The Big 4 American banks, also known as the Big Four, are the four largest and most influential banking institutions in the United States, dominating the financial landscape with their extensive reach and diverse services. Comprising JPMorgan Chase, Bank of America, Wells Fargo, and Citigroup, these financial powerhouses collectively manage trillions of dollars in assets and play a pivotal role in shaping the country's economy. Each of these banks offers a wide array of financial products, including retail banking, investment banking, wealth management, and corporate banking, catering to millions of individual and institutional clients nationwide. Their significant market presence, global operations, and systemic importance make them key players in the U.S. financial system and beyond.

Explore related products

What You'll Learn

- JPMorgan Chase: Largest U.S. bank by assets, global investment banking leader

- Bank of America: Second-largest U.S. bank, strong consumer banking focus

- Citigroup: Global financial services giant, major presence in international markets

- Wells Fargo: Known for retail banking, faced recent regulatory scandals

- Market Dominance: Combined, they control nearly 45% of U.S. banking assets

![]()

JPMorgan Chase: Largest U.S. bank by assets, global investment banking leader

JPMorgan Chase & Co. stands as the largest bank in the United States by assets, a title it has held consistently for over a decade. With over $3.7 trillion in assets as of 2023, it dwarfs competitors like Bank of America, Citigroup, and Wells Fargo. This financial behemoth’s scale is not just a number—it translates into unparalleled market influence, enabling it to dominate sectors from retail banking to complex investment banking operations. Its asset size also provides a buffer during economic downturns, allowing it to absorb shocks that smaller institutions might struggle with.

What sets JPMorgan Chase apart is its dual role as a global investment banking leader. While other banks may excel in specific niches, JPMorgan Chase seamlessly integrates commercial banking with high-stakes investment services. Its investment banking division advises on mergers, acquisitions, and capital raises for corporations worldwide, while its trading desks handle trillions in securities annually. This hybrid model allows it to cross-sell services effectively, creating a revenue stream that is both diverse and resilient. For instance, a corporate client might use its commercial banking services while also relying on its investment bankers for an IPO or bond issuance.

To understand JPMorgan Chase’s dominance, consider its strategic acquisitions and innovations. The 2008 acquisition of Bear Stearns and Washington Mutual during the financial crisis not only expanded its footprint but also solidified its position as a "too big to fail" institution. More recently, its investment in digital banking platforms, such as the Chase Mobile App and fintech partnerships, has kept it ahead of both traditional competitors and neobanks. These moves demonstrate a willingness to adapt, a critical trait in an industry where stagnation equals decline.

For investors or businesses considering JPMorgan Chase, its size and leadership come with both advantages and caveats. On the positive side, its global reach and financial stability make it a safe bet for large-scale transactions and long-term partnerships. However, its complexity can lead to higher fees and less personalized service for smaller clients. Additionally, its regulatory scrutiny as a systemically important financial institution (SIFI) means it operates under stricter capital requirements, which can sometimes limit flexibility.

In conclusion, JPMorgan Chase’s status as the largest U.S. bank by assets and a global investment banking leader is no accident. Its ability to balance scale with innovation, coupled with a strategic approach to diversification, has cemented its position at the top. Whether you’re a multinational corporation seeking advisory services or an individual looking for a reliable banking partner, understanding JPMorgan Chase’s unique strengths and limitations is essential for making informed financial decisions.

Go Paperless with Capital One: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Bank of America: Second-largest U.S. bank, strong consumer banking focus

Bank of America stands as the second-largest bank in the United States by assets, a position it has solidified through its extensive consumer banking network. With over 4,100 financial centers and 16,000 ATMs across the country, it offers unparalleled physical access to banking services. This vast footprint is complemented by a robust digital platform, serving over 42 million retail clients. For individuals seeking a bank with both physical presence and digital convenience, Bank of America’s infrastructure is a key differentiator.

