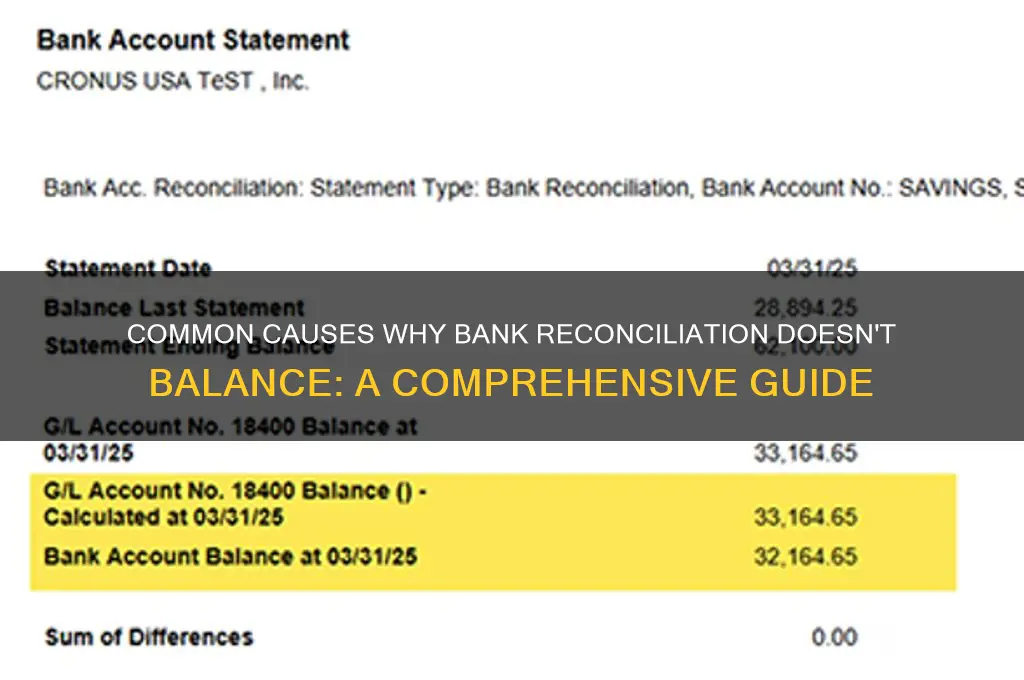

Bank reconciliation discrepancies can arise from various factors, including timing differences between when transactions are recorded in the company’s books and when they appear on the bank statement, unrecorded deposits or payments, bank errors, outstanding checks or deposits in transit, fees or interest charges not yet accounted for, and data entry mistakes. Additionally, discrepancies may stem from duplicate entries, incorrect transaction amounts, or uncashed checks that remain outstanding for extended periods. Identifying the root cause requires a meticulous review of both the company’s records and the bank statement to ensure accuracy and resolve imbalances effectively.

| Characteristics | Values |

|---|---|

| Timing Differences | Deposits or payments recorded in the company’s books but not yet reflected in the bank statement (e.g., outstanding checks, deposits in transit). |

| Bank Errors | Mistakes made by the bank, such as incorrect posting of transactions, duplicate entries, or omitted transactions. |

| Company Errors | Errors in the company’s records, such as incorrect amounts, omitted entries, or transposition of numbers. |

| Fees and Charges | Bank fees (e.g., service charges, overdraft fees) deducted by the bank but not recorded in the company’s books. |

| Interest Income | Interest earned on the bank account not yet recorded by the company. |

| Outstanding Checks | Checks issued by the company but not yet cashed or cleared by the bank. |

| Deposits in Transit | Funds deposited by the company but not yet credited by the bank. |

| Electronic Transactions | Pending or uncleared electronic transactions (e.g., ACH transfers, wire transfers). |

| Reconciliation Period Mismatch | Using incorrect statement periods or dates during reconciliation. |

