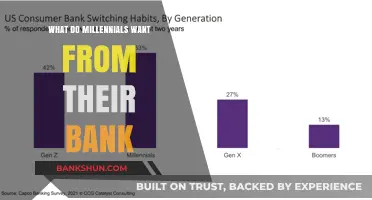

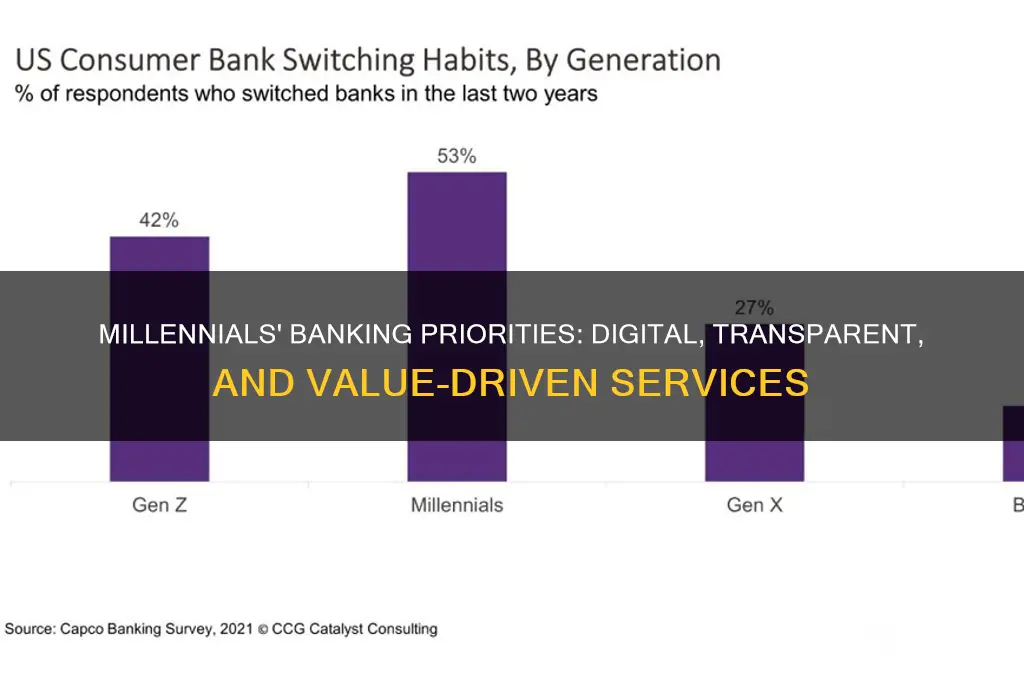

Millennials, often defined as those born between 1981 and 1996, represent a significant demographic in the banking sector, and their preferences are reshaping the industry. Unlike previous generations, millennials prioritize digital convenience, transparency, and personalized services when it comes to their financial institutions. They seek seamless mobile banking experiences, real-time transaction notifications, and user-friendly interfaces that allow them to manage their finances on the go. Additionally, millennials value banks that align with their social and environmental values, such as those offering sustainable investment options or supporting ethical practices. Low fees, accessible financial education, and tools for budgeting and saving are also high on their list of priorities. As this tech-savvy generation continues to gain financial influence, banks must adapt to meet their unique expectations to remain competitive in an increasingly digital world.

| Characteristics | Values |

|---|---|

| Digital-First Experience | Seamless mobile banking, user-friendly apps, and online account management |

| Low or No Fees | No monthly maintenance fees, free ATM access, and no overdraft charges |

| Transparency | Clear fee structures, straightforward terms, and no hidden costs |

| Personalized Services | Tailored financial advice, budgeting tools, and personalized offers |

| Sustainability & Social Responsibility | Ethical banking practices, ESG investments, and support for social causes |

| Fast & Secure Transactions | Instant payments, secure encryption, and fraud protection |

| Rewards & Cashback | Cashback on purchases, rewards programs, and loyalty incentives |

| Integration with Fintech | Compatibility with budgeting apps (e.g., Mint, YNAB) and payment platforms |

| Financial Education | Access to resources, webinars, and tools for improving financial literacy |

| 24/7 Customer Support | Round-the-clock assistance via chat, phone, or social media |

| Flexibility in Products | Customizable accounts, short-term loans, and flexible savings options |

| Global Accessibility | Low or no foreign transaction fees and multi-currency accounts |

| Innovative Features | AI-driven insights, voice banking, and gamified savings challenges |

| Community & Belonging | Banks that align with their values and foster a sense of community |

| Data Privacy | Strong data protection policies and control over personal information |