Analyzing its business model reveals a clear emphasis on consumer banking, which accounts for approximately 55% of its total revenue. This focus is evident in its product suite, tailored to meet the needs of everyday customers. From checking and savings accounts to credit cards and mortgages, Bank of America prioritizes accessibility and affordability. For instance, its Preferred Rewards program offers tiered benefits, including waived fees and higher interest rates, rewarding loyal customers with tangible perks. This strategy not only retains clients but also encourages deeper engagement with the bank’s ecosystem.

Comparatively, while other big banks like JPMorgan Chase and Wells Fargo also have strong consumer divisions, Bank of America’s approach is more consumer-centric. Its Keep the Change program, which rounds up debit card purchases and transfers the difference to a savings account, exemplifies its commitment to helping customers save effortlessly. Such initiatives highlight its role as a financial partner rather than just a service provider. However, this consumer focus comes with challenges, such as managing lower profit margins compared to corporate or investment banking.

For those considering Bank of America, practical tips can enhance the experience. First, leverage its digital tools, such as Erica, the AI-powered virtual assistant, to manage finances efficiently. Second, take advantage of its SafeBalance Banking account, designed to prevent overdraft fees—ideal for budget-conscious individuals. Lastly, explore its Home Loans offerings, which include low down payment options and closing cost assistance, making homeownership more attainable. By aligning with its consumer-focused services, customers can maximize the bank’s value proposition.

In conclusion, Bank of America’s position as the second-largest U.S. bank is underpinned by its unwavering focus on consumer banking. Its blend of physical accessibility, digital innovation, and customer-centric products sets it apart in a competitive landscape. While it may not dominate in corporate or investment banking, its strength lies in serving the everyday financial needs of millions. For those prioritizing convenience, affordability, and a comprehensive suite of personal banking solutions, Bank of America remains a top contender.

Is Bank of Triumph Destiny 2's Fixed Destiny?

You may want to see also

Explore related products

![]()

Citigroup: Global financial services giant, major presence in international markets

Citigroup stands as a cornerstone of the global financial system, its reach extending far beyond the borders of the United States. While often grouped with the "Big 4" American banks, Citigroup's true distinction lies in its international footprint. With operations in over 160 countries and jurisdictions, it's a financial behemoth that truly operates on a global scale.

Imagine a financial services company that can cater to the needs of a multinational corporation in Tokyo, a high-net-worth individual in Dubai, and a small business owner in Mexico City – all within the same day. That's the reality of Citigroup's global reach.

This international presence isn't just about geographical spread; it's about depth and expertise. Citigroup boasts a comprehensive suite of financial products and services tailored to diverse markets. From corporate banking and investment banking to wealth management and consumer banking, they offer a one-stop shop for clients navigating the complexities of the global economy. This breadth of services, combined with their local market knowledge, positions them as a trusted partner for businesses and individuals seeking to thrive in an interconnected world.

Consider the example of a U.S.-based tech company expanding into Southeast Asia. Citigroup can provide not only the necessary financing but also invaluable insights into local regulations, cultural nuances, and market dynamics, ensuring a smoother and more successful entry.

However, operating on such a vast scale comes with its own set of challenges. Navigating diverse regulatory environments, managing currency fluctuations, and mitigating geopolitical risks are constant considerations for Citigroup. The company's ability to adapt to these complexities and maintain its global leadership position is a testament to its resilience and strategic acumen.

For investors, Citigroup's global reach presents both opportunities and considerations. On the one hand, it offers exposure to diverse markets and growth potential beyond the U.S. economy. On the other hand, it introduces a higher degree of risk due to its reliance on international markets. Careful analysis of Citigroup's global strategy, risk management practices, and performance across different regions is crucial for making informed investment decisions.

Ultimately, Citigroup's status as a global financial services giant is undeniable. Its ability to seamlessly connect markets, facilitate international trade, and provide tailored financial solutions makes it a key player in the global economy. As the world becomes increasingly interconnected, Citigroup's global presence positions it to play an even more pivotal role in shaping the future of finance.

Is Maze Bank Tower a Worthwhile Investment in GTA Online?

