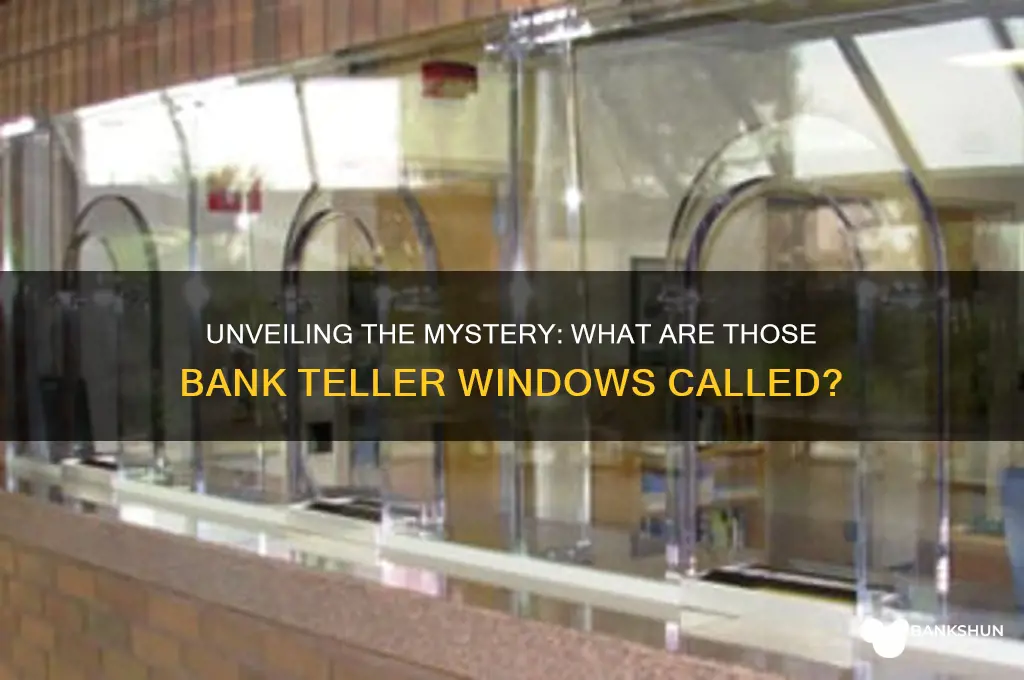

When visiting a bank, you’ve likely noticed the small, enclosed windows where tellers assist customers with transactions. These windows are officially called teller windows or teller stations, designed to provide a secure and efficient space for handling cash, deposits, withdrawals, and other banking services. They often feature a combination of glass barriers, transaction drawers, and communication systems to ensure both safety and convenience for customers and staff. While the term teller window is most common, they may also be referred to as cashier windows or bank teller booths, depending on regional terminology or bank-specific naming conventions.

Explore related products

What You'll Learn

- Drive-Thru Teller Windows: Specialized windows for banking services accessible directly from a vehicle

- Bulletproof Glass Windows: Security feature in teller windows to protect against theft or violence

- Sliding Drawer Mechanism: Allows secure exchange of documents, cash, or items between teller and customer

- Privacy Panels: Designed to block view from other customers for confidential transactions

- Transaction Counter Windows: Main point of interaction for in-branch banking services with customers

![]()

Drive-Thru Teller Windows: Specialized windows for banking services accessible directly from a vehicle

Drive-thru teller windows, often referred to as bank teller drive-up lanes or drive-thru banking windows, are a specialized feature designed to offer customers the convenience of conducting banking transactions directly from their vehicles. These windows are typically equipped with intercom systems, pneumatic tubes for secure document exchange, and sometimes even video conferencing capabilities for enhanced customer interaction. Unlike traditional walk-in teller windows, drive-thru windows prioritize speed and accessibility, making them ideal for busy individuals or those with mobility challenges.

