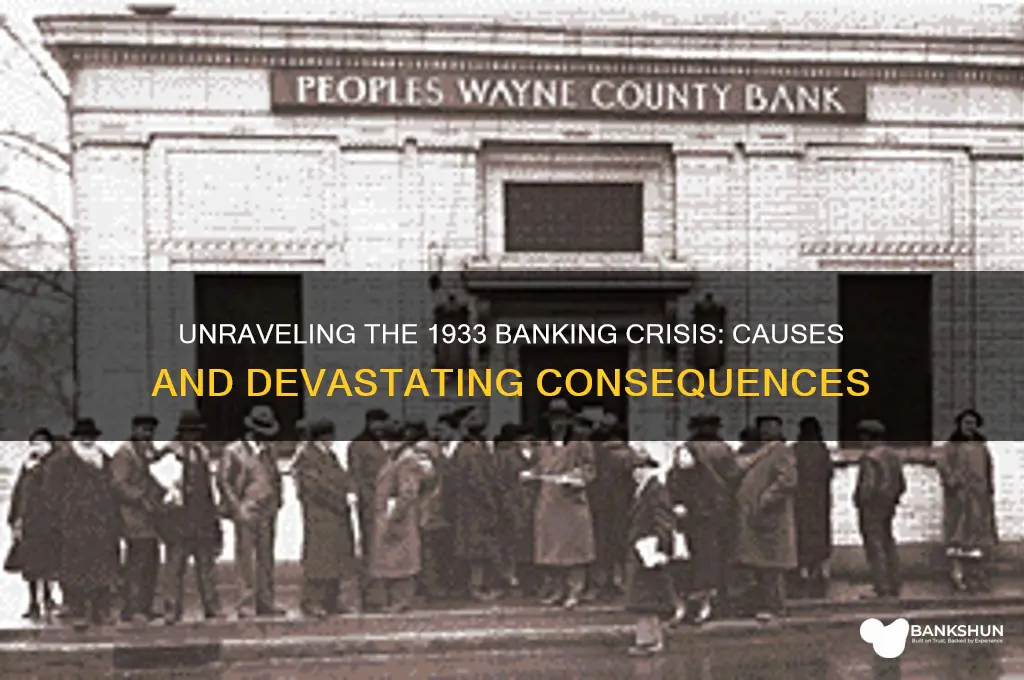

The banking crisis of 1933 was a pivotal event in American financial history, deeply rooted in the aftermath of the 1929 stock market crash and the ensuing Great Depression. Widespread panic, economic instability, and a lack of confidence in the banking system led to massive bank runs, as depositors rushed to withdraw their funds, fearing insolvency. The crisis was exacerbated by the absence of federal deposit insurance, which left banks vulnerable to liquidity shortages. Additionally, speculative lending practices, overleveraged financial institutions, and a deflationary spiral further weakened the banking sector. The situation culminated in President Franklin D. Roosevelt declaring a national bank holiday in March 1933, temporarily closing all banks to prevent collapse, and subsequently implementing reforms like the Glass-Steagall Act and the creation of the FDIC to restore trust and stabilize the financial system.

| Characteristics | Values |

|---|---|

| Economic Downturn | Severe contraction following the 1929 stock market crash (Great Depression) |

| Banking System Fragility | Over 9,000 banks failed between 1930-1933 due to insolvency and panic |

| Speculative Lending | Excessive loans for stock market speculation and real estate |

| Lack of Deposit Insurance | No federal insurance, leading to widespread panic and bank runs |

| Gold Standard Pressure | Deflationary policies tied to the gold standard exacerbated debt burdens |

| Contagion Effect | Bank failures spread rapidly, eroding public trust in the financial system |

| Regulatory Weakness | Inadequate oversight and lack of centralized banking regulation |

| Agricultural Distress | Farm foreclosures and declining commodity prices strained rural banks |

| International Factors | Global economic slowdown and trade restrictions reduced U.S. exports |

| Policy Inaction | Delayed federal intervention until the 1933 Banking Act (Glass-Steagall) |

Explore related products

$9.99 $29.95

$32.95 $16.95

What You'll Learn

- Excessive risk-taking by banks in the 1920s led to unstable financial practices

- Stock market crash of 1929 eroded public confidence and triggered withdrawals

- Unregulated banking system lacked oversight, allowing widespread fraud and mismanagement

- Economic downturn reduced loan repayments, causing bank liquidity shortages

- Panicked depositors withdrew funds en masse, accelerating bank failures nationwide

![]()

Excessive risk-taking by banks in the 1920s led to unstable financial practices

The Roaring Twenties, a period of unprecedented economic growth and prosperity, saw banks embracing a culture of excessive risk-taking that ultimately sowed the seeds of the 1933 banking crisis. Flush with deposits from a booming economy, banks ventured into speculative investments, often using customer funds to purchase stocks and make high-risk loans. This departure from traditional, conservative banking practices created a fragile financial system built on the quicksand of speculation.