You may want to see also

Explore related products

$11.99 $14.99

![]()

Wells Fargo: Known for retail banking, faced recent regulatory scandals

Wells Fargo, one of the Big 4 American banks alongside JPMorgan Chase, Bank of America, and Citigroup, has long been synonymous with retail banking. With over 5,000 branches and 13,000 ATMs, it serves as a cornerstone of personal finance for millions of Americans. Its focus on everyday banking needs—checking accounts, mortgages, and credit cards—has solidified its position as a household name. However, this retail dominance has been overshadowed by a series of regulatory scandals that have tarnished its reputation and raised questions about its internal practices.

The most notorious scandal emerged in 2016, when it was revealed that Wells Fargo employees had opened millions of unauthorized accounts to meet aggressive sales targets. This unethical behavior resulted in a $185 million fine from the Consumer Financial Protection Bureau (CFPB) and sparked widespread public outrage. The fallout extended beyond financial penalties, as the bank faced congressional hearings, leadership shakeups, and a loss of customer trust. For individuals, this serves as a cautionary tale: always review your bank statements regularly and question any unfamiliar activity, regardless of the institution’s reputation.

Comparatively, while other Big 4 banks have faced their own controversies, Wells Fargo’s scandals stand out for their direct impact on retail customers. Unlike JPMorgan Chase’s involvement in complex financial instruments or Citigroup’s role in the 2008 financial crisis, Wells Fargo’s issues were rooted in the exploitation of everyday consumers. This distinction highlights the importance of transparency and accountability in retail banking, where trust is paramount. For those considering Wells Fargo, it’s essential to weigh its extensive branch network and services against its history of regulatory issues.

From a practical standpoint, if you’re a Wells Fargo customer or considering becoming one, take proactive steps to protect yourself. Opt for digital notifications for account activity, monitor your credit report annually (free via AnnualCreditReport.com), and familiarize yourself with the bank’s dispute resolution process. Additionally, consider diversifying your banking relationships to reduce reliance on a single institution. While Wells Fargo has implemented reforms, including eliminating sales quotas and enhancing oversight, vigilance remains key in safeguarding your financial interests.

Ultimately, Wells Fargo’s story serves as a reminder that even the largest institutions are not immune to failure. Its retail banking strength, once a hallmark of reliability, now coexists with a legacy of scandal. For consumers, this duality underscores the need for informed decision-making and active engagement with personal finances. Whether you stay with Wells Fargo or explore alternatives, understanding its history equips you to navigate the banking landscape more wisely.

The Meaning of ATM in Banking

You may want to see also

Explore related products

![]()