From an analytical perspective, the design of drive-thru teller windows reflects a shift in banking priorities toward customer convenience and efficiency. Banks invest in these systems to reduce wait times and streamline operations, particularly during peak hours. For instance, a study by the American Bankers Association found that drive-thru lanes can handle up to 30% more transactions per hour compared to indoor tellers. However, this efficiency comes with challenges, such as ensuring security and maintaining a personal touch in a fast-paced environment. Banks often address these concerns by integrating advanced surveillance systems and training staff to provide quick yet friendly service.

For those considering using drive-thru teller windows, here’s a practical guide: First, ensure your vehicle’s windows can fully lower to facilitate easy communication and document exchange. Keep all necessary items, such as deposit slips, IDs, and checks, organized before approaching the window to minimize delays. If using a pneumatic tube system, double-check that your documents are securely placed in the carrier to avoid damage or loss. Lastly, be mindful of the queue and avoid blocking other vehicles if you need to complete a complex transaction; consider parking and moving indoors instead.

Comparatively, drive-thru teller windows differ significantly from other banking channels like ATMs or mobile apps. While ATMs offer 24/7 access for basic transactions, drive-thru windows provide a broader range of services, including cash deposits, loan payments, and account inquiries, all with the assistance of a live teller. Mobile apps, on the other hand, offer digital convenience but lack the personal interaction that some customers prefer. Drive-thru windows strike a balance by combining the efficiency of technology with the human touch of traditional banking.

Descriptively, a typical drive-thru teller window setup includes a canopy-covered lane with clear signage directing customers to the service area. The window itself is often reinforced with bulletproof glass for security, while the intercom system ensures clear communication even in noisy environments. Some banks enhance the experience with digital displays showing transaction details or promotional offers. The overall design aims to create a seamless, stress-free experience, allowing customers to complete their banking tasks without leaving their cars.

In conclusion, drive-thru teller windows are a testament to the banking industry’s adaptability in meeting evolving customer needs. By blending technology, security, and personalized service, these specialized windows offer a unique solution for those seeking convenience without compromising on functionality. Whether you’re a busy professional or someone who values accessibility, understanding how to effectively use drive-thru teller windows can significantly enhance your banking experience.

Coin Counting: Banks Offering Free Services?

You may want to see also

Explore related products

![]()

Bulletproof Glass Windows: Security feature in teller windows to protect against theft or violence

Bank teller windows, often referred to as teller lines or transaction windows, are a critical interface between financial institutions and their customers. Among their most vital components is bulletproof glass, a security feature designed to protect employees from theft, violence, and other threats. This specialized glass is engineered to withstand high-impact forces, including gunfire, while maintaining clarity for effective communication. Its presence is a silent yet powerful deterrent, ensuring that even in high-risk situations, tellers remain shielded from harm.

From a technical standpoint, bulletproof glass used in teller windows is typically composed of multiple layers of glass and polycarbonate materials bonded together. This construction absorbs and disperses the energy from a projectile, preventing penetration. For instance, UL 752 is a common standard for bullet-resistant materials, rating them based on their ability to stop specific calibers of ammunition. Banks often opt for Level 1 or Level 3 protection, which can withstand handgun rounds or high-powered rifles, respectively. The choice depends on the institution’s risk assessment and location.

Implementing bulletproof glass in teller windows is not just about physical security; it’s also a psychological safeguard. Employees working behind these windows report feeling safer, which can improve job satisfaction and performance. However, it’s essential to balance security with customer experience. Modern designs incorporate features like speak-through panels and transaction drawers that allow for seamless interaction without compromising safety. Regular maintenance, such as checking for cracks or delamination, is crucial to ensure the glass remains effective over time.

When considering bulletproof glass for teller windows, banks must weigh cost against necessity. While the initial investment can be significant—ranging from $100 to $300 per square foot—the long-term benefits often outweigh the expense. For example, a single thwarted robbery can save an institution thousands in losses and reputational damage. Additionally, many insurance providers offer reduced premiums for banks with robust security measures, making it a financially prudent decision.

In conclusion, bulletproof glass in teller windows is more than a barrier; it’s a strategic investment in safety and trust. By understanding its composition, standards, and practical implications, banks can create a secure environment for both employees and customers. As threats evolve, so too must security measures, ensuring that teller windows remain a reliable line of defense in the financial world.

