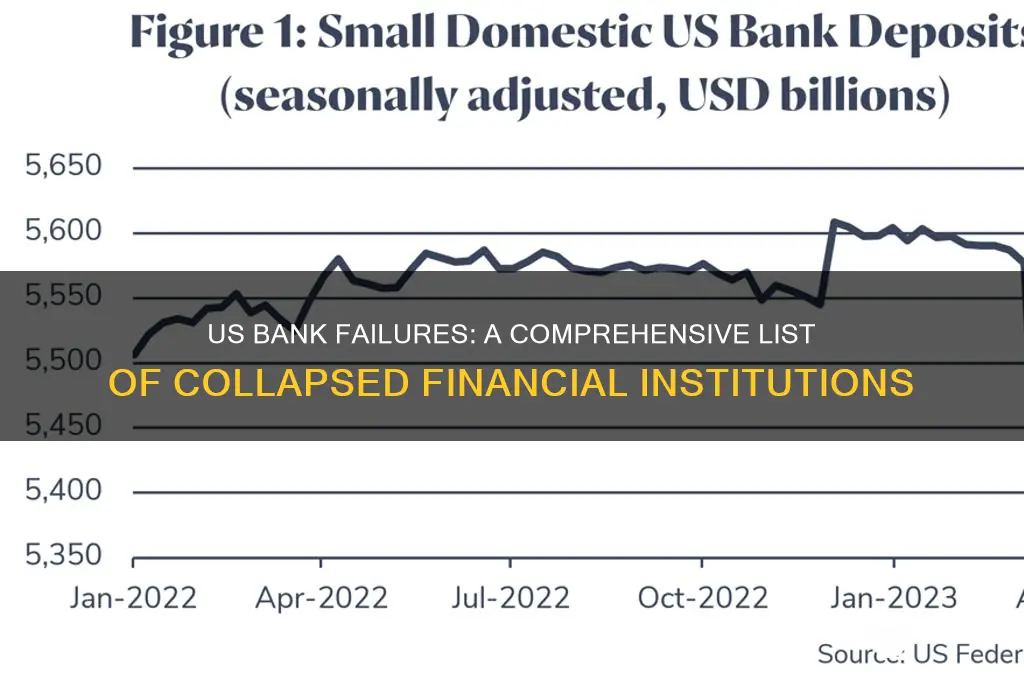

The United States has witnessed several significant bank collapses throughout its history, often triggered by economic downturns, risky lending practices, or systemic financial crises. Notable examples include the failure of Washington Mutual in 2008 during the Great Recession, which remains the largest bank collapse in U.S. history, and the more recent collapse of Silicon Valley Bank in 2023, which sent shockwaves through the tech and financial sectors. These events highlight vulnerabilities within the banking system and often lead to regulatory reforms aimed at preventing future failures. Understanding which banks have collapsed provides insight into the broader economic challenges and the resilience of the financial system.

| Characteristics | Values |

|---|---|

| Number of Bank Failures (2008-2023) | Over 500 banks failed during the financial crisis and its aftermath. |

| Largest Bank Failure | Washington Mutual (2008) - $307 billion in assets. |

| Recent Notable Failures | Silicon Valley Bank (2023), Signature Bank (2023), First Republic Bank (2023). |

| Primary Causes | Subprime mortgage crisis (2008), economic downturns, risk management failures, liquidity issues. |

| Regulatory Response | Increased oversight, Dodd-Frank Act (2010), FDIC insurance limits raised. |

| Impact on Economy | Loss of consumer confidence, tightened credit, increased unemployment. |

| FDIC Role | Protected depositors up to $250,000 per account. |

| Recovery Efforts | Bailouts, TARP (Troubled Asset Relief Program), bank mergers/acquisitions. |

| Long-Term Effects | Stricter banking regulations, reduced risk-taking, slower economic growth. |

| Notable Banks Acquired | Washington Mutual (by JPMorgan Chase), Wachovia (by Wells Fargo). |

Explore related products

What You'll Learn

- Bank Failures: Silicon Valley Bank, Signature Bank, and First Republic Bank closures

- Financial Crisis: Major collapses, including Washington Mutual and Wachovia

- Savings and Loan Crisis: Over 1,000 banks failed in the 1980s and early 1990s

- Great Depression Era: Thousands of banks collapsed between 1929 and 1933

- FDIC Role: How the Federal Deposit Insurance Corporation handles bank failures and protects depositors

![]()

2023 Bank Failures: Silicon Valley Bank, Signature Bank, and First Republic Bank closures

The year 2023 marked a significant turning point in the U.S. banking sector with the rapid and high-profile collapses of Silicon Valley Bank (SVB), Signature Bank, and First Republic Bank. These failures, occurring within weeks of each other, sent shockwaves through financial markets and raised questions about the stability of regional banks. SVB’s downfall began with a liquidity crisis triggered by depositors withdrawing funds en masse, a run exacerbated by its concentrated exposure to the tech and venture capital sectors. Signature Bank, heavily tied to cryptocurrency and real estate, followed suit, while First Republic Bank, despite initial rescue efforts, succumbed to similar pressures. Together, these closures highlighted vulnerabilities in risk management, depositor confidence, and regulatory oversight.

