The Federal Reserve System, often referred to as the Fed, is the central banking system of the United States, and at its core are the twelve Federal Reserve Banks. These banks serve as the operating arms of the nation's central banking system, each responsible for a specific geographic region known as a Federal Reserve District. Established by the Federal Reserve Act of 1913, these banks play a critical role in implementing monetary policy, supervising and regulating member banks, and providing financial services to the U.S. government, financial institutions, and the public. Together, they ensure the stability and efficiency of the nation's financial system, manage currency circulation, and act as lenders of last resort during economic crises. Each Federal Reserve Bank operates independently but coordinates with the Federal Reserve Board in Washington, D.C., to achieve the Fed's broader economic objectives.

| Characteristics | Values |

|---|---|

| Number of Banks | 12 |

| Purpose | Implement monetary policy, supervise banks, and regulate financial institutions |

| Headquarters Locations | Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, San Francisco |

| Governing Body | Federal Reserve System (The Fed) |

| Established | December 23, 1913 (Federal Reserve Act) |

| Key Functions | Conducting monetary policy, regulating banks, providing financial services to banks and the U.S. government |

| Board of Directors | Each bank has a nine-member board (3 appointed by the Fed, 6 elected by member banks) |

| President | Each bank has a president appointed by the board of directors |

| Geographic Coverage | Each bank serves a specific region of the U.S. |

| Monetary Policy Role | Participate in setting interest rates and managing the money supply |

| Bank Supervision | Oversee and regulate state-chartered banks and bank holding companies |

| Financial Services | Provide payment services, distribute currency, and act as fiscal agents for the U.S. government |

| Research and Data | Conduct economic research and publish data on regional and national economies |

| Emergency Lending | Act as lenders of last resort during financial crises |

| Public Engagement | Engage with local communities and businesses to understand economic conditions |

Explore related products

What You'll Learn

- Locations of the 12 Federal Reserve Banks across the United States

- Roles and responsibilities of each Federal Reserve Bank

- Governance structure: boards of directors and their functions

- Services provided, including payments, supervision, and currency distribution

- Relationship between Federal Reserve Banks and the central board

![]()