| Foreign Currency Fluctuations | Differences in exchange rates when reconciling accounts in multiple currencies. |

| Fraud or Unauthorized Transactions | Unauthorized withdrawals, deposits, or adjustments not reflected in the company’s records. |

| Adjusting Entries | Failure to include adjusting journal entries (e.g., accruals, deferrals) in the reconciliation process. |

| Void or Stopped Payments | Voided checks or stopped payments not accounted for in the company’s records. |

| Manual Entry Errors | Mistakes in manually entering transactions into the company’s accounting system. |

| System Glitches | Technical issues in accounting software or banking systems causing discrepancies. |

Explore related products

What You'll Learn

- Unrecorded Transactions: Deposits or payments not yet recorded in the bank or company books

- Timing Differences: Transactions posted in different periods between bank and company records

- Data Entry Errors: Mistakes in recording amounts, dates, or account numbers

- Bank Fees/Interest: Unaccounted bank charges or interest not reflected in company records

- Outstanding Checks: Checks issued but not yet cleared by the bank

![]()

Unrecorded Transactions: Deposits or payments not yet recorded in the bank or company books

Unrecorded transactions are a common yet often overlooked culprit behind bank reconciliation discrepancies. These occur when deposits or payments are made but fail to appear in either the bank statement or the company’s accounting records. For instance, a business might deposit a client’s check on Friday afternoon, but if the bank processes it after the statement cutoff, it won’t reflect in the current period. Similarly, a company may issue a payment that hasn’t yet cleared the recipient’s account, leaving it unrecorded in the bank’s ledger. Such timing gaps create temporary mismatches, making reconciliation challenging.

To address unrecorded transactions, start by cross-referencing dates meticulously. Compare the cutoff dates of the bank statement with the transaction dates in your accounting software. For example, if the bank statement ends on the 30th, ensure all transactions up to that date are accounted for. Use a reconciliation tool or spreadsheet to flag entries that fall outside this window. Additionally, maintain a log of pending transactions, such as outstanding checks or deposits in transit, to anticipate discrepancies before they arise.

A proactive approach involves establishing clear communication channels with your bank. Verify processing times for deposits and payments, as these can vary depending on the bank’s policies or the transaction type. For instance, mobile deposits often take 1–2 business days to process, while wire transfers are typically same-day. By understanding these timelines, you can better predict when transactions will appear in the bank statement. Regularly review the bank’s online portal for real-time updates, as these often reflect transactions faster than monthly statements.

Finally, implement internal controls to minimize unrecorded transactions. For deposits, ensure receipts are immediately logged in the accounting system, even if the funds haven’t cleared. For payments, reconcile issued checks or electronic transfers against the bank statement weekly, not just monthly. Train staff to document every transaction promptly and accurately, reducing the risk of oversight. By combining vigilance, process improvement, and technology, businesses can significantly reduce reconciliation issues stemming from unrecorded transactions.

Repossessed Cars: A Good Deal or a Money Pit?

You may want to see also

Explore related products

![]()

Timing Differences: Transactions posted in different periods between bank and company records

Timing differences between bank and company records are a common yet often overlooked culprit behind reconciliation discrepancies. These occur when transactions are recorded in different periods by the bank and the business, creating a temporary imbalance. For instance, a company might record a sale on the day an invoice is issued, while the bank only posts the transaction when the payment is received, which could be days or even weeks later. This lag can lead to confusion, especially if the business assumes the funds are immediately available. Understanding this delay is crucial for accurate financial reporting and cash flow management.

Consider a small business that issues an invoice on December 28th and records the revenue immediately. However, the customer’s payment isn’t processed by the bank until January 2nd. In this scenario, the company’s December records will show the transaction, but the bank statement for the same period will not. Without recognizing this timing difference, the business might incorrectly conclude that the bank reconciliation is off due to an error, rather than a simple delay in posting. To address this, businesses should cross-reference transaction dates with bank processing times and adjust their expectations accordingly.

