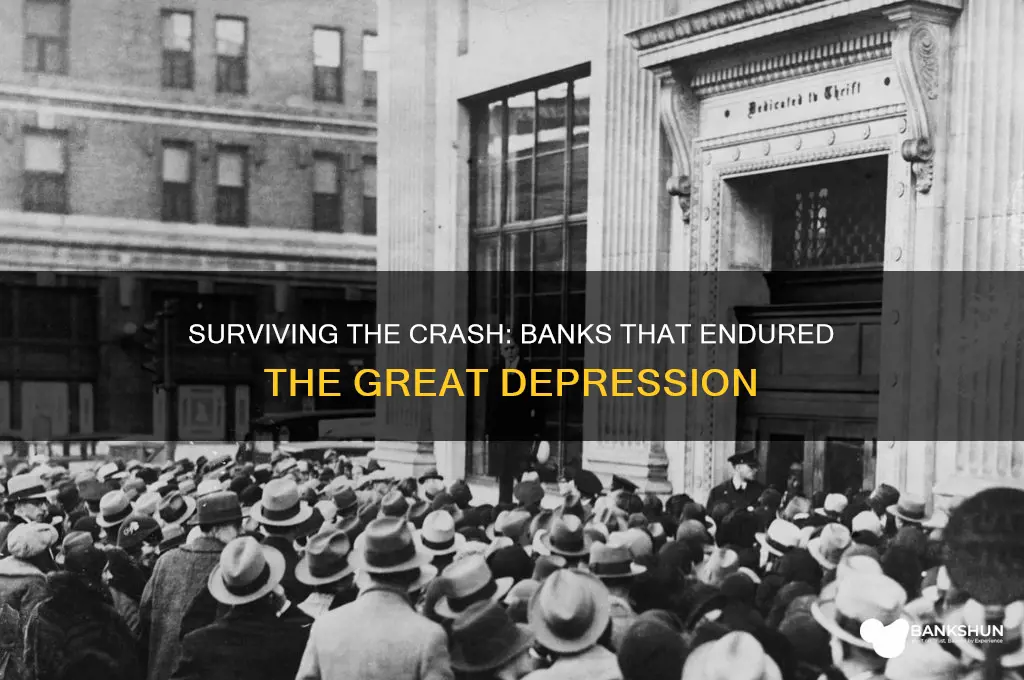

The Great Depression of the 1930s had a profound and devastating impact on the global banking system, leading to widespread bank failures and a significant loss of public trust in financial institutions. In the United States alone, over 9,000 banks closed between 1930 and 1933, leaving only a fraction of the original institutions intact. The banks that survived this tumultuous period were those that had maintained strong capital reserves, diversified their assets, and implemented sound risk management practices. Among the notable survivors were large national banks such as Chase National Bank, National City Bank (now Citibank), and First National Bank of New York, which later became part of Citibank. These institutions, along with a few others, played a crucial role in rebuilding the financial system and restoring confidence in the banking sector during the subsequent years of recovery and reform.

Explore related products

What You'll Learn

- Surviving National Banks: Major national banks like Chase and BofA endured, reshaping post-Depression banking

- Regional Bank Resilience: Smaller regional banks adapted, focusing on local economies to survive

- Government-Backed Institutions: Entities like FDIC and Federal Reserve emerged to stabilize banking

- Merged Entities: Weak banks merged, forming stronger institutions to weather economic turmoil

- Credit Unions Growth: Community-based credit unions expanded, offering alternative financial services post-Depression

![]()

Surviving National Banks: Major national banks like Chase and BofA endured, reshaping post-Depression banking

The Great Depression decimated the American banking sector, yet a handful of national banks not only survived but emerged as architects of the post-Depression financial landscape. Institutions like Chase National Bank (now JPMorgan Chase) and Bank of America (BofA) leveraged their size, diversified portfolios, and strategic adaptability to weather the storm. While thousands of smaller banks collapsed under the weight of panic-driven withdrawals and bad loans, these giants restructured operations, consolidated weaker competitors, and positioned themselves as pillars of stability in an era defined by economic uncertainty.

Consider Chase National Bank’s approach: under the leadership of Albert H. Wiggin, Chase aggressively acquired failing banks, expanding its branch network and customer base. This consolidation strategy not only rescued distressed assets but also allowed Chase to dominate key markets, particularly in the Northeast. Similarly, Bank of America, then known as Bank of Italy under A.P. Giannini, focused on serving underserved communities, including immigrants and small businesses, which fostered loyalty and insulated it from the worst of the panic. These tactics highlight a critical survival principle: diversification of services and clientele acted as a buffer against systemic shocks.

However, survival alone wasn’t enough—these banks actively reshaped banking practices to align with new regulatory realities. The Glass-Steagall Act of 1933, for instance, forced a separation between commercial and investment banking, prompting Chase and BofA to streamline operations and focus on core services like retail banking and corporate lending. Chase, for example, exited riskier investment activities, while BofA doubled down on its retail-focused model, offering savings accounts with FDIC insurance to restore public trust. This pivot wasn’t just reactive; it was a calculated move to redefine their roles in a regulated environment.

