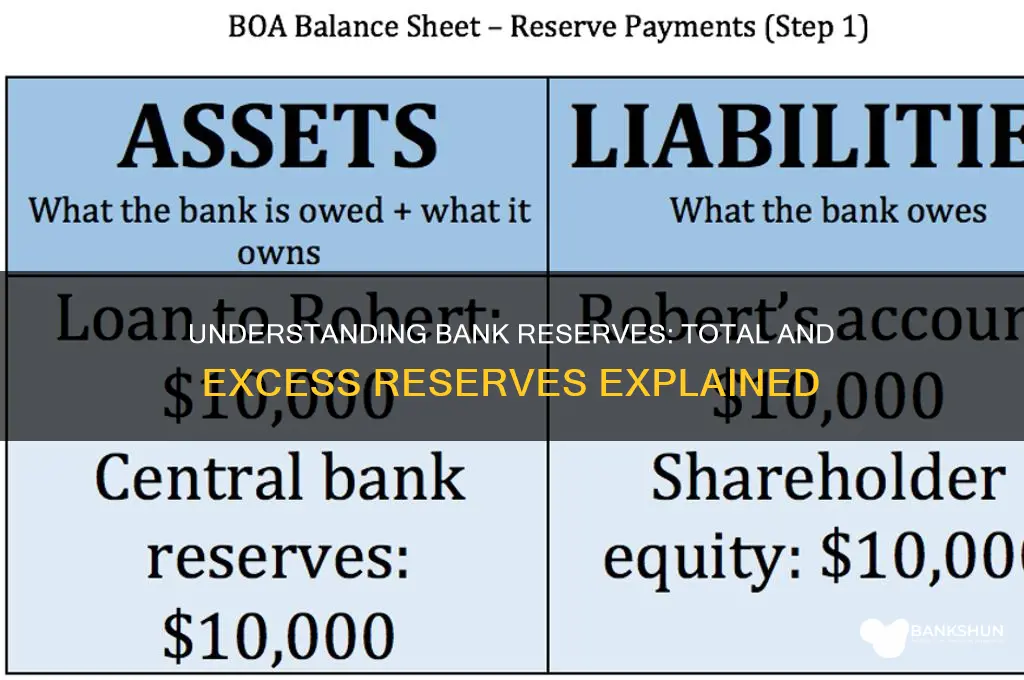

Banks' total reserves refer to the sum of cash held in their vaults and deposits maintained at the central bank, which are essential for meeting daily operational needs and regulatory requirements. Excess reserves, on the other hand, represent the amount of reserves held by banks beyond what is mandated by regulatory authorities. These excess reserves can be used for lending, investment, or as a buffer during financial stress, playing a critical role in influencing the money supply and credit availability within the economy. Understanding the distinction between total and excess reserves is crucial for assessing a bank's liquidity position and its potential impact on broader economic activity.

Explore related products

What You'll Learn

![]()

Definition of Total Reserves

Banks are required to hold a certain amount of funds in reserve to ensure they can meet their financial obligations and maintain stability. Total reserves refer to the sum of cash and other highly liquid assets that a bank keeps on hand, either in its vaults or on deposit with a central bank. This figure is a critical component of a bank's balance sheet and is closely monitored by regulators to ensure compliance with reserve requirements.

To understand the concept of total reserves, consider a bank's daily operations. As customers deposit and withdraw funds, the bank must maintain a buffer to cover these fluctuations. Total reserves serve as this buffer, providing a safety net to absorb unexpected shocks and ensure the bank can honor its commitments. For instance, if a bank has $100 million in deposits, it may be required to hold 10% of this amount, or $10 million, in total reserves. This percentage, known as the reserve ratio, is set by central banks and can vary depending on economic conditions and the bank's size.

The composition of total reserves is also essential. Typically, these reserves include physical currency, funds held in accounts with the central bank, and other highly liquid assets that can be quickly converted to cash. In the United States, for example, banks are required to hold reserves in the form of vault cash or deposits with the Federal Reserve. The European Central Bank (ECB) has similar requirements, with banks in the Eurozone holding reserves in their national central banks or the ECB itself. By diversifying the composition of total reserves, banks can minimize risk and ensure they have sufficient liquidity to meet their obligations.

One practical aspect of total reserves is their role in monetary policy. Central banks can influence the money supply and credit conditions by adjusting reserve requirements. For instance, if a central bank wants to stimulate economic growth, it may lower reserve requirements, freeing up funds for banks to lend to businesses and consumers. Conversely, if inflation is a concern, the central bank may increase reserve requirements, reducing the amount of funds available for lending and slowing economic activity. This delicate balance highlights the importance of total reserves in maintaining financial stability and achieving broader economic objectives.

In summary, total reserves are a vital component of a bank's operations, serving as a buffer to absorb fluctuations in deposits and withdrawals. By understanding the definition, composition, and role of total reserves, banks can effectively manage their liquidity and comply with regulatory requirements. As a critical tool for central banks in conducting monetary policy, total reserves play a significant role in shaping economic conditions and ensuring the stability of the financial system. By carefully managing their total reserves, banks can contribute to a more resilient and stable financial environment, benefiting both individual customers and the broader economy.

