Banking services, while essential for managing finances, come with a variety of associated costs that can impact consumers and businesses alike. These costs typically include monthly maintenance fees, overdraft charges, ATM fees, wire transfer fees, and penalties for early account closures or insufficient funds. Additionally, interest rates on loans and credit cards, as well as annual fees for premium accounts or credit cards, contribute to the overall expense. Understanding these costs is crucial for making informed financial decisions, as they can vary significantly between banks and account types, and may affect long-term financial health.

Explore related products

What You'll Learn

- Account Maintenance Fees: Monthly or annual charges for holding a bank account

- Transaction Fees: Costs for transfers, withdrawals, or payments beyond limits

- Overdraft Charges: Fees for spending more than the available account balance

- ATM Fees: Charges for using out-of-network or international ATMs

- Loan Interest Rates: Costs associated with borrowing money from the bank

![]()

Account Maintenance Fees: Monthly or annual charges for holding a bank account

Bank accounts aren’t free to maintain, and account maintenance fees are a prime example of hidden costs that can erode your balance over time. These fees, typically charged monthly or annually, cover the bank’s operational expenses for managing your account, such as record-keeping, statement processing, and customer service. While some institutions waive these fees under certain conditions (like maintaining a minimum balance or setting up direct deposits), others impose them universally. For instance, a common monthly fee ranges from $5 to $15, which might seem insignificant but adds up to $60 to $180 annually. Understanding these charges is the first step in managing them effectively.

To minimize account maintenance fees, start by evaluating your banking habits and the services you actually use. Many banks offer fee-free accounts for students, seniors, or customers who meet specific criteria. For example, a student checking account often waives fees for individuals under 25 enrolled in higher education. Similarly, some banks exempt seniors aged 65 and above from these charges. If you don’t qualify for a fee-free account, consider switching to an online bank, which typically has lower overhead costs and, consequently, fewer or no maintenance fees. Always read the fine print to ensure you’re not trading one fee for another.

A comparative analysis reveals that traditional brick-and-mortar banks are more likely to charge account maintenance fees than their online counterparts. For instance, a major national bank might charge $12 monthly unless you maintain a $1,500 minimum balance, while an online bank like Ally or Chime offers no-fee accounts with no balance requirements. This disparity highlights the importance of shopping around. Additionally, credit unions often provide more favorable terms due to their not-for-profit structure, with many waiving fees for members who use their services regularly.

Persuasively, it’s worth noting that account maintenance fees are not inevitable. By being proactive, you can avoid or reduce these charges. Set up automatic transfers to meet minimum balance requirements, or link your account to direct deposits if that’s a waiver condition. Regularly review your bank’s fee schedule, as policies can change without notice. If you’re paying fees despite rarely using the account, consider closing it or downgrading to a no-fee option. Small actions like these can save you hundreds of dollars annually, making your banking experience more cost-effective.

Discover Exclusive Bank Offers on Amazon: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Transaction Fees: Costs for transfers, withdrawals, or payments beyond limits

Transaction fees can quickly erode your bank balance if you’re not mindful of your account’s limits and terms. Banks often charge for transfers, withdrawals, or payments that exceed predefined thresholds, such as a certain number of transactions per month or a maximum amount per transfer. For instance, a basic checking account might allow five free withdrawals from out-of-network ATMs before imposing a $2.50 fee per transaction. Similarly, wire transfers often incur fees ranging from $15 to $35 domestically and up to $75 internationally, depending on the bank and destination. Understanding these limits is the first step to avoiding unnecessary costs.

To minimize transaction fees, start by analyzing your banking habits. Track how often you exceed your account’s free transaction limits and identify patterns. For example, if you frequently withdraw cash from out-of-network ATMs, consider switching to a bank with a larger ATM network or carrying more cash per withdrawal to reduce frequency. Alternatively, if you regularly send large sums via wire transfer, explore lower-cost options like ACH transfers or peer-to-peer payment apps, which often charge little to no fees. Adjusting your behavior to stay within limits can save you hundreds annually.