Explore related products

What You'll Learn

- Digital-first services: Seamless online/mobile banking with intuitive interfaces and 24/7 accessibility

- Transparent fees: Clear, straightforward fee structures with no hidden charges or surprises

- Personalized experiences: Tailored financial products and advice based on individual needs and goals

- Sustainable banking: Eco-friendly practices and investment options aligned with social responsibility

- Instant support: Real-time customer service via chat, phone, or AI-powered assistants

![]()

Digital-first services: Seamless online/mobile banking with intuitive interfaces and 24/7 accessibility

Millennials, now the largest generation in the workforce, have grown up with technology as an integral part of their lives. This digital nativity shapes their expectations of banking services, demanding seamless online and mobile experiences that mirror the convenience of their favorite apps.

For this tech-savvy cohort, clunky interfaces, limited functionality, and restricted access hours are deal-breakers. They crave banking that feels intuitive, accessible, and integrated into their digital lives.

Imagine a 28-year-old freelance designer, Sarah, managing her finances on the go. She needs to transfer funds to a client while waiting for her morning coffee, check her account balance during a lunch break, and set up automatic bill payments before heading to a networking event. A digital-first bank caters to Sarah's needs by offering a sleek mobile app with fingerprint login, instant transaction notifications, and budgeting tools that categorize her spending in real-time. This level of accessibility and control empowers her to manage her finances efficiently, fitting seamlessly into her busy lifestyle.

The key lies in creating interfaces that are not just functional but delightful. Think drag-and-drop budgeting tools, personalized financial insights presented in visually appealing dashboards, and chatbots offering instant support 24/7. Millennials value transparency and control, and digital-first banking provides this through real-time transaction updates, detailed spending breakdowns, and the ability to freeze cards instantly if needed.

However, digital-first doesn't mean abandoning human interaction entirely. Millennials appreciate the option to connect with a human representative when needed, whether through in-app messaging, video calls, or even AI-powered chatbots trained to handle complex queries. The goal is to strike a balance between the efficiency of digital solutions and the reassurance of human support.

By prioritizing seamless online and mobile banking with intuitive interfaces and 24/7 accessibility, banks can tap into the vast potential of the millennial market. This generation demands more than just financial services; they seek a banking experience that is as seamless, personalized, and tech-driven as the rest of their digital lives.

Black Tuesday's Impact: How Many Banks Collapsed in the Great Crash?

You may want to see also

Explore related products

![]()

Transparent fees: Clear, straightforward fee structures with no hidden charges or surprises

Millennials, often burdened by student loans and navigating a gig-based economy, are acutely sensitive to financial unpredictability. A 2022 survey by Bankrate found that 63% of millennials prioritize low or no fees when choosing a bank, outranking even interest rates on savings accounts. This preference isn’t just about saving money—it’s about trust. Hidden fees erode confidence in financial institutions, leaving millennials feeling manipulated rather than supported.

Consider the overdraft fee, a common pain point. Many banks charge $35 or more for overdrafts, a penalty that disproportionately affects younger adults living paycheck to paycheck. Transparent fee structures would clearly outline these charges, perhaps offering alternatives like real-time balance alerts or grace periods to avoid them. For instance, Chime, a digital bank popular with millennials, eliminates overdraft fees entirely by allowing transactions only when sufficient funds are available. This approach not only builds trust but also aligns with millennial values of fairness and simplicity.

To implement transparency effectively, banks should adopt a layered communication strategy. First, provide a concise fee summary during account opening, avoiding legalese. Second, integrate fee explanations into digital platforms, such as pop-up notifications when a fee-triggering action is about to occur. Third, offer annual fee reviews, breaking down all charges incurred over the year and suggesting ways to reduce them. For example, Ally Bank’s “No Fee” promise includes a detailed breakdown of potential fees on its website, even though it claims to avoid them—a proactive approach that educates customers.

However, transparency alone isn’t enough. Banks must also ensure fees are reasonable. A $5 monthly maintenance fee might be clear but still unjustifiable if the account offers minimal benefits. Millennials are quick to compare options, and platforms like NerdWallet make it easy to do so. Banks should benchmark their fees against competitors and justify any charges with tangible value, such as access to financial planning tools or cashback rewards.

