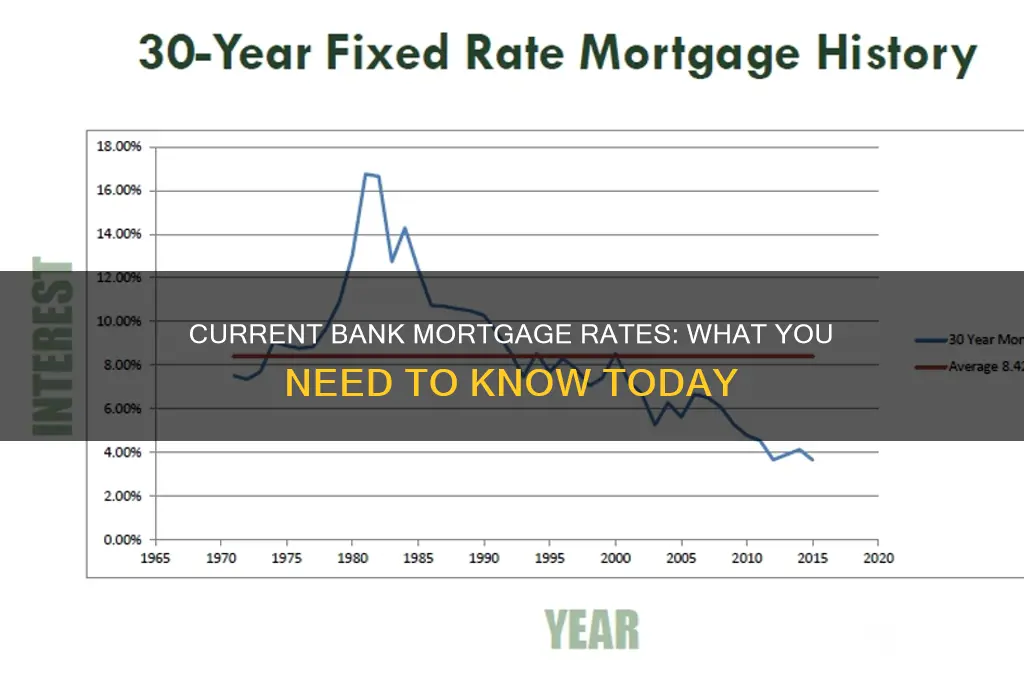

Understanding current bank mortgage rates is essential for anyone considering purchasing a home or refinancing an existing mortgage. These rates, which fluctuate based on economic conditions, Federal Reserve policies, and market trends, directly impact monthly payments and the overall cost of homeownership. As of [current date], rates vary widely among lenders, typically ranging from [insert range, e.g., 6% to 8%] for conventional 30-year fixed-rate mortgages, though they can differ based on factors like credit score, loan amount, and down payment size. Staying informed about these rates helps borrowers make informed decisions, secure the best terms, and potentially save thousands of dollars over the life of their loan.

Explore related products

$12.99

What You'll Learn

![]()

Fixed vs. Adjustable Rates

As of the latest data, current bank mortgage rates hover around 6.5% to 7.5% for 30-year fixed loans, though these figures fluctuate based on economic conditions, lender policies, and borrower creditworthiness. Within this landscape, the choice between fixed and adjustable rates becomes pivotal, as it directly impacts long-term financial stability and monthly cash flow. Fixed rates lock in a consistent interest rate for the loan’s duration, offering predictability, while adjustable rates (ARMs) start lower but can rise after an initial period, tying payments to market shifts.

Consider a scenario where a borrower opts for a 5/1 ARM at 5.5% instead of a 30-year fixed at 7.0%. For the first five years, the ARM saves them approximately $200 monthly on a $300,000 loan. However, if rates climb by 2% after the adjustment period, their payment could surge by $350—a risk that demands careful planning. This example underscores the trade-off between short-term savings and long-term uncertainty, making ARMs ideal for those planning to sell or refinance before the adjustment period ends.

Analytically, fixed rates excel in high-rate environments or for risk-averse borrowers. They eliminate the stress of payment shocks, ensuring budgeting consistency. Conversely, ARMs thrive in falling-rate markets or for borrowers with short-term horizons. A key metric to evaluate ARMs is the fully indexed rate (initial rate + margin + index), which caps potential increases. For instance, a 5/1 ARM with a 2% margin and tied to the SOFR index (currently ~5%) could theoretically rise to 7% post-adjustment—a figure borrowers must stress-test against their financial resilience.

Persuasively, fixed rates align with the adage, “Plan for the worst, hope for the best.” They shield against inflationary spikes, as seen in the 1980s when rates topped 18%. ARMs, however, can be strategically paired with extra principal payments during the low-rate period, reducing overall interest costs. For instance, allocating the $200 monthly savings from the ARM example to principal could shorten the loan term by 5–7 years, provided rates remain stable.

