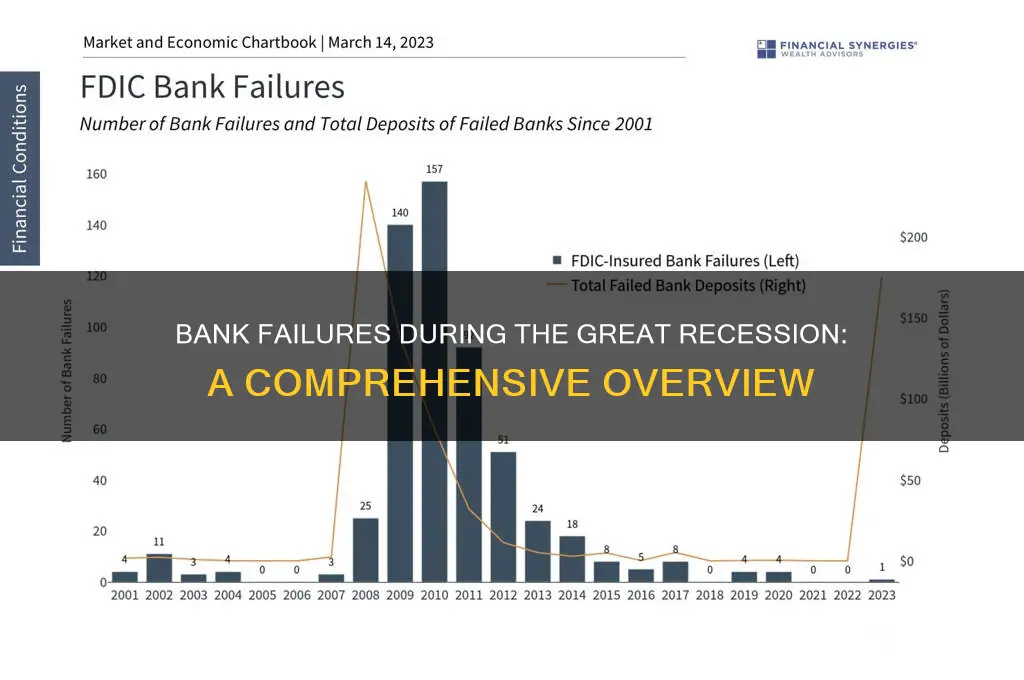

The Great Recession, which spanned from 2007 to 2009, was marked by a severe global financial crisis that led to the failure of numerous banks and financial institutions. Triggered by the collapse of the U.S. housing market and the subsequent subprime mortgage crisis, the downturn exposed vulnerabilities in the banking sector, including excessive risk-taking, inadequate regulation, and over-leveraging. Among the most notable bank failures during this period were Lehman Brothers, whose bankruptcy in September 2008 became a symbol of the crisis, and Washington Mutual, which remains the largest bank failure in U.S. history. Other institutions, such as Bear Stearns and IndyMac, also succumbed to the financial pressures, prompting government interventions and bailouts to stabilize the economy and prevent further systemic collapse. These failures underscored the interconnectedness of global financial markets and the need for stronger regulatory frameworks to mitigate future risks.

Explore related products

$47.63 $78

$12 $32

What You'll Learn

- Washington Mutual collapse: largest US bank failure, seized by regulators in 2008

- Wachovia downfall: acquired by Wells Fargo amid liquidity crisis in 2008

- IndyMac bankruptcy: mortgage lender failed due to subprime lending losses in 2008

- Lehman Brothers collapse: iconic investment bank filed for bankruptcy in September 2008

- Bank of America struggles: acquired Merrill Lynch to avoid failure during the crisis

![]()

Washington Mutual collapse: largest US bank failure, seized by regulators in 2008

The Washington Mutual collapse in 2008 stands as a stark reminder of the fragility of financial institutions during economic downturns. As the largest bank failure in U.S. history at the time, it sent shockwaves through the financial sector and highlighted systemic vulnerabilities. Washington Mutual, affectionately known as WaMu, had been a cornerstone of American banking, boasting over 2,200 branches and $307 billion in assets. Yet, its aggressive push into subprime mortgage lending during the housing boom ultimately sealed its fate. By September 2008, a liquidity crisis forced regulators to seize the bank, marking a pivotal moment in the Great Recession.

To understand the collapse, consider the bank’s business model. WaMu prioritized rapid growth over risk management, offering adjustable-rate mortgages to borrowers with poor credit histories. These loans were then bundled into mortgage-backed securities and sold to investors, generating substantial short-term profits. However, when the housing market crashed, defaults soared, and the value of these securities plummeted. Depositors, fearing losses, began withdrawing funds en masse, draining WaMu’s liquidity reserves. Despite efforts to secure capital, the bank’s inability to meet obligations left regulators with no choice but to intervene.