Banks rarely waive transaction fees unless you meet specific criteria, such as maintaining a minimum balance or enrolling in direct deposit. For instance, some accounts eliminate monthly maintenance fees if you keep a $1,500 balance or receive at least $500 in direct deposits each month. Others offer fee-free transactions for customers over 65 or students under 24. If you’re unable to meet these requirements, consider switching to a no-fee online bank or credit union, which often provide more lenient terms and fewer hidden charges.

A comparative analysis of transaction fees across banks reveals significant disparities. For example, while Bank A charges $35 for domestic wire transfers, Bank B offers the same service for $15. Similarly, Credit Union C allows unlimited ATM withdrawals with no fees, whereas Bank D caps free withdrawals at five per month. By comparing fee structures and aligning your banking needs with the right institution, you can avoid paying for services you don’t need. Use online comparison tools or consult a financial advisor to identify the best fit for your lifestyle.

Finally, stay proactive in monitoring your account activity to catch and dispute any erroneous fees. Banks occasionally impose charges incorrectly, such as double-billing for a single transaction or applying fees to accounts that should be exempt. Regularly review your monthly statements and use mobile banking alerts to track transactions in real time. If you spot an error, contact your bank immediately to request a refund. Being vigilant not only protects your funds but also reinforces your understanding of how transaction fees work, empowering you to manage your finances more effectively.

Is PNC Bank Affiliated with Capital One? Unraveling the Connection

You may want to see also

Explore related products

![]()

Overdraft Charges: Fees for spending more than the available account balance

Overdraft charges are a common yet often misunderstood banking fee that can quickly escalate if not managed carefully. When you spend more than your available account balance, banks typically charge an overdraft fee, which can range from $25 to $35 per transaction, depending on the institution. For instance, if you overdraw your account by $10 to buy a coffee and then again by $20 for a quick lunch, you could face two separate fees totaling $60—far exceeding the cost of your purchases. This example highlights how small, everyday transactions can lead to significant financial penalties.

To avoid these fees, it’s essential to monitor your account balance regularly. Many banks offer mobile apps or text alerts that notify you when your balance falls below a certain threshold. Setting up these notifications can provide a real-time safeguard against accidental overdrafts. Additionally, linking your checking account to a savings account or line of credit can act as a buffer, automatically transferring funds to cover the shortfall for a lower fee or no fee at all. For example, a transfer from a savings account might incur a $10 charge, compared to the $35 overdraft fee.

While overdraft protection services can mitigate costs, they are not without pitfalls. Some banks charge daily fees for remaining overdrawn, which can accumulate if you don’t replenish your account promptly. For instance, a $3 daily fee on a $50 overdraft can add up to $90 in just one month. To avoid this, prioritize repaying the overdrawn amount as soon as possible. If you frequently find yourself overdrawing, consider switching to a bank account that offers free overdraft protection or has lower fees, such as those designed for students or low-income individuals.

From a broader perspective, overdraft charges disproportionately affect low-income account holders, who may lack the financial cushion to cover unexpected expenses. A 2021 study found that overdraft fees account for nearly 60% of banks’ consumer deposit fee revenue, with the average overdraft user paying $298 annually. This underscores the importance of financial literacy and proactive account management. Banks are increasingly offering tools like spending trackers and budgeting apps to help customers avoid overdrafts, but it’s up to the account holder to utilize these resources effectively.

In conclusion, overdraft charges are avoidable with the right strategies and awareness. By monitoring your balance, leveraging overdraft protection options, and choosing accounts with favorable fee structures, you can minimize the risk of incurring these costly penalties. Remember, the goal is not just to react to overdrafts but to prevent them altogether, ensuring your banking experience remains affordable and stress-free.