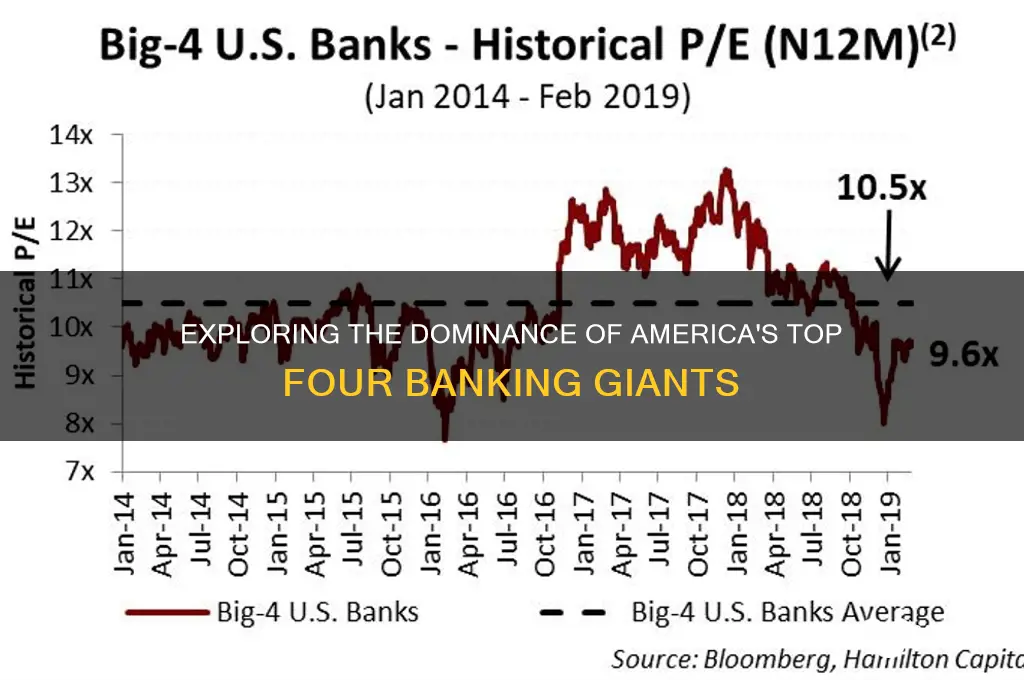

Market Dominance: Combined, they control nearly 45% of U.S. banking assets

The Big Four American banks—JPMorgan Chase, Bank of America, Wells Fargo, and Citigroup—are not just financial institutions; they are economic powerhouses. Together, they wield control over nearly 45% of U.S. banking assets, a staggering figure that underscores their collective market dominance. This concentration of power raises critical questions about competition, consumer choice, and systemic risk in the financial sector.

Consider the implications of this dominance. With such a large share of assets, these banks have unparalleled influence over lending rates, investment flows, and even regulatory conversations. For instance, their size allows them to offer a wide array of financial products, from mortgages to investment banking services, often at scale and efficiency that smaller banks struggle to match. However, this advantage comes with a trade-off: smaller banks, which often serve niche markets or underserved communities, find it increasingly difficult to compete. As a result, consumers in these areas may face limited options or higher costs, perpetuating financial inequality.

To illustrate, JPMorgan Chase alone holds over $3.7 trillion in assets, dwarfing the assets of many regional banks combined. This scale enables them to invest heavily in technology, such as mobile banking apps and AI-driven fraud detection, further solidifying their market position. Yet, this technological edge can also create barriers to entry for smaller competitors, who lack the resources to keep pace. Policymakers must grapple with how to foster innovation while ensuring fair competition—a delicate balance that often involves antitrust scrutiny and regulatory reforms.

From a practical standpoint, understanding this dominance is crucial for both consumers and investors. For consumers, it means recognizing that the Big Four often set industry standards, whether in fees, interest rates, or customer service. Shopping around for financial products remains essential, but the reality is that these banks’ offerings frequently become the benchmark. Investors, on the other hand, should view this concentration as both an opportunity and a risk. While the Big Four’s stability and profitability make them attractive investments, their size also means that any misstep could have far-reaching consequences for the broader economy.

In conclusion, the Big Four’s control of nearly 45% of U.S. banking assets is more than a statistic—it’s a defining feature of the American financial landscape. It shapes consumer experiences, drives industry innovation, and poses challenges for regulators. As these banks continue to grow, their dominance will remain a central issue in discussions about the future of banking, requiring careful consideration of its benefits and drawbacks.

Is Bank Branch Capitalization Required? Understanding Financial Terminology Basics

You may want to see also

Frequently asked questions

The Big 4 American banks refer to the four largest banking institutions in the United States by assets. They are JPMorgan Chase, Bank of America, Wells Fargo, and Citigroup.

The Big 4 American banks are distinguished by their size, global reach, and diverse range of financial services, including retail banking, investment banking, wealth management, and corporate banking. They also have a significant presence in the global financial markets.

The Big 4 American banks offer a wide range of financial services, including checking and savings accounts, credit cards, mortgages, auto loans, investment products, wealth management, and commercial banking services for businesses.

Yes, all four of the Big 4 American banks are publicly traded companies listed on major stock exchanges. JPMorgan Chase is listed on the NYSE (JPM), Bank of America on the NYSE (BAC), Wells Fargo on the NYSE (WFC), and Citigroup on the NYSE (C).