When traveling abroad, one of the most frustrating expenses can be international ATM fees, which can quickly add up and eat into your travel budget. Fortunately, several banks and financial institutions offer accounts with no international ATM fees, allowing you to access your money conveniently and cost-effectively while overseas. These banks typically reimburse any fees charged by ATM operators or partner with global networks to provide fee-free withdrawals. Popular options include Charles Schwab, Ally Bank, and Capital One, which are known for their traveler-friendly policies. Additionally, some credit unions and digital banks like Revolut and Wise also offer similar benefits, making it easier for globetrotters to manage their finances without incurring unnecessary charges.

Explore related products

What You'll Learn

![]()

Banks with Global ATM Networks

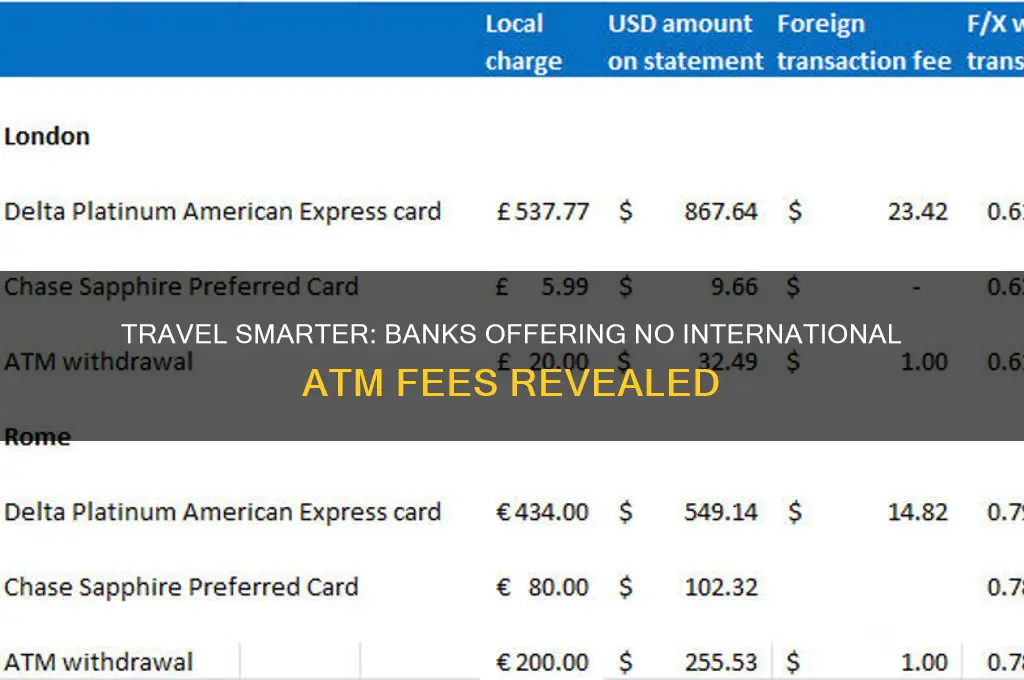

Travelers and expatriates often face steep fees when withdrawing cash abroad, but some banks have responded by building or partnering with global ATM networks to eliminate these charges. For instance, Charles Schwab Bank offers unlimited ATM fee reimbursements worldwide through its High Yield Investor Checking Account, making it a top choice for frequent international travelers. Similarly, Ally Bank provides up to $10 in ATM fee reimbursements per statement cycle, though it’s less comprehensive than Schwab’s offering. These banks leverage partnerships with networks like Global ATM Alliance (which includes banks such as Bank of America, Barclays, and Deutsche Bank) to offer fee-free withdrawals at specific ATMs in over 50 countries.

Analyzing these offerings reveals a strategic shift in banking services: institutions are prioritizing customer convenience over traditional fee structures to attract globally mobile clients. For example, HSBC’s Premier Checking Account grants access to its vast international ATM network without fees, but it requires a minimum balance of $75,000 or a monthly deposit of $5,000, limiting accessibility. In contrast, Capital One’s 360 Checking Account waives all foreign transaction fees and offers fee-free withdrawals at Allpoint ATMs globally, though its network is smaller than Schwab’s. This comparison highlights the trade-offs between accessibility, cost, and network size.

To maximize benefits, travelers should adopt a multi-bank strategy. Pairing a Charles Schwab account for unlimited ATM fee reimbursements with a Capital One card (which also waives foreign transaction fees) ensures coverage in areas where Schwab’s network may fall short. Additionally, always notify your bank of travel plans to avoid card blocks, and withdraw larger amounts less frequently to minimize fees when using non-partner ATMs. For those with substantial assets, HSBC Premier’s global network is unparalleled, but its steep eligibility requirements make it impractical for most.

A cautionary note: not all global ATM networks are created equal. While Global ATM Alliance offers fee-free withdrawals, its member ATMs are often located in urban areas, leaving rural travelers stranded. Similarly, Ally Bank’s $10 reimbursement cap means frequent withdrawals abroad can still incur costs. Always verify ATM locations before traveling and carry a backup card from a different network to avoid emergencies.

