Ally Bank, a well-known online bank, offers a range of competitive Certificate of Deposit (CD) rates designed to help savers grow their money securely. With terms ranging from 3 months to 5 years, Ally’s CDs cater to various financial goals, whether you’re looking for short-term liquidity or long-term growth. Their rates are consistently among the highest in the industry, often outperforming traditional brick-and-mortar banks. Additionally, Ally Bank provides flexibility with features like no minimum deposit requirements for most CDs and penalty-free options for early withdrawal on select accounts. This makes Ally an attractive choice for those seeking reliable, high-yield savings solutions.

Explore related products

What You'll Learn

![]()

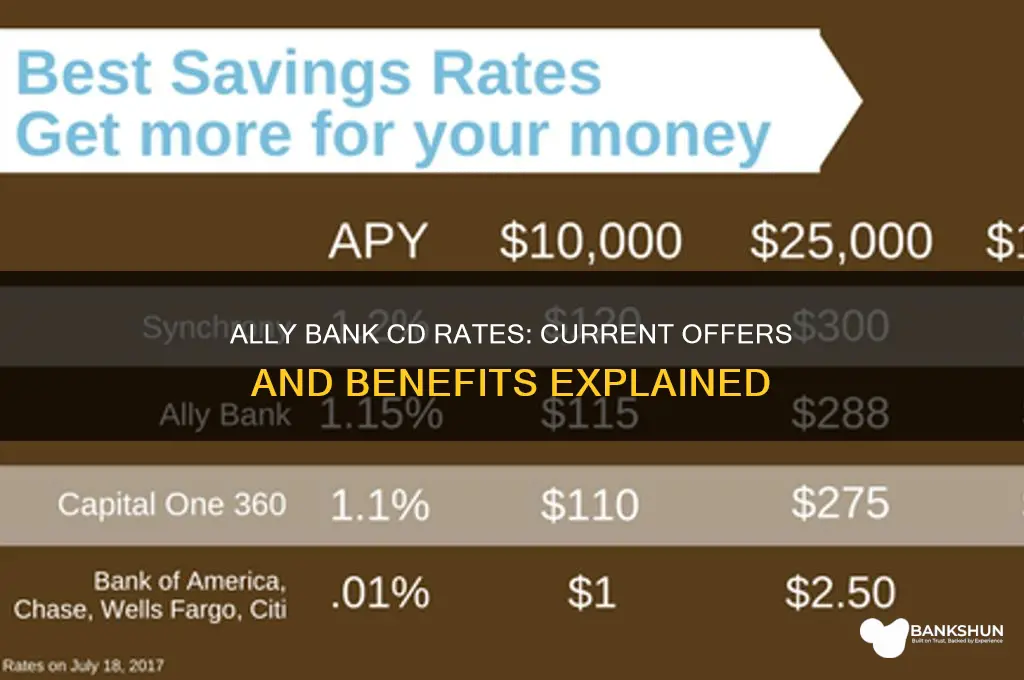

Current Ally Bank CD Rates

Ally Bank's current CD rates are a standout in the digital banking landscape, offering competitive returns that often surpass those of traditional brick-and-mortar institutions. As of the latest update, Ally’s 12-month CD yields 4.85% APY, while its 5-year CD climbs to 4.35% APY. These rates are particularly attractive in a market where many banks struggle to offer above 3% APY on similar terms. For savers seeking predictable growth, Ally’s CDs provide a low-risk avenue to capitalize on higher interest rates without locking funds away for excessively long periods.

One of the most appealing aspects of Ally’s CD offerings is their flexibility. Unlike some banks that penalize early withdrawals with fees as high as 12 months’ interest, Ally’s 11-day Best Rate Guarantee ensures you lock in the highest rate available during the funding period. Additionally, their No Penalty CD allows withdrawals after the first six days of funding without incurring fees, making it an ideal option for those who want liquidity paired with higher returns than a traditional savings account.