Ace Your Bank Teller Test: Essential Preparation Tips and Strategies

You may want to see also

Explore related products

![]()

Definition of Excess Reserves

Banks are required to hold a certain percentage of their deposits as reserves, a mandate set by central banking authorities to ensure financial stability and liquidity. Excess reserves refer to the amount of funds that banks hold in addition to these required reserves. This surplus is not mandated by law but is kept voluntarily, often as a buffer against unexpected withdrawals or economic downturns. For instance, if a bank has $100 million in deposits and is required to hold 10% as reserves ($10 million), any amount above this—say, $15 million—constitutes excess reserves.

Analytically, excess reserves serve as a critical indicator of a bank’s liquidity position and risk appetite. During periods of economic uncertainty, banks tend to increase their excess reserves to safeguard against potential shocks. Conversely, in stable or booming economies, banks may reduce excess reserves to deploy more capital into lending or investments, thereby maximizing profitability. Central banks, such as the Federal Reserve, closely monitor these levels to gauge the banking sector’s health and adjust monetary policies accordingly.

From a practical standpoint, managing excess reserves requires a delicate balance. Holding too much can limit a bank’s ability to generate revenue through loans or investments, while holding too little exposes it to liquidity risks. For example, during the 2008 financial crisis, excess reserves in the U.S. banking system surged as banks became risk-averse, leading the Federal Reserve to implement policies to encourage lending. This highlights the dual role of excess reserves: as both a safety net and a strategic tool.

Comparatively, excess reserves differ from required reserves in purpose and flexibility. While required reserves are a regulatory obligation, excess reserves are discretionary and reflect a bank’s individual risk management strategy. In countries with higher economic volatility, banks often maintain larger excess reserves compared to those in stable economies. For instance, banks in emerging markets may hold excess reserves equivalent to 5-10% of their deposits, whereas banks in developed economies might hold 1-3%.

In conclusion, excess reserves are a vital component of a bank’s financial strategy, offering both protection and opportunity. By understanding their definition and role, stakeholders—from bank managers to policymakers—can make informed decisions to navigate economic fluctuations effectively. Whether as a cushion against uncertainty or a lever for growth, excess reserves remain a cornerstone of modern banking.

The Banking Sector: Private or Public?

You may want to see also

Explore related products

![]()

Calculation of Required Reserves

Banks are required to hold a certain percentage of their deposits as reserves, a mandate set by central banking authorities to ensure financial stability. The calculation of required reserves is a critical component in understanding a bank's liquidity and its ability to lend. This process involves a straightforward formula: Required Reserves = Reserve Requirement Ratio × Total Deposits. For instance, if a bank has $100 million in deposits and the reserve requirement is 10%, the required reserves would be $10 million. This amount must be held either as cash in the bank’s vault or as a deposit at the central bank, ensuring the bank can meet withdrawal demands and maintain confidence in the financial system.

The reserve requirement ratio is not static; it varies by jurisdiction and can be adjusted by central banks to influence monetary policy. In the United States, for example, the Federal Reserve sets different reserve ratios for nonpersonal time deposits, Eurocurrency liabilities, and transaction accounts based on the bank’s net transaction accounts. Banks with higher transaction volumes typically face higher reserve requirements. Understanding these tiers is essential for accurate calculations, as missteps can lead to non-compliance penalties or inefficient capital allocation.

A practical example illustrates the calculation’s real-world application. Consider a small bank with $50 million in transaction accounts and a reserve requirement of 3%. The required reserves would be $1.5 million. If the bank holds $2 million in reserves, the excess reserves amount to $500,000, which can be lent out to generate interest income. This highlights the balance banks must strike between meeting regulatory obligations and maximizing profitability.

While the formula appears simple, banks must navigate complexities such as changes in deposit levels and regulatory updates. For instance, a sudden influx of deposits would increase required reserves, potentially reducing excess reserves available for lending. Banks often use reserve management strategies, such as forecasting deposit fluctuations and maintaining buffer reserves, to avoid liquidity shortfalls. Additionally, central banks may lower reserve requirements during economic downturns to encourage lending and stimulate growth, underscoring the dynamic nature of this calculation.

In conclusion, the calculation of required reserves is a foundational aspect of banking operations, blending regulatory compliance with strategic financial management. By accurately determining this figure, banks can ensure liquidity, optimize lending, and contribute to broader economic stability. Mastery of this calculation is not just a regulatory necessity but a key skill for effective bank management in a fluctuating financial landscape.

Exploring Bangor Savings Bank's Presence in Georgia: Fact or Fiction?

You may want to see also

Explore related products

$3.99

![]()

Factors Influencing Excess Reserves

Banks' excess reserves, the funds held beyond the required reserve ratio, are not merely a buffer but a dynamic component influenced by a myriad of factors. One of the primary drivers is monetary policy decisions by central banks. When central banks lower interest rates or engage in quantitative easing, banks are incentivized to lend more, potentially reducing excess reserves. Conversely, tighter monetary policies, such as higher interest rates, can lead banks to hold more excess reserves as a precautionary measure against liquidity shortages. For instance, during the 2008 financial crisis, the Federal Reserve's aggressive easing led to a surge in excess reserves as banks opted for safety over lending.