Analyzing the root causes reveals a common thread: mismatches between asset and liability structures. SVB, for instance, invested heavily in long-term Treasury bonds, leaving it exposed when interest rates rose and depositors sought higher returns elsewhere. Signature Bank’s reliance on volatile sectors like crypto amplified its risk profile, while First Republic’s high concentration of uninsured deposits made it particularly susceptible to panic withdrawals. These banks’ inability to quickly liquidate assets without incurring substantial losses underscored the dangers of misaligned balance sheets. For financial institutions, the takeaway is clear: diversification and stress testing are not optional but essential for survival in a dynamic economic environment.

From a regulatory perspective, the 2023 bank failures prompted urgent calls for reform. The Federal Deposit Insurance Corporation (FDIC) and the Federal Reserve faced scrutiny for not identifying these risks sooner. Policymakers are now reconsidering deposit insurance limits, currently capped at $250,000, and exploring stricter liquidity requirements for mid-sized banks. For consumers, these events serve as a reminder to monitor bank health indicators, such as capital adequacy ratios and asset diversification, and to spread large deposits across multiple institutions to mitigate risk. Practical tip: Use tools like Bankrate or the FDIC’s BankFind suite to assess a bank’s financial stability before committing funds.

Comparatively, the 2023 failures differ from the 2008 financial crisis in scale but share similarities in systemic risk. While 2008 was driven by widespread mortgage defaults and securitization, 2023’s collapses were more localized yet equally disruptive. The swift government intervention, including FDIC guarantees and acquisitions by larger banks, prevented a broader contagion. However, the speed and severity of these failures underscore the interconnectedness of modern finance. For investors, this is a cautionary tale: even seemingly stable institutions can falter under the right conditions. Diversification across asset classes and regular portfolio reviews are critical to safeguarding wealth.

Finally, the closures of SVB, Signature Bank, and First Republic Bank offer a sobering lesson in the importance of transparency and communication. All three banks struggled to reassure depositors and investors amid mounting uncertainty, accelerating their declines. Financial institutions must prioritize clear, proactive messaging during crises to maintain trust. For depositors, staying informed and acting decisively—whether by diversifying holdings or seeking insured accounts—can mitigate potential losses. As the banking sector adapts to these lessons, individuals and businesses alike must remain vigilant, recognizing that even in a regulated environment, risk is ever-present.

Securing Your E-Bank: Understanding Online Banking Protection Measures

You may want to see also

Explore related products

![]()

2008 Financial Crisis: Major collapses, including Washington Mutual and Wachovia

The 2008 financial crisis remains one of the most devastating economic events in modern history, marked by the collapse of several major financial institutions. Among these, Washington Mutual (WaMu) and Wachovia stand out as prime examples of how the subprime mortgage crisis and subsequent credit crunch led to their downfall. WaMu, once the largest savings and loan association in the U.S., filed for bankruptcy in September 2008, becoming the largest bank failure in American history at the time. Its collapse was fueled by aggressive lending practices and a heavy exposure to risky mortgage-backed securities. Wachovia, another banking giant, faced a similar fate due to its acquisition of Golden West Financial, a company deeply entrenched in adjustable-rate mortgages. By October 2008, Wachovia was acquired by Wells Fargo in a government-encouraged deal to prevent its outright collapse.

Analyzing these failures reveals a common thread: the overreliance on subprime mortgages and the assumption that housing prices would continue to rise indefinitely. WaMu’s "Option ARM" loans, which allowed borrowers to pay less than the accruing interest, created a ticking time bomb of defaults. Wachovia’s Golden West acquisition amplified its exposure to these toxic assets, leaving it vulnerable when the housing market crashed. Both banks were also heavily dependent on short-term funding, such as repurchase agreements, which dried up during the credit freeze. This liquidity crisis turned a solvency issue into an existential threat, forcing regulators to intervene.