Comparatively, Ally’s rates hold strong against competitors like Marcus by Goldman Sachs and Discover Bank. For instance, Marcus offers 4.75% APY on its 12-month CD, while Discover caps at 4.60% APY. Ally’s edge lies not just in slightly higher rates but also in its user-friendly platform and absence of hidden fees. However, for longer-term commitments, some credit unions may offer marginally better rates, though they often require membership or higher minimum deposits.

To maximize Ally’s CD rates, consider a CD laddering strategy. For example, divide $10,000 into four CDs with terms of 6, 12, 18, and 24 months. As each CD matures, reinvest the principal into a new long-term CD, ensuring consistent access to funds while maintaining exposure to higher rates. This approach balances liquidity and growth, especially in a fluctuating interest rate environment.

In conclusion, Ally Bank’s current CD rates are a compelling option for savers prioritizing stability and competitive returns. With terms ranging from 3 months to 5 years, flexible features like the No Penalty CD, and rates consistently above industry averages, Ally positions itself as a top choice for both short-term and long-term savings goals. Always review their latest offerings, as rates fluctuate with market conditions, but as of now, Ally remains a leader in the CD space.

Is Capital One 360 a Massachusetts Bank? Exploring Its Origins

You may want to see also

Explore related products

![]()

Ally Bank CD Term Options

Ally Bank stands out in the digital banking space with its competitive CD rates, but the real flexibility lies in its term options. Ranging from 3 months to 5 years, these terms cater to diverse financial goals. Short-term CDs, like the 3-month or 6-month options, are ideal for those seeking quick liquidity with minimal risk. Conversely, longer terms, such as the 3-year or 5-year CDs, offer higher interest rates for savers willing to commit their funds for an extended period. This tiered approach allows customers to align their savings strategy with their timeline, whether they’re planning for an emergency fund or a long-term financial goal.

Choosing the right CD term requires a strategic mindset. For instance, laddering—a technique where you divide your savings across multiple CDs with varying terms—can optimize returns while maintaining access to funds periodically. Ally Bank’s 1-year CD is a popular choice for laddering, as it strikes a balance between yield and flexibility. However, it’s crucial to consider the Federal Reserve’s interest rate movements; locking into a long-term CD during a rising rate environment might mean missing out on higher yields later. Ally’s no-penalty 11-month CD offers a unique solution, allowing early withdrawals without penalty, though it typically comes with a slightly lower rate.

One of Ally Bank’s most appealing features is its High Yield CD, which combines competitive rates with term flexibility. For example, a 2-year High Yield CD currently offers a rate significantly above the national average, making it an attractive option for mid-term savers. Additionally, Ally’s Raise Your Rate CDs provide a safety net for those worried about future rate increases. This product allows you to increase your rate once (for 2-year terms) or twice (for 4-year terms) if Ally’s rates rise during your term. This feature adds a layer of adaptability rarely seen in traditional CDs.

For those new to CDs, Ally Bank simplifies the process with straightforward terms and no hidden fees. Opening a CD requires a minimum deposit of $0, making it accessible to savers at all levels. However, it’s essential to note that early withdrawals typically incur a penalty, ranging from 60 days of interest for terms under 24 months to 150 days for longer terms. To maximize returns, consider setting up automatic renewals or transferring funds to a higher-yielding account upon maturity. Ally’s user-friendly platform makes these adjustments seamless, ensuring your savings strategy remains on track.

In summary, Ally Bank’s CD term options are designed to meet a wide range of financial needs, from short-term liquidity to long-term growth. By understanding the nuances of each term and leveraging strategies like laddering or Raise Your Rate CDs, savers can optimize their returns while maintaining flexibility. Whether you’re a seasoned investor or just starting, Ally’s transparent terms and competitive rates make it a top contender in the CD market. Always assess your financial goals and risk tolerance before committing to a term, and remember that the right CD can be a powerful tool in your savings arsenal.

