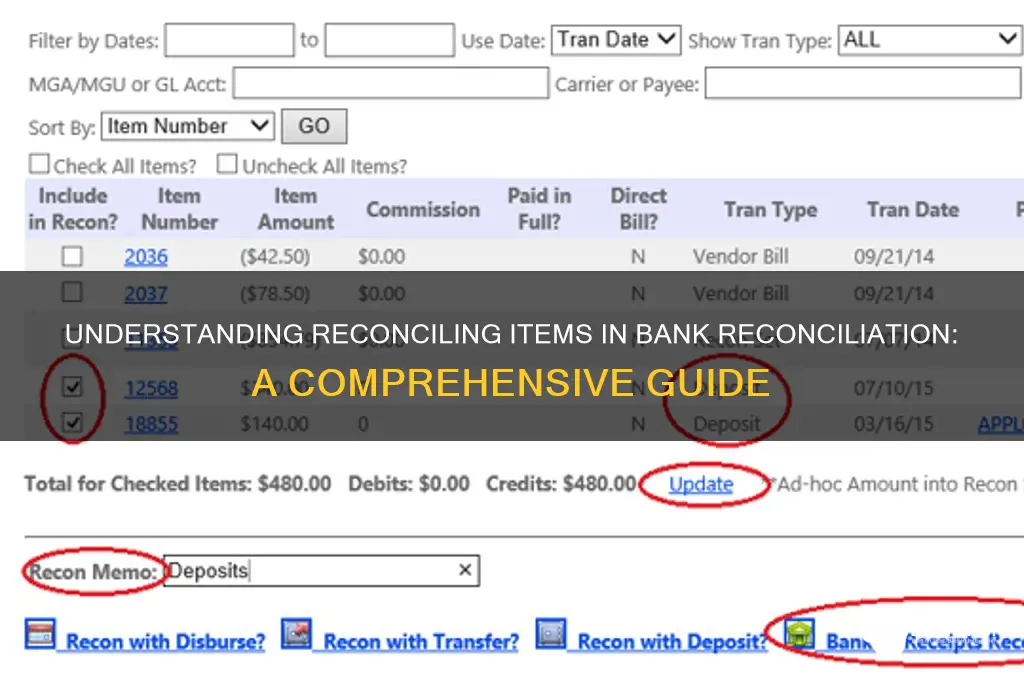

Bank reconciliation is a critical process for ensuring the accuracy of a company's financial records by comparing the internal accounting records with the bank statement. Reconciling items play a pivotal role in this process, as they represent discrepancies or differences between the two sets of records. These items can include outstanding checks, deposits in transit, bank service charges, interest income, or errors in recording transactions. Identifying and adjusting for these reconciling items is essential to align the company's books with the bank's records, providing a clear and accurate picture of the organization's financial health. Understanding and properly managing these items helps maintain transparency, detect errors, and prevent financial discrepancies.

| Characteristics | Values |

|---|---|

| Definition | Items that cause discrepancies between the company's bank statement and its internal records during bank reconciliation. |

| Types | Unrecorded Deposits, Unrecorded Payments, Bank Errors, Company Errors, Timing Differences. |

| Unrecorded Deposits | Deposits made by the company but not yet recorded by the bank. |

| Unrecorded Payments | Payments made by the bank (e.g., checks, fees) but not yet recorded by the company. |

| Bank Errors | Mistakes made by the bank, such as incorrect amounts or duplicate entries. |

| Company Errors | Mistakes made by the company, such as incorrect recording of transactions. |

| Timing Differences | Transactions recorded in different periods by the company and the bank due to processing delays. |

| Purpose | To identify and correct discrepancies, ensuring accuracy in financial records. |

| Frequency | Typically performed monthly, quarterly, or annually, depending on business needs. |

| Documentation | Requires bank statements, company ledger, and supporting documents for reconciliation. |

| Outcome | Adjusted bank balance matches the company's internal records after reconciling items are addressed. |

| Importance | Ensures financial accuracy, detects fraud, and maintains compliance with accounting standards. |

Explore related products

What You'll Learn

- Outstanding Checks: Uncashed checks issued but not yet processed by the bank

- Deposits in Transit: Funds deposited but not yet credited by the bank

- Bank Errors: Mistakes made by the bank affecting account balances

- Interest Income: Interest earned and credited by the bank

- Service Charges: Fees deducted by the bank for account services

![]()