Step-by-Step Guide to Applying for Jobs at Wells Fargo Bank

You may want to see also

Explore related products

![]()

ATM Fees: Charges for using out-of-network or international ATMs

ATM fees for out-of-network or international transactions can quickly erode your finances if not managed carefully. When you use an ATM outside your bank’s network, you typically face two charges: one from the ATM operator (surcharge fee) and another from your own bank (out-of-network fee). International ATMs add currency conversion fees, often 1–3% of the transaction, plus potential foreign exchange markups. For example, withdrawing $100 from an out-of-network ATM might cost $3.50 domestically but jump to $10–$15 abroad due to additional layers of fees.

To minimize these costs, plan ahead by locating in-network ATMs or using banks with fee-free alliances. Many credit unions and online banks reimburse out-of-network fees up to a monthly limit, so check your account terms. If traveling internationally, withdraw larger amounts less frequently to reduce per-transaction fees, but balance this with safety concerns. Alternatively, use a debit card with no foreign transaction fees, such as those offered by Charles Schwab or Capital One, to avoid currency conversion markups.

A comparative analysis reveals that out-of-network ATM fees vary widely by bank and location. For instance, Bank of America charges $2.50 for out-of-network use, while Chase imposes $3. Smaller regional banks may charge up to $5. Internationally, fees spike due to cross-border processing costs. For example, a European ATM might add a €5 surcharge on top of your bank’s fees. Understanding these disparities allows you to choose accounts or strategies that align with your usage patterns, such as opting for a bank with a large ATM network if you frequently travel domestically.

Persuasively, avoiding unnecessary ATM fees is not just about saving money—it’s about adopting smarter banking habits. Apps like ATM Hunter or your bank’s mobile locator can pinpoint fee-free ATMs nearby. If you must use an out-of-network machine, consider making a purchase at a retailer with cash-back options, often fee-free. For international travelers, prepaid travel cards or local currency withdrawals via a multi-currency account can bypass hefty conversion fees. Small adjustments like these can save you hundreds annually, proving that awareness and preparation are your best defenses against hidden banking costs.

Central Bank Policies: Fueling or Fighting Persistent Low Inflation?

You may want to see also

Explore related products

![]()

Loan Interest Rates: Costs associated with borrowing money from the bank

Borrowing money from a bank is rarely a free endeavor, and one of the most significant costs borrowers face is the interest rate on their loan. This rate, expressed as a percentage of the loan amount, is essentially the price you pay for the privilege of using the bank’s money. Understanding how interest rates work and their impact on your finances is crucial for making informed borrowing decisions.

The Mechanics of Interest Rates: Interest rates on loans are determined by a combination of factors, including the borrower’s creditworthiness, the loan term, and prevailing market conditions. Banks assess your credit score, income, and debt-to-income ratio to gauge the risk of lending to you. Higher-risk borrowers typically face higher interest rates to compensate the bank for the increased likelihood of default. For example, a borrower with a credit score of 750 might secure a personal loan at 8% interest, while someone with a score of 600 could be offered the same loan at 18%. Loan terms also play a role; shorter-term loans often have lower interest rates because the bank’s money is at risk for less time.

The True Cost of Borrowing: Interest rates aren’t the only cost associated with loans, but they are the most substantial over time. Consider a $10,000 loan with a 10% interest rate over five years. Using the amortization formula, the total repayment would be approximately $12,748, meaning you’d pay $2,748 in interest alone. This example underscores the importance of shopping around for the lowest possible rate, as even a 1% difference can save hundreds or thousands of dollars over the life of the loan.

Strategies to Minimize Interest Costs: To reduce the financial burden of borrowing, start by improving your credit score. Paying bills on time, reducing credit card balances, and correcting errors on your credit report can all boost your score, potentially qualifying you for lower rates. Additionally, consider making extra payments toward the principal balance when possible. Since interest accrues on the outstanding balance, reducing the principal faster decreases the total interest paid. For instance, adding $50 to your monthly payment on a $10,000 loan at 10% could save over $500 in interest and shorten the loan term by several months.