From a regulatory perspective, the collapses of WaMu and Wachovia underscored the need for stricter oversight and risk management practices. The Dodd-Frank Wall Street Reform and Consumer Protection Act, enacted in 2010, was a direct response to these failures, introducing measures like stress testing and higher capital requirements. For investors and consumers, these events serve as a cautionary tale about the dangers of unchecked risk-taking and the importance of diversification. Practical steps for individuals include maintaining an emergency fund, avoiding excessive debt, and scrutinizing financial products for hidden risks.

Comparatively, the collapses of WaMu and Wachovia differ from other 2008 failures, such as Lehman Brothers, in their focus on retail banking rather than investment banking. While Lehman’s downfall was a dramatic Wall Street collapse, WaMu and Wachovia’s failures had a more direct impact on Main Street, affecting millions of depositors and mortgage holders. This distinction highlights the systemic nature of the crisis, which spanned both the high-stakes world of investment banking and the everyday operations of consumer banking.

In conclusion, the collapses of Washington Mutual and Wachovia during the 2008 financial crisis illustrate the catastrophic consequences of reckless lending and inadequate risk management. These events not only reshaped the banking industry but also left lasting lessons for regulators, investors, and consumers. By understanding the specific factors that led to their downfall, we can better prepare for future financial challenges and work toward a more resilient economic system.

Trump's Debt: Unraveling His Financial Ties to Bank of China

You may want to see also

Explore related products

![]()

Savings and Loan Crisis: Over 1,000 banks failed in the 1980s and early 1990s

Between 1980 and 1995, the United States witnessed the collapse of over 1,000 savings and loan associations (S&Ls), a crisis that cost taxpayers an estimated $160 billion. This period, known as the Savings and Loan Crisis, was marked by a perfect storm of deregulation, risky investments, and economic downturns. S&Ls, traditionally conservative institutions focused on home mortgages, found themselves suddenly free to engage in speculative ventures after the Depository Institutions Deregulation and Monetary Control Act of 1980. This newfound freedom, combined with rising interest rates and a slumping real estate market, proved disastrous for many institutions.

As interest rates soared in the early 1980s, S&Ls faced a dire situation. Their long-term, fixed-rate mortgages were yielding lower returns than the high interest rates they had to pay on deposits. This "interest rate risk" left many S&Ls struggling to stay afloat. Desperate to maintain profitability, some institutions turned to increasingly risky investments, including commercial real estate ventures and junk bonds. The gamble backfired spectacularly when the real estate market crashed in the late 1980s, leaving S&Ls holding the bag on billions of dollars in bad loans.

The crisis wasn't merely a result of bad luck or poor decisions; it was also a failure of regulatory oversight. The Federal Home Loan Bank Board, tasked with supervising S&Ls, was understaffed and ill-equipped to handle the rapid changes in the industry. Lax enforcement and political pressure further hindered effective regulation, allowing problematic practices to continue unchecked. The result was a cascade of failures, with S&Ls collapsing at an alarming rate, eroding public confidence in the financial system and necessitating a massive government bailout.

The Savings and Loan Crisis serves as a stark reminder of the dangers of unchecked deregulation and the importance of robust financial oversight. It highlights the need for regulators to adapt to changing market conditions and to prioritize consumer protection over industry interests. While the crisis was ultimately resolved through a combination of government intervention and industry restructuring, its legacy continues to shape financial regulations and inform our understanding of the inherent risks within the banking system.

How Treasury Bills Impact Bank Reserves and Monetary Policy

You may want to see also

Explore related products

![]()

Great Depression Era: Thousands of banks collapsed between 1929 and 1933

Between 1929 and 1933, the United States witnessed an unprecedented wave of bank failures, with over 9,000 banks collapsing during the Great Depression. This period marked a catastrophic loss of public trust in the financial system, as depositors rushed to withdraw their funds, triggering a vicious cycle of bank runs and insolvencies. The sheer scale of these failures underscores the fragility of the banking sector during this era, which was characterized by inadequate regulation, speculative lending, and a lack of deposit insurance. This crisis not only devastated individual savers but also crippled the economy, as credit dried up and businesses struggled to operate.

Analyzing the causes of these bank collapses reveals a perfect storm of economic and structural vulnerabilities. In the years leading up to the Great Depression, banks had engaged in risky practices, such as investing heavily in the stock market and making unsecured loans. When the stock market crashed in October 1929, banks were left with worthless assets and mounting liabilities. Compounding this issue was the absence of a federal safety net; unlike today, there was no Federal Deposit Insurance Corporation (FDIC) to protect depositors. As a result, panic spread rapidly, and bank runs became a common sight, with crowds of anxious citizens demanding their money back, often to no avail.

