The repo market, short for the repurchase agreement market, is a critical component of the financial system, providing liquidity and facilitating short-term borrowing and lending among banks, financial institutions, and other market participants. In this market, institutions engage in repo transactions, where one party sells securities to another with an agreement to repurchase them at a later date, typically at a slightly higher price. Understanding which banks are actively participating in the repo market is essential, as these institutions play a pivotal role in maintaining market stability, managing interest rates, and ensuring the smooth flow of credit. Major global and domestic banks, including central banks, commercial banks, and investment banks, are key players in this market, each contributing to its depth and efficiency. Identifying these participants helps stakeholders gauge market dynamics, assess risk, and comprehend the broader implications of repo activities on the financial ecosystem.

Explore related products

What You'll Learn

![]()

Major U.S. banks active in repo market operations

The repo market, short for the repurchase agreement market, is a critical component of the financial system, providing liquidity and short-term funding for banks and other financial institutions. Among the most active participants in this market are major U.S. banks, which leverage repo transactions to manage their balance sheets, meet regulatory requirements, and facilitate broader market operations. These banks include JPMorgan Chase, Bank of America, Citigroup, Goldman Sachs, and Morgan Stanley, each playing a significant role in the repo market's daily functioning. Their involvement is not just a matter of scale but also of strategic importance, as they act as both borrowers and lenders, ensuring the market remains liquid and efficient.

Analyzing the role of these banks reveals a nuanced interplay between risk management and market influence. For instance, JPMorgan Chase, with its vast balance sheet and diverse portfolio, often acts as a primary dealer in repo transactions, providing liquidity to smaller institutions and government agencies. Similarly, Bank of America’s active participation helps stabilize the market during periods of stress, as seen during the 2019 repo market turmoil when it stepped in to provide much-needed funding. Citigroup, known for its global reach, uses the repo market to manage its international operations, while Goldman Sachs and Morgan Stanley leverage their expertise in securities trading to optimize their repo activities. Each bank’s approach reflects its unique business model and strategic priorities, yet all contribute to the market’s overall resilience.

To understand the practical implications of these banks’ involvement, consider the following steps: first, monitor their repo activity through financial disclosures and regulatory filings, as this provides insights into their liquidity positions and risk appetite. Second, track market rates and volumes, as spikes or declines often signal broader economic trends or stress points. Third, analyze the collateral used in repo transactions, typically high-quality securities like U.S. Treasuries, to gauge the banks’ risk management practices. For investors and market participants, staying informed about these dynamics is crucial, as it helps anticipate potential disruptions and opportunities in the financial system.

A comparative analysis highlights the competitive edge these banks gain through their repo market operations. For example, JPMorgan Chase’s dominance in the repo market complements its leadership in investment banking and asset management, creating a synergistic effect. In contrast, Goldman Sachs’ focus on trading and market-making allows it to capitalize on short-term arbitrage opportunities in the repo market. Meanwhile, Bank of America’s retail banking strength provides a stable funding base for its repo activities, reducing reliance on volatile wholesale markets. These differences underscore the strategic diversity among major U.S. banks and their ability to adapt to changing market conditions.

In conclusion, the active participation of major U.S. banks in the repo market is a cornerstone of financial stability and efficiency. Their roles as liquidity providers, risk managers, and market influencers are indispensable, particularly during times of economic uncertainty. By understanding their strategies, market participants can better navigate the complexities of the repo market and leverage its opportunities. Whether through direct involvement or indirect observation, the actions of these banks offer valuable lessons in financial management and market dynamics, making them a focal point for anyone interested in the inner workings of the U.S. financial system.

Mastering Extreme Turns: Understanding 90-Degree Bank in Paragliding

You may want to see also

Explore related products

![]()

Global banks participating in international repo transactions

Global banks are pivotal in the international repo market, facilitating liquidity and risk management across borders. Major players include JPMorgan Chase, Citigroup, and Bank of America, which leverage their extensive balance sheets and global networks to execute large-scale repo transactions. These institutions often act as both borrowers and lenders, depending on market conditions and their liquidity needs. For instance, during periods of heightened volatility, they may lend securities to stabilize funding pressures, while in calmer markets, they borrow to optimize their asset portfolios. Their participation underscores the repo market’s role as a critical tool for financial stability and operational efficiency.

