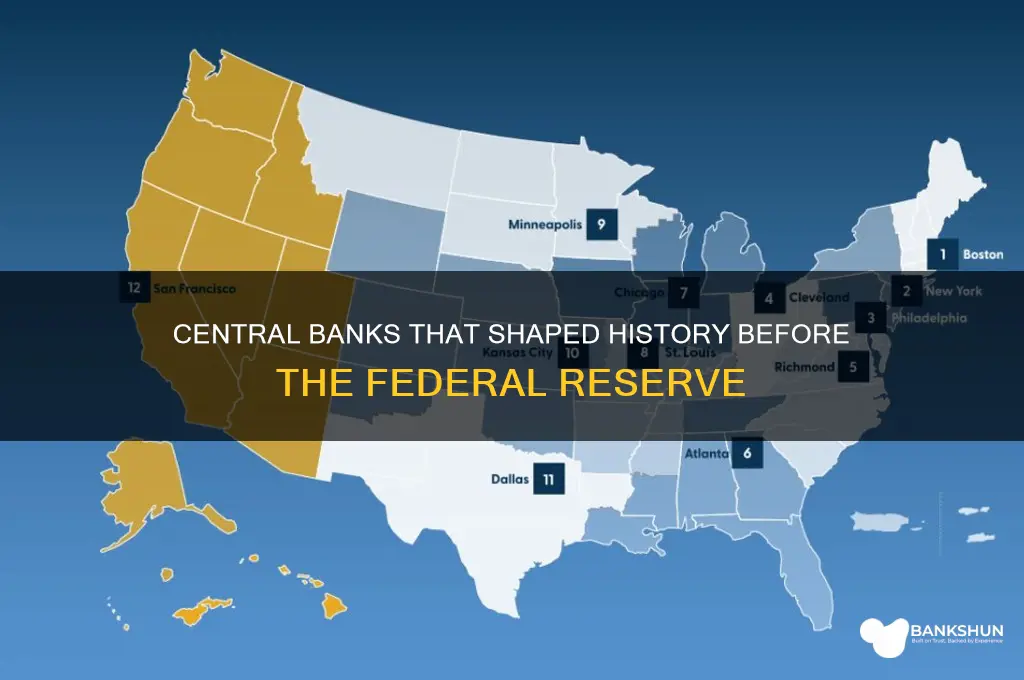

Before the establishment of the Federal Reserve Bank in 1913, several central banking institutions existed in the United States, each with varying degrees of success and influence. The First Bank of the United States, chartered in 1791 under Alexander Hamilton's leadership, was the nation's initial attempt at a central bank, aimed at managing the country's finances post-Revolutionary War. However, its charter expired in 1811 due to political opposition. The Second Bank of the United States, chartered in 1816, faced similar challenges and was ultimately disbanded in 1836 after President Andrew Jackson vetoed its recharter. In the absence of a formal central bank, state-chartered banks and the free banking era prevailed, leading to financial instability and a series of panics, most notably the Panic of 1907, which highlighted the need for a more robust and centralized banking system, ultimately paving the way for the creation of the Federal Reserve.

Explore related products

What You'll Learn

- Early U.S. Banking Attempts: First and Second Banks of the United States (1791-1811, 1816-1836)

- State-Chartered Banks: Independent state banks issued currency, leading to financial instability

- Free Banking Era: Unregulated banking system (1837-1863) with widespread bank failures

- National Banking System: Established in 1863 to standardize currency and regulate banks

- Panic of 1907: Financial crisis highlighted need for a central banking authority

![]()

Early U.S. Banking Attempts: First and Second Banks of the United States (1791-1811, 1816-1836)

The United States, in its infancy, grappled with the need for a stable financial system. This led to the creation of the First Bank of the United States in 1791, a pivotal moment in the nation's financial history. Chartered for 20 years, this bank was a brainchild of Alexander Hamilton, the first Secretary of the Treasury. Its primary objectives were to manage the country's financial affairs, stabilize the currency, and foster economic growth. The bank's establishment marked a significant shift from the post-revolutionary war era, where state banks issued their own currencies, leading to a chaotic and unstable financial environment.