SBA 7(a) Program: Partnering with Banks for Success

You may want to see also

Explore related products

![]()

Minimum Deposit Requirements

Ally Bank stands out in the competitive landscape of online banking with its accessible Certificate of Deposit (CD) options, particularly when it comes to minimum deposit requirements. Unlike traditional banks that often mandate hefty initial deposits, Ally Bank sets the bar remarkably low, requiring just $0 to open a CD account. This zero-dollar entry point democratizes access to CD investments, allowing individuals with varying financial capacities to take advantage of fixed, competitive interest rates. For those new to investing or working with limited funds, this feature removes a significant barrier, making Ally Bank an attractive choice for building savings.

Consider the practical implications of this low threshold. A college student with a part-time job, for instance, could allocate even $50 into a CD without worrying about meeting a high minimum deposit. Similarly, someone looking to diversify their savings portfolio can start small, testing the waters without committing substantial funds. Ally Bank’s approach aligns with the principle of micro-investing, where small, consistent contributions can accumulate over time, especially when paired with compound interest. This flexibility not only fosters financial inclusion but also encourages disciplined saving habits.

However, while the $0 minimum deposit is a clear advantage, it’s essential to weigh it against other factors. Ally Bank offers a range of CD terms, from 3 months to 5 years, each with its own interest rate. Longer-term CDs typically yield higher returns but require locking in funds for an extended period. For example, a 5-year CD might offer a more attractive rate than a 3-month CD, but the trade-off is reduced liquidity. Investors should assess their financial goals and liquidity needs before committing, even if the initial deposit is minimal.

Another critical aspect to consider is the opportunity cost of tying up funds in a CD, regardless of the deposit size. While Ally Bank’s CDs are FDIC-insured up to $250,000, making them a low-risk investment, the fixed nature of CDs means missing out on potential higher returns from more volatile assets like stocks. For instance, someone with a $500 deposit might opt for a high-yield savings account instead if they anticipate needing the funds within a year. Ally Bank’s no-penalty CD, which allows withdrawal without fees after the first six days of funding, offers a middle ground, but its rates are generally lower than those of traditional CDs.

In conclusion, Ally Bank’s $0 minimum deposit requirement for CDs is a game-changer for individuals seeking low-risk, accessible investment options. It empowers savers to start small, fostering financial discipline and inclusivity. Yet, investors must balance this accessibility with considerations like term length, interest rates, and liquidity needs. By understanding these nuances, one can maximize the benefits of Ally Bank’s CD offerings while aligning them with personal financial objectives.

Exploring Union Bank's Network: Total Number of Branches Revealed

You may want to see also

Explore related products

![]()

Early Withdrawal Penalties

Ally Bank's CD rates are competitive, but understanding the early withdrawal penalties is crucial for anyone considering locking their money away. These penalties can significantly impact your earnings if you need access to your funds before the CD matures. Ally Bank's penalty structure is straightforward: for CDs with terms of 24 months or less, you'll forfeit 60 days of interest; for CDs with terms longer than 24 months, the penalty increases to 150 days of interest. This means that if you withdraw early, you could lose a substantial portion of the interest you’ve earned, potentially even dipping into your principal if the withdrawal is made too early in the term.

Let’s break this down with an example. Suppose you invest $10,000 in a 3-year Ally CD with an annual percentage yield (APY) of 4.5%. Over the term, you’d earn approximately $1,350 in interest. However, if you withdraw after 18 months, you’ll lose 150 days of interest. At a daily interest rate of about $1.23, the penalty would be roughly $184.50. This reduces your total earnings to $1,165.50, a noticeable difference. The takeaway here is that while Ally’s rates are attractive, early withdrawals can erode your returns, making it essential to plan carefully before committing to a long-term CD.

To minimize the risk of early withdrawal penalties, consider laddering your CDs. This strategy involves dividing your investment across multiple CDs with varying terms. For instance, instead of putting all $10,000 into a single 3-year CD, you could invest $2,500 in a 1-year CD, $2,500 in a 2-year CD, and $5,000 in a 3-year CD. As each CD matures, you can reinvest the funds or use them without incurring penalties. This approach provides flexibility while still allowing you to take advantage of higher long-term rates.