Analyzing regional trends reveals that European banks like Deutsche Bank and BNP Paribas are equally active in international repo transactions, particularly in euro-denominated markets. These institutions often engage in cross-currency repos, swapping securities to manage currency exposure and meet regulatory requirements. Asian banks, such as ICBC and MUFG, are also significant participants, reflecting the growing importance of emerging markets in global finance. Their involvement highlights the repo market’s ability to bridge liquidity gaps between developed and developing economies, fostering interconnectedness in the global financial system.

A practical takeaway for market participants is the importance of understanding counterparty risk in international repo transactions. Global banks often rely on central clearinghouses like the Fixed Income Clearing Corporation (FICC) to mitigate this risk, but bilateral agreements remain common. Institutions should prioritize robust collateral management practices, ensuring that securities pledged in repos are of high quality and easily liquidatable. For example, government bonds and agency securities are preferred due to their low credit risk and high market acceptance. Additionally, monitoring regulatory changes, such as Basel III liquidity requirements, is essential to stay compliant and competitive.

Comparatively, smaller regional banks face challenges in accessing the international repo market due to limited balance sheets and operational capabilities. However, they can partner with larger global banks or utilize repo platforms like the General Collateral Finance Repo Service (GCF Repo) to participate indirectly. This approach allows them to benefit from the liquidity and risk management advantages of the repo market without the need for extensive infrastructure. For instance, a mid-sized European bank might borrow securities from JPMorgan Chase to meet short-term funding needs, demonstrating the market’s inclusivity and adaptability.

In conclusion, global banks’ participation in international repo transactions is a cornerstone of modern finance, enabling liquidity, risk management, and cross-border connectivity. By understanding the roles of major players, regional trends, and practical considerations, institutions can navigate this complex market effectively. Whether acting as a borrower, lender, or intermediary, the ability to leverage repo transactions strategically is a critical skill in today’s interconnected financial landscape.

Is Receipt Bank Free for Pro Advisors? Exploring Costs and Benefits

You may want to see also

Explore related products

![]()

Regional banks' role in the domestic repo market

Regional banks play a pivotal role in the domestic repo market by providing liquidity and stability to local economies. Unlike their larger counterparts, regional banks often have deeper ties to their communities, enabling them to channel funds efficiently into local businesses and municipalities. For instance, during periods of tight credit, regional banks can step in to provide short-term financing through repo agreements, ensuring that local entities maintain operational continuity. This localized focus not only supports economic resilience but also fosters trust among stakeholders who value personalized financial services.

To understand their impact, consider the mechanics of repo transactions. Regional banks act as both borrowers and lenders in the repo market, leveraging their asset portfolios to secure funding or provide liquidity. For example, a regional bank with a surplus of Treasury securities can lend them in a repo agreement, earning interest while maintaining a low-risk position. Conversely, when in need of cash, the same bank can borrow funds by temporarily exchanging high-quality collateral. This dual role underscores their flexibility and adaptability in managing liquidity, a critical function in maintaining financial stability.

However, regional banks face unique challenges in the repo market. Their smaller size often limits access to the same volume of high-quality collateral as larger institutions, which can restrict their participation in larger repo transactions. Additionally, regulatory requirements, such as liquidity coverage ratios, may impose stricter constraints on regional banks, forcing them to allocate more resources to compliance rather than active market participation. Despite these hurdles, many regional banks have innovated by forming consortia or partnering with larger institutions to pool resources and enhance their repo market presence.

A practical takeaway for regional banks is to focus on niche opportunities within the repo market. For instance, they can specialize in providing repo financing to local government entities or small-to-medium enterprises (SMEs), where their community-centric approach gives them a competitive edge. By tailoring their services to meet specific local needs, regional banks can carve out a sustainable role in the repo market while strengthening their broader financial ecosystem. This strategy not only maximizes their impact but also aligns with their core mission of supporting regional economic growth.

In conclusion, regional banks are indispensable participants in the domestic repo market, offering localized expertise and flexibility that larger institutions often lack. While they face challenges related to scale and regulation, their ability to innovate and focus on niche opportunities ensures their continued relevance. By leveraging their community ties and adapting to market dynamics, regional banks can effectively contribute to liquidity management and economic stability, proving that size is not the sole determinant of influence in the financial landscape.