For instance, banks heavily invested in the stock market, leveraging customer deposits to buy shares at inflated prices. This practice, known as "buying on margin," allowed investors to purchase stocks with only a fraction of the actual cost, amplifying potential gains but also magnifying losses. When the stock market crashed in 1929, these leveraged positions crumbled, leaving banks holding worthless assets and unable to meet withdrawal demands.

This reckless behavior wasn't limited to stock market speculation. Banks also extended loans to businesses and individuals with little regard for creditworthiness. The allure of quick profits blinded them to the inherent risks, leading to a surge in bad debts. As the economy slowed in the early 1930s, borrowers defaulted on these loans in droves, further depleting bank reserves and eroding public confidence in the financial system.

Imagine a scenario where a bank, enticed by the promise of high returns, lends a significant portion of its deposits to a fledgling company with a shaky business plan. When the company fails, the bank is left holding the bag, unable to recover its investment and facing a severe liquidity crisis. This scenario played out repeatedly across the country, highlighting the dangers of unchecked risk-taking.

The consequences of this excessive risk-taking were devastating. Bank failures became commonplace, triggering a wave of panic as depositors rushed to withdraw their funds, fearing they would lose everything. This bank run further exacerbated the crisis, leading to a vicious cycle of bank closures and economic contraction. The resulting loss of trust in the banking system had a ripple effect throughout the economy, stifling investment, consumption, and ultimately, economic growth.

The 1933 banking crisis serves as a stark reminder of the dangers of unchecked risk-taking in the financial sector. It underscores the importance of prudent banking practices, robust regulation, and a culture of responsible risk management to safeguard the stability of the financial system and protect the interests of depositors and the wider economy.

Citizens Bank in Florida: Exploring Branch Availability and Services

You may want to see also

Explore related products

![]()

Stock market crash of 1929 eroded public confidence and triggered withdrawals

The stock market crash of 1929 was a seismic event that shattered the financial optimism of the Roaring Twenties. On October 24, 1929, also known as Black Thursday, the market began its precipitous decline, culminating in the catastrophic losses of Black Tuesday on October 29. Billions of dollars in wealth evaporated overnight, leaving investors stunned and panicked. This sudden collapse was not merely a financial event; it was a psychological blow that eroded public confidence in the stability of the economic system. As headlines screamed of fortunes lost and businesses ruined, ordinary citizens began to question the safety of their own money, particularly the funds they had entrusted to banks.

This erosion of confidence directly triggered a wave of bank withdrawals as people sought to secure their savings. The logic was simple: if the stock market could fail so spectacularly, what was stopping banks from collapsing next? By 1930, banks were already feeling the strain as depositors lined up to withdraw their funds. The situation worsened in 1932, when a series of bank failures further fueled public anxiety. For instance, in December 1932, the Bank of the United States, one of the largest banks in the country, closed its doors, sparking a nationwide panic. This event alone led to the withdrawal of over $100 million in deposits within days, a staggering amount at the time.

The mechanics of the banking system exacerbated the crisis. Banks in the 1930s operated on a fractional reserve system, meaning they only kept a fraction of their depositors’ money on hand, lending out the rest. When withdrawals surged, banks were unable to meet the demand, leading to a vicious cycle of bank runs and failures. By 1933, the situation had reached a breaking point. In the first three months of the year, over 2,000 banks closed, and by March, President Franklin D. Roosevelt declared a nationwide bank holiday to halt the hemorrhaging of funds. This drastic measure underscored the direct link between the stock market crash, the loss of public confidence, and the ensuing banking crisis.

To understand the human impact, consider the story of a typical depositor in 1933. A middle-class family with $500 in savings—a substantial sum at the time—would have watched in horror as neighbors and news reports detailed bank failures. Faced with the choice of leaving their money in a potentially failing bank or withdrawing it, many opted for the latter, even if it meant keeping cash under mattresses or in safes. This behavior, while rational for individuals, collectively doomed banks that were otherwise solvent. The lesson here is clear: financial systems are as much about perception as they are about balance sheets. When trust evaporates, even the most robust institutions can crumble.

In retrospect, the stock market crash of 1929 acted as the catalyst for a chain reaction that culminated in the banking crisis of 1933. It was not just the loss of wealth but the loss of faith in the system that proved devastating. Today, this period serves as a cautionary tale about the fragility of financial systems and the critical role of public confidence. Modern safeguards, such as deposit insurance and stricter regulations, are direct responses to the lessons learned from this era. For anyone managing personal finances or studying economic history, the takeaway is unmistakable: trust is the bedrock of banking, and once shaken, its effects can be far-reaching and catastrophic.