Citizens Bank Refund Timeline: What to Expect After Requesting

You may want to see also

Explore related products

$46.99

$46.99

![]()

Sliding Drawer Mechanism: Allows secure exchange of documents, cash, or items between teller and customer

Bank teller windows, often referred to as teller lines or transaction windows, are essential components of traditional banking infrastructure. Among their most distinctive features is the sliding drawer mechanism, a simple yet ingenious device designed to facilitate secure exchanges between tellers and customers. This mechanism, typically embedded within a reinforced glass or acrylic partition, serves as a discreet and protected channel for transferring cash, documents, or other items. Its design prioritizes both security and efficiency, ensuring that transactions occur smoothly while minimizing the risk of theft or tampering.

From a functional perspective, the sliding drawer mechanism operates on a straightforward principle: a small, enclosed tray moves back and forth through an opening in the teller window. The customer places their items into the drawer, which is then securely locked and slid to the teller’s side. Once the teller completes the transaction, they return the drawer with the necessary items, maintaining a physical barrier between both parties throughout the process. This system eliminates the need for direct hand-to-hand exchanges, reducing opportunities for errors or unauthorized access. For instance, a customer depositing a check or withdrawing cash can do so without exposing the transaction to onlookers, enhancing privacy and security.

Practical considerations for implementing a sliding drawer mechanism include material durability and ease of maintenance. The drawer itself is typically constructed from sturdy materials like metal or high-impact plastic to withstand frequent use and potential tampering. The sliding mechanism should be smooth yet secure, often incorporating locking features that activate when the drawer is in transit. Banks must also ensure the drawer’s size is adequate for common transaction items—envelopes, cash bundles, or small packages—while remaining compact enough to fit seamlessly into the window design. Regular maintenance, such as lubricating tracks and inspecting locks, is crucial to prevent malfunctions that could disrupt service.

Comparatively, the sliding drawer mechanism stands out against alternative transaction methods, such as pass-through slots or open-counter exchanges. Unlike slots, which may limit the size of items that can be exchanged, drawers accommodate bulkier objects without compromising security. Open-counter exchanges, while more personal, expose transactions to greater risk and reduce the physical separation between teller and customer. The drawer mechanism strikes a balance, preserving the human element of face-to-face interaction while providing a secure, controlled environment for exchanges. This makes it particularly valuable in high-traffic branches or areas with elevated security concerns.

In conclusion, the sliding drawer mechanism is a cornerstone of secure and efficient bank teller windows. Its design reflects a thoughtful blend of functionality, security, and user experience, addressing the unique challenges of financial transactions. By understanding its mechanics, benefits, and maintenance requirements, banks can optimize this tool to enhance customer trust and operational reliability. Whether in a bustling urban branch or a small-town credit union, the sliding drawer remains a testament to the enduring importance of simplicity and security in banking design.

Launching a Mobile-Only Bank: Essential Steps for Success

You may want to see also

Explore related products

![]()

Privacy Panels: Designed to block view from other customers for confidential transactions

Bank teller windows, often referred to as teller lines or transaction windows, are essential components of financial institutions, designed to facilitate secure and efficient customer interactions. Among their features, privacy panels stand out as a critical element, specifically engineered to block the view from other customers during confidential transactions. These panels are not merely decorative; they serve a functional purpose in maintaining discretion and trust in banking environments.

Consider the typical layout of a bank branch. Privacy panels are strategically placed between teller stations, often extending above the countertop to create a visual barrier. Their height and width are carefully calibrated to ensure that only the customer and teller can see the transaction details, such as account numbers, signatures, or cash exchanges. For example, panels are commonly 4 to 5 feet tall and 2 to 3 feet wide, providing ample coverage without obstructing the teller’s ability to assist multiple customers efficiently. This design balances openness and confidentiality, a key consideration in high-traffic banking spaces.