The seizure of Washington Mutual offers critical lessons for both financial institutions and consumers. For banks, it underscores the importance of prudent risk management and diversified revenue streams. Overreliance on volatile markets, like subprime mortgages, can lead to catastrophic outcomes. Consumers, meanwhile, should remain vigilant about the stability of their financial institutions and diversify their assets to mitigate risk. The Federal Deposit Insurance Corporation (FDIC) insured WaMu’s deposits up to $250,000, protecting most account holders, but the collapse still disrupted millions of lives.

Comparatively, WaMu’s failure differs from other bank collapses during the Great Recession in its scale and public impact. While institutions like Lehman Brothers and Bear Stearns dominated headlines, WaMu’s retail focus made its downfall more tangible for everyday Americans. Its acquisition by JPMorgan Chase for $1.9 billion just days after the seizure prevented a deeper crisis, but the episode exposed the dangers of unchecked lending practices. Unlike investment banks, WaMu’s collapse directly affected Main Street, serving as a cautionary tale about the interconnectedness of financial systems.

In practical terms, the Washington Mutual collapse should prompt individuals to monitor their bank’s health indicators, such as capital adequacy ratios and loan delinquency rates. Tools like the FDIC’s BankFind Suite can provide insights into an institution’s stability. Additionally, maintaining emergency funds outside of banks and investing in diversified portfolios can reduce vulnerability to systemic shocks. For policymakers, WaMu’s failure reinforces the need for stricter regulatory oversight and stress testing to prevent similar crises. By learning from this historic event, stakeholders can build a more resilient financial ecosystem.

Are Bank Charges Considered Part of Finance Costs?

You may want to see also

Explore related products

![A Summary of Savings Banks That Have Failed in the State of New York, by Willis S. Paine 1906 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Wachovia downfall: acquired by Wells Fargo amid liquidity crisis in 2008

The 2008 financial crisis exposed vulnerabilities in the banking sector, leading to the collapse or acquisition of several major institutions. Among these, Wachovia's downfall stands out as a cautionary tale of aggressive growth, risky lending practices, and the devastating impact of a liquidity crisis.

A Recipe for Disaster: Wachovia's Expansion Strategy

Wachovia's rapid expansion through acquisitions, particularly its 2006 purchase of Golden West Financial, a specialist in adjustable-rate mortgages, proved to be a fatal misstep. This move significantly increased Wachovia's exposure to the subprime mortgage market, a sector already showing signs of distress. As the housing bubble burst, Wachovia found itself holding a toxic portfolio of deteriorating loans, leading to massive write-downs and eroding investor confidence.

The bank's reliance on short-term funding, such as commercial paper, further exacerbated its vulnerability. When the credit markets froze in 2008, Wachovia faced a severe liquidity crunch, unable to roll over its maturing debt. This liquidity crisis, coupled with mounting losses from its mortgage portfolio, pushed Wachovia to the brink of collapse.

Wells Fargo to the Rescue: A Forced Marriage

Facing imminent failure, Wachovia was acquired by Wells Fargo in a government-brokered deal in October 2008. The acquisition, valued at $15.1 billion, was a lifeline for Wachovia, preventing a potential systemic collapse. However, it came at a significant cost. Wells Fargo inherited Wachovia's troubled assets, including its toxic mortgage portfolio, which required substantial write-downs and restructuring.

Lessons Learned: The Aftermath of Wachovia's Downfall

Wachovia's downfall highlights several key lessons for the banking industry. Firstly, aggressive growth strategies, particularly through acquisitions, can mask underlying risks and vulnerabilities. Secondly, over-reliance on short-term funding leaves banks susceptible to liquidity crises during times of market stress. Lastly, the acquisition of Wachovia by Wells Fargo underscores the importance of government intervention in preventing systemic failures, but also raises questions about moral hazard and the potential for taxpayer-funded bailouts.

Practical Takeaways for Investors and Regulators

For investors, Wachovia's story serves as a reminder to scrutinize banks' lending practices, funding sources, and risk management strategies. Diversification and a focus on institutions with strong capital positions and conservative lending practices can mitigate exposure to similar risks. Regulators, on the other hand, must prioritize stricter oversight of banks' risk management frameworks, particularly regarding complex financial products and reliance on short-term funding. Stress testing and contingency planning are essential tools to ensure banks' resilience during periods of market turmoil. By learning from Wachovia's downfall, stakeholders can work towards a more stable and resilient financial system.