Weekend Payroll Processing: Banks and Saturdays

You may want to see also

Explore related products

![]()

Unregulated banking system lacked oversight, allowing widespread fraud and mismanagement

The absence of regulatory oversight in the early 20th-century banking system created an environment ripe for exploitation. Banks operated with minimal scrutiny, enabling fraudulent practices to flourish unchecked. For instance, the "wildcat banking" era saw institutions issuing their own currency without sufficient assets to back it, leading to rampant instability. This lack of accountability allowed bank owners to mismanage funds, often investing recklessly in speculative ventures while depositors remained oblivious to the risks. The result? A fragile system where public trust was built on quicksand, setting the stage for the 1933 crisis.

Consider the mechanics of fraud in this unregulated landscape. Without federal supervision, banks could falsify financial statements, inflate asset values, and conceal insolvency. One notorious example was the practice of "kiting," where banks shuffled funds between branches to create the illusion of liquidity. Such tactics not only deceived depositors but also regulators, who lacked the authority to audit or intervene. This systemic deceit eroded the financial foundation, making banks vulnerable to even minor economic shocks. By the time the Great Depression hit, many institutions were already operating on borrowed time.

To understand the role of mismanagement, examine the incentives driving bank leadership. Without regulatory constraints, executives prioritized short-term profits over long-term stability. For example, banks often extended loans to unqualified borrowers or invested heavily in speculative stocks, assuming the market would perpetually rise. When the stock market crashed in 1929, these risky decisions backfired spectacularly. Depositors, realizing their savings were at risk, began mass withdrawals, triggering bank runs. The absence of oversight meant no safety nets existed to halt this downward spiral, accelerating the collapse of thousands of banks by 1933.

A comparative analysis highlights the stark contrast between the pre-1933 era and subsequent regulatory reforms. The establishment of the Federal Deposit Insurance Corporation (FDIC) in 1933 introduced deposit insurance, restoring public confidence. Similarly, the Glass-Steagall Act separated commercial and investment banking, curbing reckless speculation. These measures addressed the root causes of the crisis by imposing accountability and transparency. Had such oversight existed earlier, the fraud and mismanagement that characterized the 1920s might have been mitigated, preventing the catastrophic banking failures of 1933.

Practical lessons from this period emphasize the need for vigilance in modern financial systems. While today’s regulatory frameworks are more robust, the principle remains: oversight is non-negotiable. Investors and policymakers must remain wary of deregulation trends that could reintroduce vulnerabilities. Regular audits, stringent reporting requirements, and whistleblower protections are essential tools to deter fraud. By studying the 1933 crisis, we learn that an unregulated system is not just inefficient—it’s inherently dangerous, capable of undermining entire economies. The takeaway? Oversight isn’t a burden; it’s a safeguard.

Step-by-Step Guide to Adding a Beneficiary in Riyad Bank

You may want to see also

Explore related products

![]()

Economic downturn reduced loan repayments, causing bank liquidity shortages

The banking crisis of 1933 was a pivotal moment in American financial history, deeply intertwined with the broader economic collapse of the Great Depression. At its core, the crisis was fueled by a vicious cycle: as the economy deteriorated, borrowers struggled to repay loans, which in turn depleted banks' liquidity reserves. This section dissects how economic downturn directly led to reduced loan repayments and subsequent bank liquidity shortages, offering a focused analysis of this causal chain.

Consider the domino effect of declining economic activity on individual borrowers. During the early 1930s, unemployment soared to nearly 25%, leaving millions without steady income. For instance, a farmer with a mortgage or a small business owner with a commercial loan faced insurmountable challenges as crop prices plummeted and consumer spending dried up. Without income, these borrowers defaulted on their loans, leaving banks with a growing portfolio of non-performing assets. This wasn’t an isolated incident but a widespread trend, as evidenced by the fact that over 9,000 banks failed between 1930 and 1933. Each default chipped away at banks' liquidity, as loan repayments were a primary source of cash flow for lending institutions.

To understand the liquidity crisis, imagine a bank as a reservoir of funds, with loan repayments acting as the inflow that keeps the reservoir full. When repayments dried up, banks were left with insufficient cash to meet withdrawal demands from panicked depositors. This liquidity shortage was exacerbated by the fractional reserve banking system, where banks only held a fraction of deposits as reserves. For example, if a bank had $100 in deposits and only $10 in reserves, a sudden surge in withdrawals would quickly deplete its cash on hand. The result? Bank runs became commonplace, with depositors lining up to withdraw funds before their bank collapsed, further accelerating the liquidity crisis.

