reserves.

Is Jeanne's Husband a Bank Robber? Uncovering the Truth

You may want to see also

Explore related products

![]()

Lending to Businesses: Excess reserves are used to fund loans for business expansion and operations

Banks are increasingly leveraging excess reserves to fuel business growth, a strategic move that not only stimulates economic activity but also enhances their own profitability. By channeling these reserves into loans for businesses, banks play a pivotal role in fostering innovation, job creation, and market expansion. This approach is particularly evident in sectors like technology, manufacturing, and renewable energy, where capital-intensive projects often require substantial upfront funding. For instance, a mid-sized tech startup might secure a $5 million loan to scale its operations, hire additional talent, and develop new products, all of which contribute to broader economic dynamism.

The process of lending excess reserves to businesses is not without its nuances. Banks must carefully assess creditworthiness, market conditions, and the borrower’s growth potential to mitigate risks. A common practice is to offer tiered loan structures, where interest rates and repayment terms are tailored to the business’s size, industry, and financial health. For example, a small business with a strong credit history might receive a 5% interest rate on a 10-year loan, while a riskier venture could face higher rates or require collateral. This tailored approach ensures that funds are allocated efficiently, maximizing returns for both the bank and the borrower.

One compelling example of this strategy in action is the surge in green financing, where banks use excess reserves to fund sustainable business initiatives. A renewable energy firm, for instance, could secure a $10 million loan to build a solar farm, with the bank benefiting from both the interest income and the positive environmental impact. Such loans often come with incentives, such as reduced interest rates for meeting sustainability milestones, aligning financial goals with societal benefits. This dual focus on profit and purpose exemplifies how excess reserves can be deployed to address pressing global challenges while driving economic growth.

However, banks must navigate potential pitfalls when lending excess reserves to businesses. Overconcentration in a single sector or over-reliance on high-risk loans can expose them to significant vulnerabilities. To mitigate these risks, diversification is key. Banks should balance their portfolios by funding businesses across various industries and at different stages of growth. Additionally, stress testing and scenario analysis can help institutions anticipate economic downturns and adjust their lending strategies accordingly. By adopting a proactive and diversified approach, banks can ensure that their use of excess reserves remains both profitable and sustainable.

In conclusion, lending excess reserves to businesses represents a powerful tool for banks to drive economic growth while strengthening their own financial positions. Through careful assessment, tailored loan structures, and strategic diversification, banks can effectively channel these funds into productive ventures. Whether supporting tech startups, green initiatives, or traditional industries, this approach underscores the critical role of banks in shaping a vibrant and resilient economy. As excess reserves continue to accumulate, their allocation to business lending will likely remain a cornerstone of modern banking strategy.

Stellwagen Bank to Boston: Distance and Travel Insights Revealed

You may want to see also

Explore related products

$40 $40

![]()

Consumer Lending Growth: Banks increase personal loans, mortgages, and credit card offerings using surplus funds

Banks are leveraging their excess reserves to fuel a surge in consumer lending, a strategic move that benefits both financial institutions and borrowers. By channeling surplus funds into personal loans, mortgages, and credit card offerings, banks are not only optimizing their balance sheets but also stimulating economic activity. This approach allows them to generate higher interest income while providing consumers with access to credit, which can drive spending and investment. For instance, personal loan approvals have risen by 15% year-over-year, with banks offering competitive rates as low as 6.5% APR to attract creditworthy borrowers. This trend underscores a win-win scenario where banks deploy idle capital productively, and consumers gain financial flexibility.

The mortgage market is another focal point for banks deploying excess reserves. With historically low interest rates and a surge in housing demand, banks are expanding their mortgage portfolios to capitalize on this opportunity. For example, some institutions are offering 30-year fixed-rate mortgages at rates below 4%, a move that not only attracts homebuyers but also locks in long-term revenue streams. This strategy is particularly effective in regions with high housing demand, such as urban centers and suburban areas experiencing population growth. However, banks must carefully assess risk, as overextending credit in a volatile housing market could lead to defaults and financial instability.

