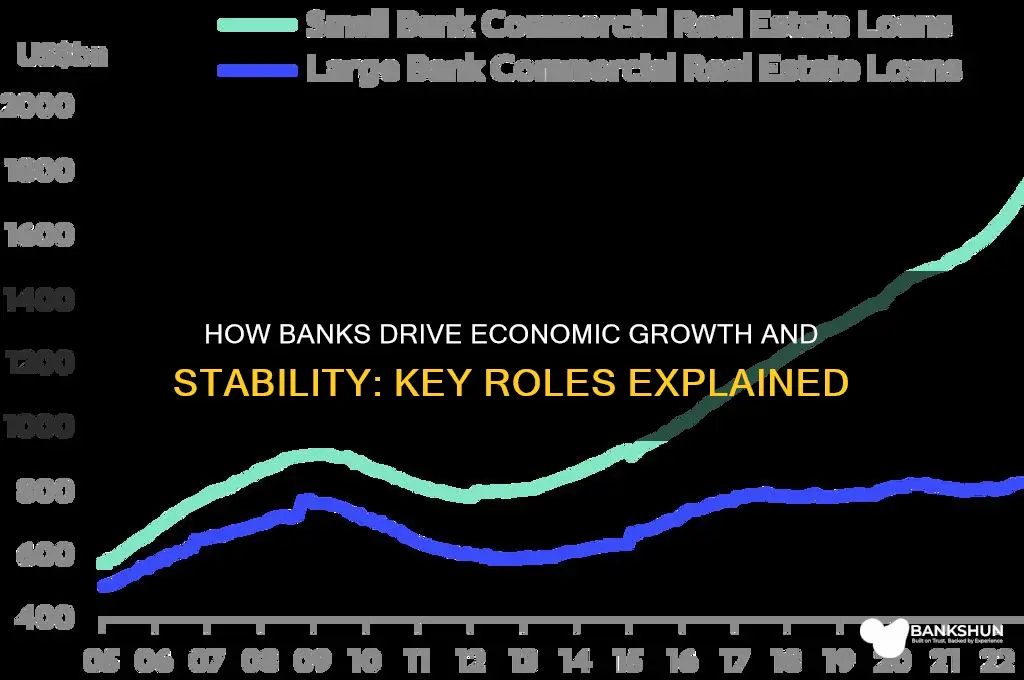

Banks play a crucial role in the economy by facilitating the flow of money and credit, which is essential for economic growth and stability. They act as intermediaries between savers and borrowers, collecting deposits from individuals and businesses and lending those funds to others who need capital for investments, purchases, or operations. Through this process, banks enable businesses to expand, individuals to buy homes or start ventures, and governments to finance public projects. Additionally, banks provide payment systems, manage risks, and support financial inclusion, ensuring that economic activities run smoothly and efficiently. By influencing interest rates, managing liquidity, and safeguarding assets, banks also contribute to monetary policy and overall economic resilience.

| Characteristics | Values |

|---|---|

| Financial Intermediation | Banks act as intermediaries between savers and borrowers, channeling funds from those with surplus capital to those in need of financing. In 2023, global bank credit to the private sector reached approximately $150 trillion (Source: World Bank). |

| Payment Systems | Banks facilitate the transfer of funds through various payment systems, including wire transfers, debit/credit cards, and digital wallets. In 2022, non-cash transactions globally exceeded 500 billion annually (Source: World Payments Report). |

| Credit Creation | Banks create credit by lending out deposits, which increases the money supply in the economy. As of 2023, the global money supply (M2) stood at over $100 trillion (Source: IMF). |

| Economic Growth | Banks provide financing for businesses, infrastructure, and households, driving economic growth. In 2023, bank lending to SMEs contributed to 30-40% of GDP in developed economies (Source: OECD). |

| Risk Management | Banks help manage financial risks through products like insurance, derivatives, and hedging tools. The global derivatives market size in 2023 was valued at $15 trillion (Source: BIS). |

| Monetary Policy Transmission | Banks play a crucial role in implementing monetary policy by adjusting interest rates and credit availability. Central bank interest rates in 2023 ranged from 0.5% to 5.5% across major economies (Source: Bloomberg). |

| Financial Inclusion | Banks expand access to financial services, reducing inequality. As of 2023, 76% of adults globally had a bank account (Source: World Bank). |

| Stability and Trust | Banks maintain financial stability by adhering to regulations and ensuring liquidity. In 2023, the global bank capital adequacy ratio averaged 15.5%, above regulatory requirements (Source: Basel Committee). |

| Investment and Savings | Banks encourage savings and provide investment opportunities through deposits, bonds, and mutual funds. Global household savings in 2023 totaled $50 trillion (Source: McKinsey). |

| Innovation and Technology | Banks drive financial innovation through digital banking, fintech partnerships, and blockchain. In 2023, global fintech investment reached $130 billion (Source: CB Insights). |