The First Bank's operations were multifaceted. It acted as a fiscal agent for the government, managing tax revenues and making payments on behalf of the federal government. Additionally, it regulated the money supply by issuing banknotes backed by gold and silver reserves, thereby instilling confidence in the currency. The bank's influence extended to the private sector, providing loans to businesses and individuals, which stimulated economic activity. However, its existence was not without controversy. Critics, led by Thomas Jefferson, argued that the bank's centralized power posed a threat to states' rights and democratic principles. This ideological divide ultimately led to the bank's charter not being renewed in 1811, marking the end of its initial 20-year run.

The aftermath of the First Bank's closure revealed the nation's financial vulnerabilities. The War of 1812 exacerbated these issues, highlighting the need for a centralized banking system. In response, the Second Bank of the United States was chartered in 1816, with a 20-year mandate. This bank aimed to address the shortcomings of its predecessor, focusing on maintaining financial stability and regulating state banks. It employed various tools, such as open market operations and reserve requirements, to control the money supply and prevent excessive inflation or deflation. The Second Bank's influence was more pronounced, as it established branches across the country, extending its reach and impact on the national economy.

Despite its successes, the Second Bank faced intense opposition, particularly from President Andrew Jackson. Jackson, a staunch advocate of states' rights, viewed the bank as a symbol of federal overreach and elitism. He vetoed the recharter bill in 1832, arguing that the bank benefited the wealthy at the expense of the common man. This decision marked a significant turning point, as it led to the eventual demise of the Second Bank in 1836. The subsequent era, known as the "Free Banking" period, saw a proliferation of state-chartered banks, but it also brought increased financial instability and a lack of uniform currency. The experiences of the First and Second Banks of the United States underscore the complexities of establishing a central banking system in a young nation, shaping the future of American financial policy.

In retrospect, the First and Second Banks of the United States served as crucial experiments in central banking. They demonstrated the importance of a stable financial system in fostering economic growth and the challenges of balancing centralized power with democratic ideals. The lessons learned from these early attempts laid the groundwork for future financial institutions, ultimately influencing the creation of the Federal Reserve System in 1913. By examining the successes and failures of these banks, we gain valuable insights into the evolution of central banking and its role in shaping a nation's economic trajectory. This historical perspective is essential for understanding the complexities of modern financial systems and the ongoing debates surrounding central bank independence and policy.

How to Locate Your Bank's EIN: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

State-Chartered Banks: Independent state banks issued currency, leading to financial instability

Before the establishment of the Federal Reserve Bank, the United States financial system was a patchwork of state-chartered banks, each operating with considerable autonomy. These banks had the authority to issue their own currency, a practice that, while fostering local economic growth, also sowed the seeds of widespread financial instability. The absence of a centralized regulatory authority meant that the value and acceptance of these currencies varied wildly, creating confusion and risk for both consumers and businesses.

Consider the practical implications for a merchant in the late 19th century. Accepting a banknote from a state-chartered bank in another region was a gamble. The note’s value depended on the issuing bank’s solvency, which was often uncertain. This uncertainty discouraged interstate trade and investment, as merchants and investors lacked confidence in the medium of exchange. For instance, during the Panic of 1907, many state-chartered banks failed, rendering their currencies worthless and leaving depositors and creditors in financial ruin.

The analytical lens reveals a systemic flaw: the lack of uniformity in currency issuance. Each state-chartered bank operated under its own rules, leading to over 8,000 different types of banknotes in circulation by the early 20th century. This fragmentation made it nearly impossible to maintain a stable monetary system. Counterfeiting was rampant, further eroding trust in the banking system. The takeaway is clear: decentralized currency issuance without oversight is a recipe for economic chaos.

To address this instability, reformers advocated for a centralized banking system. The Federal Reserve Act of 1913 was the culmination of these efforts, establishing a national currency and a system of regional Federal Reserve Banks to regulate monetary policy. State-chartered banks were brought under federal oversight, and their ability to issue currency was severely restricted. This shift marked a turning point, replacing financial unpredictability with a framework designed to ensure stability and uniformity.

In conclusion, the era of state-chartered banks issuing their own currency highlights the dangers of unchecked decentralization in monetary systems. While these banks played a role in local economic development, their independence contributed to widespread financial instability. The lessons from this period underscore the importance of centralized regulation and standardized currency in fostering a stable and trustworthy financial environment.