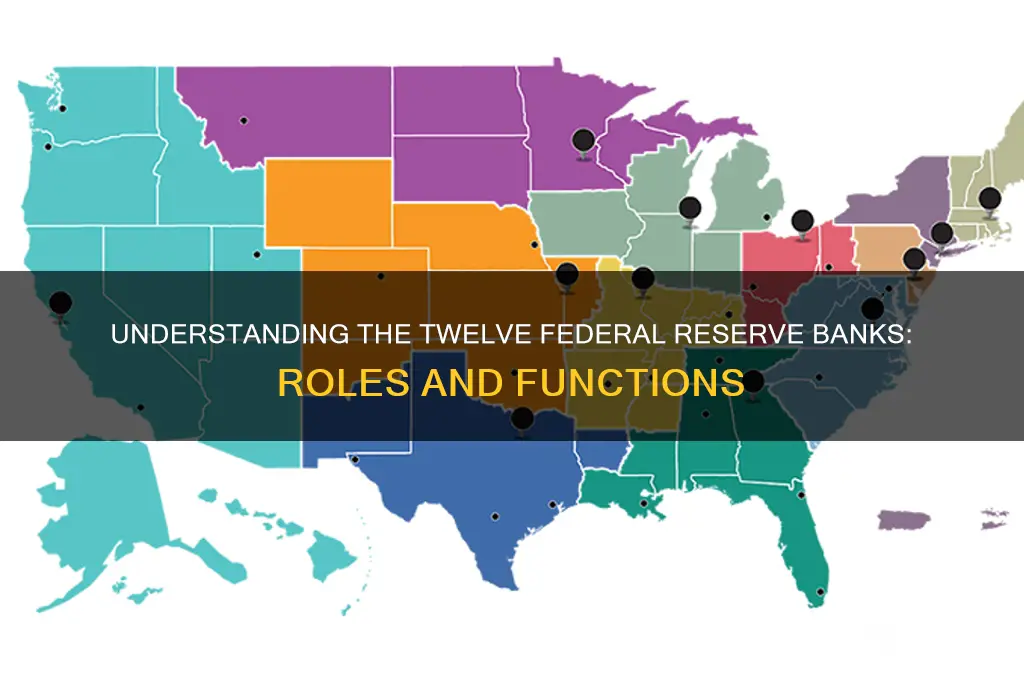

Locations of the 12 Federal Reserve Banks across the United States

The Federal Reserve System, often referred to as "the Fed," is the central banking system of the United States, and it is composed of 12 regional Federal Reserve Banks. These banks are strategically located across the country to ensure comprehensive coverage and representation of diverse economic regions. Each bank operates within its designated district, contributing to the overall stability and efficiency of the nation's financial system.

A Geographical Overview: The 12 Federal Reserve Banks are situated in major cities, each serving a specific region. Starting from the East Coast, the Federal Reserve Bank of Boston covers New England, including states like Massachusetts, Rhode Island, and Maine. Moving south, the Federal Reserve Bank of New York is a prominent institution, overseeing a district that includes not only New York State but also parts of Connecticut and New Jersey, as well as the Commonwealth of Puerto Rico and the U.S. Virgin Islands. The Federal Reserve Bank of Philadelphia serves the eastern states of Pennsylvania, southern New Jersey, and Delaware.

Midwestern and Southern Presence: In the Midwest, the Federal Reserve Bank of Chicago plays a crucial role, covering a vast area that includes Illinois, Indiana, Iowa, Michigan, and Wisconsin. Further south, the Federal Reserve Bank of St. Louis serves Arkansas, southern Indiana, southern Illinois, eastern Missouri, western Tennessee, northern Mississippi, and Kentucky. The Federal Reserve Bank of Minneapolis is responsible for Minnesota, Montana, North Dakota, South Dakota, and parts of Wisconsin and Michigan. Meanwhile, the Federal Reserve Bank of Kansas City oversees Colorado, Kansas, Nebraska, Oklahoma, Wyoming, and western Missouri.

Western Regions: The western United States is served by four Federal Reserve Banks. The Federal Reserve Bank of Dallas covers not only Texas but also northern Louisiana and southern New Mexico. The Federal Reserve Bank of San Francisco is responsible for the Pacific Northwest, including Alaska, American Samoa, Arizona, California, Guam, Hawaii, Idaho, Northern Mariana Islands, Montana, Nevada, Oregon, Utah, Washington, and Wyoming. The Federal Reserve Bank of Atlanta serves the southeastern states of Alabama, Florida, Georgia, and parts of Louisiana, Mississippi, and Tennessee. Lastly, the Federal Reserve Bank of Cleveland covers Ohio, western Pennsylvania, the northern panhandle of West Virginia, and eastern Kentucky.

Strategic Placement for Economic Diversity: The distribution of these banks is not arbitrary. Each location was carefully chosen to represent distinct economic zones, ensuring that the Federal Reserve System can effectively monitor and respond to regional economic conditions. For instance, the Federal Reserve Bank of Richmond, serving Maryland, Virginia, and the Carolinas, is well-positioned to address the unique economic dynamics of the mid-Atlantic region. Similarly, the Federal Reserve Bank of Minneapolis's coverage of the upper Midwest allows for a focused approach to the agricultural and industrial economies of those states. This strategic placement enables the Fed to gather localized economic intelligence, making informed decisions that cater to the specific needs of each region while contributing to the overall health of the national economy.