Practically, borrowers should assess their financial elasticity—income stability, savings buffer, and tolerance for risk. Tools like mortgage calculators can model worst-case ARM scenarios, while consulting a financial advisor ensures alignment with broader goals. For instance, a 35-year-old with a growing career might lean toward an ARM, while a retiree prioritizes fixed-rate security. Ultimately, the decision hinges on balancing today’s affordability with tomorrow’s adaptability.

Are Greek Banks Facing a Run Amid Economic Uncertainty?

You may want to see also

Explore related products

![]()

Impact of Credit Scores

Credit scores wield significant influence over the mortgage rates banks offer, acting as a financial report card that lenders scrutinize to gauge risk. A higher credit score—typically 740 or above—often unlocks access to the most competitive rates, sometimes dipping below the national average. Conversely, scores below 620 may confine borrowers to subprime rates, which can be 1.5% to 2% higher, adding tens of thousands of dollars in interest over a 30-year loan. This disparity underscores the tangible impact of creditworthiness on long-term financial commitments.

To illustrate, consider two borrowers seeking a $300,000 mortgage. Borrower A, with a credit score of 780, might secure a 5.5% interest rate, resulting in a monthly payment of $1,703. Borrower B, with a score of 600, could face a 7.5% rate, pushing their monthly payment to $2,098. Over 30 years, Borrower B would pay $135,480 more in interest. This example highlights how a seemingly small difference in credit scores can translate into substantial financial consequences.

Improving a credit score before applying for a mortgage is a strategic move that can yield significant savings. Practical steps include paying down high credit card balances to keep utilization below 30%, disputing inaccuracies on credit reports, and avoiding new credit inquiries six months prior to application. For those with scores in the mid-600s, even a 20-point increase can sometimes lower the offered rate by 0.25% to 0.5%, depending on the lender’s criteria.

It’s also worth noting that credit scores aren’t the sole determinant of mortgage rates, but they carry disproportionate weight. Lenders may offer slight adjustments for factors like a large down payment or stable employment history, but a poor credit score can negate these benefits. Borrowers with scores below 640 should explore FHA loans, which accept lower scores but require mortgage insurance, or consider co-signing with a creditworthy individual to secure a better rate.

In conclusion, understanding the impact of credit scores on mortgage rates empowers borrowers to take proactive steps toward financial optimization. Whether through meticulous credit management or strategic loan selection, the goal is to position oneself as a low-risk candidate in the eyes of lenders. The reward? Thousands of dollars saved over the life of the loan—a testament to the power of a few numerical points on a credit report.

Is Bank of the West a Fortune 500 Company? Unveiling the Truth

You may want to see also

Explore related products

![]()

Loan Term Options (15/30 Years)

Choosing between a 15-year and 30-year mortgage term is one of the most critical decisions you’ll make when securing a home loan. Current bank mortgage rates reflect a significant difference in monthly payments and total interest costs between these two options. As of recent data, 30-year fixed mortgage rates hover around 6.5% to 7.0%, while 15-year rates are typically lower, ranging from 5.5% to 6.0%. This disparity directly impacts your financial strategy.

For instance, a $300,000 mortgage at 6.7% for 30 years results in a monthly payment of approximately $1,939, with total interest paid over the life of the loan exceeding $400,000. In contrast, the same loan amount at 5.8% for 15 years yields a higher monthly payment of around $2,650 but slashes total interest to roughly $177,000. This example underscores the trade-off: lower monthly payments with a 30-year term versus substantial interest savings with a 15-year term.

Analytically, the 15-year term is ideal for borrowers with stable income and a desire to build equity quickly. It forces disciplined repayment, ensuring the home is owned outright in half the time. However, the higher monthly payments may strain cash flow, leaving less flexibility for emergencies or other financial goals. Conversely, the 30-year term offers breathing room in monthly budgeting, making it suitable for those prioritizing liquidity or planning to invest the difference in higher-yield opportunities.

Persuasively, if you’re nearing retirement or aiming to be debt-free sooner, the 15-year term aligns with long-term financial security. Younger borrowers or those anticipating income growth might lean toward the 30-year term, refinancing later if rates drop. Practical tip: Use online mortgage calculators to model scenarios based on your income, savings, and financial goals before committing.

Comparatively, the choice boils down to risk tolerance and financial priorities. A 15-year mortgage is a high-commitment, high-reward option, while a 30-year mortgage provides flexibility at the cost of long-term interest. Current rates amplify this decision, as even a 1% difference in rates can translate to tens of thousands in savings or additional costs. Ultimately, align your choice with your timeline, cash flow needs, and broader financial strategy.

Is Bank of Hawaii a Good Bank? Pros, Cons, and Reviews

You may want to see also

Explore related products

![]()

Down Payment Requirements

As of the latest data, current bank mortgage rates fluctuate between 6.5% and 7.5% for conventional 30-year fixed loans, influenced by factors like credit score, loan term, and market conditions. Amid these rates, understanding down payment requirements becomes critical, as it directly impacts borrowing costs and eligibility. Lenders typically require a minimum down payment of 3% to 20% of the home’s purchase price, but the optimal amount varies based on financial goals and loan type.