Explore related products

What You'll Learn

- Facilitate Payments: Enable transactions, ensuring smooth flow of money between individuals, businesses, and governments

- Provide Loans: Offer credit to stimulate growth, supporting businesses, homebuyers, and personal investments

- Manage Risk: Mitigate financial risks through insurance, hedging, and diversified investment products

- Mobilize Savings: Pool deposits to fund economic activities, fostering investment and development

- Support Stability: Act as intermediaries, maintaining liquidity and preventing economic shocks

![]()

Facilitate Payments: Enable transactions, ensuring smooth flow of money between individuals, businesses, and governments

Banks act as the circulatory system of the economy, ensuring the seamless flow of money between individuals, businesses, and governments. Without this facilitation, transactions would grind to a halt, stifling economic activity. Consider the complexity of a simple purchase: a customer swipes a card, and within seconds, funds transfer from their account to the merchant’s. This instantaneous exchange, enabled by banks, underpins daily commerce and fosters trust in the financial system.

The mechanics of payment facilitation involve a network of systems, from debit and credit card processing to wire transfers and direct deposits. For instance, the Automated Clearing House (ACH) network processes over 29 billion transactions annually in the U.S. alone, handling everything from payroll to bill payments. Banks act as intermediaries, verifying identities, ensuring sufficient funds, and settling transactions securely. This reduces friction in the economy, allowing businesses to operate efficiently and individuals to manage finances with ease.

However, the role of banks in payment facilitation extends beyond mere convenience. It is a critical function that supports economic stability. During crises, such as the COVID-19 pandemic, banks enabled governments to distribute stimulus payments swiftly, mitigating economic hardship. Similarly, businesses relied on payment systems to adapt to remote work and online sales, highlighting the resilience of bank-enabled transactions. Without this infrastructure, economic recovery would have been far slower and more chaotic.

To maximize the benefits of bank-facilitated payments, individuals and businesses should leverage available tools strategically. For example, small businesses can reduce costs by using low-fee payment processors and automating recurring transactions. Individuals can protect themselves from fraud by monitoring accounts regularly and using secure payment methods like chip-enabled cards or digital wallets. Governments, meanwhile, can invest in modernizing payment systems to enhance speed, security, and inclusivity, ensuring no one is left behind in the digital economy.

In conclusion, banks’ role in facilitating payments is not just operational—it is foundational to economic vitality. By enabling transactions with speed, security, and efficiency, banks ensure that money flows where it is needed, when it is needed. This function supports growth, stabilizes economies, and empowers individuals and businesses alike. As technology evolves, banks must continue to innovate, ensuring payment systems remain robust, inclusive, and adaptable to the demands of a dynamic global economy.

Unblock Your KCB Mobile Banking PIN: A Quick Step-by-Step Guide

You may want to see also

Explore related products

![]()

Provide Loans: Offer credit to stimulate growth, supporting businesses, homebuyers, and personal investments

Banks play a pivotal role in economic growth by providing loans, which act as the lifeblood for various sectors. For businesses, access to credit enables expansion, innovation, and job creation. A small tech startup, for instance, might secure a $500,000 loan to develop a new product, hire engineers, and scale operations. This not only boosts the company’s revenue but also contributes to the broader economy through increased tax income and consumer spending. Similarly, homebuyers rely on mortgages to purchase property, a cornerstone of personal wealth accumulation and housing market stability. Without such financing, many would remain renters, limiting both individual financial growth and the construction industry’s vitality.

The mechanics of loan provision reveal a delicate balance between risk and reward. Banks assess creditworthiness through metrics like credit scores, income stability, and debt-to-income ratios. For example, a borrower with a 720 credit score and a 30% down payment is more likely to secure a favorable mortgage rate. This evaluation ensures that funds are allocated efficiently, minimizing defaults while maximizing economic impact. However, stringent criteria can exclude underserved populations, such as low-income entrepreneurs or first-time homebuyers, highlighting the need for inclusive lending practices like microloans or government-backed programs.

From a persuasive standpoint, loans are not just financial tools but catalysts for societal progress. Consider the ripple effect of a $1 million loan to a renewable energy firm. The company installs solar panels, reduces carbon emissions, and creates green jobs, aligning economic growth with environmental sustainability. Personal loans for education or home improvements similarly empower individuals to invest in themselves, fostering long-term productivity and quality of life. Critics may argue that debt burdens individuals, but when structured responsibly, loans transform aspirations into achievements, driving collective prosperity.