Step-by-Step Guide to Establishing Your Own Internet Bank

You may want to see also

Explore related products

![]()

Roles and responsibilities of each Federal Reserve Bank

The Federal Reserve System, often referred to as "the Fed," is the central banking system of the United States, comprising 12 regional Federal Reserve Banks. Each of these banks operates within its designated district, playing a unique yet interconnected role in maintaining the nation’s financial stability. While their core functions align with the Fed’s broader objectives, each bank tailors its responsibilities to address the economic nuances of its region. Understanding these roles is critical for grasping how monetary policy, financial supervision, and economic research are implemented at a local level.

Consider the Federal Reserve Bank of New York, arguably the most influential of the 12. Located in the heart of the world’s financial capital, it executes open market operations—the buying and selling of government securities to control the money supply—on behalf of the entire system. It also serves as the primary regulator for many of the nation’s largest banks and houses the Fed’s foreign currency operations. In contrast, the Federal Reserve Bank of St. Louis is renowned for its economic research and public education initiatives, publishing widely cited data series like the Financial Stress Index. This bank’s focus on transparency and education underscores its commitment to demystifying monetary policy for the public.

Each Federal Reserve Bank acts as a lender of last resort for its region’s financial institutions, providing liquidity during times of crisis to prevent bank runs and stabilize markets. For example, the Federal Reserve Bank of San Francisco played a pivotal role in supporting West Coast banks during the 2008 financial crisis, ensuring they had sufficient funds to meet withdrawal demands. Additionally, these banks supervise and regulate state-chartered banks and bank holding companies, ensuring compliance with federal laws and safeguarding consumer rights. The Federal Reserve Bank of Chicago, for instance, oversees a district that includes major agricultural states, requiring it to monitor the unique financial risks associated with farming and rural banking.

Beyond supervision, each bank contributes to monetary policy through its president’s participation in Federal Open Market Committee (FOMC) meetings. While only five of the 12 bank presidents vote in any given year, all provide critical insights into regional economic conditions. The Federal Reserve Bank of Dallas, for example, offers perspectives on the energy sector’s impact on inflation and employment, given its district’s heavy reliance on oil and gas. This regional input ensures that monetary policy decisions reflect the diverse economic realities across the U.S.

Finally, the Federal Reserve Banks serve as fiscal agents for the U.S. government, processing payments, issuing currency, and managing the national debt. The Federal Reserve Bank of Cleveland is one of the four banks that destroy worn-out currency, replacing it with new bills to maintain the integrity of the money supply. Each bank also engages in community outreach, partnering with local organizations to address issues like financial literacy and economic inequality. For instance, the Federal Reserve Bank of Atlanta collaborates with Southern nonprofits to promote affordable housing and small business development, demonstrating how these institutions extend their impact beyond Wall Street to Main Street.

In summary, while the 12 Federal Reserve Banks share common objectives, their roles are distinctly shaped by the economic landscapes of their districts. From executing monetary policy to regulating banks and fostering community development, each bank operates as a vital node in the nation’s financial network. Their collective efforts ensure that the Federal Reserve System remains responsive to both national priorities and regional needs, making them indispensable to the U.S. economy.

How to Cancel a Mandate in Federal Bank: Step-by-Step Guide

You may want to see also

Explore related products

![]()

Governance structure: boards of directors and their functions

The Federal Reserve System's governance structure is a complex web of oversight and decision-making, with the boards of directors playing a pivotal role in shaping monetary policy and ensuring the stability of the financial system. Each of the twelve Federal Reserve Banks has its own board of directors, comprising nine members, to provide local perspective and expertise. This decentralized approach is a cornerstone of the Fed's design, allowing for a nuanced understanding of regional economic conditions.

Composition and Selection: The boards are strategically composed to represent diverse interests. Each board includes six non-banking representatives from the local community, elected by member banks, and three banking representatives, appointed by the Board of Governors in Washington, D.C. This mix ensures a balance between financial industry knowledge and broader economic insights. For instance, non-banking directors might include business leaders, economists, or community organizers, bringing a wealth of experience from various sectors. The selection process is meticulous, aiming to identify individuals with a deep understanding of their region's economic landscape.

