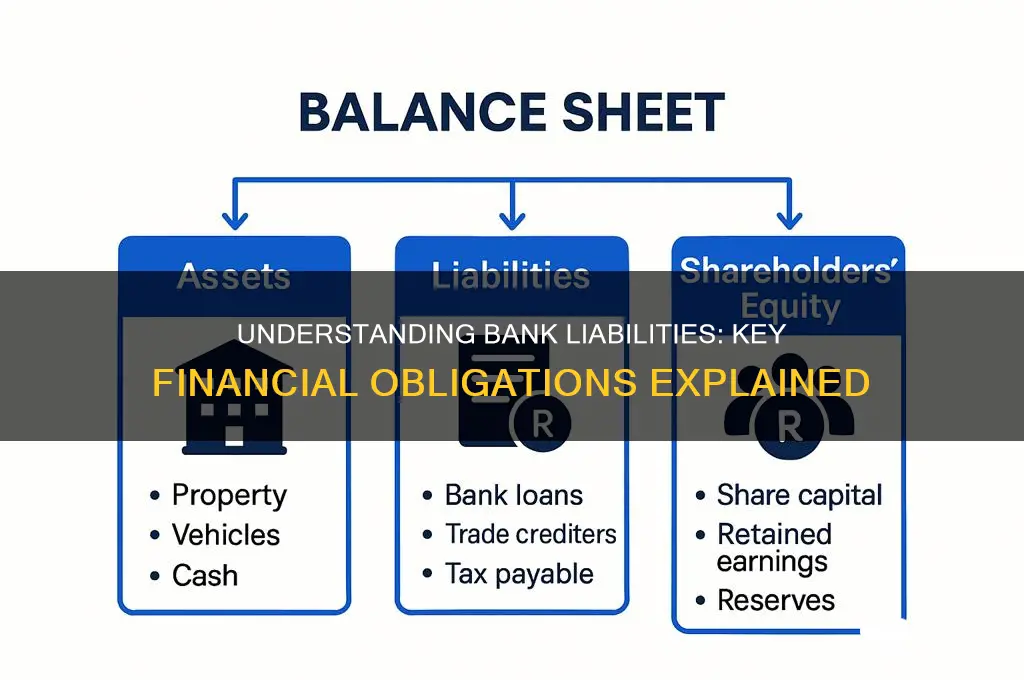

Liabilities for a bank represent the obligations or debts it owes to others, which are crucial for understanding its financial health and stability. These typically include customer deposits, such as checking and savings accounts, which are the primary source of funding for banks. Additionally, liabilities encompass borrowed funds from other financial institutions, outstanding loans from central banks, and bond issuances. Banks also account for accrued expenses, unpaid dividends, and derivative liabilities. Proper management of these liabilities is essential, as they directly impact liquidity, solvency, and the bank's ability to meet its short-term and long-term obligations.

| Characteristics | Values |

|---|---|

| Customer Deposits | Checking accounts, savings accounts, certificates of deposit (CDs), money market accounts |

| Borrowings | Short-term loans (e.g., repo agreements), long-term debt (e.g., bonds, subordinated debt), interbank loans |

| Accrued Expenses | Interest payable, salaries and wages payable, taxes payable, dividends payable |

| Deferred Revenue | Prepaid services, unearned income |

| Off-Balance Sheet Liabilities | Letters of credit, loan commitments, derivatives (e.g., interest rate swaps, options) |

| Subordinated Debt | Debt that ranks lower in priority for repayment in case of liquidation |

| Pension Obligations | Liabilities related to employee pension plans |

| Allowance for Loan Losses | Reserve set aside for potential loan defaults |

| Customer Advances | Funds provided to customers for specific purposes (e.g., overdrafts) |

| Other Payables | Miscellaneous liabilities like accounts payable, accrued interest, and other short-term obligations |

Explore related products

What You'll Learn

- Customer Deposits: Funds held by banks, owed to customers, and payable on demand or term

- Borrowed Funds: Money banks borrow from other institutions or central banks for liquidity

- Unpaid Loans: Outstanding loan amounts owed by borrowers to the bank

- Derivative Obligations: Financial contracts requiring banks to meet specific payment or delivery terms

- Accrued Expenses: Unpaid short-term obligations like wages, taxes, or interest expenses

![]()

Customer Deposits: Funds held by banks, owed to customers, and payable on demand or term

Customer deposits form the backbone of a bank's liability structure, representing the primary source of funds that banks use to fuel their operations. These deposits are essentially monies entrusted to banks by customers, with the understanding that the bank owes these funds back, either on demand or at a specified future date. This dynamic creates a unique relationship where the bank acts as both a custodian and a borrower, leveraging these liabilities to generate income through loans, investments, and other financial activities.