A comparative analysis underscores the global significance of loan provision. In developed economies, banks offer diverse products—from business lines of credit to auto loans—fueling consumerism and innovation. In contrast, emerging markets often lack robust banking systems, stifling entrepreneurial potential. For example, while U.S. small businesses access over $600 billion in loans annually, African entrepreneurs secure less than 20% of their financing needs. Bridging this gap through initiatives like digital lending platforms or international partnerships could unlock trillions in economic value, proving that the reach and structure of loan systems directly correlate with national development.

In conclusion, providing loans is not merely a banking function but a strategic lever for economic transformation. By tailoring credit to diverse needs—whether funding a bakery’s expansion or a family’s first home—banks catalyze growth at both micro and macro levels. Yet, this power comes with responsibility: ensuring equitable access, managing risk, and aligning lending with broader societal goals. As economies evolve, so must lending practices, adapting to technological advancements, demographic shifts, and global challenges. Ultimately, the loan is more than a transaction—it’s a promise of possibility, turning financial resources into real-world impact.

Travel Bank vs. Miles: Which United Option Maximizes Your Rewards?

You may want to see also

Explore related products

$51.06 $54.99

![]()

Manage Risk: Mitigate financial risks through insurance, hedging, and diversified investment products

Financial instability can cripple economies, but banks act as shock absorbers by offering tools to manage risk. Insurance products, for instance, transfer the burden of potential losses from individuals and businesses to entities better equipped to handle them. A farmer insuring his crop against drought doesn't just protect his livelihood; he safeguards the stability of the agricultural supply chain and the businesses dependent on it. Similarly, a homeowner's insurance policy doesn't just rebuild a house after a fire; it prevents a family from spiraling into debt, allowing them to continue contributing to the economy.

Banks also facilitate hedging, allowing participants to lock in prices for future transactions. Imagine an airline concerned about rising fuel costs. By entering into a fuel futures contract, they effectively cap their expenses, ensuring profitability even if oil prices surge. This predictability encourages investment and expansion, fostering economic growth.

Diversified investment products offered by banks further mitigate risk by spreading exposure across various asset classes. A retiree relying solely on stocks for income is vulnerable to market downturns. However, a balanced portfolio including bonds, real estate, and commodities provides a safety net, ensuring a more stable income stream even during volatile periods. This stability allows individuals to plan for the future, make long-term investments, and contribute to economic activity with greater confidence.

It's crucial to remember that risk management isn't about eliminating risk entirely, but about managing its impact. Banks, through their risk management tools, act as facilitators, enabling individuals and businesses to navigate uncertainty and participate in the economy with greater resilience. This, in turn, fosters a more stable and prosperous economic environment for all.

Can You Trade Stock Options with ICICI Bank? Find Out Here

You may want to see also

Explore related products

![]()

Mobilize Savings: Pool deposits to fund economic activities, fostering investment and development

Banks play a pivotal role in transforming idle savings into productive capital, a process that fuels economic growth and development. By pooling deposits from individuals and businesses, banks create a reservoir of funds that can be channeled into loans, investments, and other economic activities. This mechanism not only ensures that savings are utilized efficiently but also democratizes access to capital, enabling both small-scale entrepreneurs and large corporations to pursue their ventures. For instance, a small business owner in a rural area might secure a loan to expand operations, creating jobs and stimulating local economies. Similarly, a multinational corporation could access funds to finance innovation or infrastructure projects, driving national and global economic progress.

Consider the practical steps involved in this process. When you deposit money into a bank, it doesn’t sit idle. Instead, the bank uses a portion of these funds to extend loans, adhering to regulatory requirements that ensure liquidity and stability. For example, in the U.S., banks are required to maintain a reserve ratio of 10% of their deposits, meaning 90% can be lent out. This multiplier effect amplifies the impact of individual savings, turning $10,000 in deposits into $100,000 in loans across the economy. This system is not without risks, however. Banks must carefully assess creditworthiness to avoid defaults, which can destabilize the financial system. Prudent risk management, therefore, is critical to sustaining this economic function.

From a comparative perspective, the role of banks in mobilizing savings contrasts sharply with informal lending systems or hoarding practices. In economies where formal banking is underdeveloped, savings often remain untapped or are channeled into unproductive assets like gold or real estate. For example, in some developing countries, individuals rely on family networks or local moneylenders, who charge exorbitant interest rates and offer limited scalability. Banks, on the other hand, provide a structured, regulated environment that fosters trust and encourages long-term savings. This formalization not only protects depositors but also ensures that funds are allocated to high-impact projects, such as renewable energy initiatives or affordable housing, which drive sustainable development.