Analyzing these timing differences requires a systematic approach. Start by comparing the dates of transactions in both the company’s ledger and the bank statement. Highlight any entries that fall within a close timeframe but appear in different periods. For example, payments made near the end of a month might not clear until the beginning of the next. Tools like accounting software with reconciliation features can automate this process, flagging potential discrepancies for review. Regularly updating both records and maintaining open communication with the bank can also minimize these issues.

A practical tip for mitigating timing differences is to establish a reconciliation schedule that accounts for typical bank processing delays. For instance, if payments often take 2–3 business days to post, wait until after this period to perform the reconciliation. Additionally, businesses should maintain a buffer in their cash flow projections to accommodate these lags. By recognizing and planning for timing differences, companies can avoid unnecessary stress and ensure their financial records remain accurate and reliable.

Load Airtime Easily: A Step-by-Step Guide Using Skye Bank

You may want to see also

Explore related products

![BML 7mm Heel Lifts, 3pk (Mens Large, Brown [soft]) by BML Basic Physicians Supply, Inc.](https://m.media-amazon.com/images/I/619s94H7HVL._AC_UY218_.jpg)

![]()

Data Entry Errors: Mistakes in recording amounts, dates, or account numbers

A single misplaced decimal point can throw off an entire bank reconciliation. Data entry errors, particularly those involving amounts, dates, or account numbers, are a leading cause of discrepancies. Imagine transposing digits in a $1,250 deposit, recording it as $1,520. This seemingly small mistake creates a $270 imbalance, requiring tedious investigation to uncover.

Even experienced bookkeepers are susceptible. Fatigue, time pressure, or simply a momentary lapse in concentration can lead to these errors.

Let's break down the impact. Mistyping an account number routes a transaction to the wrong account, leaving both the intended and unintended accounts out of sync. Entering the wrong date can cause a transaction to appear in the wrong reconciliation period, creating a phantom discrepancy. And incorrect amounts, as illustrated earlier, directly distort the balance. These errors compound, making reconciliation a frustrating and time-consuming process.

The consequences extend beyond frustration. Unreconciled accounts can lead to inaccurate financial reporting, missed payments, or even overdraft fees.

To minimize data entry errors, implement a multi-pronged approach. First, utilize accounting software with built-in checks and balances. These systems often flag potential errors, such as transposed numbers or unrealistic amounts. Second, establish a double-entry verification process. Have a second pair of eyes review all data entries, especially those involving large sums or sensitive accounts. Finally, encourage a culture of accuracy. Provide training on common data entry pitfalls and emphasize the importance of careful review.

Consider these practical tips:

- Standardize Data Entry: Create templates or drop-down menus for frequently used accounts and transaction types to reduce manual input.

- Utilize Copy and Paste with Caution: While convenient, copying and pasting data increases the risk of propagating errors. Always double-check pasted information.

- Take Breaks: Fatigue is a major contributor to data entry errors. Schedule regular breaks to maintain focus and accuracy.

By acknowledging the prevalence of data entry errors and implementing proactive measures, businesses can significantly improve the accuracy and efficiency of their bank reconciliations. Remember, a little extra attention to detail upfront can save a lot of time and headaches down the line.

Interning at the Central Bank of Kenya: Are Stipends Offered?

You may want to see also

Explore related products

![]()

Bank Fees/Interest: Unaccounted bank charges or interest not reflected in company records

Bank fees and interest charges are often the silent culprits behind reconciliation discrepancies. These seemingly minor expenses can accumulate over time, creating a significant gap between a company's internal records and the bank statement. For instance, a business might overlook monthly maintenance fees, transaction charges, or overdraft penalties, especially if they vary in amount or frequency. Such oversight is common when multiple accounts are managed, and the finance team fails to track these fees systematically.