Outstanding Checks: Uncashed checks issued but not yet processed by the bank

Outstanding checks represent a common reconciling item in bank reconciliation, yet their impact on financial accuracy is often underestimated. These are checks that a business has issued and recorded as expenses but that the bank has not yet processed. The lag between issuance and processing creates a discrepancy between the company’s internal records and the bank statement. For instance, if a company writes a $500 check to a supplier on October 1st but the supplier doesn’t deposit it until October 15th, the company’s books will show a $500 reduction in cash on October 1st, while the bank statement will only reflect this reduction after the check clears. This timing difference is critical to identify and adjust for during reconciliation to ensure both records align.

To manage outstanding checks effectively, businesses must maintain a detailed register of all issued checks, including the date, payee, and amount. This register serves as a reference during reconciliation to identify which checks have cleared and which remain outstanding. For example, if a company’s bank statement shows a balance of $10,000 but the internal records show $9,500 due to outstanding checks totaling $500, the reconciliation process would add the $500 back to the bank statement balance to match the company’s records. Without this step, the company might mistakenly believe it has less cash on hand than it actually does, potentially leading to poor financial decisions.

One practical tip for minimizing the impact of outstanding checks is to encourage payees to deposit checks promptly. Businesses can achieve this by clearly communicating payment terms, using electronic payments where possible, or offering incentives for quick deposits. For example, a company might include a note on the check stating, “Please deposit within 5 business days to ensure timely processing.” Additionally, businesses should periodically review their outstanding check register and follow up on checks that remain uncashed for an unusually long time. This proactive approach reduces the risk of stale-dated checks, which can become void after a certain period, typically six months, depending on local banking regulations.

Comparatively, outstanding checks differ from other reconciling items like deposits in transit or bank errors because they represent a reduction in cash that has already been accounted for internally. While deposits in transit increase the bank’s balance, outstanding checks decrease it. Understanding this distinction is crucial for accurate reconciliation. For instance, if a company has $200 in deposits in transit and $500 in outstanding checks, the net adjustment to the bank statement would be a reduction of $300 ($500 - $200). This nuanced understanding ensures that financial statements reflect the true cash position of the business.

In conclusion, outstanding checks are a reconciling item that requires careful tracking and adjustment during bank reconciliation. By maintaining a detailed check register, encouraging prompt deposits, and understanding the unique impact of these items, businesses can ensure their financial records remain accurate and reliable. Ignoring outstanding checks can lead to misstated cash balances, potentially affecting liquidity management and decision-making. As such, mastering this aspect of reconciliation is essential for any business seeking to maintain robust financial health.

Capital One and Synchrony Bank: Potential Buyout Rumors Explained

You may want to see also

Explore related products

![]()

Deposits in Transit: Funds deposited but not yet credited by the bank

Deposits in transit represent a critical reconciling item in bank reconciliation, often causing discrepancies between a company's internal records and its bank statement. These are funds that a business has deposited into its bank account but that the bank has not yet processed or credited. This lag occurs due to the time it takes for the bank to receive, verify, and post the deposit, which can range from one to several business days depending on the deposit method and the bank's processing policies. For instance, a deposit made late in the day or via a remote mobile deposit might take longer to clear compared to one made in person during banking hours.

Understanding deposits in transit is essential for accurate financial reporting. When a company records a deposit internally, it assumes immediate availability of the funds, but the bank operates on a different timeline. This mismatch can lead to overstatement of the company's cash balance if not properly accounted for. For example, if a business deposits $5,000 on Friday afternoon but the bank credits it the following Tuesday, the company’s records will show $5,000 more than the bank statement until the deposit is processed. Failure to reconcile this difference can result in incorrect cash flow analysis, misinformed financial decisions, or even overdrafts if the company spends against unposted funds.

To manage deposits in transit effectively, businesses should maintain a detailed deposit log that tracks the date, amount, and method of each deposit. This log should be cross-referenced during the reconciliation process to identify which deposits are still in transit. For instance, if a company’s internal records show a cash balance of $20,000 but the bank statement reflects $15,000, the deposit log can reveal that $5,000 is in transit. Adjusting entries should then be made to reconcile the difference, ensuring the company’s records align with the bank’s once the deposit is credited.