Functions and Responsibilities: These boards are not mere figureheads; they wield significant influence. Their primary duties include overseeing the management of their respective Reserve Banks, setting the discount rate (the interest rate charged to commercial banks for short-term loans), and advising the Board of Governors on monetary policy. This advisory role is critical, as it provides a grassroots perspective on economic conditions, ensuring that policy decisions are informed by on-the-ground realities. For example, a board might highlight emerging trends in local industries, such as agriculture or manufacturing, which could have broader implications for the national economy.

A key aspect of their function is the monthly meetings where directors discuss economic developments, review bank operations, and make recommendations. These meetings are a forum for robust debate, where directors can challenge assumptions and propose innovative solutions. The boards also have the power to appoint the president of their Reserve Bank, a position of immense responsibility, further emphasizing their role in shaping the Fed's leadership.

Impact and Influence: The influence of these boards extends beyond their regional boundaries. Their collective insights contribute to the Federal Open Market Committee (FOMC), the body responsible for setting national monetary policy. This is where the local becomes national, as the boards' perspectives help shape decisions on interest rates and other critical economic levers. For instance, a board's input on regional unemployment rates or housing market trends can significantly impact the FOMC's understanding of the overall economic health.

In essence, the boards of directors are the Federal Reserve's eyes and ears on the ground, providing a critical link between local economies and national policy. Their unique governance structure ensures that the Fed's decisions are informed by a rich tapestry of regional experiences, making the system more responsive and adaptable to the diverse needs of the American economy. This decentralized approach is a key strength, allowing the Fed to navigate the complexities of a vast and varied economic landscape.

Easy Steps to Generate Challan in SBI Bank Online

You may want to see also

Explore related products

![]()

Services provided, including payments, supervision, and currency distribution

The Federal Reserve System, often referred to as "the Fed," operates through twelve regional Federal Reserve Banks, each serving a specific geographic area. These banks are not merely administrative divisions but active participants in the nation’s financial ecosystem, providing critical services that underpin the economy. Among their core functions are payments processing, financial institution supervision, and currency distribution—each playing a distinct yet interconnected role in maintaining financial stability and efficiency.

Consider the payments system, the lifeblood of modern commerce. The Federal Reserve Banks process trillions of dollars in transactions daily, including wire transfers, automated clearinghouse (ACH) payments, and check clearing. For instance, when you pay your mortgage or receive a direct deposit, the Fed’s infrastructure ensures these transactions are settled securely and efficiently. This service is particularly vital for large-value payments, where delays or errors could have cascading effects on businesses and consumers. By operating systems like Fedwire, the Fed reduces systemic risk and ensures liquidity flows smoothly through the economy.

Supervision is another cornerstone of the Fed’s mandate, though it’s often less visible to the public. The twelve banks oversee state-chartered institutions and foreign banks operating within their districts, ensuring compliance with regulations and assessing financial health. This involves on-site inspections, risk assessments, and enforcement actions when necessary. For example, during the 2008 financial crisis, the Fed’s supervisory role was critical in identifying weaknesses in bank balance sheets and implementing corrective measures. This function is not just about punishment but about fostering a safer, more resilient banking system that protects depositors and supports economic growth.

Currency distribution, while seemingly mundane, is a logistical marvel. The Federal Reserve Banks manage the supply of physical cash, ensuring ATMs are stocked, banks have sufficient reserves, and damaged or counterfeit bills are removed from circulation. Each year, billions of dollars in currency are processed, with worn notes replaced and new ones introduced. This service is particularly crucial during times of crisis, such as natural disasters, when cash demand spikes. For instance, after Hurricane Katrina, the Fed coordinated emergency cash shipments to affected areas, demonstrating its role as a financial first responder.