Analytical Perspective:

A 20% down payment is often touted as the gold standard because it eliminates private mortgage insurance (PMI), reducing monthly expenses. For example, on a $300,000 home, a 20% down payment ($60,000) saves approximately $150–$200 monthly in PMI. However, not all buyers can afford this upfront cost. FHA loans, for instance, allow as little as 3.5% down, making homeownership accessible to those with limited savings. Yet, this lower threshold comes with higher long-term costs due to mortgage insurance premiums.

Instructive Steps:

To navigate down payment requirements effectively, follow these steps:

- Assess Your Budget: Calculate how much you can comfortably save without depleting emergency funds.

- Explore Loan Programs: Research options like VA loans (0% down for eligible veterans) or USDA loans (0% down in rural areas).

- Consider Down Payment Assistance: Many states and local programs offer grants or low-interest loans to first-time buyers.

- Factor in Closing Costs: Ensure your savings cover both the down payment and additional fees, typically 2%–5% of the purchase price.

Comparative Insight:

While a larger down payment reduces interest costs over time, it’s not always the best strategy. For example, investing the extra cash in a diversified portfolio with a 7% annual return could yield higher returns than saving on mortgage interest. Conversely, a smaller down payment allows buyers to enter the market sooner, potentially benefiting from home equity growth in rising markets.

Practical Tips:

- Gift Funds: Many lenders accept down payment gifts from relatives, but documentation is required.

- Retirement Accounts: First-time buyers can withdraw up to $10,000 penalty-free from a Roth IRA for a down payment.

- Negotiate Seller Concessions: In a buyer’s market, sellers may contribute up to 3%–6% of the home’s price toward closing costs, indirectly reducing the down payment burden.

By weighing these factors, borrowers can align their down payment strategy with both current mortgage rates and long-term financial objectives.

Is a Ripped Bank Note Still Legal Tender? Find Out Now

You may want to see also

Explore related products

![]()

Current Market Trends

Mortgage rates have been on a rollercoaster ride over the past year, with fluctuations driven by shifting economic indicators and Federal Reserve policies. As of the latest data, the average 30-year fixed mortgage rate hovers around 6.5% to 7.0%, a stark contrast to the sub-3% rates seen in late 2020 and early 2021. This upward trend reflects efforts to curb inflation, which has been persistently high since 2022. For prospective homebuyers, this means higher monthly payments and a more cautious approach to borrowing. However, rates remain historically moderate compared to pre-2008 levels, offering a silver lining for those prepared to navigate the current market.

One notable trend is the widening gap between fixed and adjustable-rate mortgages (ARMs). While 30-year fixed rates have climbed steadily, ARMs have seen more modest increases, with some 5/1 ARMs starting below 5.5%. This disparity is prompting borrowers to reconsider their long-term plans. For those expecting to sell or refinance within five years, an ARM could provide short-term savings. However, this strategy carries risk, as rates could rise significantly after the initial fixed period. Financial advisors caution against ARMs unless borrowers have a clear exit strategy or can afford potential payment increases.

Another key trend is the growing importance of credit scores in securing favorable rates. Lenders are tightening underwriting standards in response to economic uncertainty, making it harder for borrowers with scores below 700 to qualify for the lowest rates. For example, a borrower with a 760+ score might secure a rate of 6.5%, while someone with a 680 score could face rates closer to 7.5%. To improve their position, prospective buyers should prioritize paying down debt, avoiding new credit inquiries, and correcting any errors on their credit reports at least six months before applying for a mortgage.

Finally, the rise of discount points as a rate-reduction tool is worth noting. By paying upfront fees, borrowers can lower their interest rates, often by 0.25% per point. For instance, on a $300,000 mortgage, one point typically costs $3,000 and reduces the rate from 7.0% to 6.75%. This strategy is most effective for long-term homeowners who plan to stay in their property for at least a decade. Online calculators can help determine the break-even point, ensuring the upfront cost pays off over time. In a high-rate environment, this approach can provide meaningful savings for those with the liquidity to invest upfront.

Mastering Va Bank a Million: Winning Strategies for Big Rewards

You may want to see also

Frequently asked questions

Current average mortgage rates vary by lender, loan type, and borrower creditworthiness, but as of recent data, they typically range between 6.5% and 7.5% for a 30-year fixed-rate mortgage. Rates fluctuate based on economic conditions and Federal Reserve policies.

Banks determine mortgage rates based on factors such as the borrower’s credit score, loan-to-value ratio, loan term, and overall financial health. Additionally, market conditions, inflation, and the Federal Reserve’s benchmark interest rate play a significant role in rate setting.

Banks offer both fixed-rate and adjustable-rate mortgages (ARMs). Fixed rates remain constant throughout the loan term, providing stability, while ARMs start with a lower rate that can adjust periodically. The better option depends on your financial goals, how long you plan to stay in the home, and your tolerance for potential rate increases.