Key Performance Indicators (KPIs) for banks are critical metrics used to evaluate their financial health, operational efficiency, and overall performance. These indicators encompass a range of financial and non-financial measures, including profitability ratios like Return on Assets (ROA) and Return on Equity (ROE), asset quality metrics such as Non-Performing Loan (NPL) ratios, liquidity measures like the Loan-to-Deposit Ratio (LDR), and efficiency ratios such as Cost-to-Income (CIR). Additionally, KPIs may include customer-centric metrics like Net Promoter Score (NPS) and digital adoption rates, as well as risk management indicators such as capital adequacy ratios. Together, these KPIs provide stakeholders with a comprehensive view of a bank’s ability to generate sustainable returns, manage risks, and deliver value to customers and shareholders.

Explore related products

What You'll Learn

- Asset Quality Metrics: Measures like non-performing loans ratio assess credit risk and portfolio health

- Capital Adequacy Ratios: Ensures banks maintain sufficient capital to cover risks and losses

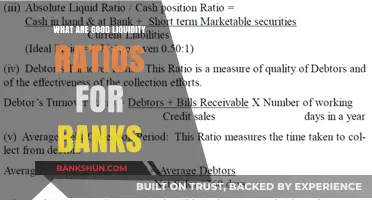

- Liquidity Ratios: Tracks ability to meet short-term obligations, e.g., current ratio, LCR

- Profitability Indicators: Includes net interest margin, ROA, and ROE to gauge earnings efficiency

- Operational Efficiency: Cost-to-income ratio measures expense management and operational productivity

![]()

Asset Quality Metrics: Measures like non-performing loans ratio assess credit risk and portfolio health

Banks rely heavily on asset quality metrics to gauge the health of their loan portfolios and overall financial stability. One critical measure is the non-performing loans (NPL) ratio, which quantifies the percentage of loans in default or nearing default relative to total loans. A high NPL ratio signals elevated credit risk, potential liquidity issues, and weakened profitability. For instance, during the 2008 financial crisis, banks with NPL ratios exceeding 5% faced severe capital erosion and regulatory scrutiny. Monitoring this metric allows banks to identify deteriorating asset quality early, enabling proactive risk mitigation strategies such as loan restructuring or increased provisioning.

Beyond the NPL ratio, banks employ additional asset quality metrics to provide a comprehensive view of portfolio health. The loan-to-value (LTV) ratio, for example, assesses the collateral coverage of loans, with higher ratios indicating greater risk in case of borrower default. Similarly, the net charge-off rate measures the percentage of loans written off as uncollectible, directly impacting profitability. These metrics, when analyzed collectively, offer a nuanced understanding of credit risk exposure. For instance, a bank with a low NPL ratio but high LTV ratios in its mortgage portfolio may still face significant risks during economic downturns.

Implementing asset quality metrics requires a structured approach. Banks should segment their loan portfolios by product type, borrower demographics, and geographic location to identify risk concentrations. Regular stress testing, simulating adverse economic scenarios, helps assess resilience. For example, a bank might model the impact of a 10% unemployment rate on its consumer loan portfolio to gauge potential NPL increases. Additionally, integrating these metrics into management dashboards ensures real-time visibility, enabling swift decision-making.

While asset quality metrics are indispensable, they are not without limitations. Over-reliance on historical data can lead to blind spots, particularly in rapidly changing economic conditions. For instance, the COVID-19 pandemic exposed vulnerabilities in sectors like hospitality and aviation, which traditional metrics failed to predict. Banks must complement quantitative measures with qualitative assessments, such as borrower behavior trends and industry outlooks. Furthermore, benchmarking against peers provides context, though caution is needed to avoid misalignment with unique business models or risk appetites.

In conclusion, asset quality metrics serve as a cornerstone of bank performance management, offering critical insights into credit risk and portfolio health. By leveraging measures like the NPL ratio, LTV ratio, and net charge-off rate, banks can proactively manage risks and safeguard financial stability. However, success hinges on a balanced approach—combining robust data analysis with qualitative judgment and continuous monitoring. As economic landscapes evolve, so too must the tools and strategies banks employ to assess and protect their most valuable assets.

Steps to Launch Your Career as an Eye Bank Technician

You may want to see also

Explore related products

![]()

Capital Adequacy Ratios: Ensures banks maintain sufficient capital to cover risks and losses

Capital Adequacy Ratios (CAR) are a cornerstone of banking regulation, designed to ensure that financial institutions maintain a buffer of capital sufficient to absorb losses and protect depositors. At its core, CAR measures a bank’s available capital relative to its risk-weighted assets, expressed as a percentage. Regulatory bodies, such as the Basel Committee on Banking Supervision, mandate a minimum CAR of 8%, though many banks aim higher to demonstrate financial resilience. This ratio is not just a compliance metric; it’s a critical indicator of a bank’s ability to withstand economic shocks, from market volatility to loan defaults.