Together, these services illustrate the Fed’s dual role as both a facilitator and a regulator. Payments processing keeps the economy moving, supervision safeguards its integrity, and currency distribution ensures its tangible foundation remains intact. While each function operates independently, they collectively contribute to the Fed’s broader mission of promoting monetary stability and economic prosperity. Understanding these services offers insight into how the Federal Reserve Banks are not just regional entities but essential cogs in the machinery of the U.S. financial system.

Is Bank of Cyprus UK Safe? A Comprehensive Financial Security Review

You may want to see also

Explore related products

![]()

Relationship between Federal Reserve Banks and the central board

The Federal Reserve System, often referred to as "the Fed," is a complex network where the twelve Federal Reserve Banks and the Board of Governors (the central board) operate in a delicate balance of autonomy and oversight. Each of the twelve Reserve Banks, strategically located across the United States, serves as the operational arm of the Fed in its respective region. They are responsible for implementing monetary policy, supervising and regulating member banks, and providing financial services to the banking system. However, their actions are not taken in isolation. The central board, headquartered in Washington, D.C., sets the overarching policies and ensures consistency across the system. This relationship is not hierarchical in the traditional sense but rather a partnership designed to maintain economic stability while allowing regional flexibility.

Consider the process of setting interest rates, a critical tool in monetary policy. The Federal Open Market Committee (FOMC), which includes members of the central board and Reserve Bank presidents, collaboratively decides on these rates. While the central board provides the strategic direction, Reserve Bank presidents contribute regional insights, ensuring that national policies are informed by local economic conditions. For instance, a Reserve Bank in an agricultural region might highlight the impact of crop yields on local employment, influencing the FOMC’s decision. This collaborative approach underscores the importance of both national oversight and regional expertise.

Despite this partnership, the central board retains ultimate authority over the Reserve Banks. It appoints the presidents of the Reserve Banks, subject to the approval of the Fed’s Board of Governors, and oversees their operations. Additionally, the central board conducts regular audits and enforces compliance with federal regulations. This oversight ensures that the Reserve Banks align with the Fed’s broader objectives, such as maintaining price stability and maximum employment. However, the Reserve Banks are not merely passive executors of policy; they actively participate in shaping it through research, data collection, and advocacy for their regions.

A practical example of this relationship can be seen in the response to the 2008 financial crisis. The central board implemented unprecedented measures, such as quantitative easing, while Reserve Banks played a crucial role in executing these policies. For instance, the Federal Reserve Bank of New York, due to its proximity to Wall Street, took the lead in stabilizing financial markets. Meanwhile, other Reserve Banks focused on supporting local banks and businesses. This coordinated effort demonstrates how the central board’s strategic decisions are effectively implemented through the operational capabilities of the Reserve Banks.

In conclusion, the relationship between the Federal Reserve Banks and the central board is a dynamic interplay of authority and collaboration. While the central board sets the tone and ensures uniformity, the Reserve Banks provide the regional insights and operational expertise necessary to implement policies effectively. This structure allows the Fed to address both national economic challenges and regional disparities, making it a unique and effective institution in the global financial landscape. Understanding this relationship is key to appreciating how the Fed fulfills its dual mandate of stabilizing prices and promoting employment across the United States.

Cancel Standard Bank Overdraft via App: A Step-by-Step Guide

You may want to see also

Frequently asked questions

The twelve Federal Reserve Banks are the operating arms of the Federal Reserve System, the central banking system of the United States. Each bank serves a specific region of the country, known as a Federal Reserve District, and works to implement monetary policy, supervise banks, and provide financial services.

The twelve Federal Reserve Banks are located in Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, and San Francisco. Each location serves its respective district, which covers multiple states or parts of states.

The primary functions of the twelve Federal Reserve Banks include conducting monetary policy, supervising and regulating member banks, providing financial services to banks and the U.S. government, and ensuring the stability of the financial system. They also play a key role in distributing currency and managing the nation’s payments system.