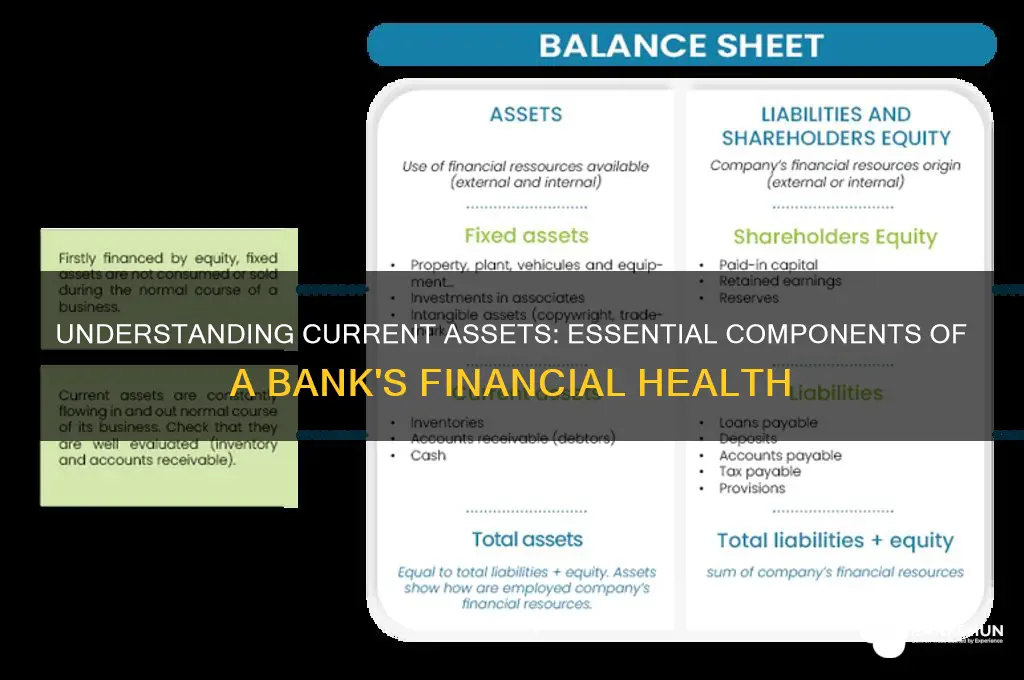

Current assets for a bank are short-term assets that are expected to be converted into cash or used up within one year or one operating cycle, whichever is longer. These assets are crucial for a bank's liquidity and operational efficiency, ensuring it can meet its immediate financial obligations and support day-to-day operations. Key examples of current assets for banks include cash and cash equivalents, such as currency, coins, and funds in checking accounts; short-term investments like treasury bills and certificates of deposit; accounts receivable from loans and overdrafts; and any inventory or supplies held for operational purposes. Understanding and effectively managing these assets is essential for maintaining a bank's financial health and stability.

Explore related products

What You'll Learn

- Cash and Equivalents: Includes physical currency, deposits, and highly liquid assets quickly convertible to cash

- Loans and Advances: Funds lent to customers, expected to be repaid within a short period

- Marketable Securities: Easily tradable financial instruments like bonds or stocks held for liquidity

- Accounts Receivable: Short-term amounts owed to the bank by borrowers or clients

- Inventory: Assets held for sale or use in banking operations, like foreclosed properties

![]()

Cash and Equivalents: Includes physical currency, deposits, and highly liquid assets quickly convertible to cash

Banks thrive on liquidity, and at the heart of this liquidity lies cash and equivalents. This category isn’t just about physical banknotes in vaults; it’s a dynamic pool encompassing deposits, treasury bills, and other assets that can be converted to cash within days or weeks. Think of it as a bank’s emergency fund, ensuring it can meet withdrawal demands, settle obligations, and seize opportunities without disruption.

Consider the composition: physical currency is the most tangible form, but it’s often a smaller portion of the total. Demand deposits (checking accounts) are a cornerstone, offering immediate access to funds for customers while providing banks with a source of short-term liquidity. Highly liquid assets like treasury bills, certificates of deposit, and money market instruments round out the category, offering slightly higher returns than cash while maintaining near-instant convertibility.

The strategic importance of cash and equivalents cannot be overstated. During economic downturns or sudden liquidity crunches, this buffer acts as a lifeline. For instance, during the 2008 financial crisis, banks with robust cash and equivalents were better positioned to weather the storm. Conversely, over-reliance on illiquid assets can lead to solvency issues, as seen in the collapse of several institutions during that period.

Managing this asset class requires precision. Banks must balance the need for liquidity with the desire for yield. Holding too much cash can erode profitability, while holding too little risks insolvency. Regulatory bodies like the Basel Committee impose liquidity coverage ratios (LCRs) to ensure banks maintain sufficient high-quality liquid assets to cover 30 days of net cash outflows under stress scenarios.