Prosperity Bank Hours: When to Visit for Your Banking Needs

You may want to see also

Explore related products

$7.78 $16.99

![]()

IndyMac bankruptcy: mortgage lender failed due to subprime lending losses in 2008

The IndyMac bankruptcy stands as a stark reminder of the dangers of unchecked subprime lending. In July 2008, this California-based mortgage lender collapsed under the weight of billions in losses tied to risky loans. Its failure marked the second-largest bank collapse in U.S. history at the time, sending shockwaves through the financial system and foreshadowing the depths of the Great Recession.

IndyMac's downfall wasn't an isolated incident. It was a symptom of a broader disease: the subprime mortgage crisis. Lenders, fueled by a booming housing market and lax regulations, had been aggressively pushing loans to borrowers with poor credit histories. These "subprime" loans often came with adjustable rates that started low but ballooned over time, trapping borrowers in unaffordable payments. When the housing bubble burst, home values plummeted, and borrowers defaulted en masse, leaving lenders like IndyMac holding the bag.

Imagine a house of cards built on shaky foundations. That was IndyMac's business model. They relied heavily on Alt-A loans, a type of subprime mortgage that required little to no documentation of income or assets. This "liar loans" approach attracted borrowers who couldn't afford the mortgages, but it also inflated IndyMac's loan portfolio, creating a facade of success. When the market turned, this facade crumbled, revealing a mountain of bad debt.

The IndyMac bankruptcy wasn't just a financial failure; it was a human tragedy. Thousands of employees lost their jobs, and countless homeowners faced foreclosure. The fallout also eroded public trust in the financial system, contributing to the panic that gripped the markets during the Great Recession.

The IndyMac story serves as a cautionary tale about the perils of predatory lending and the importance of responsible financial practices. It highlights the need for stricter regulations, better consumer protection, and a more sustainable approach to mortgage lending. By learning from IndyMac's mistakes, we can strive to build a more resilient and equitable financial system, one that serves the needs of all, not just the few.

Elizabeth Banks: Game Show Host or Hollywood Star?

You may want to see also

Explore related products

![]()

Lehman Brothers collapse: iconic investment bank filed for bankruptcy in September 2008

The collapse of Lehman Brothers in September 2008 remains one of the most iconic and consequential events of the Great Recession. As the fourth-largest investment bank in the United States, its bankruptcy sent shockwaves through global financial markets, marking a turning point in the crisis. Unlike other bank failures during this period, Lehman’s downfall was not a quiet liquidation but a dramatic, public unraveling that exposed the fragility of the financial system. Its $613 billion in assets made it the largest bankruptcy filing in U.S. history at the time, dwarfing those of other failed institutions like Washington Mutual and IndyMac. This event was not merely a failure of a single bank but a symbol of the systemic risks embedded in subprime mortgage lending, excessive leverage, and regulatory oversight gaps.

Analyzing the collapse reveals a cascade of missteps and external pressures. Lehman Brothers had aggressively invested in mortgage-backed securities, a strategy that proved disastrous as the housing market cratered. By mid-2008, the bank’s balance sheet was laden with toxic assets, and its attempts to offload them or secure a bailout failed. The Federal Reserve and Treasury Department, wary of moral hazard after rescuing Bear Stearns earlier that year, declined to intervene. This decision, while intended to discourage reckless behavior, instead triggered a panic. The bank’s bankruptcy on September 15, 2008, froze credit markets, accelerated the global financial crisis, and underscored the interconnectedness of modern finance. It was a stark reminder that even institutions deemed "too big to fail" could, in fact, collapse.

From a practical standpoint, the Lehman Brothers collapse offers critical lessons for investors, policymakers, and financial institutions. First, diversification and risk management are paramount. Lehman’s overreliance on a single market (housing) left it vulnerable to a downturn. Investors should scrutinize portfolio concentrations and stress-test assets against adverse scenarios. Second, transparency and accountability are essential. Lehman’s use of accounting gimmicks, such as Repo 105, to mask its true financial condition eroded trust and exacerbated its downfall. Regulators must enforce stricter reporting standards, while institutions should prioritize ethical practices. Finally, systemic risks require proactive mitigation. The failure to rescue Lehman highlighted the need for a coordinated crisis response framework, which later informed policies like Dodd-Frank and the establishment of the Financial Stability Oversight Council.

Comparatively, Lehman’s collapse stands apart from other bank failures during the Great Recession due to its global impact and symbolic significance. While Washington Mutual’s collapse was larger in terms of assets, it was a commercial bank whose failure was contained through a swift sale to JPMorgan Chase. IndyMac, though a high-profile casualty, was a regional player with limited systemic reach. Lehman, however, was a global investment bank whose bankruptcy triggered a chain reaction, from the collapse of money market funds to the near-failure of AIG. Its downfall exposed the dangers of shadow banking and the inadequacy of existing regulatory frameworks, prompting a reevaluation of financial oversight worldwide. This distinction makes Lehman’s collapse not just a historical event but a case study in the consequences of unchecked risk-taking.