Jill Wine-Banks' Age and Marital Status: Unveiling Her Personal Life

You may want to see also

![]()

Central banks' involvement in repo market stabilization

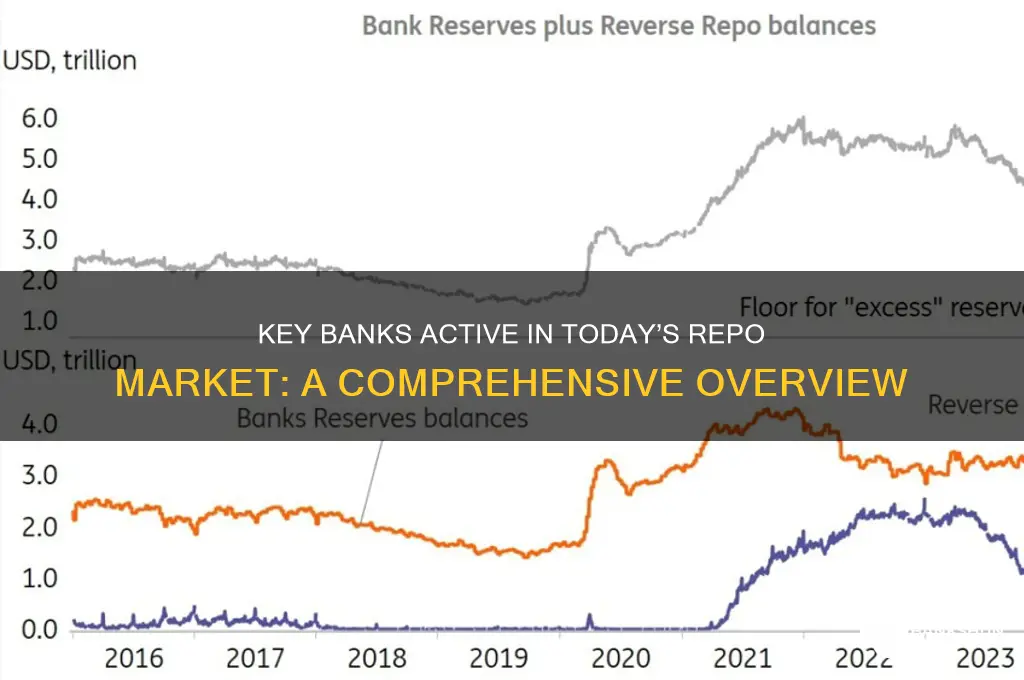

Central banks play a pivotal role in stabilizing the repo market, a critical component of the financial system that facilitates short-term borrowing and lending between banks and other financial institutions. Their involvement is not merely reactive but is often proactive, aimed at ensuring liquidity, maintaining market confidence, and preventing systemic risks. For instance, during periods of market stress, central banks like the Federal Reserve, the European Central Bank, and the Bank of Japan step in to provide liquidity through repo operations, effectively acting as lenders of last resort. This intervention is crucial in calming markets and preventing a liquidity crunch that could cascade into broader financial instability.

One of the primary tools central banks use to stabilize the repo market is open market operations, where they buy or sell securities to adjust the supply of reserve balances in the banking system. For example, the Federal Reserve conducts overnight and term repurchase agreements to inject liquidity into the market. During the 2019 repo market turmoil, the Fed increased its repo operations, offering hundreds of billions of dollars in short-term loans to alleviate funding pressures. Similarly, the European Central Bank has utilized its repo facilities to ensure that eurozone banks have access to sufficient liquidity, particularly during periods of heightened uncertainty.

However, central bank involvement in repo market stabilization is not without challenges. Over-reliance on central bank liquidity can create moral hazard, encouraging market participants to take excessive risks under the assumption that the central bank will always intervene. To mitigate this, central banks often impose strict collateral requirements and limit the duration and size of their repo operations. For instance, the Fed accepts only high-quality collateral, such as U.S. Treasury securities, and sets clear terms for its repo agreements to discourage dependency.