For individuals, understanding a bank’s cash and equivalents provides insight into its financial health. A higher proportion suggests stability but may indicate missed investment opportunities. Conversely, a lower proportion could signal efficiency or, if too low, vulnerability. Investors and customers alike should scrutinize this metric in financial statements to gauge a bank’s resilience and risk appetite.

Is Robbing a Bank Illegal? Understanding the Legal Consequences

You may want to see also

Explore related products

![]()

Loans and Advances: Funds lent to customers, expected to be repaid within a short period

Banks thrive on the delicate balance of liquidity and profitability. A critical component of this equilibrium lies in their current assets, particularly loans and advances. These represent funds disbursed to customers with the expectation of repayment within a short timeframe, typically one year or less. This category encompasses a diverse range of lending products, from overdraft facilities and credit cards to short-term business loans and personal lines of credit.

Unlike long-term loans, which are classified as non-current assets, loans and advances are considered current due to their imminent repayment horizon. This classification reflects their role in a bank's day-to-day operations, providing a readily accessible source of liquidity.

The allure of loans and advances for banks lies in their ability to generate interest income, a primary driver of profitability. By carefully assessing creditworthiness and setting appropriate interest rates, banks can effectively manage risk while maximizing returns. However, this pursuit of profit must be balanced with prudent risk management. Default rates, economic downturns, and unforeseen circumstances can all impact repayment, potentially leading to loan losses and eroding a bank's financial health.

Consequently, banks employ rigorous underwriting standards, credit scoring models, and ongoing portfolio monitoring to mitigate these risks.

The composition of a bank's loan and advances portfolio provides valuable insights into its strategic focus and risk appetite. A high proportion of short-term business loans might indicate a focus on supporting local enterprises, while a significant share of personal loans could suggest a consumer-centric approach. Analyzing the distribution across industries, loan sizes, and borrower demographics allows stakeholders to gauge the bank's exposure to specific sectors and economic cycles.

Understanding the nuances of loans and advances is crucial for investors, regulators, and even customers. Investors scrutinize this asset class to assess a bank's profitability, risk profile, and overall financial stability. Regulators monitor loan quality and provisioning practices to ensure the safety and soundness of the banking system. Meanwhile, customers benefit from the availability of diverse loan products tailored to their short-term financing needs, whether it's bridging a temporary cash flow gap or funding a small business venture.

Step-by-Step Guide: Applying for Food Bank Assistance Made Easy

You may want to see also

Explore related products

![]()

Marketable Securities: Easily tradable financial instruments like bonds or stocks held for liquidity

Banks, like any business, rely on a healthy mix of assets to ensure stability and growth. Among these, marketable securities stand out for their dual role: generating returns and providing readily accessible liquidity. These are financial instruments—think government bonds, corporate stocks, or treasury bills—that can be quickly converted to cash with minimal impact on their market price. This liquidity is crucial for banks to meet short-term obligations, such as customer withdrawals or regulatory requirements, without disrupting their core operations.

Consider the strategic advantage of holding marketable securities. Unlike long-term investments, which tie up capital for years, these assets offer banks the flexibility to respond to market opportunities or unforeseen challenges. For instance, a bank might sell a portion of its treasury bond holdings to capitalize on a sudden rise in interest rates or to shore up reserves during an economic downturn. This agility is a cornerstone of effective risk management in the banking sector.

However, not all marketable securities are created equal. Banks must carefully assess factors like credit risk, maturity, and market volatility when building their portfolio. For example, while corporate bonds may offer higher yields, they carry greater risk compared to government-backed securities. Similarly, stocks, though potentially more lucrative, are subject to market fluctuations that could erode their value. Striking the right balance requires a nuanced understanding of both financial markets and the bank’s risk appetite.

Practical considerations also come into play. Banks must ensure their marketable securities align with regulatory guidelines, such as liquidity coverage ratios (LCR) mandated by Basel III. These rules dictate that a certain percentage of a bank’s assets must be held in high-quality liquid assets (HQLA), including marketable securities. Compliance not only avoids penalties but also reinforces the bank’s credibility with investors and customers alike.

In essence, marketable securities are more than just a line item on a bank’s balance sheet—they are a strategic tool for managing liquidity, mitigating risk, and optimizing returns. By carefully selecting and managing these assets, banks can navigate the complexities of the financial landscape while safeguarding their stability and growth.