To calculate CAR, banks categorize assets based on risk—loans, investments, and other exposures are weighted accordingly. For instance, government bonds might carry a 0% risk weight, while unsecured personal loans could be weighted at 100%. The bank’s Tier 1 and Tier 2 capital (core equity and supplementary capital, respectively) are then divided by these risk-weighted assets. A higher CAR indicates greater stability, while a ratio below the threshold triggers regulatory intervention, such as restricting dividends or mandating capital raises.

Consider a mid-sized bank with $10 billion in Tier 1 capital and $50 billion in risk-weighted assets. Its CAR would be 20% ($10B / $50B), well above the regulatory minimum. However, if the bank’s asset quality deteriorates—say, due to rising non-performing loans—its risk-weighted assets could increase, lowering the CAR. This scenario underscores the dynamic nature of CAR and its sensitivity to asset quality, making it a real-time gauge of financial health.

Banks must balance the need for a robust CAR with the pressure to deploy capital for growth. Holding excess capital improves safety but may limit profitability, as unused funds generate no returns. Conversely, operating near the minimum threshold maximizes leverage but increases vulnerability to losses. Strategic capital management, therefore, involves forecasting risk, diversifying assets, and maintaining a buffer above regulatory requirements. For example, during economic downturns, banks with higher CARs are better positioned to extend credit, supporting both their customers and the broader economy.

In practice, investors and regulators scrutinize CAR as a key performance indicator. A declining ratio may signal deteriorating asset quality or aggressive risk-taking, while a consistently high CAR can enhance a bank’s credit rating and reduce funding costs. For stakeholders, understanding CAR provides insight into a bank’s risk appetite, management discipline, and long-term sustainability. By ensuring banks maintain sufficient capital, CAR not only safeguards individual institutions but also fortifies the stability of the entire financial system.

Sustaining Biodiversity: The Innovative Power Behind Global Seed Banks

You may want to see also

Explore related products

![]()

Liquidity Ratios: Tracks ability to meet short-term obligations, e.g., current ratio, LCR

Liquidity ratios are the financial pulse check every bank relies on to ensure it can honor its commitments without breaking a sweat. Among these, the Current Ratio (current assets divided by current liabilities) offers a quick snapshot of short-term solvency. A ratio above 1 signals a bank can cover its near-term debts, but anything below 1 raises red flags. However, this metric isn’t foolproof—it doesn’t account for asset liquidity. For instance, a bank with a high current ratio might still struggle if its assets are tied up in illiquid investments like long-term loans.

Enter the Liquidity Coverage Ratio (LCR), a more robust measure introduced post-2008 to stress-test a bank’s ability to survive a 30-day liquidity crunch. The LCR mandates that high-quality liquid assets (HQLA), such as cash and government bonds, cover 100% of net cash outflows during this period. Banks must maintain an LCR of at least 1, but many aim higher to buffer against unforeseen shocks. For example, during the 2020 pandemic, banks with LCRs above 1.2 were better equipped to handle sudden deposit withdrawals and market volatility.

While both ratios are critical, they serve different purposes. The current ratio is a broad, high-level indicator, whereas the LCR is a granular, regulatory-driven metric. A bank might have a healthy current ratio but fail to meet LCR requirements if its liquid assets are insufficient or poorly diversified. Conversely, a bank with a stellar LCR might still face challenges if its overall asset-liability management is misaligned.

To optimize liquidity ratios, banks should adopt a dual strategy. First, diversify liquid assets—rely not just on cash but also on easily tradable securities like Treasury bills. Second, stress-test regularly to simulate extreme scenarios, ensuring the bank can withstand shocks like a run on deposits or a freeze in interbank lending. For instance, a quarterly stress test that models a 20% outflow in deposits can reveal gaps in liquidity planning.

In practice, striking the right balance between liquidity and profitability is key. Holding too many liquid assets can drag down returns, while holding too few risks insolvency. A pragmatic approach is to benchmark against peers and regulatory standards while tailoring strategies to the bank’s risk appetite and business model. For smaller banks, maintaining an LCR of 1.1–1.3 might suffice, while larger, systemically important banks should aim for 1.5 or higher to account for their interconnectedness. Ultimately, liquidity ratios aren’t just numbers—they’re a lifeline, ensuring banks remain resilient in the face of uncertainty.

Uploading Test Banks into Canvas: A Step-by-Step Guide for Educators

You may want to see also

Explore related products

$28.43 $42.99

![]()

Profitability Indicators: Includes net interest margin, ROA, and ROE to gauge earnings efficiency

Banks live and die by their ability to generate profit, and profitability indicators are the vital signs that reveal their financial health. Among these, net interest margin (NIM), return on assets (ROA), and return on equity (ROE) stand out as the triumvirate of metrics that gauge earnings efficiency. NIM measures the difference between interest income generated and interest paid out relative to the average earning assets, offering a snapshot of how effectively a bank leverages its core lending and deposit-taking functions. A healthy NIM typically ranges between 2% and 5%, though this varies by market conditions and business model. For instance, a bank with a NIM of 3.5% is generally considered more efficient than one at 2.5%, assuming similar risk profiles.