Identifying the Issue: To pinpoint unaccounted bank fees, start by scrutinizing the bank statement for any charges not reflected in the company's ledger. These could include monthly service fees, ATM charges, wire transfer fees, or interest deductions. Cross-referencing each transaction is crucial, as some fees might be bundled with other transactions, making them easy to miss. For example, a $50 wire transfer fee might be included in a larger payment, requiring a detailed review to identify.

Preventive Measures: Implementing a robust system to capture and record bank fees is essential. This can be achieved by setting up a dedicated expense category for bank charges and ensuring that every statement is thoroughly reviewed. Automating this process through accounting software can significantly reduce errors. For instance, many accounting platforms allow for the automatic import of bank statements, flagging potential fees for review. Additionally, maintaining open communication with the bank to understand their fee structure and any changes can prevent surprises.

The Impact and Resolution: Unrecorded bank fees can lead to a snowball effect, causing recurring reconciliation issues. Over time, this may result in financial misstatements and affect decision-making. To resolve this, a retrospective review of past statements is necessary to identify and record missed charges. Adjusting entries should be made to correct the company's records, ensuring accuracy moving forward. A proactive approach, such as monthly fee audits, can prevent future discrepancies and maintain financial integrity.

In summary, unaccounted bank fees and interest are common yet avoidable causes of reconciliation imbalances. By adopting meticulous review practices and leveraging technology, businesses can ensure that every charge is captured, thereby maintaining accurate financial records. This attention to detail is vital for financial health and compliance, especially in organizations with complex banking activities.

Santander Bank's Guide to Ordering Foreign Currency: Tips and Steps

You may want to see also

Explore related products

![The U.S. Error Coin Bible: [3 in 1] A Comprehensive Visual Guide to Unlock Hidden Value in America’s Rarest Mint Errors and Variations](https://m.media-amazon.com/images/I/71nvBK1NLeL._AC_UY218_.jpg)

![]()

Outstanding Checks: Checks issued but not yet cleared by the bank

Outstanding checks, those issued but not yet cleared by the bank, are a common culprit behind bank reconciliation discrepancies. Imagine writing a check to a vendor, but the recipient hasn’t deposited it yet. Your records show the payment, but the bank statement doesn’t reflect the deduction. This timing gap creates a mismatch, leaving your reconciliation out of balance until the check clears.

To address this, start by identifying all outstanding checks during reconciliation. Compare the check numbers and amounts on your records with those on the bank statement. Any checks listed as paid in your ledger but absent from the bank’s records are outstanding. For example, if you issued Check #1234 for $500 on October 1st, but the October 31st bank statement doesn’t show it, that $500 is the discrepancy.

A practical tip: maintain a separate register or spreadsheet for outstanding checks. Update it monthly, noting the check date, payee, amount, and status (cleared or outstanding). This tool not only streamlines reconciliation but also helps track stale checks—those over six months old that may need to be voided or reissued.

Finally, consider reducing reliance on paper checks. Encourage vendors to accept electronic payments, which clear faster and minimize outstanding check issues. For unavoidable checks, follow up with recipients to confirm receipt and deposit, ensuring timely clearing. By managing outstanding checks proactively, you’ll eliminate a major source of reconciliation headaches.

Step-by-Step Guide to Canceling Your East Bank Club Membership Easily

You may want to see also

Frequently asked questions

Common reasons include unrecorded transactions, timing differences (deposits in transit or outstanding checks), bank errors, or miscalculations in either the company's records or the bank statement.

Unrecorded transactions, such as bank fees, interest income, or automatic deductions, can cause discrepancies if they are not reflected in the company’s books but appear on the bank statement.

Timing differences occur when transactions are recorded in the company’s books but have not yet cleared the bank (e.g., outstanding checks or deposits in transit), or vice versa, leading to mismatches in balances.

Yes, simple errors like transposed numbers, incorrect amounts, or duplicate entries in either the company’s records or the bank statement can prevent the reconciliation from balancing.