A comparative analysis highlights the contrast between banks in agricultural and industrial regions. In rural areas, where farming communities were hit hardest by falling commodity prices, loan defaults were particularly acute. Banks in these regions often held mortgages backed by farmland, which lost value rapidly. In contrast, urban banks faced defaults from businesses and consumers, but the concentration of defaults in rural areas led to a disproportionate number of bank failures in those regions. This regional disparity underscores how localized economic downturns amplified the liquidity crisis in specific banking sectors.

Practical takeaways from this analysis include the importance of diversified loan portfolios and robust liquidity management. Banks today are required to maintain higher capital reserves and undergo stress testing to ensure they can withstand economic shocks. For individuals, the lesson is clear: economic downturns can disrupt even the most carefully planned finances, emphasizing the need for emergency funds and diversified income sources. By studying the 1933 crisis, we gain insights into the fragile relationship between economic health, loan repayments, and bank stability—a relationship that remains critical in modern financial systems.

Uncovering Oreo Insights: A Comprehensive Guide to Bank Analysis Techniques

You may want to see also

Explore related products

![]()

Panicked depositors withdrew funds en masse, accelerating bank failures nationwide

The banking crisis of 1933 was a pivotal moment in American financial history, and at its core was a vicious cycle of fear and uncertainty. Panicked depositors, worried about the solvency of their banks, withdrew funds en masse, creating a self-fulfilling prophecy of bank failures. This phenomenon, known as a bank run, was not isolated but widespread, accelerating the collapse of financial institutions nationwide. To understand this, consider the fragile state of banks during the Great Depression: many were already struggling with bad loans and dwindling reserves. When depositors lost confidence, their collective actions turned a precarious situation into a catastrophic one.

Imagine a bank with $1 million in deposits but only $100,000 in cash reserves—a common scenario in the 1930s due to fractional reserve banking. If even 15% of depositors withdrew their funds simultaneously, the bank would be unable to meet the demand, forcing it to close. This is exactly what happened across the country. For instance, in the weeks leading up to the banking holiday declared by President Roosevelt in March 1933, over 5,000 banks failed as depositors rushed to withdraw their money. The psychological trigger was often a single rumor or a high-profile bank failure, which spread like wildfire, causing otherwise solvent banks to crumble under the weight of panic.

To break this cycle, practical steps were necessary. First, restoring confidence was critical. Roosevelt’s fireside chats played a key role in calming the public, but structural changes were equally important. The Emergency Banking Act of 1933 and the establishment of the Federal Deposit Insurance Corporation (FDIC) in 1934 provided deposit insurance, assuring account holders that their funds were safe up to a certain limit. For modern readers, this underscores the importance of transparency and safety nets in banking systems. If you’re ever in a financial crisis, stay informed, avoid knee-jerk reactions, and consider insured accounts to protect your assets.

Comparatively, the 1933 crisis contrasts sharply with modern banking panics, such as those seen during the 2008 financial crisis. While technology has made bank runs less literal—no crowds outside banks—digital withdrawals can still cripple institutions. However, the presence of deposit insurance and stronger regulatory frameworks has mitigated the risk. For example, during the 2008 crisis, FDIC insurance prevented widespread panic withdrawals, highlighting the effectiveness of lessons learned from 1933. This historical comparison serves as a reminder that while the methods of banking have evolved, the underlying principles of trust and stability remain unchanged.

In conclusion, the mass withdrawal of funds by panicked depositors in 1933 was not just a symptom of the banking crisis but a driving force behind its escalation. It exposed the vulnerabilities of an underregulated banking system and the power of collective fear. By examining this specific aspect, we gain insights into the importance of confidence, insurance, and regulation in maintaining financial stability. Whether in 1933 or today, understanding these dynamics can help individuals and policymakers navigate future crises more effectively.

M&T Bank Stadium Turf: Real Grass or Artificial Surface?

You may want to see also

Frequently asked questions

The banking crisis of 1933 was primarily caused by the Great Depression, which led to widespread bank runs, deflation, and a collapse in consumer confidence. Additionally, speculative lending, overextended credit, and a lack of deposit insurance exacerbated the situation, causing thousands of banks to fail.

The Great Depression caused a severe economic downturn, leading to high unemployment, reduced consumer spending, and widespread business failures. As a result, borrowers defaulted on loans, banks faced liquidity shortages, and panicked depositors withdrew their funds en masse, triggering bank runs and failures.

Bank runs were a major factor in the 1933 banking crisis. As depositors lost confidence in banks' solvency, they rushed to withdraw their funds, depleting banks' cash reserves. This forced many banks to liquidate assets at a loss or close their doors entirely, further eroding public trust and deepening the crisis.

The government responded to the banking crisis by declaring a nationwide bank holiday in March 1933 to halt bank runs. President Franklin D. Roosevelt also signed the Emergency Banking Act and later established the Federal Deposit Insurance Corporation (FDIC) to insure deposits, restore confidence, and prevent future banking panics.