From a customer's perspective, deposits are a cornerstone of personal and business financial management. Demand deposits, such as checking accounts, offer immediate access to funds, making them ideal for everyday transactions. Term deposits, like certificates of deposit (CDs), lock funds away for a fixed period, often in exchange for higher interest rates. This duality allows customers to balance liquidity needs with the desire to earn returns, while banks benefit from a stable funding base. For instance, a small business might maintain a checking account for payroll and expenses, while simultaneously holding a CD to grow surplus cash.

Analyzing the risk profile of customer deposits reveals their dual nature as both a liability and a strategic asset for banks. On one hand, demand deposits pose liquidity risk, as customers can withdraw funds at any time, potentially straining the bank's cash reserves. On the other hand, term deposits provide predictable funding, but early withdrawal penalties and interest rate mismatches can introduce challenges. Banks mitigate these risks through careful liquidity management, such as maintaining reserves and diversifying funding sources. For example, a bank might hold 10% of its demand deposits in liquid assets to ensure it can meet withdrawal demands without disrupting operations.

Persuasively, banks must prioritize transparency and trust when managing customer deposits. Clear communication about terms, fees, and interest rates fosters customer confidence and reduces the likelihood of disputes. Additionally, offering competitive rates and flexible products can attract and retain depositors, strengthening the bank's financial position. A bank that consistently communicates changes in interest rates or introduces innovative deposit products, such as high-yield savings accounts, can differentiate itself in a crowded market.

In conclusion, customer deposits are a critical liability for banks, serving as both a funding source and a tool for customer engagement. By understanding the nuances of demand and term deposits, banks can optimize their balance sheets while meeting the diverse needs of their customers. Practical steps, such as maintaining adequate liquidity buffers and fostering transparency, ensure that this liability remains a stable foundation for growth. For customers, recognizing the trade-offs between liquidity and returns empowers them to make informed decisions, maximizing the value of their deposits.

Is Taiwan a Member of the World Bank? Exploring Its Status

You may want to see also

Explore related products

![]()

Borrowed Funds: Money banks borrow from other institutions or central banks for liquidity

Banks often turn to borrowed funds as a strategic tool to manage liquidity, ensuring they can meet withdrawal demands and fund lending activities. These funds, sourced from other financial institutions or central banks, are a critical component of a bank's liability structure. When a bank borrows, it gains immediate access to cash, but it also incurs an obligation to repay the principal plus interest, typically within a specified timeframe. This dynamic underscores the dual nature of borrowed funds: they provide essential liquidity but also introduce financial commitments that must be carefully managed.

Consider the mechanics of interbank lending, a common form of borrowed funds. Banks with surplus reserves lend to those facing temporary shortages, often through overnight or short-term loans. For instance, a regional bank might borrow $50 million from a larger institution at a rate of 2.5% for a 30-day term. This transaction allows the borrowing bank to maintain its reserve requirements while the lending bank earns a modest return on idle funds. Central banks also play a pivotal role by offering loans through mechanisms like the discount window, where banks can borrow at a higher rate, typically as a last resort. For example, during the 2008 financial crisis, many banks relied on central bank funding to avert liquidity crises.

The strategic use of borrowed funds requires precision. Banks must balance the cost of borrowing against the potential returns from lending or investment activities. A bank that borrows at 2.5% must ensure its lending portfolio yields a higher rate, say 5%, to generate a profit. However, this strategy carries risks. If market interest rates rise, the bank’s borrowing costs could increase, squeezing profit margins. Additionally, over-reliance on borrowed funds can signal financial instability, potentially eroding investor confidence.