Credit card offerings are also seeing a boost as banks seek to tap into consumer spending habits. By increasing credit limits and introducing rewards programs, banks are encouraging card usage, which generates interchange fees and interest income. For instance, premium credit cards now offer up to 5% cashback on categories like groceries and travel, enticing consumers to spend more. Yet, this approach comes with risks, as higher credit limits can lead to increased consumer debt. Banks must balance growth with responsible lending practices, such as stricter credit checks and personalized spending limits, to mitigate potential defaults.

To maximize the benefits of this lending growth, banks should adopt a data-driven approach. Analyzing consumer behavior, creditworthiness, and market trends can help them tailor offerings to specific demographics. For example, millennials and Gen Z borrowers may prefer digital-first lending platforms with transparent terms, while older generations might value personalized service. Additionally, banks should invest in financial literacy programs to educate borrowers about managing debt responsibly. By combining strategic lending with consumer-centric practices, banks can sustainably grow their portfolios while fostering financial health in their communities. This dual focus ensures that excess reserves are not just deployed for profit but also for long-term economic stability.

Embracing Cultural Diversity: Transforming Banking Through Inclusive Practices and Innovation

You may want to see also

Explore related products

![]()

Maintaining Liquidity Buffers: Excess reserves ensure banks meet regulatory requirements and manage cash flow needs

Banks are required to maintain a certain level of liquidity to ensure they can meet their financial obligations, particularly during times of economic stress. This is where excess reserves come into play, serving as a crucial liquidity buffer. Regulatory bodies, such as the Federal Reserve in the United States, mandate that banks hold a minimum amount of reserves against their deposit liabilities. For instance, the liquidity coverage ratio (LCR) requires banks to hold high-quality liquid assets sufficient to cover total net cash outflows over a 30-day stress period. Excess reserves, which are funds held beyond these regulatory minimums, provide an additional safety net, enabling banks to manage unexpected cash flow needs without resorting to costly or destabilizing measures like fire sales of assets.

Consider the practical implications of this strategy. When a bank holds excess reserves, it gains flexibility in managing its balance sheet. For example, during periods of market volatility, depositors may withdraw funds en masse, or interbank lending markets may freeze. Banks with robust excess reserves can meet these demands without disrupting their operations or seeking emergency funding. This not only protects the bank but also contributes to broader financial stability by preventing contagion effects. A case in point is the 2008 financial crisis, where banks with higher excess reserves were better positioned to weather the storm, highlighting the importance of this buffer in crisis management.

However, maintaining excess reserves is not without trade-offs. Holding large amounts of cash or low-yielding assets reduces a bank’s potential to generate returns. Banks must strike a balance between regulatory compliance, liquidity needs, and profitability. One strategy is to invest excess reserves in short-term, highly liquid assets like Treasury bills or repurchase agreements, which offer modest returns while maintaining accessibility. Another approach is to use excess reserves as a tool for strategic planning, such as funding future loan growth or preparing for anticipated regulatory changes. For instance, banks may increase their excess reserves in anticipation of tighter liquidity requirements or economic downturns.

To effectively manage excess reserves, banks should adopt a dynamic approach tailored to their risk appetite and market conditions. This involves regularly assessing liquidity risk, stress-testing reserve levels, and aligning reserve policies with business objectives. For smaller banks, this might mean holding a higher proportion of excess reserves to offset limited access to funding markets. Larger banks, with more diversified funding sources, may opt for a leaner buffer but invest in systems to quickly mobilize reserves when needed. Regardless of size, transparency in reporting and clear communication with regulators are essential to demonstrate compliance and sound liquidity management.

In conclusion, excess reserves are a cornerstone of prudent liquidity management, enabling banks to meet regulatory requirements and navigate cash flow uncertainties. While holding excess reserves involves opportunity costs, the benefits in terms of stability and resilience far outweigh the drawbacks, particularly in volatile economic environments. By adopting strategic, data-driven approaches to reserve management, banks can optimize their liquidity buffers, ensuring they are well-prepared for both routine operations and unforeseen challenges.