Should You Invest in Yes Bank Shares? A Comprehensive Analysis

You may want to see also

Explore related products

![]()

Free Banking Era: Unregulated banking system (1837-1863) with widespread bank failures

The Free Banking Era, spanning from 1837 to 1863, was a period of profound experimentation in the American banking system, marked by the absence of a central regulatory authority. During this time, states granted banking charters with minimal oversight, allowing virtually anyone to establish a bank by meeting basic capital requirements. This laissez-faire approach aimed to democratize banking and stimulate economic growth, but it also sowed the seeds of instability. Banks issued their own currency, often backed by questionable assets, leading to widespread confusion and mistrust among the public. The era’s lack of uniform standards and regulatory safeguards set the stage for frequent bank failures, which eroded confidence in the financial system and highlighted the need for centralized oversight.

One of the most striking features of the Free Banking Era was the sheer volume of bank notes in circulation, each issued by a different institution. While this diversity initially seemed to foster competition, it quickly became a liability. Counterfeiting was rampant, and the value of bank notes fluctuated wildly depending on the perceived solvency of the issuing bank. Farmers, merchants, and ordinary citizens bore the brunt of this volatility, as their savings could be wiped out overnight if a bank collapsed. For instance, in New York alone, over 20% of free banks failed during this period, leaving depositors with worthless currency. This unpredictability underscored the dangers of an unregulated system and the imperative for a more stable financial framework.

A closer examination of the Free Banking Era reveals both its ambitions and its flaws. Proponents argued that market forces would naturally weed out weak banks, ensuring only the strongest survived. However, this theory ignored the systemic risks posed by interconnected financial institutions. When one bank failed, it often triggered a domino effect, as depositors rushed to withdraw funds from other banks, leading to widespread panics. The era’s most notorious example is the Panic of 1837, which precipitated a prolonged economic depression. This crisis demonstrated that self-regulation was insufficient to prevent catastrophic failures, particularly in the absence of a lender of last resort.

To navigate the challenges of the Free Banking Era, individuals had to become de facto experts in assessing bank solvency. Practical tips included scrutinizing a bank’s asset portfolio, monitoring its lending practices, and diversifying holdings across multiple institutions. However, such vigilance was impractical for most people, especially in rural areas with limited access to information. The era’s failures ultimately paved the way for the National Banking Act of 1863, which established a uniform currency and laid the groundwork for federal oversight. While the Free Banking Era was a bold experiment, its legacy is a cautionary tale about the limits of unregulated markets and the indispensable role of central banking in maintaining financial stability.

Securely Stacking Silver: A Step-by-Step Guide to Bank Purchases

You may want to see also

Explore related products

![]()

National Banking System: Established in 1863 to standardize currency and regulate banks

The National Banking System, established in 1863, marked a pivotal shift in American financial history by addressing the chaos of a fragmented banking system. Before its creation, the United States lacked a uniform currency, with over 8,000 types of banknotes issued by state-chartered banks. This patchwork system led to widespread confusion, counterfeiting, and economic instability, particularly during the Civil War when the Union needed a reliable financial backbone to fund its efforts. The National Banking System introduced a standardized national currency, backed by U.S. government bonds, which not only stabilized the economy but also provided a mechanism for financing the war.

To achieve its goals, the system implemented a three-tiered structure: national banks, the Comptroller of the Currency, and the U.S. Treasury. National banks were chartered by the federal government and required to purchase government bonds, which served as collateral for issuing banknotes. The Comptroller of the Currency was tasked with overseeing these banks, ensuring compliance with federal regulations, and maintaining the integrity of the banking system. Meanwhile, the U.S. Treasury played a crucial role in issuing and regulating the new national currency, which quickly replaced the myriad state banknotes. This centralized approach laid the groundwork for a more stable and unified financial system.

One of the most significant impacts of the National Banking System was its role in reducing counterfeiting. Prior to 1863, counterfeit banknotes were rampant, eroding public trust in the currency. The new system introduced standardized designs, watermarks, and other security features, making counterfeiting far more difficult. Additionally, the requirement for national banks to back their currency with government bonds ensured that banknotes were redeemable in gold or legal tender, further bolstering confidence. This standardization not only protected consumers but also facilitated interstate commerce by creating a universally accepted medium of exchange.