To mitigate these risks, banks employ rigorous liquidity management frameworks. Stress testing, for example, helps assess a bank’s ability to withstand sudden funding shocks. Regulators also impose limits on borrowing levels relative to a bank’s capital base, ensuring institutions maintain a buffer against unexpected withdrawals. Practical tips for bankers include diversifying funding sources to reduce dependency on any single lender and maintaining a robust liquidity reserve to minimize the need for emergency borrowing.

In conclusion, borrowed funds are a double-edged sword in banking. They provide essential liquidity but demand disciplined management to avoid financial strain. By understanding the mechanics, costs, and risks associated with these liabilities, banks can leverage borrowed funds effectively, ensuring stability and profitability in an ever-changing financial landscape.

Bank Regulators: Fair Lending Supervision Inadequate?

You may want to see also

Explore related products

![]()

Unpaid Loans: Outstanding loan amounts owed by borrowers to the bank

Unpaid loans, or outstanding loan amounts owed by borrowers to the bank, represent a significant liability that directly impacts a bank's financial health and stability. These loans, often categorized as non-performing assets (NPAs), arise when borrowers fail to meet their repayment obligations, whether due to financial distress, mismanagement, or economic downturns. For banks, managing these liabilities is critical, as they tie up capital, reduce profitability, and increase risk exposure. Unlike other liabilities, such as customer deposits, which are predictable and interest-bearing, unpaid loans are unpredictable and erode the bank's asset quality over time.

Consider the lifecycle of an unpaid loan: it begins as a performing asset, generating interest income for the bank. However, once a borrower defaults, the loan transitions into a liability, requiring the bank to allocate provisions for potential losses. These provisions, mandated by regulatory bodies, reduce the bank's net income and weaken its balance sheet. For instance, if a bank has $10 million in unpaid loans, it might need to set aside 10-20% of that amount as provisions, depending on the loan's risk classification. This not only diminishes profits but also restricts the bank's ability to lend further, stifling growth.

From a strategic perspective, banks employ various tactics to mitigate the impact of unpaid loans. Debt restructuring, where repayment terms are modified to make them more manageable for the borrower, is one approach. Another is loan recovery through legal means, though this is often costly and time-consuming. Banks also invest in robust credit assessment frameworks to minimize the risk of defaults upfront. For example, leveraging advanced analytics and AI to evaluate borrower creditworthiness can reduce the likelihood of issuing loans to high-risk individuals or businesses.

A comparative analysis reveals that banks in emerging markets often face higher levels of unpaid loans due to less mature financial systems and greater economic volatility. In contrast, banks in developed economies benefit from stronger regulatory frameworks and more diversified loan portfolios, which help cushion the impact of defaults. For instance, during the 2008 financial crisis, U.S. banks with higher exposure to subprime mortgages experienced a sharp rise in unpaid loans, leading to widespread financial instability. This underscores the importance of diversification and risk management in banking operations.

In conclusion, unpaid loans are a critical liability for banks, demanding proactive management and strategic foresight. By understanding the lifecycle of these loans, implementing effective recovery mechanisms, and leveraging technology for better risk assessment, banks can minimize their exposure and safeguard their financial health. Borrowers, too, play a role by maintaining transparency and seeking assistance early when facing repayment challenges. Ultimately, addressing unpaid loans is not just about managing liabilities—it’s about fostering a resilient banking ecosystem that supports both lenders and borrowers alike.

Unlocking Academic Success: Strategies to Locate Your School Test Banks

You may want to see also

Explore related products

![]()

Derivative Obligations: Financial contracts requiring banks to meet specific payment or delivery terms

Derivative obligations stand as a cornerstone of modern banking, yet they are often misunderstood. These financial contracts bind banks to specific payment or delivery terms, contingent on underlying assets, interest rates, or market indices. Unlike traditional loans or deposits, derivatives introduce complexity through their sensitivity to market fluctuations, creating both opportunities and risks. For instance, a bank might enter a swap agreement to hedge against interest rate volatility, but if rates move unfavorably, the bank could face significant payout obligations, transforming the derivative into a liability.

Consider the mechanics of a common derivative: an interest rate swap. Here, a bank agrees to exchange fixed-rate payments for floating-rate payments with a counterparty. If interest rates rise sharply, the bank’s obligation to pay the fixed rate becomes costlier, while the floating rate it receives may not compensate adequately. This mismatch can erode profitability and strain liquidity, underscoring why derivatives are classified as contingent liabilities. Banks must meticulously manage these exposures through stress testing, collateral requirements, and hedging strategies to mitigate potential losses.