While NIM focuses on interest-related income, ROA and ROE provide broader perspectives on profitability. ROA calculates how efficiently a bank uses its total assets to generate earnings, expressed as a percentage. A ROA of 1% or higher is often seen as satisfactory, indicating that the bank is generating at least $1 in profit for every $100 in assets. However, this metric must be interpreted cautiously, as high ROA can sometimes mask excessive risk-taking or underutilized assets. For example, a bank with a ROA of 1.5% might appear strong, but if it’s achieved through high-risk loans, sustainability becomes questionable.

ROE, on the other hand, measures profitability relative to shareholders’ equity, revealing how effectively a bank uses investor capital to produce profits. A ROE of 10% to 15% is generally viewed as robust, though this varies by industry benchmarks and economic cycles. For instance, a bank with a ROE of 12% is often seen as more attractive to investors than one at 8%, as it demonstrates superior returns on invested capital. However, an excessively high ROE can signal over-leverage or aggressive profit-taking at the expense of long-term stability.

To illustrate, consider a mid-sized bank with a NIM of 3.2%, ROA of 1.2%, and ROE of 11%. These figures suggest strong earnings efficiency, with balanced performance across interest income, asset utilization, and equity returns. However, if the same bank reported a NIM of 4%, ROA of 1.8%, and ROE of 18%, it might raise red flags about unsustainable practices or excessive risk. The key is to analyze these indicators collectively, not in isolation, to paint a comprehensive picture of profitability.

In practice, banks should monitor these metrics quarterly, benchmarking against industry averages and historical performance. For instance, a sudden drop in NIM could indicate rising funding costs or declining loan yields, warranting immediate action. Similarly, a consistent decline in ROA or ROE might signal operational inefficiencies or strategic missteps. By tracking these indicators rigorously and responding proactively, banks can optimize earnings efficiency, ensuring long-term profitability and stakeholder confidence.

Calculating EBITDA for Banks: A Comprehensive Step-by-Step Guide

You may want to see also

Explore related products

$54.78 $95

![]()

Operational Efficiency: Cost-to-income ratio measures expense management and operational productivity

Banks striving for operational excellence obsess over the cost-to-income ratio, a metric that lays bare the efficiency of their operations. This ratio, calculated by dividing operating expenses by operating income, reveals how much a bank spends to generate each dollar of revenue. A lower ratio signifies a leaner, more efficient operation, while a higher one suggests bloated costs eating into profitability.

Imagine two banks with identical revenue. Bank A boasts a cost-to-income ratio of 40%, while Bank B struggles with 60%. This 20% difference translates to Bank A having significantly more funds available for growth initiatives, loan provisions, or shareholder returns.

Achieving a healthy cost-to-income ratio isn't merely about slashing expenses. It's a delicate balancing act. Banks must strategically invest in technology to automate processes, streamline workflows, and enhance customer experience. For instance, implementing robust digital banking platforms can reduce reliance on physical branches and their associated costs. However, these investments themselves come with upfront costs, requiring careful planning and prioritization.

Banks must also scrutinize their operational processes, identifying redundant steps, manual interventions, and areas prone to errors. Lean Six Sigma methodologies can be invaluable tools for eliminating waste and optimizing workflows, directly contributing to a lower cost-to-income ratio.

The pursuit of operational efficiency through cost-to-income ratio management is a continuous journey, not a destination. Banks must constantly benchmark themselves against industry peers, analyze trends, and adapt their strategies to evolving market conditions and customer expectations. Regular reviews of expense categories, coupled with a data-driven approach to decision-making, are essential for sustained improvement.

Ultimately, a well-managed cost-to-income ratio is a powerful indicator of a bank's financial health and its ability to compete in a dynamic marketplace. It reflects not just cost control, but a commitment to operational excellence, innovation, and delivering value to customers and shareholders alike.

How to Safely Unlink Your Bank Account from Apple Pay

You may want to see also

Frequently asked questions

Key Performance Indicators (KPIs) for banks are measurable metrics used to evaluate the financial health, operational efficiency, and overall performance of a bank. They help stakeholders assess how well the bank is achieving its strategic and operational goals.

KPIs are crucial for banks as they provide insights into profitability, risk management, customer satisfaction, and operational efficiency. They enable banks to make data-driven decisions, identify areas for improvement, and ensure compliance with regulatory standards.

Common financial KPIs for banks include Return on Assets (ROA), Return on Equity (ROE), Net Interest Margin (NIM), Cost-to-Income Ratio, and Non-Performing Loan (NPL) Ratio. These metrics help assess profitability, efficiency, and asset quality.

Banks often measure customer satisfaction through KPIs such as Net Promoter Score (NPS), Customer Satisfaction Score (CSAT), customer retention rate, and the number of customer complaints. These metrics reflect the quality of service and customer loyalty.

Risk-related KPIs, such as Capital Adequacy Ratio (CAR), Loan-to-Deposit Ratio, and Liquidity Coverage Ratio (LCR), help banks monitor and manage financial risks. They ensure the bank maintains sufficient capital and liquidity to withstand adverse conditions.