Ultimately, transparent fees are a cornerstone of millennial-friendly banking. They signal respect for the customer’s time, intelligence, and financial well-being. By eliminating surprises and fostering clarity, banks can transform fees from a source of frustration into an opportunity to strengthen relationships. For millennials, this isn’t just a preference—it’s a prerequisite.

Does Webster Bank Offer Coin Counting Machines? A Quick Guide

You may want to see also

Explore related products

![]()

Personalized experiences: Tailored financial products and advice based on individual needs and goals

Millennials, often characterized by their tech-savviness and desire for individuality, are reshaping the banking industry by demanding personalized experiences that go beyond one-size-fits-all solutions. This generation, born between 1981 and 1996, seeks financial products and advice that align with their unique life stages, goals, and values. For instance, a 28-year-old freelancer saving for a down payment on a house has vastly different needs than a 35-year-old entrepreneur scaling their business. Banks that leverage data analytics and artificial intelligence to offer tailored solutions are more likely to win millennial loyalty.

Consider the example of budgeting apps integrated into banking platforms. Instead of generic spending categories, these tools can analyze individual transaction patterns to provide customized insights. For a millennial earning $50,000 annually and aiming to save 20% of their income, the app could suggest reducing dining-out expenses by 15% or automating monthly transfers to a high-yield savings account. Such specificity not only fosters trust but also empowers users to make informed financial decisions. Banks that fail to offer this level of personalization risk being perceived as outdated or indifferent to their customers’ unique circumstances.

However, personalization must be balanced with transparency and control. Millennials are acutely aware of data privacy concerns and are more likely to engage with banks that clearly explain how their data is used to tailor recommendations. For example, a bank might notify a customer that their spending habits indicate a high interest in travel and then suggest a credit card with no foreign transaction fees and airline rewards. By providing the rationale behind the recommendation, the bank builds credibility and ensures the customer feels in charge of their financial journey.

To implement personalized experiences effectively, banks should adopt a multi-step approach. First, gather comprehensive customer data through digital interactions, account activity, and self-reported goals. Second, use advanced algorithms to identify patterns and predict needs—for instance, detecting that a millennial customer has recently started investing and recommending a robo-advisor with low fees. Third, deliver tailored solutions through omnichannel touchpoints, whether via mobile apps, email, or in-branch consultations. Finally, continuously refine offerings based on customer feedback and evolving preferences.

The takeaway is clear: millennials want banks that act as proactive financial partners, not just service providers. By offering personalized products and advice, banks can differentiate themselves in a crowded market and build long-term relationships with this influential demographic. For example, a millennial planning for retirement might appreciate a bank that automatically adjusts their investment portfolio based on their risk tolerance and time horizon. Such proactive measures not only enhance customer satisfaction but also position banks as indispensable allies in achieving financial success.

Does M&T Bank Offer Overdraft Protection? What You Need to Know

You may want to see also

Explore related products

![]()

Sustainable banking: Eco-friendly practices and investment options aligned with social responsibility

Millennials, now the largest generation in the workforce, are reshaping the banking industry by demanding more than just financial services—they want institutions that reflect their values. A 2021 Deloitte survey revealed that 77% of millennials are more likely to bank with institutions that prioritize sustainability. This isn’t just a trend; it’s a fundamental shift in how this demographic interacts with money. Sustainable banking, which integrates eco-friendly practices and socially responsible investment options, has emerged as a critical differentiator for banks aiming to attract and retain millennial customers.

Consider the practical steps banks can take to align with millennial expectations. First, adopt eco-friendly operational practices, such as transitioning to renewable energy for branches, reducing paper usage through digital banking, and implementing carbon offset programs. For instance, ING Bank’s commitment to becoming carbon neutral by 2020 included investing in wind energy projects and offering green mortgages for energy-efficient homes. Second, banks must provide transparent investment options that exclude harmful industries like fossil fuels, tobacco, and weapons. ESG (Environmental, Social, and Governance) funds have seen explosive growth, with assets under management surpassing $35 trillion globally in 2023, according to Morningstar. Millennials are not just investing for returns; they’re investing for impact.