A proactive approach to minimizing the impact of deposits in transit includes optimizing deposit practices. Businesses can expedite processing by depositing funds earlier in the day, using in-branch deposits instead of remote methods, or leveraging electronic transfers where possible. Additionally, maintaining a buffer in the account to cover potential delays can prevent liquidity issues. For companies with high transaction volumes, investing in accounting software that integrates with banking systems can automate tracking and reconciliation, reducing manual errors and saving time.

In conclusion, deposits in transit are a common yet manageable reconciling item in bank reconciliation. By understanding their nature, maintaining meticulous records, and adopting efficient deposit practices, businesses can ensure accurate financial reporting and avoid cash flow disruptions. Recognizing the temporary nature of these discrepancies and addressing them systematically transforms a potential source of confusion into a routine aspect of financial management.

Buying Bank Foreclosed Homes: A Step-by-Step Guide to Smart Purchases

You may want to see also

Explore related products

![]()

Bank Errors: Mistakes made by the bank affecting account balances

Bank errors, though relatively rare, can significantly impact account balances and complicate the reconciliation process. These mistakes, stemming from data entry errors, system glitches, or procedural oversights, require prompt identification and resolution to maintain financial accuracy. For instance, a bank might incorrectly record a deposit amount, post a transaction to the wrong account, or fail to process a payment altogether. Such errors not only distort the account holder’s financial picture but also erode trust in the banking institution. Vigilance in reviewing statements and understanding common error types are essential for swift correction.

Consider a scenario where a business deposits $5,000, but the bank records it as $500. This discrepancy would immediately skew the company’s available funds, potentially leading to overdrafts or missed payments. Similarly, a bank might duplicate a withdrawal, effectively debiting the account twice for the same transaction. These errors often surface during reconciliation when the account holder’s records do not align with the bank’s statement. To address such issues, account holders should first verify the accuracy of their own records before contacting the bank with specific details, such as transaction dates, amounts, and supporting documentation like deposit slips or receipts.

Banks typically have procedures in place to investigate and rectify errors, but the onus often falls on the account holder to initiate the process. For example, under Regulation E in the United States, customers have 60 days from the statement date to report unauthorized or incorrect transactions. Failure to meet this deadline may result in the bank denying liability. Practical tips include regularly monitoring account activity through online banking, setting up transaction alerts, and maintaining meticulous records of all deposits and withdrawals. Proactive measures like these can expedite error resolution and minimize financial disruption.

Comparatively, while customer errors—such as forgotten transactions or miscalculations—are common, bank errors carry a unique urgency due to their potential to affect multiple accounts or systems. For instance, a bank’s software glitch could incorrectly apply fees to thousands of accounts, requiring a mass correction. Unlike customer mistakes, which are often isolated, bank errors may necessitate broader institutional responses, including system audits or policy revisions. This distinction underscores the importance of clear communication between the account holder and the bank, as well as the need for transparency in error reporting and resolution.

In conclusion, bank errors are reconciling items that demand immediate attention and systematic resolution. By understanding their nature, maintaining detailed records, and leveraging available tools, account holders can effectively address discrepancies and safeguard their financial integrity. Banks, in turn, must prioritize accuracy and accountability to restore trust and ensure customer satisfaction. Together, these efforts contribute to a more reliable and transparent banking ecosystem.

John Dillinger's Bank Heists: Unraveling the Infamous Robbery Count

You may want to see also

Explore related products

![]()

Interest Income: Interest earned and credited by the bank

Interest income is a reconciling item that often appears on bank statements but may not yet be recorded in a company's books. This discrepancy arises because banks typically credit interest earned on a monthly or quarterly basis, while businesses might only update their records at the end of an accounting period. For instance, if a company maintains a $50,000 balance in an interest-bearing account with a 2% annual interest rate, the bank could credit $83.33 in interest income each month. However, the company’s internal records might not reflect this until the month-end reconciliation, creating a temporary mismatch between the bank statement and the company’s ledger.