In conclusion, the Lehman Brothers collapse serves as a cautionary tale and a call to action. It demonstrated how the failure of a single institution could destabilize the entire financial system, underscoring the need for robust regulation, prudent risk management, and systemic resilience. For individuals, it highlights the importance of vigilance and diversification in investment strategies. For policymakers, it reinforces the necessity of proactive measures to prevent and manage crises. As we reflect on the Great Recession, Lehman’s bankruptcy remains a stark reminder of the interconnectedness of global finance and the enduring impact of decisions made in moments of crisis. Its legacy continues to shape financial practices and policies, ensuring that such a collapse is never repeated.

Understanding KYC Documents: Essential Requirements for Bank Account Verification

You may want to see also

Explore related products

![]()

Bank of America struggles: acquired Merrill Lynch to avoid failure during the crisis

The 2008 financial crisis exposed deep vulnerabilities within the banking sector, with several institutions teetering on the brink of collapse. While some banks failed outright, others survived through strategic acquisitions that masked their own weaknesses. Bank of America’s purchase of Merrill Lynch in 2008 exemplifies this dynamic, revealing how one of the nation’s largest banks used a high-profile merger to avert its own potential failure. At first glance, the acquisition appeared to be a bold move to expand Bank of America’s investment banking capabilities. However, a closer examination uncovers a desperate attempt to shore up its balance sheet amid mounting losses tied to toxic mortgage assets.

Consider the context: by late 2008, Bank of America was hemorrhaging capital due to its exposure to subprime mortgages and the collapse of the housing market. Merrill Lynch, though prestigious, was equally distressed, holding billions in deteriorating assets. The merger, announced in September 2008, was framed as a transformative deal, but internal documents later revealed that Bank of America’s leadership viewed it as a lifeline. Without the acquisition, the bank risked facing the same fate as Lehman Brothers, which had filed for bankruptcy just days earlier. This strategic maneuver highlights the lengths to which banks went to survive the crisis, often at the expense of transparency and long-term stability.

From a tactical standpoint, the acquisition allowed Bank of America to absorb Merrill Lynch’s losses while presenting a facade of strength. However, this came at a steep cost. The deal required a massive government bailout, with Bank of America receiving $45 billion in Troubled Asset Relief Program (TARP) funds. Additionally, the merger exposed significant cultural and operational incompatibilities between the two firms, leading to years of integration challenges. Shareholders suffered as well, with Bank of America’s stock price plummeting in the aftermath of the deal. This case underscores the risks of using mergers as a crisis management tool, particularly when the underlying issues remain unaddressed.

Comparatively, other banks that failed during the Great Recession, such as Washington Mutual and Wachovia, lacked the opportunity or means to orchestrate such a rescue. Bank of America’s ability to acquire Merrill Lynch was a testament to its size and political influence, but it also revealed the systemic flaws that allowed troubled institutions to consolidate rather than fail. This approach raised ethical questions about moral hazard, as it incentivized risky behavior under the assumption that "too big to fail" banks would be rescued. For policymakers and investors, the episode serves as a cautionary tale about the dangers of allowing distressed institutions to merge without addressing their core problems.

In practical terms, the Bank of America-Merrill Lynch merger offers several takeaways for navigating financial crises. First, transparency is critical; hiding weaknesses through acquisitions only delays inevitable reckoning. Second, regulators must scrutinize mergers during crises to ensure they do not perpetuate systemic risks. Finally, banks should focus on strengthening their core operations rather than pursuing growth through acquisitions in times of distress. While Bank of America survived the Great Recession, its struggles illustrate the high costs of using mergers as a band-aid solution. Understanding this case provides valuable insights into the complexities of crisis management in the banking sector.

US Bank and BBVA Compass: Exploring Their Affiliation and Connection

You may want to see also

Frequently asked questions

Several major banks failed or were acquired during the Great Recession, including Washington Mutual (the largest bank failure in U.S. history at the time), Wachovia, and IndyMac.

Banks failed primarily due to the collapse of the housing market, risky mortgage lending practices, and the proliferation of toxic assets like mortgage-backed securities.

Yes, many banks received government bailouts through the Troubled Asset Relief Program (TARP), including Bank of America, Citigroup, and JPMorgan Chase.

The collapse of Lehman Brothers in September 2008 marked a turning point in the Great Recession, triggering a global financial crisis, freezing credit markets, and accelerating the economic downturn.