The regulatory landscape further complicates derivative obligations. Basel III and Dodd-Frank Act regulations mandate higher capital reserves for banks holding derivatives, reflecting their inherent risk. Additionally, central clearing requirements aim to reduce counterparty risk but increase operational complexity. Banks must navigate these rules while balancing the strategic use of derivatives for risk management and revenue generation. Failure to comply can result in penalties, reputational damage, and financial instability, amplifying the liability aspect of these contracts.

Practical management of derivative obligations requires a dual focus: robust risk assessment and transparent reporting. Banks should employ Value-at-Risk (VaR) models to quantify potential losses under adverse market conditions. Regular mark-to-market valuations ensure liabilities are accurately reflected on balance sheets. Moreover, educating stakeholders—from traders to board members—about derivative risks fosters a culture of accountability. By treating derivatives not as mere tools for profit but as dynamic liabilities, banks can safeguard their financial health and maintain trust in the broader financial system.

Spotting Unrecognized Bank Transactions: A Step-by-Step Guide to Protect Your Finances

You may want to see also

Explore related products

![]()

Accrued Expenses: Unpaid short-term obligations like wages, taxes, or interest expenses

Accrued expenses represent a critical subset of a bank's liabilities, embodying unpaid short-term obligations that have been incurred but not yet settled. These include wages owed to employees, taxes due to government entities, and interest expenses on deposits or loans. Unlike long-term debt, accrued expenses are immediate financial commitments that must be addressed within a short timeframe, typically within the same operating cycle. For banks, managing these obligations is essential to maintaining liquidity, regulatory compliance, and stakeholder trust. Failure to account for accrued expenses can distort financial statements, leading to misrepresentations of a bank's financial health.

Consider the example of employee wages. Banks operate with large workforces, and payroll expenses accrue daily as employees perform their duties. Even if payday is bi-weekly, the bank must recognize these wages as a liability in the period they are earned. Similarly, interest payable on customer deposits accrues daily, even if it is paid monthly. These obligations are recorded in the bank’s balance sheet under current liabilities, ensuring transparency and adherence to accounting principles like the matching concept, which pairs expenses with the revenues they help generate.

From a practical standpoint, banks must implement robust accounting systems to track accrued expenses accurately. This involves estimating the amounts owed and ensuring they are recorded in the correct accounting period. For instance, if a bank owes $500,000 in wages for the last week of December but pays it in January, the expense must still be recognized in December’s financial statements. Failure to do so could inflate profits artificially and mislead investors or regulators. Tools like accrual journals and automated accounting software can streamline this process, reducing the risk of errors.

The strategic importance of managing accrued expenses extends beyond compliance. Banks with efficient accrual management can better forecast cash flows, allocate resources effectively, and avoid liquidity crunches. For example, a bank that underestimates its tax liabilities may face penalties or reputational damage when unable to meet obligations. Conversely, overestimating expenses ties up capital unnecessarily, limiting investment opportunities. Striking this balance requires a combination of meticulous record-keeping, forward-looking analysis, and a deep understanding of operational rhythms.

In conclusion, accrued expenses are a dynamic and indispensable component of a bank’s liability structure. They reflect the day-to-day operations of the institution, from compensating employees to honoring depositors’ interest. By treating these obligations with the attention they deserve, banks not only uphold financial integrity but also position themselves for sustainable growth. For financial professionals, mastering the nuances of accrued expenses is not just an accounting task—it’s a cornerstone of strategic financial management.

Effortlessly Update Your Information with USAA Bank: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Liabilities for a bank include customer deposits (such as savings, checking, and time deposits), borrowed funds from other banks or financial institutions, and obligations like certificates of deposit (CDs) and bonds payable.

Customer deposits are classified as liabilities because the bank owes the deposited funds to the account holders and must be prepared to return them upon demand or at maturity, depending on the type of deposit.

No, loans given by a bank are considered assets because they represent money owed to the bank by borrowers. Liabilities, on the other hand, are obligations the bank owes to others.