In conclusion, banks with global ATM networks provide a lifeline for international travelers, but their value depends on individual needs and travel patterns. Charles Schwab leads in flexibility, HSBC in network breadth (for eligible customers), and Capital One in accessibility. By understanding these nuances and combining accounts strategically, travelers can eliminate international ATM fees and focus on their journeys, not their wallets.

Banks Still Open in Shelby: Your Updated Local Banking Guide

You may want to see also

Explore related products

![]()

No Foreign Transaction Fee Policies

Travelers and expatriates often face hidden costs when using their debit or credit cards abroad, with foreign transaction fees (FTFs) typically ranging from 1% to 3% per purchase. However, a growing number of banks are eliminating these charges through No Foreign Transaction Fee Policies, making international spending more predictable and affordable. For instance, Charles Schwab Bank’s High Yield Investor Checking® account not only waives all international ATM fees but also reimburses ATM fees charged by other banks worldwide, while simultaneously eliminating FTFs on debit card purchases. This dual benefit positions it as a top choice for frequent travelers.

When evaluating banks with no foreign transaction fees, it’s critical to distinguish between debit card policies and credit card policies, as they often differ. For example, Capital One offers no FTFs on both its debit and credit cards, including popular travel cards like the Venture Rewards Credit Card. In contrast, Ally Bank waives FTFs on its debit card but does not offer a credit card option. Understanding this distinction ensures you choose the right product for your spending habits—whether you rely more on credit for rewards or debit for cash withdrawals.

A lesser-known but impactful aspect of no-FTF policies is their indirect savings on currency conversion. Banks without these fees often use competitive exchange rates, avoiding the markup typically applied by institutions that charge FTFs. For example, a €100 purchase with a 3% FTF bank costs $103 at a 1:1 exchange rate, whereas a no-FTF bank like Fidelity’s Cash Management Account charges only the base exchange rate, saving you $3 per transaction. Over a two-week trip with daily purchases, this small difference compounds to significant savings.

While no-FTF policies are advantageous, they’re not universally applicable across all bank services. Prepaid travel cards or wire transfers may still incur fees, even at banks with no FTFs on debit or credit cards. For instance, TD Bank’s Beyond Checking account waives FTFs on debit purchases but charges $15 for international wire transfers. Always review the fine print to avoid unexpected costs, especially when using less common banking services abroad.

Finally, pairing a no-FTF bank account with strategic usage habits maximizes savings. For example, use your no-FTF debit card for large purchases and ATM withdrawals, but carry a backup card from a different network (e.g., Visa if your primary card is Mastercard) to avoid incompatibility issues abroad. Additionally, notify your bank of travel plans to prevent card freezes, and monitor exchange rates to time large purchases when the rate is favorable. These practices ensure you fully leverage the benefits of no-FTF policies while minimizing travel-related financial stress.

Mastering Manulife Bank Cheques: A Step-by-Step Guide to Reading Them

You may want to see also

Explore related products

![]()

Travel-Friendly Checking Accounts

Traveling abroad often means navigating a maze of hidden fees, especially when accessing your money. One of the most frustrating is the international ATM fee, which can quickly add up. Fortunately, some banks have recognized the needs of globetrotters and offer travel-friendly checking accounts designed to minimize or eliminate these charges. These accounts not only save you money but also provide peace of mind, knowing you can access your funds without unexpected costs.

When selecting a travel-friendly checking account, look for banks that waive international ATM fees entirely. Institutions like Charles Schwab, Capital One 360, and Ally Bank are pioneers in this space, offering accounts with no foreign transaction fees and reimbursements for ATM fees charged by other banks. For instance, Charles Schwab’s High Yield Investor Checking account refunds all ATM fees worldwide, making it a top choice for frequent travelers. Similarly, Capital One 360’s checking account provides fee-free withdrawals at any ATM, regardless of location. These features can save you upwards of $5–$10 per transaction, which compounds significantly over a long trip.

Another critical aspect to consider is the account’s currency conversion rates. Some banks mark up exchange rates, effectively charging a hidden fee on every transaction. Travel-friendly accounts often use the real-time exchange rate, ensuring you get the best possible deal. For example, Revolut and Wise (formerly TransferWise) offer multi-currency accounts that allow you to hold and spend money in multiple currencies at the interbank exchange rate, avoiding excessive conversion fees. These accounts are particularly useful for travelers who frequently move between countries with different currencies.

Practical tips can further enhance your experience with a travel-friendly checking account. Always notify your bank of your travel plans to avoid account freezes due to suspicious activity. Keep a backup payment method, such as a credit card with no foreign transaction fees, in case your primary account is inaccessible. Additionally, monitor your account regularly for unauthorized transactions, especially when using ATMs in unfamiliar locations. Finally, consider carrying a small amount of local currency for emergencies, as some remote areas may not have ATMs or accept cards.