Despite its successes, the National Banking System was not without limitations. It failed to address the issue of bank panics, which continued to plague the economy in the late 19th and early 20th centuries. The system’s reliance on a fixed supply of currency, tied to the amount of government bonds held by national banks, made it inflexible during economic downturns. This rigidity highlighted the need for a more dynamic institution capable of responding to financial crises—a gap eventually filled by the establishment of the Federal Reserve System in 1913.

In retrospect, the National Banking System served as a critical stepping stone in the evolution of U.S. central banking. It demonstrated the importance of a standardized currency and federal oversight in maintaining economic stability. However, its shortcomings underscored the necessity of a more adaptable and proactive financial authority. By standardizing currency and regulating banks, the system laid the foundation for the Federal Reserve, which would later build upon its principles to create a more resilient and responsive monetary framework.

Word Bank vs. Matching: Understanding the Key Differences in Learning Tools

You may want to see also

Explore related products

$40.6 $58

![]()

Panic of 1907: Financial crisis highlighted need for a central banking authority

The Panic of 1907 was a financial crisis that exposed the fragility of the U.S. banking system, revealing a critical need for a central banking authority. Unlike Europe, where central banks like the Bank of England had long served as lenders of last resort, the U.S. relied on a decentralized system of private banks and trusts. When a failed attempt to manipulate the stock market triggered a run on banks, the system collapsed under the weight of panic and liquidity shortages. This crisis underscored the absence of a stabilizing force to inject funds into the economy during emergencies.

Consider the sequence of events: a failed corner on United Copper stock led to the insolvency of several prominent banks and trusts, sparking widespread fear. Depositors rushed to withdraw funds, but without a central authority to provide liquidity, banks were forced to suspend payments. The economy ground to a halt as credit dried up, businesses failed, and unemployment soared. J.P. Morgan, a private banker, stepped in to organize a bailout, but his efforts highlighted the ad hoc nature of crisis management. This makeshift solution was no substitute for a structured, centralized response.

The Panic of 1907 served as a turning point, catalyzing public and political demand for reform. It demonstrated that private interests, no matter how powerful, could not reliably stabilize a financial system during a crisis. The Aldrich-Vreeland Act of 1908 was a temporary fix, allowing national banks to issue emergency currency, but it fell short of creating a permanent solution. The crisis laid bare the necessity of a central institution to regulate monetary policy, manage liquidity, and act as a lender of last resort—roles that would later be fulfilled by the Federal Reserve.

To understand the impact, compare the U.S. response to that of nations with established central banks. During the same period, the Bank of England successfully averted similar panics by injecting liquidity and reassuring markets. This contrast illustrated the advantages of a centralized authority in maintaining financial stability. The Panic of 1907 was not just a failure of individual banks but a systemic failure of the U.S. financial architecture, one that demanded a comprehensive solution.

The takeaway is clear: the Panic of 1907 was a wake-up call that the U.S. could no longer afford to operate without a central banking authority. It exposed the limitations of decentralized, private-led crisis management and paved the way for the creation of the Federal Reserve in 1913. This crisis remains a cautionary tale, reminding us that financial stability requires more than just individual institutions—it demands a coordinated, centralized framework to safeguard the economy.

Donating Sperm: A Guide to the Process and Requirements

You may want to see also

Frequently asked questions

Before the Federal Reserve Bank was established in 1913, several central banking institutions existed globally, including the Bank of England (1694), the Bank of France (1800), the Bank of Japan (1882), and the Reichsbank in Germany (1876).

Yes, the United States had two earlier central banking attempts: the First Bank of the United States (1791–1811) and the Second Bank of the United States (1816–1836), both of which were chartered by Congress but ultimately dissolved.

Central banks were established to stabilize currencies, manage national debts, and provide financial services to governments. They also aimed to regulate banking systems and ensure economic stability during crises.

The Federal Reserve was designed as a decentralized system with 12 regional banks, unlike earlier central banks that were more centralized. It also had a dual mandate to stabilize prices and maximize employment, which was unique compared to the narrower focuses of its predecessors.