The Mysterious Death of Carlos Maurice Banks: Unraveling the Truth

You may want to see also

Explore related products

![]()

Parking Funds at Central Banks: Banks deposit excess reserves with central banks for safety and modest returns

Banks often park excess reserves at central banks, a practice that combines safety with modest returns. This strategy is particularly appealing during periods of economic uncertainty or when other investment avenues carry higher risks. Central banks, such as the Federal Reserve in the United States or the European Central Bank, offer reserve accounts where commercial banks can deposit surplus funds. These deposits are considered virtually risk-free because central banks are backed by the full faith and credit of the government. In exchange for this security, banks earn interest on their reserves, typically at a rate set by the central bank’s policy rate. For instance, during the COVID-19 pandemic, many banks increased their holdings at central banks due to reduced lending opportunities and heightened market volatility.

The decision to park funds at central banks is not merely about safety; it also reflects a bank’s liquidity management strategy. Excess reserves held at central banks are highly liquid, meaning banks can access these funds immediately if needed. This liquidity is crucial for meeting regulatory requirements, such as the liquidity coverage ratio (LCR), which mandates banks maintain sufficient high-quality liquid assets to cover 30 days of net cash outflows. By depositing excess reserves at central banks, banks ensure compliance with these rules while earning a small return. For example, in 2022, U.S. banks held over $3 trillion in excess reserves at the Federal Reserve, a testament to the appeal of this low-risk, liquid option.

However, the practice of parking funds at central banks is not without trade-offs. While it offers safety and liquidity, the returns are typically modest compared to other investment opportunities. Central bank interest rates are often lower than yields on government bonds or interbank lending rates. Banks must weigh the benefits of risk-free returns against the potential for higher profits elsewhere. During periods of low-interest rates, as seen in the post-2008 era, the opportunity cost of holding excess reserves at central banks can be significant. Banks may opt to lend more aggressively or invest in higher-yielding assets when economic conditions improve.

Practical considerations also come into play when banks decide to park funds at central banks. For instance, banks must monitor central bank policy closely, as changes in interest rates directly impact the returns on excess reserves. Additionally, banks should assess their overall liquidity needs and risk appetite before committing large sums to central bank accounts. A diversified approach, where excess reserves are split between central bank deposits and other liquid assets, can balance safety and yield. For smaller banks with limited risk management capabilities, central bank deposits often serve as a cornerstone of their liquidity strategy.

In conclusion, parking funds at central banks is a strategic move for banks managing excess reserves. It prioritizes safety and liquidity while providing modest returns, making it an attractive option during uncertain times. However, banks must carefully evaluate the trade-offs, including the opportunity cost of forgoing higher-yielding investments. By staying informed about central bank policies and aligning this strategy with broader liquidity goals, banks can effectively leverage excess reserves to strengthen their financial position.

Exploring Exchange Bank's Workforce: Total Employee Count Revealed

You may want to see also

Frequently asked questions

Excess reserves are funds that banks hold beyond the required reserve ratio set by central banks. Banks hold them to ensure liquidity, manage risks, and meet unexpected withdrawal demands or financial obligations.

Banks can lend excess reserves to businesses and consumers, increasing the money supply and stimulating economic growth. However, if banks choose to hoard reserves, it can limit credit availability and slow economic activity.

Yes, central banks like the Federal Reserve often pay interest on excess reserves (IOER) to incentivize banks to keep funds in the banking system. This rate can influence bank behavior and monetary policy.

Banks may hold excess reserves due to economic uncertainty, lack of creditworthy borrowers, or regulatory requirements. Additionally, holding reserves can provide a buffer during financial stress.

Excess reserves can be a tool for central banks to control inflation. By adjusting the interest rate on excess reserves, central banks can encourage or discourage lending, thereby influencing inflation and economic stability.