Another critical factor is economic uncertainty. During periods of economic instability, banks tend to hoard excess reserves to safeguard against potential loan defaults or market downturns. The COVID-19 pandemic exemplifies this behavior, as banks globally increased their excess reserves despite central banks' accommodative policies. This trend highlights how external economic shocks can override monetary policy incentives, emphasizing the role of risk perception in reserve management.

Regulatory requirements also play a pivotal role in shaping excess reserves. Post-2008, regulations like Basel III mandated higher capital and liquidity ratios, encouraging banks to maintain larger buffers. While these measures enhance financial stability, they can inadvertently inflate excess reserves, particularly in jurisdictions with stringent compliance frameworks. Banks in such regions often prioritize regulatory adherence over lending, even in favorable economic conditions.

Lastly, technological advancements and changes in payment systems are subtly influencing excess reserve levels. The rise of real-time payment systems reduces the float time for transactions, enabling banks to manage liquidity more efficiently. This efficiency can lower the need for excess reserves, as banks gain greater visibility into their cash flows. However, the adoption of such technologies varies widely across regions, creating disparities in reserve management practices.

In summary, excess reserves are not a static metric but a reflection of monetary policy, economic conditions, regulatory landscapes, and technological evolution. Understanding these factors provides insights into banks' liquidity management strategies and their broader implications for financial stability and credit availability.

Does Valentine's Day Hide a Secret Bank Heist Opportunity?

You may want to see also

Explore related products

$28.43 $42.99

![]()

Impact on Money Supply

Banks' total and excess reserves play a pivotal role in shaping the money supply within an economy. Total reserves refer to the sum of cash held in a bank’s vault and its deposits with the central bank, while excess reserves are the funds held above the required reserve ratio set by regulators. These reserves are not idle; they directly influence the money supply through the mechanism of fractional reserve banking. When banks hold more excess reserves, they lend less, which can contract the money supply. Conversely, when excess reserves are low, banks lend more, expanding the money supply through the multiplier effect.

Consider the multiplier effect as a practical example. If the required reserve ratio is 10%, a bank with $1 million in deposits must hold $100,000 in reserves and can lend out $900,000. This $900,000 becomes a deposit in another bank, which then lends out 90% of it, and so on. The total money supply increases by up to $10 million ($1 million / 0.10). However, if banks choose to hold excess reserves instead of lending, this multiplier effect is dampened. For instance, during the 2008 financial crisis, banks in the U.S. held trillions in excess reserves, significantly slowing money supply growth despite central bank efforts to stimulate lending.

Central banks, such as the Federal Reserve, use reserve management as a tool to control the money supply. By adjusting the required reserve ratio or paying interest on excess reserves (IOER), they can incentivize or disincentivize lending. For example, during periods of inflation, central banks may increase the reserve ratio to reduce lending and cool the economy. Conversely, during recessions, lowering the ratio or reducing IOER encourages banks to lend more, boosting the money supply. In 2020, the Fed lowered the reserve ratio to 0% to stimulate lending during the COVID-19 pandemic, demonstrating the direct link between reserves and money supply dynamics.

A critical takeaway is that excess reserves act as a buffer for banks but can also be a double-edged sword for monetary policy. While they enhance bank stability by providing liquidity during crises, excessive accumulation can hinder central bank efforts to expand the money supply. Policymakers must balance these trade-offs, often using complementary tools like open market operations or quantitative easing. For instance, the Fed’s quantitative easing programs post-2008 aimed to counteract the contractionary effect of high excess reserves by injecting liquidity directly into the financial system.

In practice, understanding the relationship between reserves and money supply is essential for investors, policymakers, and even consumers. For investors, monitoring excess reserve levels can provide insights into future lending trends and economic growth. Policymakers must carefully calibrate reserve requirements and interest rates to achieve desired monetary conditions. Consumers, though indirectly affected, benefit from a stable money supply that supports employment and price stability. By grasping this dynamic, stakeholders can better navigate the complexities of modern banking and monetary policy.

Peanut Butter and Sperm Health: Fact or Fiction for Fertility?

You may want to see also

Frequently asked questions

Bank total reserves refer to the sum of cash deposits held by a bank in its vault and the deposits it maintains with the central bank (e.g., the Federal Reserve in the U.S.). These reserves are required to meet depositors' demands and ensure liquidity.

Required reserves are the minimum amount of reserves a bank must hold, as mandated by the central bank, based on a percentage of its deposits. Excess reserves are the funds a bank holds above the required reserve amount, which can be used for lending or other purposes.

Banks hold excess reserves to manage liquidity, meet unexpected withdrawal demands, and take advantage of lending opportunities. Excess reserves also provide a buffer during economic uncertainty or financial stress.

Excess reserves can influence the money supply through the money multiplier effect. When banks lend out excess reserves, it increases the amount of money circulating in the economy. However, if banks choose to hold excess reserves instead of lending, it can limit money supply growth.