Mastering the Art of Securing Your Dream Bank Teller Position

You may want to see also

Explore related products

![]()

Accounts Receivable: Short-term amounts owed to the bank by borrowers or clients

Accounts receivable represent a critical component of a bank's current assets, reflecting short-term amounts owed by borrowers or clients for services rendered or loans disbursed. These balances are typically expected to be settled within one year, making them a liquid asset that contributes to the bank's operational cash flow. Unlike long-term loans, accounts receivable are more immediate in nature, often arising from credit card balances, short-term loans, or fees for banking services. For instance, if a client uses a credit card for a purchase, the outstanding amount becomes part of the bank's accounts receivable until the client repays it.

Analyzing accounts receivable requires a focus on aging and risk management. Banks categorize these receivables based on how long they have been outstanding—typically 30, 60, or 90 days. A high percentage of receivables in the 90-day category may indicate potential credit risk or collection inefficiencies. For example, a bank might set a threshold where 10% of receivables older than 90 days triggers a review of collection strategies or credit policies. Tools like aging reports and credit scoring models help banks monitor these balances proactively, ensuring they remain a reliable source of liquidity.

From a strategic perspective, accounts receivable are not just a passive asset but an active management area. Banks employ tactics such as offering early payment discounts or automating reminders to accelerate collections. For instance, a 2% discount for payments made within 10 days of invoicing can incentivize clients to settle sooner, improving cash flow. Additionally, banks may use technology like AI-driven analytics to predict which clients are likely to delay payments, allowing for targeted interventions. These measures not only reduce risk but also enhance the overall efficiency of the bank's asset portfolio.

Comparatively, accounts receivable differ from other current assets like cash or marketable securities in their inherent risk and management complexity. While cash is immediately available, receivables depend on the borrower’s ability and willingness to pay. This distinction underscores the need for robust credit assessment and collection processes. For example, a bank might require collateral for short-term loans to mitigate the risk of non-payment, ensuring receivables remain a secure asset class. Such practices highlight the balance banks must strike between extending credit and safeguarding liquidity.

In conclusion, accounts receivable are a dynamic and essential element of a bank's current assets, demanding careful management to maximize their value. By understanding their nature, monitoring aging trends, and implementing strategic collection practices, banks can ensure these short-term balances contribute positively to their financial health. Whether through technological innovation or policy adjustments, effective receivables management is key to maintaining liquidity and minimizing risk in an ever-evolving banking landscape.

Ulster Bank Closure in Northern Ireland: What You Need to Know

You may want to see also

Explore related products

$59.95 $49.95

![]()

Inventory: Assets held for sale or use in banking operations, like foreclosed properties

Banks often find themselves in possession of unique assets that don't fit the traditional mold of cash, loans, or securities. One such category is inventory, which in the banking context refers to assets held for sale or use in their operations. A prime example of this is foreclosed properties. When borrowers default on their mortgages, banks take ownership of the underlying real estate, turning it into an asset on their balance sheet.

These properties are considered inventory because they are intended for sale, not long-term investment. Banks aim to recoup as much of the outstanding loan balance as possible by selling the property, often at a discounted price to expedite the process. This strategy helps minimize losses and free up capital for other lending activities. However, managing foreclosed properties comes with challenges, such as maintenance costs, property taxes, and the potential for depreciation if the real estate market declines.

From an operational standpoint, banks must carefully assess the value of these assets and account for them appropriately. This involves regular appraisals to ensure the properties are priced competitively and accurately reflected on financial statements. Additionally, banks may need to allocate resources for upkeep, security, and legal compliance, which can impact their overall profitability. Effective management of this inventory is crucial, as prolonged holding periods can strain liquidity and reduce returns.

A comparative analysis reveals that while traditional inventory (e.g., goods in retail) is typically held for a short period, bank inventory like foreclosed properties can remain on the books for months or even years. This extended timeline underscores the importance of strategic planning and market analysis to optimize sales. Banks often collaborate with real estate agents or auction platforms to streamline the disposal process, balancing speed and profitability.

In conclusion, inventory in banking, particularly foreclosed properties, represents a distinct asset class that requires specialized management. By understanding its unique challenges and implementing proactive strategies, banks can mitigate risks and maximize recovery. This approach not only safeguards financial health but also ensures compliance with regulatory standards, reinforcing trust in the banking system.

Mastering Banking Arrays in C Programming: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Current assets for a bank are short-term assets that are expected to be converted into cash or used up within one year or one operating cycle, whichever is longer. These assets are crucial for a bank's liquidity and day-to-day operations.

Examples of current assets for a bank include cash and cash equivalents, short-term investments, accounts receivable, loans due within one year, and marketable securities.

Current assets are important for a bank because they ensure liquidity, enable the bank to meet short-term obligations, and support daily operations such as lending, withdrawals, and settlements.

Banks manage their current assets by maintaining a balance between liquidity and profitability, monitoring cash flow, investing in short-term securities, and ensuring sufficient reserves to meet customer demands and regulatory requirements.