Persuasively, one could argue that the ability of banks to mobilize savings is a cornerstone of modern economic prosperity. Without this function, savings would remain fragmented and underutilized, stifling entrepreneurship and innovation. Take the example of post-World War II Europe, where the Marshall Plan relied heavily on banking systems to rebuild economies. By pooling resources and directing them toward reconstruction efforts, banks enabled rapid recovery and laid the foundation for decades of growth. Today, this principle remains relevant, particularly in emerging markets where access to capital is a critical bottleneck. Governments and policymakers must, therefore, prioritize strengthening banking systems to maximize the economic potential of savings.

In conclusion, the mobilization of savings through banks is a dynamic process that bridges the gap between savers and investors, fostering economic activities that benefit society at large. By understanding the mechanics, risks, and comparative advantages of this system, individuals and institutions can better appreciate its importance. Whether you’re a depositor, borrower, or policymaker, recognizing the transformative power of pooled savings can guide decisions that contribute to a more prosperous and equitable economy. Practical tips include diversifying savings across accounts to maximize interest earnings, supporting banks with strong community reinvestment records, and advocating for policies that enhance financial inclusion. In doing so, we all become active participants in the economic ecosystem that banks help sustain.

Are CTBC and China Bank the Same? Unraveling the Confusion

You may want to see also

Explore related products

$8.73 $19.99

![]()

Support Stability: Act as intermediaries, maintaining liquidity and preventing economic shocks

Banks serve as the backbone of economic stability by acting as intermediaries between savers and borrowers, ensuring that money flows efficiently through the system. This role is critical in maintaining liquidity, which is the lifeblood of any economy. Without sufficient liquidity, businesses cannot fund operations, consumers cannot make purchases, and economic activity grinds to a halt. By accepting deposits and extending loans, banks create a mechanism for funds to move from those who have surplus capital to those who need it, thereby keeping the economic wheels turning.

Consider the 2008 financial crisis, a stark example of what happens when this intermediary function fails. Banks, overwhelmed by toxic assets, froze lending, causing a liquidity crisis. Businesses couldn’t secure credit, consumers tightened spending, and the economy spiraled into recession. This illustrates the fragility of the system and the indispensable role banks play in preventing such shocks. When banks operate effectively, they act as shock absorbers, smoothing out economic fluctuations by ensuring that credit remains available even during uncertain times.

To achieve this stability, banks employ specific strategies. First, they diversify their lending portfolios to spread risk. For instance, a bank might lend to multiple sectors—manufacturing, real estate, and technology—rather than concentrating on one. This diversification ensures that a downturn in one sector doesn’t cripple the bank’s ability to lend. Second, banks maintain reserves, a portion of deposits held in liquid assets, to meet withdrawal demands and unexpected loan requests. Regulatory bodies often mandate a reserve requirement, such as 10% of deposits, to safeguard liquidity.

However, maintaining stability isn’t without challenges. Banks must balance risk and reward, as excessive lending can lead to defaults, while overly conservative practices can stifle growth. Central banks play a crucial role here by setting interest rates and providing liquidity support during crises. For example, during the COVID-19 pandemic, central banks worldwide injected trillions of dollars into the financial system to prevent a liquidity crunch. This intervention allowed banks to continue lending, supporting businesses and households through the crisis.

In practical terms, individuals and businesses can contribute to this stability by managing their finances responsibly. For businesses, maintaining a healthy debt-to-equity ratio—ideally below 2:1—reduces reliance on bank loans and minimizes default risk. For individuals, keeping an emergency fund equivalent to 3–6 months of expenses ensures they don’t withdraw savings abruptly, which could strain bank liquidity. By understanding and supporting the intermediary role of banks, everyone plays a part in preventing economic shocks and fostering stability.

Is the Deal or No Deal Banker Real? Unveiling the Truth

You may want to see also

Frequently asked questions

Banks act as intermediaries between savers and borrowers, facilitating the flow of money in the economy. They collect deposits from individuals and businesses and lend them out to others, supporting economic activities like investments, consumption, and growth.

Banks provide loans to businesses and individuals, enabling investments in projects, startups, and infrastructure. This stimulates economic activity, creates jobs, and fosters innovation, ultimately driving economic growth.

Banks help regulate the money supply through lending and deposit activities. By controlling credit availability, they influence inflation and economic stability, often in coordination with central banks.

Banks provide financing options like loans, credit lines, and mortgages to small businesses and entrepreneurs, helping them start, expand, or sustain their operations. This is crucial for job creation and economic diversification.

Banks ensure financial stability by safeguarding deposits, managing risks, and providing liquidity to the economy. They also adhere to regulatory standards to prevent financial crises and protect consumers.