To address this reconciling item, businesses must add the interest income reported by the bank to their cash balance in the general ledger. This adjustment ensures the company’s records align with the bank’s statement. For example, if the bank statement shows a balance of $50,083.33 (including the $83.33 interest), but the company’s ledger reflects only $50,000, the $83.33 must be added to the ledger balance during reconciliation. Failing to make this adjustment could lead to an understated cash balance and inaccurate financial reporting.

A critical aspect of handling interest income is verifying its accuracy. Companies should cross-check the interest amount credited by the bank against the agreed-upon interest rate and account balance. For instance, using the earlier example, the monthly interest of $83.33 is calculated as $50,000 * 0.02 / 12. Discrepancies could indicate errors in the bank’s calculation or an incorrect interest rate applied. Regular scrutiny ensures the company captures the correct amount of interest income and maintains the integrity of its financial statements.

Finally, while interest income is typically a straightforward reconciling item, it can become complex in accounts with fluctuating balances or tiered interest rates. For example, if a company’s account balance varies throughout the month, the bank might calculate interest based on daily averages. In such cases, businesses should request detailed interest calculations from the bank to ensure accurate reconciliation. By understanding and meticulously handling interest income, companies can avoid errors, maintain accurate cash records, and fully benefit from the earnings generated by their bank deposits.

Is Apple Bank a Local Financial Institution? Exploring Its Reach

You may want to see also

![]()

Service Charges: Fees deducted by the bank for account services

Service charges are a common yet often overlooked reconciling item in bank reconciliation, representing fees deducted by the bank for maintaining and servicing your account. These charges can include monthly maintenance fees, ATM usage fees, overdraft charges, and wire transfer costs, among others. Understanding and accurately accounting for these deductions is crucial for ensuring your financial records align with the bank’s statements. Failure to reconcile service charges can lead to discrepancies, potentially causing cash flow issues or misinformed financial decisions.

Analyzing service charges requires a systematic approach. Begin by identifying the specific fees listed on your bank statement, cross-referencing them with your internal records to ensure they’ve been accounted for. For instance, if your bank deducts a $10 monthly maintenance fee, verify that this amount is reflected in your ledger. Discrepancies may arise if the fee was overlooked or if the bank applied an unexpected charge, such as a penalty for falling below the minimum balance. Regularly reviewing these fees also helps in identifying trends—for example, frequent overdraft charges may indicate a need to adjust spending habits or account management practices.

From a practical standpoint, minimizing service charges can significantly improve your financial health. Many banks offer fee waivers for meeting certain criteria, such as maintaining a minimum balance, setting up direct deposits, or using specific account features. For instance, a business account holder might avoid a $25 monthly fee by keeping a $5,000 average daily balance. Additionally, negotiating with your bank or switching to a fee-free account can be effective strategies. Small businesses and individuals alike should periodically review their account terms to ensure they’re not paying unnecessary fees.

Comparatively, service charges differ from other reconciling items like deposits in transit or outstanding checks, as they directly reduce your account balance rather than being timing differences. While deposits in transit represent funds not yet credited by the bank, service charges are immediate deductions that require proactive management. This distinction underscores the importance of treating service charges as a priority during reconciliation. By doing so, you not only maintain accurate records but also gain insights into how banking fees impact your overall financial position.

In conclusion, service charges are a critical reconciling item that demands attention and strategic management. By understanding their nature, analyzing them systematically, and taking steps to minimize their impact, individuals and businesses can maintain financial accuracy and optimize their banking relationships. Regular reconciliation, coupled with proactive fee management, ensures that service charges do not become a hidden drain on resources but instead serve as a manageable aspect of account maintenance.

How Long Do ReliaCard Bank Transfers Typically Take?

You may want to see also

Frequently asked questions

Reconciling items in bank reconciliation are discrepancies or differences between a company's internal records and the bank statement that need to be adjusted to ensure both records match.

Reconciling items occur due to timing differences, errors, or transactions that have not yet been recorded by either the company or the bank, such as outstanding checks, deposits in transit, or bank fees.

Common reconciling items include outstanding checks, deposits in transit, bank service charges, interest income, NSF (non-sufficient funds) checks, and errors in recording transactions.

Reconciling items are resolved by adjusting the company's internal records or the bank statement to reflect the correct balances, ensuring both accounts align after accounting for all discrepancies.