Comparing Loan Types: Different types of loans come with varying interest rate structures. Fixed-rate loans lock in the interest rate for the life of the loan, providing predictability in monthly payments. Variable-rate loans, on the other hand, fluctuate with market conditions, which can lead to lower initial rates but higher costs if rates rise. For example, a 5/1 adjustable-rate mortgage (ARM) might offer a fixed rate for the first five years, after which it adjusts annually. Borrowers should carefully evaluate their financial stability and market trends before choosing between these options.

The Long-Term Impact: High interest rates can significantly strain your budget, particularly if you’re borrowing a large sum for a home or business. For instance, a 30-year mortgage of $300,000 at 4% interest totals $215,609 in interest payments, while the same loan at 6% would cost $369,620 in interest—a difference of $154,011. This highlights the importance of securing the lowest rate possible and considering refinancing if rates drop substantially after you’ve taken out the loan. By understanding and managing interest rates, borrowers can minimize costs and maximize the value of their loans.

Steps to Report Fraud in Union Bank: A Comprehensive Guide

You may want to see also

Frequently asked questions

Common fees include monthly maintenance fees, overdraft fees, ATM fees (for out-of-network use), and paper statement fees. Some banks waive fees with minimum balance requirements or direct deposits.

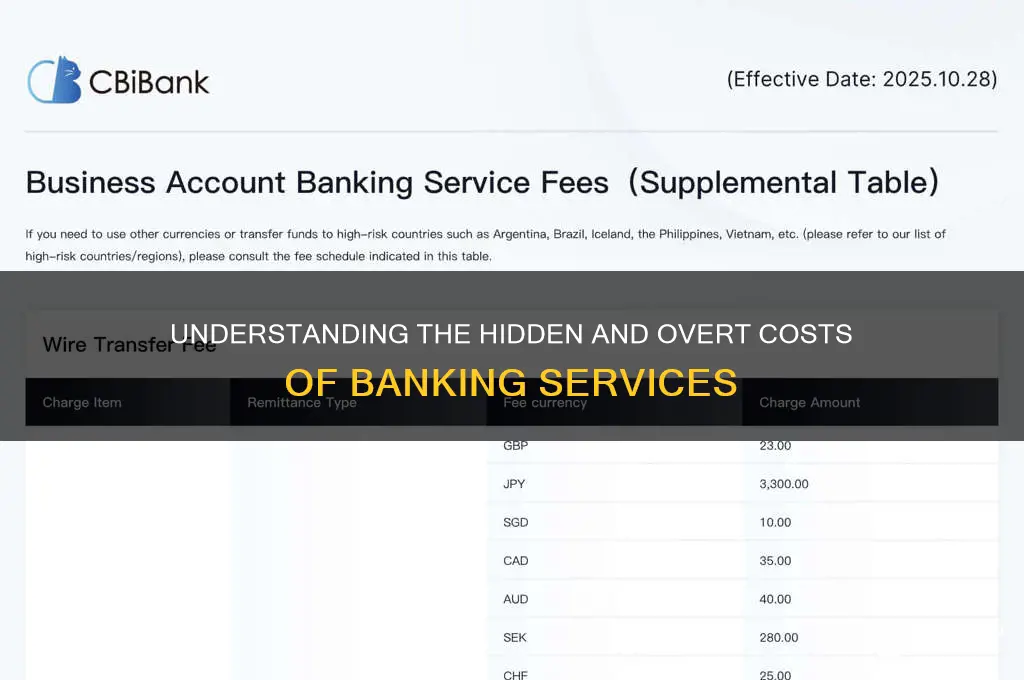

Yes, wire transfer fees typically range from $15 to $35 per transaction, depending on the bank and whether the transfer is domestic or international. Some banks offer free transfers for certain account types.

Savings accounts may charge monthly maintenance fees if the minimum balance is not maintained. Some also have excess withdrawal fees if you exceed the federal limit of six transactions per month.

Credit card costs include annual fees (if applicable), interest charges on unpaid balances, late payment fees, cash advance fees, and foreign transaction fees (usually 1-3% of the purchase amount).

Some banks charge an account closure fee, typically around $25, if the account is closed within a short period (e.g., 90-180 days) after opening. Always check the bank's fee schedule before closing an account.