In conclusion, travel-friendly checking accounts are a game-changer for international travelers, offering significant savings and convenience. By choosing a bank that waives international ATM fees, provides fair currency conversion rates, and offers robust security features, you can focus on enjoying your journey rather than worrying about financial hurdles. Whether you’re a frequent flyer or an occasional adventurer, these accounts are an essential tool for seamless global travel.

How Exchange Rates Vary Across Banks

You may want to see also

Explore related products

![]()

Credit Unions with Fee Waivers

Credit unions often emerge as unsung heroes for travelers seeking to avoid international ATM fees, offering fee waivers as a core benefit of membership. Unlike traditional banks, credit unions operate as not-for-profit cooperatives, allowing them to prioritize member value over profit margins. This model enables many to absorb or reimburse foreign transaction and ATM fees, making them an ideal choice for globetrotters. For instance, institutions like Alliant Credit Union and PenFed Credit Union provide up to $20 in monthly ATM fee rebates, ensuring members can withdraw cash abroad without penalty.

To leverage these benefits, travelers must first identify credit unions with explicit fee waiver policies. Start by researching institutions that offer international ATM fee reimbursements, such as Navy Federal Credit Union or First Tech Federal Credit Union. Next, verify eligibility for membership, as credit unions often require affiliation with specific groups, employers, or communities. Once enrolled, activate the fee waiver benefit by opting into the program or meeting minimum account requirements, such as maintaining a $500 balance or setting up direct deposits.

While credit unions with fee waivers offer significant savings, travelers should remain mindful of potential limitations. Some institutions cap the number of monthly reimbursements or the dollar amount refunded per transaction. For example, a credit union might reimburse up to $10 per ATM withdrawal, with a maximum of five transactions monthly. Additionally, ensure the credit union belongs to a global ATM network like CO-OP or Allpoint to maximize fee-free access points. Pairing this strategy with a debit card that waives foreign transaction fees further optimizes cost savings.

The persuasive case for credit unions lies in their ability to combine fee waivers with other travel-friendly perks. Many offer competitive exchange rates, no foreign transaction fees on debit card purchases, and access to shared branching networks for in-person services abroad. By choosing a credit union over a traditional bank, travelers can save upwards of $100 annually in ATM fees alone. This makes credit unions not just a cost-effective option but a strategic financial partner for frequent international travelers.

In conclusion, credit unions with fee waivers stand out as a practical solution for avoiding international ATM fees. By understanding membership requirements, benefit limits, and additional perks, travelers can maximize savings and streamline their financial experience abroad. With a bit of research and strategic planning, credit unions transform from local financial cooperatives into global travel companions.

Exploring Nightmare Zone: Uncovering the Truth About Its Banking Facilities

You may want to see also

Explore related products

![]()

Online Banks with ATM Reimbursements

Choosing an online bank with ATM reimbursements requires careful consideration of your travel habits and financial needs. Start by evaluating the reimbursement cap—some banks limit refunds to a fixed amount per month, while others offer unlimited reimbursements. For example, SoFi Money provides unlimited ATM fee reimbursements globally, but it requires a minimum direct deposit to unlock this benefit. Next, check for network partnerships; banks like Revolut and N26 often partner with global ATM networks to reduce or eliminate fees outright. Finally, ensure the bank’s mobile app supports international transactions seamlessly, as real-time notifications and currency conversion tools can enhance your travel experience.

One often-overlooked advantage of online banks with ATM reimbursements is their ability to simplify currency management. Traditional banks typically charge 1-3% foreign transaction fees, but online banks like Wise (formerly TransferWise) offer debit cards with mid-market exchange rates and no hidden fees. Pairing such a card with an ATM reimbursement program ensures you’re not double-paying for access to your money abroad. For instance, using a Wise card at an international ATM and getting reimbursed by Charles Schwab means you pay zero fees for withdrawals, regardless of location. This dual strategy maximizes savings and minimizes financial stress while traveling.

Despite their benefits, online banks with ATM reimbursements aren’t without limitations. Some require a minimum balance or direct deposit to qualify for reimbursements, while others may exclude certain ATM networks. For example, Ally Bank’s $10 monthly cap may not suffice for frequent travelers who withdraw cash multiple times abroad. Additionally, not all online banks offer joint accounts or robust customer support, which could be a dealbreaker for some. To navigate these constraints, maintain a backup payment method (like a credit card with no foreign transaction fees) and research local ATM availability in your destination countries. With careful planning, these banks can still be a game-changer for international travelers.

How to Cancel a Cheque in Axis Bank: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Banks like Charles Schwab, Capital One 360, and Ally Bank are known for offering no international ATM fees and often reimburse any fees charged by ATM operators.

Yes, some credit unions like Alliant Credit Union and First Tech Federal Credit Union offer no international ATM fees and reimburse fees charged by other banks.

No, while some banks like Charles Schwab and Capital One 360 waive international ATM fees and reimburse foreign transaction fees, others may only cover ATM fees. Always check the bank’s specific policy.