However, banks must tread carefully to avoid greenwashing—the practice of misleading consumers about a product’s environmental benefits. A 2022 report by the Competition and Markets Authority found that 40% of green claims made by businesses were misleading. To build trust, banks should provide clear, verifiable data on the sustainability impact of their products. For example, Triodos Bank publishes an annual Transparency Report detailing how every euro deposited is allocated to sustainable projects, from organic farming to renewable energy. This level of transparency resonates with millennials, who value authenticity and accountability.

The takeaway is clear: sustainable banking isn’t a niche offering—it’s a necessity for banks targeting millennials. By embedding eco-friendly practices into operations and offering socially responsible investment options, banks can differentiate themselves in a crowded market. Millennials are willing to switch banks for better sustainability offerings, and institutions that fail to adapt risk losing this influential demographic. The question isn’t whether banks should embrace sustainability, but how quickly they can do so to meet the demands of a generation that wields both financial power and a strong moral compass.

Seed Banks: Safeguarding Genetic Diversity for Future Generations

You may want to see also

Explore related products

![PEWTER TRAIN BANK - PEWTER TRAIN MONEY BANK [Kitchen]](https://m.media-amazon.com/images/I/814pJb8K-4L._AC_UL320_.jpg)

![]()

Instant support: Real-time customer service via chat, phone, or AI-powered assistants

Millennials, often dubbed the digital-first generation, expect their banks to mirror the instantaneity of their favorite apps. When it comes to customer support, they don’t want to wait on hold or sift through FAQs. They want answers now—whether it’s resolving a transaction issue at 2 a.m. or clarifying a fee during their lunch break. Real-time support via chat, phone, or AI-powered assistants isn’t a luxury for this demographic; it’s a baseline requirement. Banks that fail to deliver this level of immediacy risk losing millennial customers to fintech competitors like Chime or Revolut, which have built their models around 24/7 accessibility.

Consider the mechanics of implementing this: AI-powered chatbots, for instance, can handle 80% of routine inquiries, from balance checks to transaction disputes, freeing up human agents for complex issues. However, the AI must be sophisticated enough to understand natural language and context—millennials are quick to abandon clunky, unresponsive bots. For phone support, banks should aim for a 30-second or less wait time, backed by well-trained agents who can resolve issues in a single call. Chat support, meanwhile, should integrate seamlessly into mobile banking apps, with features like screen sharing for troubleshooting. The goal is to make the experience frictionless, as if the customer is texting a friend, not a corporation.

A cautionary note: while millennials value speed, they also prioritize accuracy and empathy. A bot that provides incorrect information or a rushed agent who misses key details can do more harm than good. Banks must strike a balance between efficiency and effectiveness, ensuring that real-time support doesn’t come at the expense of quality. Regularly audit AI responses and monitor customer satisfaction scores to identify gaps. For human agents, invest in ongoing training that emphasizes active listening and problem-solving skills. Millennials can spot a scripted response from a mile away—authenticity matters.

The takeaway is clear: instant support isn’t just about being available; it’s about being useful. Millennials want to feel empowered, not frustrated, when they reach out to their bank. By combining AI efficiency with human empathy, banks can create a support system that meets this generation’s high expectations. Start by mapping out common pain points and designing solutions that address them in real time. For example, if overdraft fees are a frequent concern, integrate a chatbot feature that alerts customers before a transaction pushes them into the red. Small, proactive touches like these can turn a transactional interaction into a loyalty-building moment.

Finally, measure success not just by response times but by outcomes. Did the customer’s issue get resolved? Did they leave the interaction feeling more confident in their financial decisions? Millennials are more likely to stay with a bank that consistently delivers on these fronts. In a world where switching banks is as easy as downloading an app, instant, effective support isn’t just a feature—it’s a competitive edge.

Step-by-Step Guide to Activating Nedbank Internet Banking Easily

You may want to see also

Frequently asked questions

Millennials prioritize digital convenience, low fees, transparency, and personalized financial tools when choosing a bank.

Yes, millennials overwhelmingly prefer mobile banking for its accessibility, ease of use, and ability to manage finances on-the-go.

Yes, many millennials seek banks that offer sustainable or socially responsible financial products, aligning with their values.

Millennials value banks that provide financial education resources, such as budgeting tools, investment advice, and debt management tips.

While millennials appreciate the innovation of fintech, they still value the security and stability of traditional banks, often using a combination of both.