A comparative analysis reveals that while both Chase and BofA survived, their paths diverged in significant ways. Chase’s growth was more acquisitive, absorbing competitors to expand geographically, whereas BofA’s success hinged on organic growth and community-centric strategies. Chase’s model prioritized scale and efficiency, while BofA emphasized accessibility and inclusivity. These contrasting approaches demonstrate that there’s no one-size-fits-all formula for survival—success depended on aligning strengths with the evolving demands of the post-Depression economy.

For modern banks facing crises, the lessons from Chase and BofA are clear: adaptability, diversification, and a focus on customer trust are non-negotiable. During downturns, banks should assess their portfolios for vulnerabilities, explore strategic acquisitions or partnerships, and prioritize services that meet immediate customer needs. For instance, offering low-interest loans to small businesses or expanding digital banking services can mitigate panic and foster resilience. The survivors of the Great Depression didn’t just endure—they innovated, setting precedents that remain relevant in today’s volatile financial landscape.

Does Citizens Bank Operate Branches in Florida? Find Out Here

You may want to see also

Explore related products

$10.87 $14.99

![]()

Regional Bank Resilience: Smaller regional banks adapted, focusing on local economies to survive

The Great Depression decimated the banking sector, leaving only a fraction of institutions standing. Yet, amidst the wreckage, smaller regional banks demonstrated a surprising resilience. Their survival wasn’t accidental; it was rooted in a strategic pivot to hyper-local focus. While larger banks crumbled under the weight of speculative investments and overextended credit, regional banks doubled down on their communities, becoming lifelines for local businesses and families. This localized approach insulated them from the broader financial contagion, proving that sometimes, smaller is stronger.

Consider the case of the First National Bank of Boston, a regional institution that thrived during the Depression by prioritizing local lending. Unlike national banks entangled in risky Wall Street ventures, it focused on mortgages for local homeowners and loans for small businesses. This strategy not only stabilized the bank but also bolstered the regional economy, creating a symbiotic relationship that ensured mutual survival. By 1933, while over 10,000 banks had failed nationwide, many regional banks like this one remained solvent, their balance sheets fortified by conservative, community-centric practices.

Adapting to local needs wasn’t just about lending; it was about understanding the unique challenges of the region. In agricultural areas, banks extended grace periods to farmers facing crop failures. In industrial towns, they restructured loans for factories struggling with plummeting demand. This flexibility, born of proximity and personal relationships, was a luxury larger banks couldn’t afford. Regional banks became de facto partners in their communities’ recovery, earning trust that translated into long-term loyalty.

However, this resilience wasn’t without its risks. Over-reliance on a single local industry could prove disastrous if that sector collapsed. Regional banks mitigated this by diversifying within their communities—supporting not just farmers or factory owners, but also grocers, doctors, and tradespeople. This micro-diversification created a buffer against localized shocks, ensuring that even if one sector faltered, others could sustain the bank’s operations.

The takeaway for modern banking is clear: in an era of globalization and digital disruption, the lessons of regional bank resilience remain relevant. Smaller institutions that prioritize local economies can weather systemic crises more effectively than their larger counterparts. By fostering deep community ties and tailoring services to local needs, regional banks don’t just survive—they thrive, proving that in banking, as in life, sometimes the best defense is a focused offense.

Lost Bank Passbook? Step-by-Step Guide to Reapply Easily

You may want to see also

Explore related products

![]()

Government-Backed Institutions: Entities like FDIC and Federal Reserve emerged to stabilize banking

The Great Depression exposed the fragility of the American banking system, leaving a trail of bank failures and shattered public trust. In response, the U.S. government established institutions like the Federal Deposit Insurance Corporation (FDIC) and empowered the Federal Reserve to prevent future collapses. These entities became pillars of financial stability, reshaping the banking landscape.

The FDIC, created in 1933, introduced a revolutionary concept: deposit insurance. By guaranteeing deposits up to $5,000 (later adjusted for inflation), it aimed to prevent bank runs fueled by panic. This safety net restored confidence, encouraging individuals to keep their money in banks rather than under mattresses. The FDIC's role extended beyond insurance; it also supervised and examined banks, identifying weaknesses and enforcing regulations to mitigate risks.

The Federal Reserve, established in 1913 but significantly strengthened during the Depression, gained tools to manage the money supply and interest rates. Through open market operations, discount lending, and reserve requirements, the Fed could inject liquidity into the system during crises and curb inflationary pressures during booms. This ability to stabilize the financial system and promote economic growth became a cornerstone of its mandate.

The impact of these institutions was profound. Bank failures plummeted, and public trust in the financial system gradually returned. The FDIC's insurance guarantee, now $250,000 per depositor per insured bank, remains a cornerstone of financial security. The Fed's role in monetary policy and financial regulation has evolved, adapting to new challenges like the 2008 financial crisis.