Another practical tip is to maintain an emergency fund separate from your CD investments. Financial experts recommend having three to six months’ worth of living expenses in a liquid account, such as a high-yield savings account. This buffer ensures that you won’t need to dip into your CDs prematurely, avoiding penalties and preserving your earnings. Ally Bank offers a competitive savings account that can serve as an excellent complement to your CD portfolio, providing both growth and accessibility.

Finally, if you’re still uncertain about committing to a CD, Ally Bank’s No Penalty CD is worth considering. This product allows you to withdraw your funds penalty-free after the first six days of funding, offering flexibility without sacrificing the benefits of a fixed rate. While the APY on this CD is typically lower than traditional options, it’s an ideal choice for those who prioritize liquidity over maximum returns. By weighing your financial goals and risk tolerance, you can choose the CD product that best aligns with your needs while avoiding the pitfalls of early withdrawal penalties.

Exploring the NYCB Family of Banks: A Comprehensive Overview

You may want to see also

Explore related products

![]()

Ally Bank No Penalty CD

Ally Bank's No Penalty CD stands out in the crowded field of certificate of deposit options by offering a unique blend of flexibility and competitive rates. Unlike traditional CDs, which lock in your funds for a fixed term and impose penalties for early withdrawal, this product allows you to withdraw your full balance without penalty after the first six days of funding. This feature makes it an attractive choice for savers who want higher returns than a savings account but hesitate to commit their funds long-term.

Consider the scenario where you have an emergency fund you want to grow but need to keep accessible. The No Penalty CD lets you take advantage of CD-level interest rates without the risk of losing money if you need to access your funds unexpectedly. Ally Bank currently offers a 11-month No Penalty CD with a rate of 4.75% APY (as of October 2023), which is significantly higher than the national average for savings accounts. This rate is variable, so it’s wise to monitor it periodically, but historically, Ally has kept its rates competitive.

One practical tip for maximizing this product is to ladder your No Penalty CDs. Start by opening one CD and then open another a month later. This strategy ensures that you have a CD maturing regularly, giving you access to funds while still earning higher interest rates. For example, if you have $10,000, put $5,000 into a No Penalty CD today and the remaining $5,000 into another CD next month. This way, you maintain liquidity while optimizing returns.

However, it’s important to note that the No Penalty CD isn’t ideal for everyone. If you’re certain you won’t need your funds for an extended period, a traditional CD with a longer term might offer a higher rate. Additionally, while Ally Bank doesn’t charge penalties for early withdrawal, you must keep the account open for at least six days to avoid forfeiting interest. Always review the terms carefully before committing.

In conclusion, Ally Bank’s No Penalty CD is a versatile tool for savers seeking a balance between growth and accessibility. Its competitive rate, combined with the freedom to withdraw funds without penalty, makes it a standout option in the market. By understanding its features and strategically incorporating it into your savings plan, you can enhance your financial flexibility without sacrificing returns.

How Long Does Virgin Travel Bank Last? A Comprehensive Guide

You may want to see also

Frequently asked questions

Ally Bank offers competitive rates for short-term CDs, typically ranging from 3 months to 12 months. Rates vary based on market conditions, but they are often higher than traditional savings accounts.

Yes, Ally Bank offers higher CD rates for longer terms, such as 18 months, 3 years, and 5 years. Longer-term CDs generally yield better returns compared to shorter-term options.

Ally Bank’s CD rates are fixed for the term of the CD. Once you open a CD, the rate remains the same until maturity, regardless of market fluctuations.

Yes, Ally Bank offers a No Penalty CD with a competitive rate. This CD allows you to withdraw your money without penalty after the first six days of funding, providing flexibility while still earning interest.

![Ally Mcbeal: Season 3 [DVD] [UK Import]](https://m.media-amazon.com/images/I/41KgqWA9POL._AC_UL320_.jpg)