From a practical standpoint, installing privacy panels involves more than just measurement and placement. Materials like tempered glass, acrylic, or laminated wood are favored for their durability and ease of cleaning, as these surfaces frequently come into contact with documents, pens, and hands. Additionally, panels should comply with accessibility standards, ensuring they do not impede wheelchair access or create hazards for customers with visual impairments. Banks often consult architects or interior designers to integrate these panels seamlessly into their branch aesthetics while prioritizing functionality.

The psychological impact of privacy panels cannot be overstated. Customers are more likely to engage in sensitive transactions, such as loan applications or large cash withdrawals, when they feel their information is shielded from prying eyes. This sense of security fosters trust in the institution and encourages open communication between customers and tellers. In contrast, branches lacking adequate privacy measures may inadvertently discourage customers from conducting complex or personal transactions, potentially driving them to competitors or digital alternatives.

For banks looking to retrofit existing teller lines with privacy panels, a step-by-step approach is recommended. First, assess the current layout to identify high-traffic areas and transaction types that require the most discretion. Next, select materials and designs that align with the branch’s branding and accessibility requirements. Finally, schedule installation during off-peak hours to minimize disruption to customers and staff. By prioritizing privacy, banks not only enhance the customer experience but also reinforce their commitment to confidentiality and professionalism.

Step-by-Step Guide to Deactivating SBI Internet Banking Safely

You may want to see also

Explore related products

![]()

Transaction Counter Windows: Main point of interaction for in-branch banking services with customers

Bank teller windows, often referred to as transaction counter windows, serve as the primary interface between financial institutions and their customers within physical branches. These windows are more than just barriers; they are designed to facilitate secure, efficient, and personalized interactions. Typically made of reinforced glass for safety, they often include a small opening or tray for exchanging documents, cash, or cards. The design balances transparency—allowing customers to see the teller—with privacy, ensuring sensitive transactions remain discreet. This dual functionality underscores their role as both a point of service and a security feature.

From a customer experience perspective, transaction counter windows are the face of in-branch banking. Tellers behind these windows handle a range of tasks, from deposits and withdrawals to account inquiries and loan applications. The layout of these counters often reflects the bank’s commitment to accessibility, with lower windows or adjacent desks to accommodate customers with disabilities. Additionally, many modern branches incorporate digital displays or interactive screens into these windows, enabling customers to verify transactions or access additional services seamlessly. This blend of human interaction and technology enhances efficiency while maintaining a personal touch.

For banks, transaction counter windows are critical operational hubs. They are strategically positioned to optimize workflow, often located near cash vaults or back-office areas for quick access to resources. Tellers are trained to manage high-volume transactions during peak hours while ensuring accuracy and compliance with regulatory standards. The design of these windows also considers ergonomics, with adjustable heights and built-in communication systems to reduce strain on staff. By prioritizing both functionality and employee well-being, banks can deliver consistent service quality.

A comparative analysis reveals how transaction counter windows have evolved over time. Traditional designs focused solely on security, often featuring thick glass and limited interaction space. Today, however, banks prioritize customer-centric designs that foster trust and engagement. For instance, some branches now incorporate open-concept counters with partial barriers, encouraging face-to-face conversations. Others integrate biometric authentication systems directly into the window, streamlining identity verification for high-value transactions. These innovations reflect a shift from transactional efficiency to relationship-building.

Practical tips for optimizing transaction counter windows include regular maintenance checks to ensure sliding trays and communication systems function smoothly. Banks should also train staff to use the window’s features effectively, such as adjusting lighting to reduce glare on screens or utilizing built-in document scanners for faster processing. For customers, understanding the layout of these counters can expedite their visit—for example, knowing which windows handle cash transactions versus those for account services. By treating these windows as more than just physical barriers, both banks and customers can maximize their utility in delivering or receiving in-branch services.

Kickstart Your Banking Career: Post-12th Exam Preparation Guide

You may want to see also

Frequently asked questions

Those bank teller windows are commonly called teller windows or teller stations.

Yes, the glass barriers at bank teller windows are often referred to as teller bands or transaction windows.

In architectural terms, they are sometimes called teller counters or service windows.

The sliding tray, often called a transaction drawer or pass-through tray, is used to securely exchange documents, cash, or other items between the customer and the teller.