While government-backed institutions have been instrumental in stabilizing banking, they are not without limitations. Moral hazard, the tendency for insured parties to take greater risks, remains a concern. Additionally, the complexity of the financial system requires constant vigilance and adaptation from these institutions. Nonetheless, the FDIC and Federal Reserve stand as testaments to the power of government intervention in safeguarding the financial well-being of individuals and the stability of the economy. Their existence serves as a reminder that a robust financial system requires both market forces and responsible oversight.

Wells Fargo Bank Services: A Comprehensive Guide to Offerings and Features

You may want to see also

Explore related products

![]()

Merged Entities: Weak banks merged, forming stronger institutions to weather economic turmoil

The Great Depression exposed the fragility of countless banks, leaving many teetering on the brink of collapse. Rather than face certain failure, some institutions chose a different path: merger. This strategic move allowed weaker banks to pool resources, share expertise, and create stronger, more resilient entities capable of weathering the economic storm.

By combining assets, customer bases, and operational infrastructure, merged banks could achieve economies of scale, reduce costs, and access a broader range of financial services. This newfound strength enabled them to better manage risk, absorb losses, and continue serving their communities during a time of unprecedented hardship.

Consider the example of the Bank of America, which emerged from the merger of the Bank of Italy and the Bank of America, Los Angeles in 1928. This union created a more robust institution that was better equipped to navigate the challenges of the Great Depression. Similarly, the Chase National Bank merged with the Equitable Trust Company in 1929, forming a powerful entity that would eventually become JPMorgan Chase. These mergers not only ensured the survival of the individual banks but also contributed to the stabilization of the broader financial system.

However, merging was not without its challenges. Integrating disparate cultures, systems, and processes could be complex and time-consuming. Moreover, the dilution of ownership and control could lead to conflicts and power struggles. To mitigate these risks, successful mergers required careful planning, transparent communication, and a shared vision for the future. Banks that approached mergers with a strategic mindset, focusing on long-term value creation rather than short-term gains, were more likely to thrive in the post-Depression era.

For banks considering merger as a strategy to enhance resilience, several key factors should be considered. First, assess the financial health and cultural compatibility of potential partners. Second, develop a clear integration plan that addresses operational, technological, and human resource challenges. Third, prioritize transparency and communication with stakeholders, including employees, customers, and regulators. By following these guidelines, banks can increase their chances of creating a stronger, more resilient institution that is better equipped to weather economic turmoil. Ultimately, the success of merged entities during the Great Depression demonstrates the power of strategic collaboration in building a more stable and sustainable financial system.

Paying HST at the Bank: A Step-by-Step Guide for Canadian Businesses

You may want to see also

Explore related products

![]()

Credit Unions Growth: Community-based credit unions expanded, offering alternative financial services post-Depression

The Great Depression left a fractured financial landscape, with thousands of banks failing and public trust in traditional institutions shattered. Amid this chaos, community-based credit unions emerged as a resilient alternative, filling the void left by collapsed banks. Unlike profit-driven banks, credit unions operated as member-owned cooperatives, prioritizing financial stability and community welfare. This model resonated with Americans seeking security and fairness in their financial dealings.

Consider the mechanics of credit union growth during this period. Membership was often tied to specific communities, workplaces, or organizations, fostering a sense of collective ownership. For example, the Harlem Co-operative Credit Union, founded in 1934, served African American residents excluded from mainstream banking. By pooling resources and offering small loans, credit unions provided lifelines to families and small businesses. Their localized focus allowed them to understand and address unique community needs, a stark contrast to the impersonal nature of larger banks.

However, this growth was not without challenges. Credit unions faced skepticism from both the public, wary of another financial collapse, and established banks, threatened by their rising popularity. To overcome these hurdles, credit unions emphasized transparency and education, hosting financial literacy workshops and demonstrating their commitment to member interests. Regulatory support also played a role, as the Federal Credit Union Act of 1934 provided a legal framework for their expansion.

The takeaway is clear: credit unions thrived post-Depression by offering a human-centered approach to finance. Their success underscores the value of community-driven models in times of economic uncertainty. For modern financial institutions, this history serves as a reminder that trust and inclusivity are as critical as profitability. By adopting similar principles, today’s organizations can build resilience and foster long-term loyalty.

Is Elizabeth Banks in Mockingjay Part 2? Unraveling the Cast Mystery

You may want to see also

Frequently asked questions

Several major banks survived the Great Depression, including JPMorgan Chase (originally known as Chase National Bank), Bank of America (formed from the merger of Bank of Italy and Bank of America, Los Angeles), and Citigroup (originally City Bank of New York).

After the Great Depression, the U.S. government implemented significant reforms, such as the Glass-Steagall Act of 1933, which separated commercial and investment banking, and the creation of the Federal Deposit Insurance Corporation (FDIC) to insure deposits and restore public trust in banks.

Yes, thousands of banks failed during the Great Depression. By 1933, approximately 11,000 of the nation’s 25,000 banks had closed, leading to widespread financial panic and loss of savings for many Americans.

Banks like the Reconstruction Finance Corporation (RFC), established in 1932, played a crucial role in stabilizing the economy by providing emergency loans to banks, railroads, and other businesses. Additionally, the Federal Reserve took steps to regulate monetary policy and prevent future banking crises.