A comparative analysis reveals that central banks in different regions adopt varying strategies based on their unique market structures and regulatory frameworks. While the Fed focuses on direct repo operations, the Bank of Japan integrates its repo activities with its broader quantitative easing program, using the repo market as a channel to inject liquidity into the economy. In contrast, the People’s Bank of China employs a more targeted approach, using repo operations to manage short-term interest rates and support specific sectors of the economy.

In conclusion, central banks are indispensable in stabilizing the repo market, employing a mix of open market operations, collateral requirements, and strategic interventions to maintain liquidity and market confidence. Their role is both reactive and preventive, addressing immediate funding pressures while fostering a resilient financial system. As the repo market continues to evolve, central banks must remain vigilant, adapting their strategies to new challenges and ensuring that their interventions do not inadvertently encourage risky behavior. Practical tips for market participants include closely monitoring central bank announcements, maintaining high-quality collateral, and diversifying funding sources to reduce reliance on repo markets during times of stress.

How to Obtain Your Vehicle Title from the Bank: A Step-by-Step Guide

You may want to see also

![]()

Investment banks' utilization of repo agreements for liquidity

Investment banks are pivotal participants in the repo market, leveraging repurchase agreements (repos) as a strategic tool to manage liquidity and optimize their balance sheets. These short-term collateralized loans allow banks to borrow cash by temporarily selling securities, with an agreement to repurchase them at a later date, typically overnight or within a few days. This mechanism provides immediate liquidity, enabling banks to meet regulatory requirements, fund trading activities, or cover short-term obligations without liquidating long-term assets.

Consider the operational mechanics: an investment bank with a portfolio of Treasury bonds can enter a repo agreement with a counterparty, such as a money market fund or another bank, to secure cash. The bank sells the bonds at a discount, receives cash, and agrees to repurchase the bonds at a slightly higher price, effectively paying interest on the borrowed funds. This process is highly efficient, with settlement often occurring within hours, making repos a preferred liquidity management tool for banks operating in fast-paced financial markets.

However, the utilization of repos is not without risks. The 2008 financial crisis highlighted the dangers of over-reliance on repo markets, as a sudden loss of confidence led to a liquidity freeze. Investment banks, such as Lehman Brothers, faced severe funding pressures when counterparties refused to renew repo agreements, exacerbating their financial distress. This underscores the importance of robust risk management frameworks, including diversification of funding sources and stress testing, to mitigate potential repo market disruptions.

To illustrate, major investment banks like JPMorgan Chase, Goldman Sachs, and Citigroup are active participants in the repo market, often acting as both borrowers and lenders. These institutions use repos to manage intraday liquidity needs, particularly during periods of market volatility. For instance, during the COVID-19 pandemic, the Federal Reserve expanded its repo operations to ensure market stability, demonstrating the critical role of repos in maintaining financial system resilience.

In conclusion, investment banks’ utilization of repo agreements for liquidity is a double-edged sword. While repos offer unparalleled flexibility and efficiency in managing short-term funding needs, they also expose banks to counterparty and market risks. By adopting prudent practices, such as maintaining high-quality collateral and monitoring market conditions, banks can harness the benefits of repos while safeguarding against potential pitfalls. This delicate balance is essential for sustaining liquidity and stability in the broader financial ecosystem.

A Cashless Society: Imagining America Without Banks and Financial Institutions

You may want to see also

Frequently asked questions

The repo market (repurchase agreement market) is a critical component of the financial system where banks and other institutions borrow and lend cash for short periods, typically overnight, using securities as collateral. It helps maintain liquidity, manage interest rates, and ensure the smooth functioning of financial markets.

Major banks such as JPMorgan Chase, Bank of America, Citigroup, Goldman Sachs, and Morgan Stanley are active participants in the repo market. These institutions play a key role in providing liquidity and facilitating transactions.

Yes, regional and smaller banks also participate in the repo market, though their involvement may be less prominent compared to larger institutions. They use the repo market to manage their short-term funding needs and maintain liquidity.

Yes, international banks with U.S. operations, such as Deutsche Bank, Credit Suisse, and Barclays, actively participate in the U.S. repo market. Their involvement helps connect global financial markets and enhance liquidity.