One of the most striking examples of this era was the collapse of the Bank of the United States in 1931, which was the largest bank failure in U.S. history at the time. With over $200 million in deposits, its failure sent shockwaves through the financial system, leading to a cascade of additional bank closures. This event highlighted the interconnectedness of banks and the economy, as the loss of a single major institution could destabilize entire regions. The Bank of the United States’ downfall was a stark reminder of the need for stronger regulatory oversight and depositor protections.

To prevent such a crisis from recurring, the U.S. government implemented sweeping reforms in the aftermath of the Great Depression. The Glass-Steagall Act of 1933 separated commercial and investment banking, while the establishment of the FDIC in 1934 provided deposit insurance, restoring public confidence in banks. These measures, along with stricter regulations, have since created a more resilient banking system. However, the lessons of the Great Depression remain relevant today, serving as a cautionary tale about the dangers of unchecked speculation and the importance of safeguarding the financial system.

Practical takeaways from this period include the value of diversification and the need for vigilance in assessing financial institutions. Modern depositors benefit from FDIC insurance, which protects up to $250,000 per depositor, per insured bank. Yet, understanding a bank’s financial health—such as its capital adequacy ratio and asset quality—remains crucial. For historians and economists, studying the Great Depression’s bank collapses offers insights into the interplay between economic policy, public behavior, and systemic risk. By learning from this dark chapter, we can better navigate future financial challenges and ensure a more stable economic environment.

Robbing a Bank Tree House: Creative Strategies and Safety Tips

You may want to see also

Explore related products

![]()

FDIC Role: How the Federal Deposit Insurance Corporation handles bank failures and protects depositors

Bank failures, though rare, can trigger widespread anxiety among depositors. Since the Great Depression, the Federal Deposit Insurance Corporation (FDIC) has stood as a bulwark against panic, ensuring that depositors’ funds remain secure even when their bank collapses. Established in 1933, the FDIC insures deposits up to $250,000 per depositor, per insured bank, for each account ownership category. This guarantee has restored confidence in the banking system, preventing the kind of mass withdrawals that can cripple financial institutions.

When a bank fails, the FDIC steps in swiftly to protect depositors and maintain financial stability. The process begins with the FDIC being appointed receiver by a bank’s chartering authority. The FDIC’s first priority is to find a healthy bank to assume the failed bank’s deposits and assets, ensuring customers can access their funds with minimal disruption. If no buyer is immediately available, the FDIC may establish a temporary bridge bank to maintain operations until a long-term solution is found. Throughout this process, insured depositors are made whole, often within days, thanks to the FDIC’s insurance fund.

The FDIC’s role extends beyond immediate crisis management. It also works to minimize losses to its insurance fund by liquidating the failed bank’s assets. This includes selling loans, real estate, and other holdings to recover as much value as possible. The FDIC’s ability to balance depositor protection with fiscal responsibility is critical to its mission. For instance, during the 2008 financial crisis, the FDIC managed over 400 bank failures, ensuring that no insured depositor lost a single penny of their insured funds.

Depositors can take proactive steps to ensure their funds are fully protected. First, verify that your bank is FDIC-insured by using the FDIC’s BankFind tool. Second, understand the $250,000 insurance limit per depositor, per bank, and structure accounts accordingly. Joint accounts, retirement accounts, and trusts may qualify for separate insurance coverage, allowing individuals to exceed the $250,000 limit across different account types. Finally, stay informed about your bank’s financial health through public reports and ratings, though the FDIC’s insurance remains a safety net regardless of a bank’s condition.

In summary, the FDIC’s role in handling bank failures is a cornerstone of U.S. financial stability. By insuring deposits, facilitating seamless transitions, and managing failed bank assets, the FDIC protects depositors and maintains public trust in the banking system. Understanding the FDIC’s processes and insurance limits empowers individuals to safeguard their funds, even in the face of bank collapses.

Trump Signs New Banking Rule: What It Means for Consumers

You may want to see also

Frequently asked questions

Notable bank collapses in recent years include Silicon Valley Bank (SVB) and Signature Bank in March 2023, and First Republic Bank in May 2023, primarily due to liquidity issues and depositor panic.

Since the 2008 financial crisis, over 500 banks have failed in the US, with the majority occurring between 2008 and 2013. The pace of failures has slowed significantly in recent years.

Banks typically collapse due to liquidity crises, poor risk management, economic downturns, or a loss of depositor confidence. External factors like market volatility or regulatory changes can also contribute.

Yes, most bank deposits are insured up to $250,000 per depositor by the Federal Deposit Insurance Corporation (FDIC), ensuring that customers recover their funds even if a bank fails.